Europe Market Open: APAC traded mixed with cautiousness ahead of US jobs data

06 Dec 2024, 07:00 by Newsquawk Desk

- APAC stocks were mixed with some cautiousness in the region after the weak lead from Wall St and ahead of the key US jobs data.

- European equity futures are indicative of a negative cash open with the Euro Stoxx 50 future -0.3% after the cash market closed higher by 0.7% on Thursday.

- DXY is a touch firmer but still on a 105 handle, antipodeans marginally lag, USD/JPY lingers around 150.

- Bunds have nursed some of the prior day's declines, crude futures are lacklustre post-OPEC+.

- Looking ahead, highlights include German Industrial Output, Canadian jobs data, US jobs report & Univ. of Michigan, Fed’s Bowman, Goolsbee, Hammack & Daly.

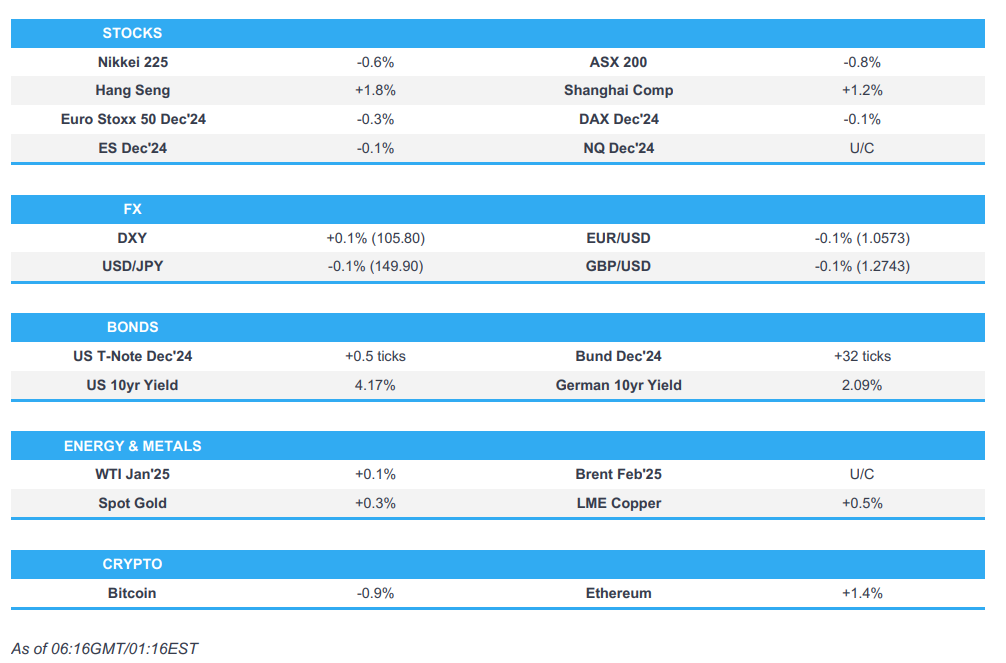

SNAPSHOT

US TRADE

EQUITIES

- US stocks were choppy and ultimately finished the session mildly lower with the small-cap Russell 2000 continuing its underperformance amid little in the way of macro drivers although the data releases showed Initial Jobless Claims disappointed and there were also higher Challenger Layoffs ahead of the looming NFP report on Friday. Sector-wise, upside was seen in Consumer Discretionary, Energy, Utilities, Financials and Staples but Materials, Healthcare and Industrials were pressured, while crypto stocks benefitted at the open following BTC hitting the 100k milestone, peaking at 103k, although the gains were erased as BTC pared the majority of the upside.

- SPX -0.19% at 6,075, NDX -0.31% at 21,425, DJIA -0.55% at 44,766, RUT -1.25% at 2,396.

- Click here for a detailed summary.

NOTABLE HEADLINES

- US President-elect Trump named David O. Sacks to be the “White House A.I. & Crypto Czar”, while he also named former Senator David Perdue to be Ambassador to China, Rodney S. Scott as Commissioner of United States Customs and Border Protection, and Caleb Vitello as Acting Director of Immigration and Customs Enforcement.

APAC TRADE

EQUITIES

- APAC stocks were mixed with some cautiousness in the region after the weak lead from Wall St and ahead of the key US jobs data.

- ASX 200 was dragged lower by early underperformance in tech and healthcare, while gold miners also suffered after initial declines in the precious metal.

- Nikkei 225 was the laggard and briefly fell beneath the 39,000 level despite encouraging Household Spending data.

- Hang Seng and Shanghai Comp were buoyed despite the lack of any major fresh catalysts heading into next week's trade and inflation data releases, as well as the Central Economic Work Conference where Chinese leaders are said to discuss economic growth and stimulus.

- US equity futures (ES -0.1%) traded uneventfully with demand constrained ahead of the key US jobs data.

- European equity futures are indicative of a negative cash open with the Euro Stoxx 50 future -0.3% after the cash market closed higher by 0.7% on Thursday.

FX

- DXY regained some composure after weakening against its peers yesterday with the greenback not helped by the higher-than-expected Initial Jobless Claims and increase in Challenger Layoffs data, while trade is rangebound overnight as the attention now shifts to NFP jobs data and with several Fed speakers also scheduled.

- EUR/USD slightly eased from this week's peak after gaining against the dollar but with trade confined beneath the 1.0600 level amid French political uncertainty.

- GBP/USD took a breather following its gradual advances and loitered around 1.2750 amid a lack of notable catalysts.

- USD/JPY traded indecisively on both sides of the 150.00 level following better-than-expected Household Spending data and in-line Labour Cash Earnings.

- Antipodeans retreated amid the cautious risk appetite and early pressure in commodity prices, while Standard Chartered suggested the RBA could have a dovish surprise although the latest Reuters poll showed unanimous expectation for the central bank to keep rates on hold at next week's meeting.

- PBoC set USD/CNY mid-point at 7.1848 vs exp. 7.2396 (prev. 7.1879)

FIXED INCOME

- 10yr UST futures traded sideways with participants lacking commitment ahead of the key US jobs data.

- Bund futures nursed some of the prior day's declines after slipping amid reports that EU nations are discussing a EUR 500bln joint fund for common defence projects and arms procurement and will tap the bond market ahead of Trump's return to the White House.

- 10yr JGB futures gradually edged higher amid the weakness in Japanese stocks but with gains in JGBs capped after better-than-expected Japanese Household Spending data and as the question remains on whether the BoJ will resume its rate hikes this month.

COMMODITIES

- Crude futures were lacklustre after the prior day's choppy performance amid the deluge of OPEC+ updates and despite the group postponing the start of planned output hikes to April 2025 and extended production cuts for OPEC and non-OPEC participating countries until 31st Dec 2026.

- UAE's ADNOC set January Murban crude OSP at USD 72.81/bbl.

- Qatar set January Marine crude and Land crude OSP at Oman/Dubai plus USD 0.15/bbl.

- Spot gold initially retreated in tandem with the declines seen in silver as Chinese commodities got underway but then recovered losses and more.

- Copper futures swung between gains and losses amid the mixed risk appetite in Asia but eventually gained amid the constructive mood in its largest buyer.

CRYPTO

- Bitcoin gradually edged higher overnight and reclaimed the USD 98,000 level after yesterday's pullback from a record high north of USD 103,000.

NOTABLE ASIA-PAC HEADLINES

- RBI kept the Repurchase Rate unchanged at 6.50%, as expected, while it maintained its neutral stance with the rate decision made by 4 out of 6 voting in favour of a hold and the policy stance vote was unanimous. However, RBI Governor Das later announced a surprise cut to the Cash Reserve Ratio by 50bps to 4.00% which will take effect in two tranches of 25bps each on December 14th and December 28th which will infuse liquidity of INR 1.16tln. Das said price stability is a mandate given to them and growth is also very important, while he noted the last mile of disinflation is prolonged and recent growth slowdown will lead to downward revision for full-year growth. Das acknowledged that inflation crossed the upper band and food inflation pressures will linger with food prices to start easing only in Q4, while headline inflation is likely to be elevated in Q3 and he noted a status quo in this policy is appropriate and essential. Das said the near-term inflation and growth outlook has turned somewhat adverse, while India's FY25 real GDP growth forecast was cut to 6.6% versus 7.2% previously and the FY25 CPI inflation forecast was raised to 4.8% versus 4.5% previously. Das also announced to introduce a new benchmark called the secured overnight rupee rate and said in order to attract more capital inflows, to increase interest rate ceilings on FCNR-B deposits.

- South Korean ruling party leader Han said President Yoon needs to be suspended from his office ASAP and that Yoon ordered to arrest prominent politicians on the grounds they are anti-state forces. It was also reported that South Korea's main opposition party said lawmakers were on high alert after many reports of another martial law declaration, although the South Korean Joint Chiefs of Staff later said there is no need to worry about a second martial law and the special warfare commander also said he would refuse should another martial law order come.

DATA RECAP

- Japanese All Household Spending MM (Oct) 2.9% vs. Exp. 0.4% (Prev. -1.3%)

- Japanese All Household Spending YY (Oct) -1.3% vs. Exp. -2.6% (Prev. -1.1%)

- Japanese Overall Labour Cash Earnings (Oct) 2.6% vs. Exp. 2.6% (Prev. 2.8%)

GEOPOLITICS

MIDDLE EAST

- Israeli intelligence officials have been startled by a faster-than-expected collapse of the Syrian army's defence lines, according to Axios.

- Russian Foreign Minister Lavrov said they are very worried after what happened in Syria, while he spoke with his Turkish and Iranian counterparts and they agreed to meet this week, according to Al Jazeera

RUSSIA-UKRAINE

- White House stated regarding National Security Advisor Sullivan's meeting with Ukrainian officials that Sullivan focused the discussion on the President’s theory of the case to improve Ukraine’s position in its war against Russia, while it was stated that Ukraine’s position in this war will improve relative to Russia's as we enter into 2025 and will allow Ukraine to enter any future negotiating process from a position of strength.

- Russia's Foreign Minister Lavrov said the use of hypersonic missiles in Ukraine means the West must understand that Russia is ready to use anything to stop notions of inflicting a strategic defeat on Moscow, while he added it is a mistake for anyone in the West to suggest that Russia has no red lines. It was separately reported that the Foreign Minister said Russia sees no reason why Moscow and Washington should not cooperate for the sake of the world.

OTHER

- Taiwan's President Lai said he hopes China does not take any unilateral actions and noted that more Chinese military drills won't win respect from any other countries in the region, while he added that authoritarian countries should not see Taiwan's engagement with other countries as a provocation and hopes China returns to rules-based international order. Furthermore, he said Taiwan's people cannot accept China's military operating around Taiwan, as well as noted that peace is priceless and there’s no winner in a war but also stated they cannot have any illusions about peace and must continue to strengthen defences.

- Armed forces from Japan, Philippines, and US conducted "multilateral maritime cooperative activity" within the Philippines’ exclusive economic zone.

EU/UK

NOTABLE HEADLINES

- BoE's Greene said UK services inflation has remained stubbornly high, underpinned by wage growth and the supply side of the UK economy is weak.

- ECB seeks to speed up approvals for significant risk transfers, according to Bloomberg.