Europe Market Open: APAC stocks trade higher, European futures flat ahead of the ECB

12 Dec 2024, 06:55 by Newsquawk Desk

- APAC stocks eventually mimicked the sentiment on Wall Street and traded mostly higher following a slow start to the session and despite a lack of macro news flow.

- DXY was flat whilst JPY saw mild strength and AUD was boosted by a strong Aussie jobs report after a dovish RBA.

- US President-elect Trump has invited Chinese President Xi to attend his inauguration next month; it was not clear whether Xi has accepted the invitation, according to CBS sources.

- European equity futures are indicative of a flat cash open with the Euro Stoxx 50 future +0.1% after cash closed +0.2% on Wednesday.

- Looking ahead, highlights include SNB & ECB Policy Announcements, ECB Press Conference, IEA OMR, US PPI, US Initial Jobless Claims, Japanese Tankan Survey, Supply from US, Italy, Earnings from Broadcom, Costco.

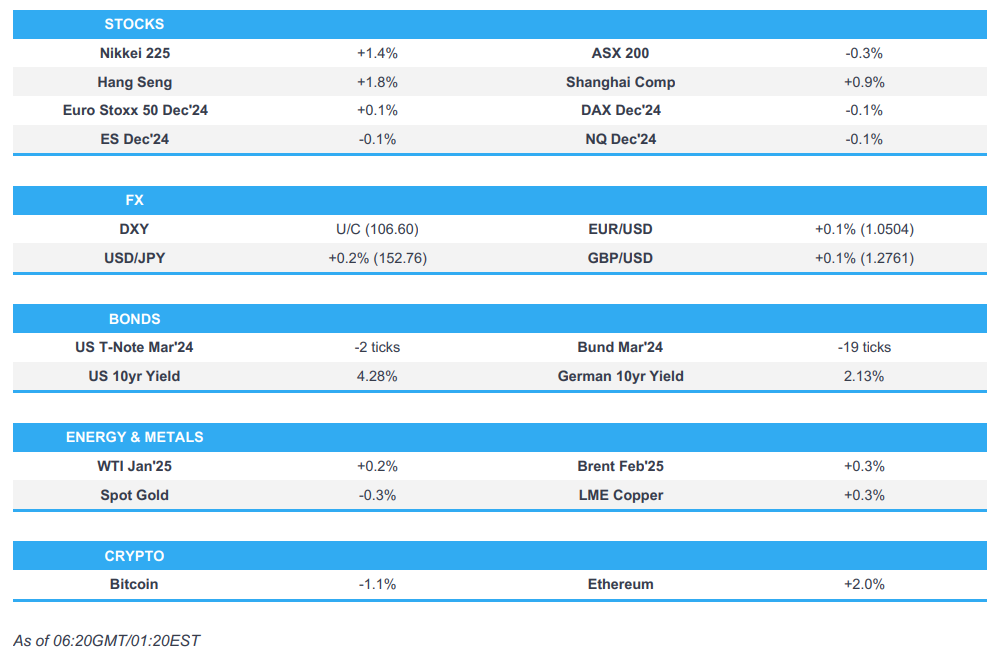

SNAPSHOT

US TRADE

EQUITIES

- US stocks mostly saw gains on Wednesday with Communications, Consumer Discretionary, and Technology the sectoral outperformers and the former once again supported by Alphabet's strength.

- Tech was further buoyed by gains in semiconductor names, highlighted by the SOXX ETF firming over 2.5%. Healthcare was the clear laggard.

- SPX +0.82% at 6,084, NDX +1.85% at 21,764, DJIA -0.22% at 44,149, RUT +0.48% at 2,394

- Click here for a detailed summary.

NOTABLE HEADLINES

- Bank of America (BAC) CEO Moynihan said US consumers are in pretty good shape, via GS conference, and companies are feeling stronger because of the favourable environment in the Trump administration. Moynihan added that M&A pipelines are full, and the IPO market is predicted to be stronger, while he expects regulatory changes will help get deals done.

APAC TRADE

EQUITIES

- APAC stocks eventually mimicked the sentiment on Wall Street and traded mostly higher following a slow start to the session and despite a lack of macro news flow.

- ASX 200 saw its earlier gains hampered after a strong Aussie jobs report which followed the dovish RBA yesterday, in which Governor Bullock said the Board will be watching all data including employment.

- Nikkei 225 reclaimed the 40,000 level for the first time since mid-October with gains driven by the Industrial and IT sectors, although at one point, the upside was capped by the firmer JPY.

- Hang Seng and Shanghai Comp were somewhat lethargic at the start, but momentum picked up, although there was little notable reaction seen on reports that US President-elect Trump invited Chinese President Xi to attend his inauguration next month, whilst it was not clear whether Xi has accepted the invitation. Participants now await the outcome of the Central Economic Work Conference.

- US equity futures were subdued across the board as futures took a breather from the post-US CPI price action and with macro news flow in APAC hours somewhat light.

- European equity futures are indicative of a flat cash open with the Euro Stoxx 50 future +0.1% after cash closed +0.2% on Wednesday.

FX

- DXY was flat throughout the session in a narrow 106.49-106.58 range, and within Wednesday's 106.26-81 parameter, with macro news flow in APAC hours on the quieter side.

- EUR/USD printed on either side of 1.0500 as traders gear up for the ECB confab with the central bank set to pull the trigger on a 25bps cut.

- GBP/USD held above 1.2750 with UK drivers light this week ahead of next week's deluge of UK releases.

- JPY strengthened as APAC players reacted to the Bloomberg sources piece which noted that the BoJ sees the next rate increase as a matter of time, with the pair eventually dipping under 152.00. USD/JPY later rose to session highs on source reports via Reuters that the BoJ is leaning towards keeping rates steady next week.

- Antipodeans were among the outperformers following the Aussie jobs report which saw Employment Change topping forecasts (driven by full-time employment) whilst the Unemployment Rate surprisingly fell to 3.9% despite forecasts of an uptick to 4.2% from 4.1%, although the Participation Rate surprisingly dipped. AUD/USD saw a boost nonetheless and held onto gains, whilst yesterday, RBA Governor Bullock said the Board will be watching all data including employment.

- PBoC set USD/CNY mid-point at 7.1854 vs exp. 7.2438 (prev. 7.1843)

FIXED INCOME

- 10yr UST futures saw horizontal trade amid a lack of catalysts and following a strong 10-year auction post-US CPI.

- Bund futures were subdued but with price action limited heading into the ECB announcement, in which a 25bps rate cut is expected and will most likely maintain a gradual approach to rate cuts.

- 10yr JGB futures were initially softer in sympathy with Western counterparts, although price action is relatively contained in quiet trade.

- US sells USD 39bln 10-year note; stop-through 1.7bps. High Yield: 4.235% (prev. 4.347%, six-auction average 4.122%). WI: 4.252%. Tail: -1.7bps (prev. -0.3bps, six-auction avg. -0.2bps). Bid-to-Cover: 2.7x (prev. 2.58x, six-auction avg. 2.55x). Dealers: 10.5% (prev. 14.7%, six-auction avg. 13.3%). Directs: 19.5% (prev. 23.6%, six-auction avg. 16.1%). Indirects: 70% (prev. 61.7%, six-auction avg. 70.6%)

COMMODITIES

- Crude futures took a breather after the price day's surge amid the weekly DoEs coupled with the broader risk appetite, which saw WTI reclaim USD 70/bbl and Brent rise north of USD 73.50/bbl.

- Spot gold was subdued but held onto a USD 2,700/oz handle with the yellow metal dipping some USD 15/oz at the Chinese cash open before immediately trimming two-thirds of the move.

- Copper futures held an upward bias following yesterday's US CPI and with traders now looking ahead to the findings from the Chinese Central Economic Work Conference.

- Natgas pipeline declares force majeure - Comp STA 343.

CRYPTO

- Bitcoin traded flat in APAC hours at the USD 101k level after finding support at USD 100k.

NOTABLE ASIA-PAC HEADLINES

- US President-elect Trump has invited Chinese President Xi to attend his inauguration next month, multiple sources told CBS News; it was not clear whether Xi has accepted the invitation.

- BoJ is reportedly leaning toward keeping rates steady next week, according to Reuters sources; there is no consensus within the bank on the final decision, some believe conditions have been met for a December hike; BoJ could hike if FOMC decision triggers JPY selloff. Many policymakers appear in no rush to pull the trigger with little risk of inflation overshooting, sources added.

- Japanese companies are reportedly worried about tariff hikes and US-China relations, according to a Reuters survey; Nearly three-quarters of Japanese companies expect Trump's next term to have a negative impact on the business environment.

- South Korean Finance Minister said they will closely monitor financial markets and respond to boost investor sentiment if needed, according to Reuters.

- South Korean President Yoon said he will fight until the last moment, according to Reuters.

DATA RECAP

- Australian Employment (Nov) 35.6k vs. Exp. 25.0k (Prev. 15.9k)

- Australian Unemployment Rate (Nov) 3.9% vs. Exp. 4.2% (Prev. 4.1%)

- Australian Participation Rate (Nov) 67.0% vs. Exp. 67.1% (Prev. 67.1%)

- Australian Full Time Employment (Nov) 52.6k (Prev. 9.7k)

- New Zealand Elec Card Retail Sale MM (Nov) 0.0% (Prev. 0.6%, Rev. 0.7%)

- New Zealand Elec Card Retail Sale YY (Nov) -2.3% (Prev. -1.1%)

GEOPOLITICS

MIDDLE EAST

- Israeli Defense Minister said there is a chance for a deal that will release all hostages, including US citizens, according to Reuters.

- "Hamas agreed to the presence of Israeli forces in Gaza after a ceasefire goes into effect", according to Kann News.

- "Israeli army announces the withdrawal from the tents area in southern Lebanon in accordance with the ceasefire agreement ", according to Al Arabiya.

OTHER

- US President-elect Trump is reportedly considering ex-intelligence chief Richard Grenell as Special Envoy for Iran, according to Reuters sources; the article suggests consideration of a key ally for the position sends a signal that Trump may be open to talks.

- US House of Representatives passed USD 895bln defence policy bill, according to Reuters.

EU/UK

NOTABLE HEADLINES

- The new French PM is reportedly set to be named on Thursday, according to a government source cited by Bloomberg

- UK RICS Housing Survey (Nov) 25.0 vs. Exp. 19.0 (Prev. 16.0); highest since September 2022.

- India-UK Free Trade Agreement talks to commence at the end of January, according to an Indian government source cited by Reuters.

LATAM

- Brazilian Selic Interest Rate 12.25% vs. Exp. 12.0% (Prev. 11.25%); Decision unanimous; in light of more adverse inflation scenario, the committee sees hikes of the same magnitude at the next two meetings.

- Brazilian Finance Minister Haddad said BCB decision was a surprise but pricing pointed to a move like that; and added there is no decision about changing the fiscal package, according to Reuters.

- Brazil's President Lula is to undergo a new medical procedure on Thursday to prevent further bleeding in the brain, via local press.

- Banxico financial stability report: Mexico's financial system has a resilient and solid position; stress tests confirmed that the banking system as a whole has the capacity to absorb significant shocks.