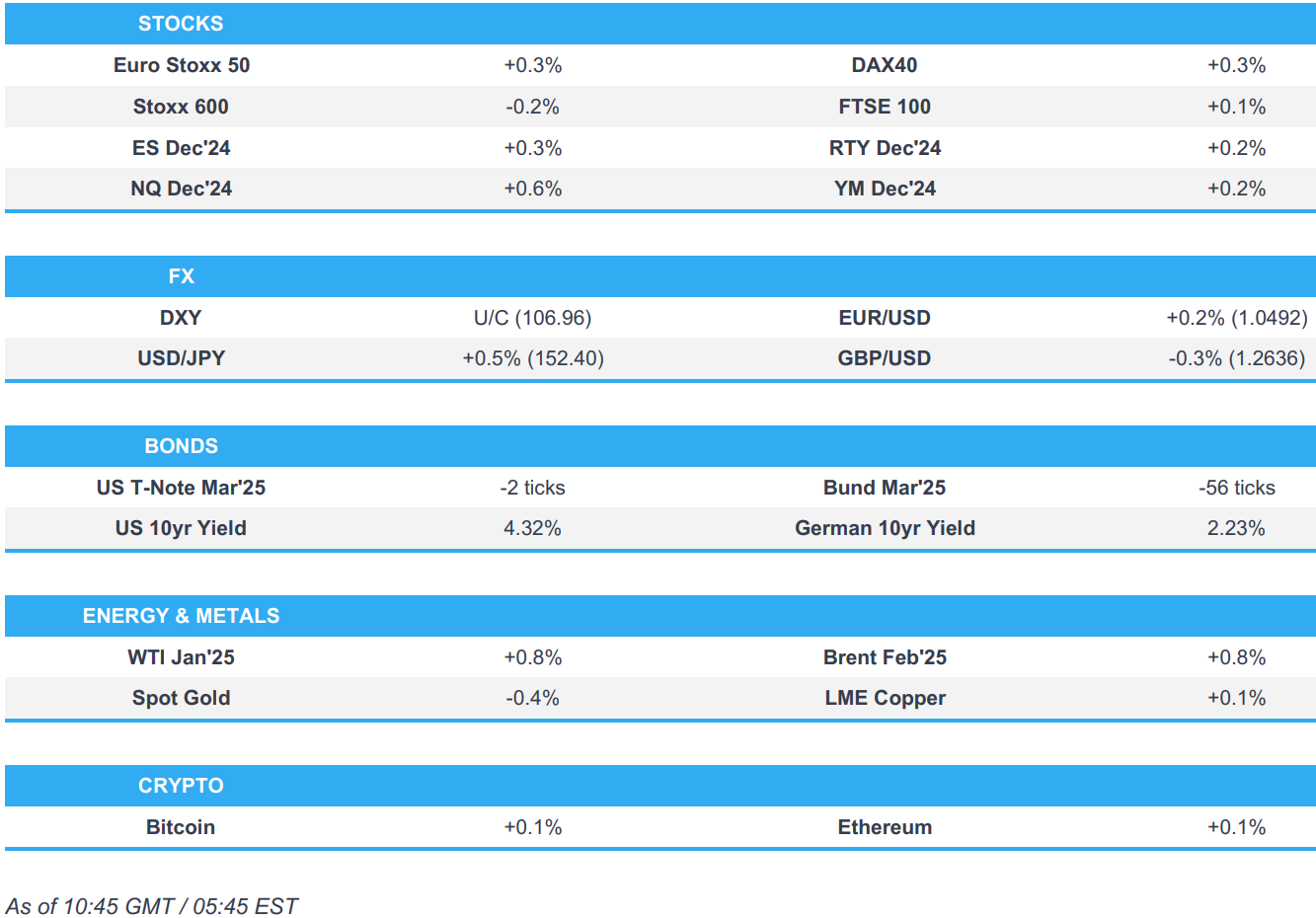

US Market Open: Risk sentiment improves with havens on the backfoot, DXY around 107.00

13 Dec 2024, 11:22 by Newsquawk Desk

- European bourses and US futures are generally firmer with specifics light, diverging from soft APAC trade; AVGO +15%.

- DXY trades around 107.00, GBP hit by soft GDP, JPY lags.

- Fixed benchmarks in the red post-ECB and ahead of a blockbuster week.

- Commodities contained, focus remains on geopols after Russian strikes on Ukrainian infrastructure and Blinken comments.

- Looking ahead, US Import/Export Prices, and Baker Hughes Rig Count.

EUROPEAN TRADE

EQUITIES

- European bourses began the European session on a modestly mixed footing, but soon after the cash open then lifted to session highs to display a positive picture in Europe.

- European sectors are mixed vs initially opening with a slight negative bias. Autos is towards the top of the pile, continuing to build on the gains seen in the prior session. Insurance follows closely behind, buoyed by gains in Swiss Re and Munich Re. Healthcare lags alongside losses in Basic Resources.

- US equity futures are entirely in the green, with clear outperformance in the tech-heavy NQ after Broadcom (+14%) shoots higher following a strong earnings report.

- Broadcom (AVGO) reported Q4 adj. EPS of 1.42 (exp. 1.39), and Q4 adj. net revenue of USD 14.05bln (exp. 14.1bln). Raised quarterly dividend +11% to 0.59/shr. Q4 semiconductor solutions revenue USD 8.23bln (exp. 8.05bln). Exec sees Q1 AI revenue growth of 65%, and expects momentum in AI connectivity to be as strong. +15% pre-market

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is essentially flat after spending most of the European morning in positive territory. DXY currently sits towards the bottom end of a 106.93-107.18 range. Today's docket is light, with just US Import/Export Prices on deck.

- EUR is slightly firmer vs. the USD as the dust continues to settle on yesterday's 25bps ECB rate cut. Sources followed the announcement, noting that the GC is prepared for a quarter-point rate cut at the next two meetings inflation stabilizes at the 2% target and economic growth remains sluggish. ECB speak this morning has continued to stress the inevitability of further easing in the coming months.

- JPY has continued to lose out to the USD throughout the European morning. JPY saw some fleeting support overnight in response to the higher-than-expected optimism among large Japanese manufacturers from the BoJ's Tankan Survey. Recent JPY weakness has coincided with a pick-up in risk sentiment (CHF has also moved lower in tandem).

- GBP is on the backfoot and near the bottom of the G10 leaderboard following soft M/M GDP data for October which printed at -0.1% vs. Exp. +0.1%. That being said, PM has cut its Q4 Q/Q forecast to 0.1% from 0.3% (MPC expects 0.3%). Accordingly, Cable slipped below its 21DMA at 1.2670 and fell to a session low at 1.2620.

- Antipodeans are contained vs. the USD in quiet trade with upside for AUD capped by the soft performance for Chinese markets overnight as traders digested the release from the Chinese Economic Work Conference, which overall seems like a disappointment as it offered little in terms of details whilst reaffirming the recent policy shift.

- PBoC set USD/CNY mid-point at 7.1876 vs exp. 7.2745 (prev. 7.1854)

- RBI likely sold USD to support the INR, according to traders cited by Reuters.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are steady overnight with specifics light and the docket ahead also limited as the countdown to the FOMC begins. Action in the European morning limited to a 110-09+ to 110-14 range. Yields little changed overall with no overt flattening/steepening bias thus far.

- Bunds began the morning in the red with EGBs trading in proximity to Thursday’s lows, after the ECB was judged to not be as dovish as some had hoped for. ECB speak this morning includes Muller saying the period of strong inflation is behind, Kazaks saying the direction is clearly down and the influential Villeroy remarking that there are more cuts to come. Since, the downside has extended slightly with Bunds at lows of 134.80 having faded below 135.00.

- OATs are down in tandem with the broader complex; once again, we are awaiting French President Macron’s announcement as to who the next PM will be.

- Initial leads for Gilts were bearish given the above but offset by a particularly soft set of UK growth data for October, with GDP missing across the board Services showing no growth while both Production and Construction fell in the period. Gilts in the red, though not as soft as EGBs are. Opened at a 94.89 session high before fading to a 94.66 trough.

- Click for a detailed summary

COMMODITIES

- WTI and Brent are on a modestly firmer footing after trading mostly rangebound overnight, amid the lack of pertinent newsflow for the complex. On geopolitics, Ukraine said Russia had attacked several Ukrainian energy facilities. As for the Middle East, the WSJ reported that "President-elect Trump is weighing options for stopping Iran from being able to build a nuclear weapon, including the possibility of preventive airstrikes". Brent'Feb 2025 currently sits around the USD 74/bbl mark.

- Gold is softer, potentially dented by the grind higher in risk sentiment seen in the European morning and continued DXY advances above 107.00.

- 3M LME Copper was flat for most the session but has just managed to recoup the USD 9.1k mark but remains markedly shy of Thursday’s USD 9.2k opening level and that session’s higher thereafter at USD 9.27k before the WTD USD 9.3k peak.

- Goldman Sachs said their base case is that Brent averages USD 76/bbl in 2025 given near offset between a modest 400k BPD surplus and a normalisation in currently low valuation.

- Moldovan Parliament declares state of emergency from Dec 16th amid the possible end of flow of Russian gas from Jan 1st, according to Reuters.

- Russian attacks on Ukrainian energy facilities were more focussed on gas infrastructure this time, via Reuters citing sources.

- UBS expects copper prices to rise to the USD 10-11k MT range, expects demand to rise above 3% Y/Y in 2025. Sees copper market that is modestly in deficit of around 250,000 T.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (Oct) -0.1% vs. Exp. 0.1% (Prev. -0.1%); YY 1.3% vs. Exp. 1.6% (Prev. 1.0%); 3M/3M 0.1% vs. Exp. 0.1% (Prev. 0.1%)

- UK GfK Consumer Confidence (Dec) -17.0 vs. Exp. -18.0 (Prev. -18.0)

- German Wholesale Price Index MM (Nov) 0% (Prev. 0.4%); YY -0.6% (Prev. -0.8%)

NOTABLE EUROPEAN HEADLINES

- ECB's Villeroy says more rate cuts are to come. Notes that French bond spreads have moved away from Germany and closer to Italy.

- ECB's Kazaks says the direction of interest rates is clearly down, the neutral rate is closer to 2% than 3%, significant reduction in rates is still necessary.

- Goldman Sachs (GS) cuts UK's 2024 GDP growth forecast to 1.0% from 1.2%.

- ECB's Holzman says yesterday's decision was "good". If things go as expected, sees no danger for prices in cutting rates next year. Neutral rate is around 2%, rates could fall to this level.

- ECB's Vasle says decisions will be taken meeting-by-meeting in a data-dependent fashion.

- BoE Inflation Attitudes Survey (Nov.): Median expectations of the rate of inflation over the coming year were 3%, up from 2.7% in August 2024. Asked about expected inflation in the twelve months after that, respondents gave a median answer of 2.8%, up from 2.6% in August 2024. Asked about expectations of inflation in the longer term, say in five years’ time, respondents gave a median answer of 3.4%, up from 3.2% in August 2024.

- VCI says producer prices down 2.5% Y/Y, total sales - 2% Y/Y to EUR 221bln, industry sales will slacken due to higher producer pries and lo order backlogs in 2025.

- Bundesbank lowers its German growth outlook across the entire forecast horizon. Economy to stagnate in the "winter half-year" and then make a slow recovery across 2025. US President-elect Trump's proposed tariffs could lower growth by 1.3-1.4% through 2027. ECB's Nagel says protectionism is the biggest area of uncertainty. Growth Forecasts: 2024: -0.2%; 2025: 0.2%; 2026: 0.8%.

NOTABLE US HEADLINES

- Microsoft (MSFT) filed for debt shelf; size undisclosed, via SEC filing. Separately, Microsoft introduces Phi-4, the company's newest small language model specialising in complex reasoning

- US President-elect Trump's transition team has reportedly started to explore pathways to shrink, consolidate or eliminate the top bank regulators, according to WSJ.

- Apple (AAPL) will begin assembling AirPods in India by early 2025, partnering with Foxconn (HNHPF), according to Bloomberg

GEOPOLITICS

- US President-elect Trump said "For the great privilege of accessing our markets, these foreign companies should hire our incredible American Workers, instead of laying them off, and sending those profits back to foreign countries", via Truth Social.

- US President-elect Trump is weighing options for stopping Iran from being able to build a nuclear weapon, including the possibility of preventive airstrikes, according to WSJ.

- US Secretary of State Blinken says that in the last few weeks he has seen encouraging signs that a Gaza ceasefire is possible

- Israeli Defense Minister orders Israeli troops to prepare to remain on Mount Hermon during winter months, via Reuters citing a statement

- Russian attacks on Ukrainian energy facilities were more focussed on gas infrastructure this time, via Reuters citing sources.

- US Sectary of State Blinken says that in the last few weeks he has seen encouraging signs that a Gaza ceasefire is possible.

CRYPTO

- Bitcoin is on a slightly softer footing and trades on either side of the USD 100k mark.

APAC TRADE

- APAC stocks traded lower across the board following a similar session on Wall Street after the hot US PPI, whilst sentiment in Asia-Pacific was somewhat hampered as participants digested the disappointing release from the Chinese Economic Work Conference.

- ASX 200 was pressured by the metals sectors, namely gold miners, after the recent slide in the yellow metal as the Buck ramped up.

- Nikkei 225 pulled back further under 40,000, failed to benefit from a softer JPY and largely overlooked higher-than-expected optimism among large Japanese manufacturers from the BoJ's Tankan Survey.

- Hang Seng and Shanghai Comp were both softer as traders digested the release from the Chinese Economic Work Conference, which overall seems like a disappointment as it offered little in terms of details whilst reaffirming the recent policy shift.

NOTABLE ASIA-PAC HEADLINES

- PBoC official Zou Lan says PBoC will deepen FX market reform next year, according to state TV. Will keep the Yuan 'basically' stable. Will respond vigorously to external shocks. Will increase treasury bond buying and selling operations. Will provide sound liquidity environment for government bond issuance.

- Trump Trade Advisor Navarro warned against currency manipulation after Reuters sources suggested China is mulling a weaker CNY.

- South Korean Finance Ministry said they will deploy more market stabilising measures if volatility heightens excessively, according to Reuters.

- BoJ Dec Tankan corporate price expectations survey: Japanese firms expect consumer prices to rise 2.4% a year from now (prev. +2.4%). 3-year expectation +2.3% (prev. +2.3%); 5-year expectation +2.2% (prev. +2.2%).

- Japan's small firms are spending more of their profits on wages than their larger counterparts and may struggle to keep raising pay, casting doubt on whether wage gains are broad enough for BoJ to keep hiking rates, according to Reuters analysis. Policymakers are reportedly looking at whether small firms (which employ 70% of Japan's workforce) can continue meeting pay demands.

- REUTERS POLL: BoJ to hold key interest rate at 0.25% in December, according to 58% of economists polled (vs 44% in Nov poll)

- Chinese President Xi is not planning to attend Trump's inauguration but might send a senior official to represent him, according to WSJ sources.

DATA RECAP

- Japanese Tankan All Big Capex Est (Q4) 11.3% vs. Exp. 9.6% (Prev. 10.6%)

- Japanese Tankan big non-mf outlook DI (Q4) 28.0 vs. Exp. 28.0 (Prev. 28.0)

- Japanese Tankan Big Mf Outlook DI (Q4) 13.0 vs. Exp. 11.0 (Prev. 14.0)

- Japanese Tankan Big Non-Mf Idx (Q4) 33.0 vs. Exp. 32.0 (Prev. 34.0)

- Japanese Tankan Big Mf Idx (Q4) 14.0 vs. Exp. 12.0 (Prev. 13.0)

- Japanese Tankan Small Non-Mf Idx (Q4) 16.0 vs. Exp. 12.0 (Prev. 14.0)

- Japanese Tankan Sm Non-Mf Outlook DI (Q4) 8.0 vs. Exp. 10.0 (Prev. 11.0)

- Japanese Tankan All Sm Capex Est (Q4) 4.0% vs. Exp. 4.3% (Prev. 2.6%)

- Japanese Tankan Small Mf Idx (Q4) 1.0 vs. Exp. -1.0

- South Korea Import Price Growth YY (Nov) 3.0% (Prev. -2.5%)

- South Korea Export Price Growth YY (Nov) 7.0% (Prev. 2.0%)

- New Zealand Manufacturing PMI (Nov) 45.5 (Prev. 45.8)

LATAM

- Brazil President Lula remains in ICU after the latest surgery on Thursday morning, according to a medical report.

- Peru Central Bank maintains reference rate at 5.00%, as expected; said future decisions will depend on inflation.