US Market Open: European equities tilt lower, USD gains & AUD lags after RBA's dovish hold

10 Dec 2024, 11:03 by Newsquawk Desk

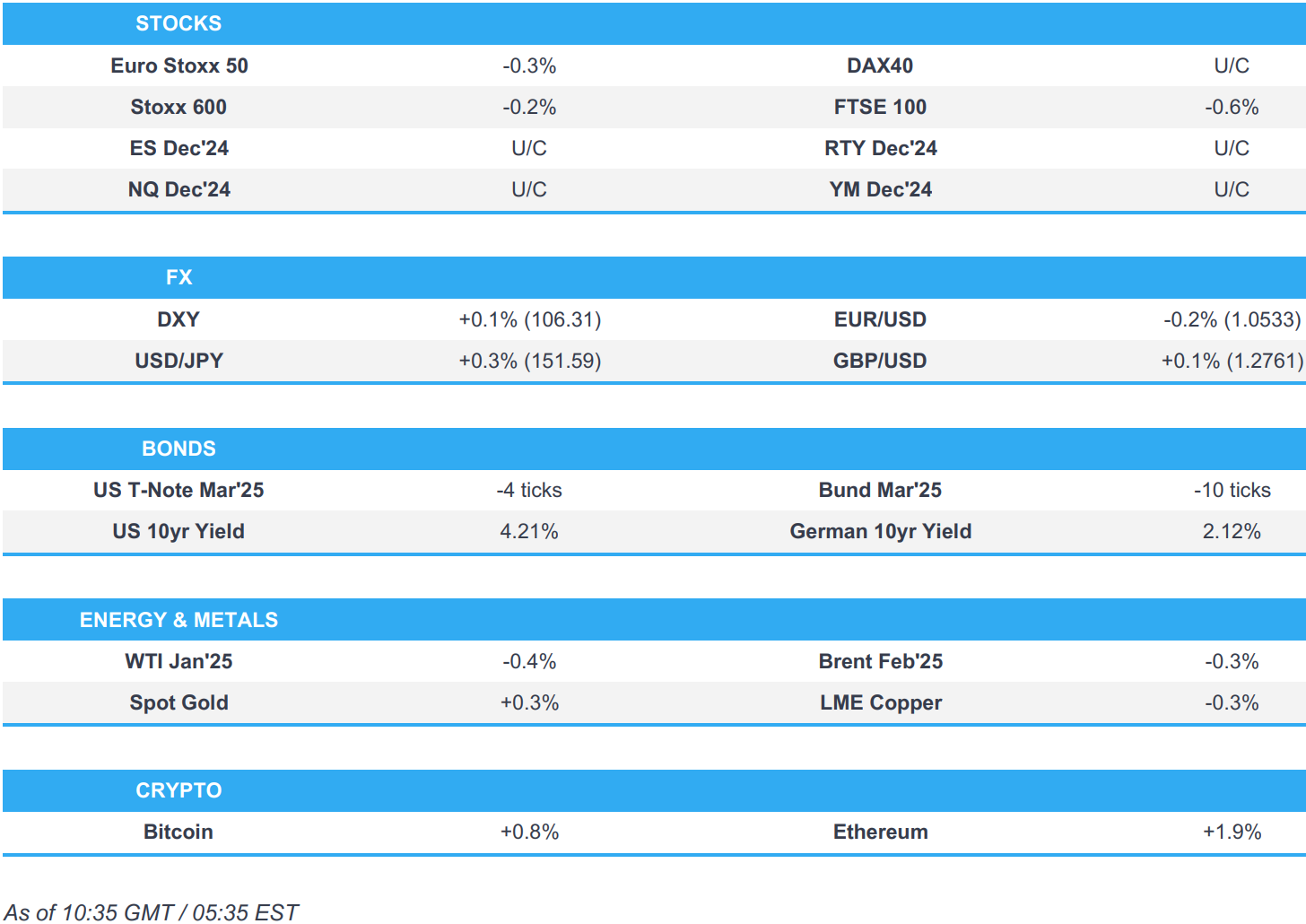

- European bourses are mostly on the backfoot; US futures trade indecisively around the unchanged mark.

- USD outmuscles peers, AUD lags after the RBA delivered a dovish hold.

- Choppy trade for European paper, US awaits 3yr supply.

- Crude edges slightly lower and base metals pare back recent strength.

- Looking ahead, US Unit Labor Costs Revision, EIA STEO, Supply from US.

EUROPEAN TRADE

EQUITIES

- European bourses began the session entirely in the red and have continued to traverse the bottom end of today’s range throughout the morning. The pressure is seemingly a paring back of the prior day’s upside and as traders react to the poor performance in Wall St. in the prior session.

- European sectors hold a strong negative bias, in-fitting with the pressure seen across the complex. There are only a handful of sectors in positive territory, and with the breadth to upside marginal; Healthcare incrementally tops the pile, followed closely by Autos and Travel & Leisure. And in a turn of fortunes from the prior day, Basic Resources and Consumer Products both give back some of the strength seen on Monday.

- US equity futures have traded on either side of the unchanged mark, but have been edging higher in recent trade.

- White House says the Commerce Department has made a > USD 6.1bln investment in Micron (MU).

- Oracle (ORCL) Q2 adj. EPS 1.47 (exp. 1.48), revenue USD 14.1bln (exp. 14.12bln). Sees Q3 EPS between 1.50-1.54 (exp. 1.57), sees Q3 revenue growth between +9-11%, sees cloud revenue growth between +25-27%. Guides FY25 revenue in the double-digits, cloud revenue projected at USD 25bln.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is up for a third consecutive session and has been growing in strength throughout trade. From a macro perspective, markets are currently in waiting mode ahead of tomorrow's CPI report which is expected to see a +0.3% M/M outturn for core CPI. DXY has gained a firmer footing on a 106 handle with a current session high at 106.41.

- EUR is a touch softer vs. the USD with not a great deal in the way of fresh macro drivers for the Eurozone. EUR/USD has slipped below yesterday's 1.0532 low with focus on a potential test of 1.05.

- JPY is extending on yesterday's losses vs. the USD with USD/JPY advancing further on a 151 handle. Fresh JPY drivers remain light in the run-up to the BoJ's December meeting with odds of a 25bps hike now at 28% vs. 42% seen at the start of last week. The next upside targets come via the 28th November high at 151.95 and then the 200DMA at 151.98.

- GBP is trivially firmer vs. the USD as UK macro drivers remain light. For now, Cable is tucked within a 1.2736-65 range.

- AUD is the laggard across the majors post-RBA. The central bank maintained its Cash Rate at 4.35% as widely expected, but struck a dovish tone as it expressed confidence that inflation is moving sustainably towards the target. NZD/USD is lower but holding above Monday's 0.5804 trough.

- PBoC set USD/CNY mid-point at 7.1876 vs exp. 7.2806 (prev. 7.1870)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are incrementally extending on Monday's losses following a bout of selling pressure in early European trade. Data focus will ultimately be on Wednesday's inflation report, but ahead of that the US 3yr auction later today. The Mar'25 UST contract is below yesterday's 111.04 low with the next target coming via Friday's trough at 110.28+.

- A particularly choppy morning for German paper with the Mar'25 Bund contract continuing to oscillate around the 136 mark. French paper is marginally outpacing its German counterpart with the DE/FR spread narrowing to 74bps vs. yesterday's opening levels of 76bps but wider than Friday's 72.4bps trough.

- Gilts are a touch lower with UK paper having moved broadly sideways in recent sessions and as UK-specific updates remain light. Mar'25 Gilt is back below the 96.00 mark with a session low @ 95.42, whilst the corresponding 10yr yield briefly rose above 4.3% for the first time since November 28th.

- UK sells GBP 1.5bln 0.75% 2033 I/L Gilt: b/c 3.39x (prev. 3.17x) and real yield 0.745% (prev. 0.486%).

- Click for a detailed summary

COMMODITIES

- Choppy trade in the crude complex thus far in what has been a catalyst thin session; Brent'Jan 2025 currently sits towards the bottom end of a USD 71.71-72.24/bbl, after generally holding an upward bias throughout the morning.

- Precious metals are ever so slightly on a firmer footing, despite a relatively firmer Dollar and amid a catalyst-thin session thus far. Spot gold has gone as high as USD 2,673.79/oz, just ahead of its 50 DMA at USD 2,668.08/oz.

- Base metals hold a strong negative bias, giving back some of the prior day’s gains, which was sparked by a positive China Politburo readout. The pressure seen within the complex is also in-fitting with broader losses in the equities complex in Europe thus far.

- BofA sees TTF Gas prices averaging EUR 40/mwh in 2025; risk of a spike to EUR 75/mwh.

- Click for a detailed summary

NOTABLE DATA RECAP

- German HICP Final YY (Nov) 2.4% vs. Exp. 2.4% (Prev. 2.4%); HICP Final MM (Nov) -0.7% vs. Exp. -0.7% (Prev. -0.7%); CPI Final YY (Nov) 2.2% vs. Exp. 2.2% (Prev. 2.2%); CPI Final MM (Nov) -0.2% vs. Exp. -0.2% (Prev. -0.2%)

- Norwegian Core Inflation MM (Nov) 0.1% vs. Exp. -0.1% (Prev. 0.2%); Consumer Price Index YY (Nov) 2.4% vs. Exp. 2.3% (Prev. 2.6%); Core Inflation YY (Nov) 3.0% vs. Exp. 2.8% (Prev. 2.7%); Consumer Price Index MM (Nov) 0.3% vs. Exp. 0.2% (Prev. 0.6%)

NOTABLE EUROPEAN HEADLINES

- Kantar says UK grocery sales +2.5% Y/Y in the 4 weeks to December 1st; food inflation 2.6%.

- Germany's engineering group VDMA expects a 2% real terms decline in 2025 (unchanged from prior forecast); 2025 expected to decline 8% in real terms (unchanged from prior forecast).

- IATA Outlook: Global airlines industry to reach a record 5.2bln passengers in 2025; industry set to make USD 26.6bln in profit in 2025 (prev. USD 31.5bln in 2024)

NOTABLE US HEADLINES

- Oracle Corp (ORCL) Q3 2024 (USD): Adj. EPS 1.47 (exp. 1.48), Revenue 14.06bln (exp. 14.12bln). Cloud revenue (IaaS plus SaaS) 5.9bln (exp. 6bln). Cloud Infrastructure revenue (IaaS) 2.4bln (exp. 2.42bln). Cloud Infrastructure revenue (IaaS) in constant currency +52% (exp. +50.9%). Shares fell 7.8 after hours.

GEOPOLITICS

MIDDLE EAST

- "Israeli forces are 20 km from Damascus, according to the Pro-Hezbollah Al Mayaden, as they seized more villages in southern Syria", according to journalist Elster.

- Israel military spokesperson denies claims army has advanced to within 25km of Damascus; says troops have remained in the buffer zone.

- Israel's Navy has carried out a large-scale operation to destroy the Syrian army fleet, according to sources cited by Al Arabiya.

- Israel has received intelligence indicating that Hamas is ready to compromise on some of its conditions, according to five Israeli officials cited by NYT.

- "Loud explosions heard in Damascus", according to AFP journalists; details light.

CRYPTO

- Bitcoin is back on a firmer footing after dipping as low as USD 96k in the prior day vs currently USD 97.8k.

APAC TRADE

- APAC stocks were mostly firmer following a negative Wall Street lead, but with APAC players reacting to China easing its overall monetary policy stance.

- ASX 200 was the regional laggard and failed to benefit from a net dovish RBA, with the index dragged by a poor performance in Tech.

- Nikkei 225 eked mild gains amid the recent JPY weakness, but with gains capped as the currency claws back some losses in APAC trade.

- Hang Seng and Shanghai Comp were the regional outperformers after Politburo said China's fiscal policy is to be more proactive next year, and monetary policy is to be moderately loose (prev. prudent), marking the first shift in the stance of monetary policy since 2011. Although bourses were off the best levels ahead of the Chinese Central Economic Work Conference.

RBA

- RBA maintained its cash rate at 4.35% as expected, and noted that some upside risks to inflation appear to have eased. RBA noted recent data on inflation and economic conditions are still consistent with these forecasts, and the Board is gaining some confidence that inflation is moving sustainably towards target. RBA also said wage pressures have eased more than expected in the November SMP, and while underlying inflation is still high, other recent data on economic activity have been mixed, but on balance softer than expected in November. Click here for the release.

- RBA Governor Bullock, at the post-meeting presser, said RBA needs to think carefully on policy, recent data have been mixed with some softening; need to see more progress on underlying inflation; the Board did not discuss rate cut or rate hike. She added that she does not know if the RBA will cut rates in February, will have to watch data - wages and demand are slowing. Click here for full comments.

NOTABLE ASIA-PAC HEADLINES

- China is confident in reaching its FY economic targets, CCTV reports; adds that it is willing to continue dialogue with the US, and will manage differences.

- Chinese official development faces challenges next year, according to Xinhua; monetary policy shift means low interest rates

- South Korea's ruling party is discussing President Yoon's potential resignation in February or March, with snap elections to follow two months later

- Australian Treasurer Chalmers said he is to consult with the Shadow Treasurer on the makeup of new RBA boards.

- Chinese President Xi said China has full confidence in achieving this year's economic growth target, via Xinhua.

- China's Politburo conducts a study session, according to Xinhua.

- South Korea Finance Ministry said recent market volatility is a bit excessive, and will respond with market stabilizing measures, according to Reuters.

- South Korean opposition leader Lee said they will pass the budget today, via Yonhap.

- Japanese Economy Minister Akazawa, when asked about revised Q3 GDP data, said while Japan has not emerged from deflation, a virtuous cycle of wage hikes and passing-through of prices has started, according to Reuters.

- Huawei suppliers to face further US limits under defence bill; firms with Huawei ties risk exclusion from Pentagon contracts, according to Bloomberg. House measures could put more pressure on Huawei's supply chain.

DATA RECAP

- Chinese Trade Balance USD (Nov) 97.44B vs. Exp. 95.0B (Prev. 95.72B)

- Chinese Imports YY (Nov) -3.9% vs. Exp. 0.3% (Prev. -2.3%)

- Chinese Exports YY (Nov) 6.7% vs. Exp. 8.5% (Prev. 12.7%)

- Australian NAB Business Confidence (Nov) -3.0 (Prev. 5.0)

- Australian NAB Business Conditions (Nov) 2.0 (Prev. 7.0)