US Market Open: Bitcoin pushes past 100k & USD remains on the backfoot

05 Dec 2024, 12:05 by Newsquawk Desk

- European bourses opened flat but started grinding higher shortly after the open despite relatively quiet newsflow; France's CAC 40 shrugged off the vote of no confidence which played out as expected.

- USD remains on the backfoot vs. peers following yesterday's ISM-induced move in yields; EUR on a firmer footing vs. the USD with not much in the way of follow-through selling from the collapse of the French government.

- Crude futures holding a modest upward bias after selling off in the US afternoon on Wednesday, which was later attributed to a bank offloading a large volume of US oil futures contracts ahead of today's OPEC+ meeting.

- Bitcoin climbed above the psychological USD 100k level for the first time ever and continued to advance with prices underpinned after US President-elect Trump picked crypto-backer Paul Atkins to lead the SEC.

- Looking ahead, highlights include US Challenger Layoffs & Weekly Jobless Claims, OPEC+ Meeting, Speakers including Fed’s Barkin, BoE’s Greene & ECB’s Patsalides, Supply from US.

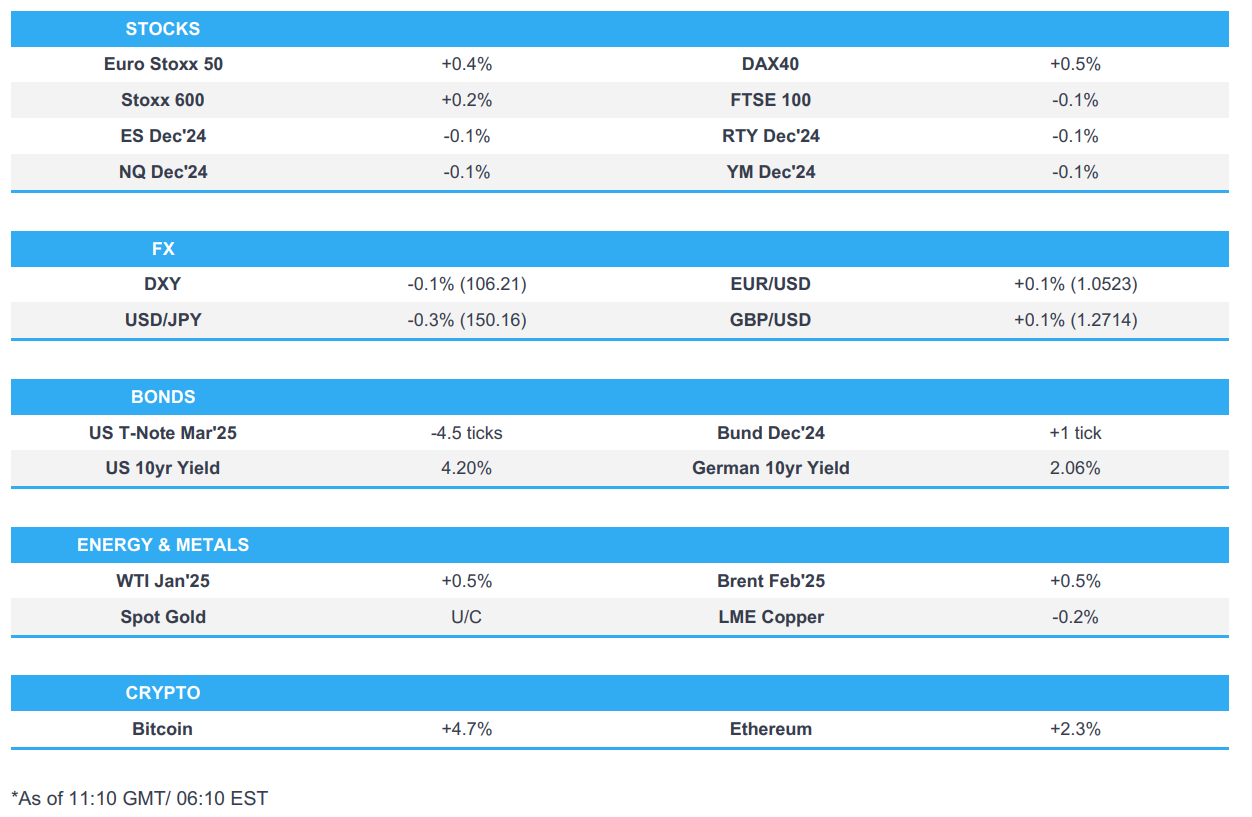

SNAPSHOT

EUROPEAN TRADE

EQUITIES

- European bourses opened flat but started grinding higher shortly after the open despite relatively quiet newsflow but potentially as some of the optimism potentially emanating from the gains on Wall Street.

- European sectors kicked off the session with a mild positive bias which later expanded as sentiment continued to improve shortly after the cash open.

- CAC 40 shrugged off the vote of no confidence which played out as expected, while President Macron is reported to be looking to announce a replacement before Saturday as opposed to taking the country to the polls.

- In terms of US equity futures, mild downward bias seen in the ES and NQ after yesterday's session on Wall Street in which US stocks gained and the major indices printed fresh record highs with the Nasdaq leading advances amid outperformance in Tech and Consumer Discretionary and Communication names.

- Foxconn (2317 TT) November revenue +3.47% Y/Y (prev. +8.59% Y/Y in October); Foxconn says Q4 operations are expected to show significant growth on a Q/Q and a Y/Y basis.

- EU antitrust Chief says Google (GOOG) split still on the table, according to Bloomberg.

- TSMC (TSM) and Nvidia (NVDA) are in talks on producing Blackwell chips at TSMC's Arizona plant. according to Reuters sources

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD remains on the backfoot vs. peers following yesterday's ISM-induced move in yields. Commentary from Fed Chair Powell who noted that the Fed can afford to be cautious in finding neutral failed to cause a stir in markets. Today's US Calendar is a lighter one with US challenger layoffs and Fed's Barkin on deck. Tomorrow's NFP release looms large. DXY briefly slipped below yesterday's 106.09 low. The next target comes via the 106 mark; Monday's low sits @ 105.78.

- EUR on a firmer footing vs. the USD with not much in the way of follow-through selling from the collapse of the French government (which was widely expected). Focus remains on the next steps and who (if anyone) Macron can appoint as PM. The main kicker is that the 2024 budget will likely be rolled into 2025. From a broader Eurozone perspective, pricing of a 50bps move at next week's ECB meeting continues to be unwound with odds of a 25bps move now @ 86%. EUR/USD has made some progress on a 1.05 handle with the next upside target coming via the 21DMA @ 1.0561.

- JPY is one of the better performers vs. the USD on account of remarks from BoJ dove Nakamura who stated that he is not against a rate hike. Pricing around the December announcement remains particularly choppy. However, odds of an unchanged rate sit @ 62% vs. 42% seen at the start of the week. USD/JPY is currently tucked within Friday's 149.51-151.22 range.

- GBP firmer vs. the USD for a third session in a row after shrugging off a dovish headline from the FT yesterday about BoE Governor Bailey's view on the rate path (which appeared to in the end be more related to market pricing than his own view). MPC member Greene is due to speak later today. The BoE's DMP (on which it places great weight) saw no follow-through into GBP. Cable has gained a firmer footing on a 1.27 handle and is now eyeing last Friday's high @ 1.2749.

- Antipodeans are both firmer vs. the USD with slight outperformance in NZD/USD despite a lack of fresh NZ-specific drivers. NZD/USD is currently caged within yesterday's 0.5829-0.5884 range and yet to approach the 0.59 mark. AUD/USD failed to garner much additional support from an improvement in Australian trade and household spending data. AUD/USD currently sits towards the middle of yesterday's 0.6399-0.6488 range.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Mar'25 USTs are seeing a modest pullback from yesterday's ISM-induced rally in US paper. The release further cemented expectations for the Fed to cut rates later this month with odds of such a move @ 73% before likely pausing in January. Comments from Fed Chair Powell yesterday did little to stand in the way of this pricing. A dovish outturn for NFP tomorrow could seal the deal on the FOMC.

- French paper remarkably calm after yesterday's collapse of the French government. The outcome was as expected and attention now turns towards who, if anyone Macron can appoint as PM (there is currently no obvious replacement candidate). The main kicker is that the 2024 budget will likely be rolled into 2025 and policy will likely end up being less restrictive than initially thought. In response to recent events, Moody's has cautioned that the no confidence vote is "credit negative". The GE/FR spread has narrowed to just below 81bps having peaked just shy of 89bps on Monday with last week’s 12yr high at 90bps just above.

- Dec'24 Bunds are currently within yesterday's 134.66-135.28 trading band with the corresponding 10yr yield around the 2.08% mark vs. yesterday's 2.10% peak.

- Mar'25 Gilts are marginally softer and in-fitting with price action in global peers. From a UK-specific standpoint, yesterday's FT headline on Governor Bailey caused a stir, however, desks are broadly of the view that his comments over four rate hikes next year were taken out of context as he was referring more to market pricing than his own view. Today's DMP release saw expectations for CPI inflation a year ahead rose from 2.6% to 2.7% in the three months to November, expected year-ahead wage growth dropped by 0.1ppt to 4.0%; BoE pricing was little changed.

- France sold EUR 5bln vs exp. EUR 3-5bln 4.0% 2038, 0.5% 2040, 1.5% 2050, 0.5% 2072 OAT

- Spain sold EUR 2.447bln vs exp. EUR 2-3bln 2.70% 2030 & 3.45% 2034 Bono

- Click for a detailed summary

COMMODITIES

- Crude futures holding a modest upward bias after selling off in the US afternoon on Wednesday, which was later attributed to a bank offloading a large volume of US oil futures contracts ahead of today's OPEC+ meeting. Sources today, so far, have failed to move prices.

- Precious metals trade with a softer bias despite the weaker Dollar with traders cautious as they look ahead to the US jobs report tomorrow ahead of the US CPI data due next week.

- Copper trades higher this morning with prices supported by the softer Dollar intraday coupled with the positive risk bias in Europe. Traders look ahead to next week's Central Economic Work Conference which was hoped to provide fiscal stimulus, although Chinese press played this down in overnight reports.

- Russian oil producer Rosneft invested USD 20bln into India, according to an Indian Government statement citing Russian President Putin. Russia are reportedly ready to set up manufacturing operations in India.

- China's Ministry of Commerce expresses strong concern over the EU's plans to impose duties on Chinese titanium dioxide in 2025. China hopes the EU will conduct its investigation in line with WTO rules and avoid abusing trade remedies. Says it will firmly safeguard the legitimate rights and interests of Chinese enterprises.

- OPEC+ has a deal in principle to delay output hike, according to delegates cited by Bloomberg; OPEC+ still discussing duration of delay, with three months in focus.

- Several OPEC+ sources suggested a delay of output cuts for three months is the most likely outcome, while others have said a longer period is possible, according to Reuters sources.

- OPEC+ voluntary cuts are expected to be pushed back by 3 months and then the group collective cut is expected to be extended until the end of 2026, according to Energy Intel's Bakr.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Retail Sales YY (Oct) 1.9% vs. Exp. 1.7% (Prev. 2.9%, Rev. 3.0%)

- EU Retail Sales MM (Oct) -0.5% vs. Exp. -0.3% (Prev. 0.5%)

- EU HCOB Construction PMI (Nov) 42.7 (Prev. 43.0)

- German HCOB Construction PMI (Nov) 38.0 (Prev. 40.2)

- French HCOB Construction PMI (Nov) 43.7 (Prev. 42.2)

- Italian HCOB Construction PMI (Nov) 48.5 (Prev. 48.2)

- Swiss Unemployment Rate Adj (Nov) 2.6% vs. Exp. 2.7% (Prev. 2.6%)

- Swedish CPIF Flash YY (Nov) 1.9% vs. Exp. 1.9% (Prev. 1.5%); CPIF MM (Nov) 0.5% (Prev. 0.5%)

NOTABLE EUROPEAN HEADLINES

- BoE Monthly Decision Maker Panel data November 2024: Year-ahead own-price inflation was expected to be 3.7% in the three months to November vs. 3.5% in October. Expectations for CPI inflation a year ahead rose from 2.6% to 2.7% in the three months to November.Three-year ahead CPI inflation expectations was unchanged at 2.6%. Firms reported that annual wage growth was 5.5% in the three months to November vs. 5.6% in October. Expected year-ahead wage growth dropped by 0.1ppt to 4.0% on a three-month moving-average basis in November

- French President Macron will address the nation on Thursday evening in a televised speech at 18:00 GMT, according to Sky News.

- French Far-right leader Marine Le Pen said they have some requirements for backing the next PM and will contribute to crafting a budget, while she is not calling for President Marcon's resignation but noted that the pressure is piling up.

- Istat cut Italy's 2024 GDP growth forecast to 0.5% (prev. 1.0% seen in June); cut 2025 GDP growth to 0.8% (prev. 1.1%).

- Moody's said French no-confidence vote is "Credit Negative".

- S&P said the fall of the French Govt. leaves France without a clear path towards reducing its budget.

NOTABLE US HEADLINES

- Fed's Daly (2024 voter) said they do not need to be urgent and need to carefully calibrate policy, while she will wait until the December meeting to make her decision. Daly also stated that inflation is still the number one challenge people are facing and there's a lot more work to deliver on 2% inflation and durable expansion.

- US President-elect Trump picked Paul Atkins for SEC Chair, while he picked Faulkender for Deputy US Treasury Secretary and Gail Slater as assistant AG for the antitrust division at the Department of Justice. Trump also named former Senator Kelly Loeffler to serve as Administrator of the Small Business Administration and Frank Bisignano to serve as the Commissioner of the Social Security Administration, while he named former Congressman Billy Long of Missouri to serve as the Commissioner of the Internal Revenue Service.

GEOPOLITICS

MIDDLE EAST

- Israel's cabinet will meet today to discuss the proposal for an exchange deal with Hamas, according to Israeli Media.

- Russia reportedly fired missiles from its bases in Tartus, targeting Syrian rebels near Hama, according to a journalist via X.

CRYPTO

- Bitcoin climbed above the psychological USD 100k level for the first time ever and continued to advance with prices underpinned after US President-elect Trump picked crypto-backer Paul Atkins to lead the SEC.

APAC TRADE

- APAC stocks traded mixed and partially sustained the momentum from the fresh record levels on Wall St where tech led the advances with the help of earnings releases and softer yields following weak ISM Services data.

- ASX 200 eked slight gains with tech stocks taking inspiration from the outperformance stateside, while there was also an improvement in the latest trade and household spending data.

- Nikkei 225 gapped higher at the open but then gave back some of the initial spoils amid a choppy currency, while there was some intraday support seen after cautious rhetoric from BoJ's Nakamura although the momentum waned shortly after.

- Hang Seng and Shanghai Comp were mixed with sentiment clouded after the PBoC's operations resulted in another net liquidity drain and with a recent article in Chinese state media downplaying the pursuit of fast growth ahead of next week's Central Economic Work Conference.

NOTABLE ASIA-PAC HEADLINES

- China Foreign Ministry has decided to impose sanctions on 13 US military firms and executives from December 5th, it announced. Some of the firms under sanctions include Teledyne Brown Engineering, Brinc Drones, Shield AI.

- South Korean army chief offered to resign, according to Yonhap

- Chinese state media warned against blindly pursuing faster growth and signalled more focus on supporting consumption in a flurry of articles ahead of the Central Economic Work Conference, according to Bloomberg.

- BoJ board member Nakamura said he is not confident about the sustainability of wage growth, while he added they are at a critical phase and must check many data and cautiously adjust the degree of monetary support in accordance with an improvement in the economy. Nakamura said that he sees a chance inflation may miss 2% from fiscal 2025 onward and noted that Japan's economy has yet to move on course for a stable growth path. Furthermore, he said structural changes in Japan's economy are required for inflation to stably hit 2% which will take a significant amount of time but also stated the adjustment of easy monetary policy will proceed gradually as the economy is expected to head toward a growth path. BoJ Board Member Nakamura later commented during a press conference that they will decide policy by examining data and he is not against a rate hike but believes it should be data-dependent.

- Japanese PM Ishiba said the government should mull what's an appropriate FX level and there are no plans to change the government-BoJ joint stance.

- South Korean ruling party leader Han said the party will try to stop the impeachment motion from passing parliament but demanded that President Yoon leave the party, according to Yonhap. Furthermore, the opposition party said it plans to vote to impeach President Yoon at 7pm local time on Saturday.

DATA RECAP

- Australian Balance on Goods (Oct) 5,953M vs. Exp. 4,550M (Prev. 4,609M)

- Australian Goods/Services Exports (Oct) 3.6% (Prev. -4.3%)

- Australian Goods/Services Imports (Oct) 0.1% (Prev. -3.1%)

- Australian Household Spending MM (Oct) 0.8% vs Exp. 0.3% (Prev. -0.1%)

- Australian Household Spending YY (Oct) 2.8% vs Exp. 2.2% (Prev. 1.3%)