US Market Open: GBP benefits from hot UK wages data, DXY bid amid a tepid risk tone ahead of US Retail Sales

17 Dec 2024, 10:57 by Newsquawk Desk

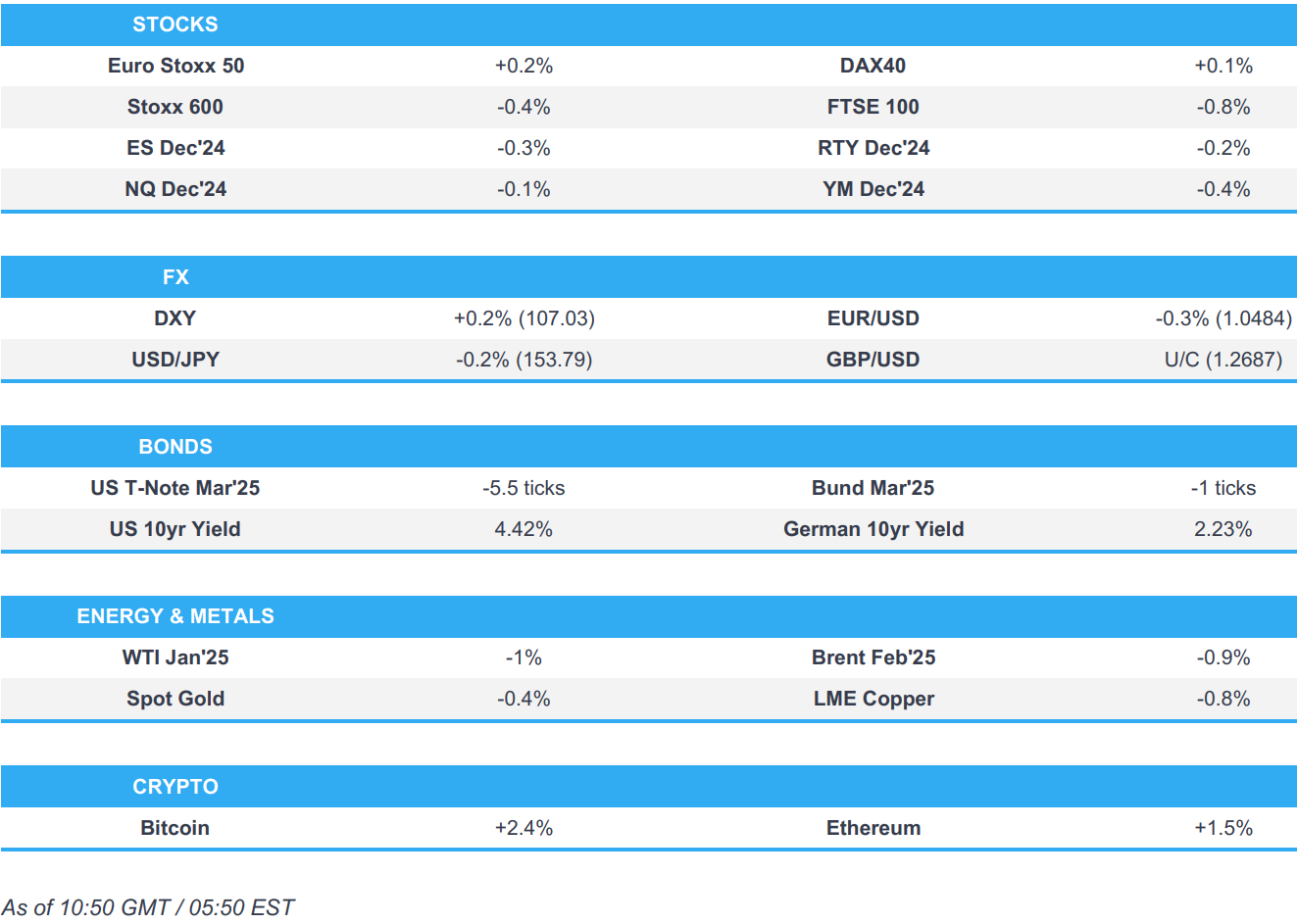

- European bourses are mostly in the red, but sentiment has improved a touch since the cash open; US futures modestly lower.

- DXY back above 107.00, GBP posted early gains after hot wages data.

- Gilts lag as UK wage data essentially removes any chance of a Dec. BoE cut ahead of CPI; USTs a little lower ahead of US Retail Sales.

- Commodities succumb to the tepid risk tone and ongoing USD strength.

- Looking ahead, US Retail Sales, Canadian Inflation, US Industrial Production, Japanese Trade Balance, NBH Policy Announcement, Supply from the US.

EUROPEAN TRADE

EQUITIES

- European bourses began the session entirely in the red and have mostly resided in negative territory throughout the European morning, but have attempted to edge a little higher in recent trade, with some indices managing to climb incrementally into the green. German Ifo data confirmed the dire situation in the region, whilst ZEW surprised to the upside; metrics which sparked little price action.

- European sectors are almost entirely in the red, given the slip in risk sentiment in today’s session thus far. Tech is marginally in positive territory, alongside Consumer Products and Services. Energy is the clear underperformer joined by Basic Resources, attributed to the losses seen in underlying commodity prices today.

- US equity futures are modestly in negative territory, in-fitting with the losses seen in Europe and the general risk tone; a slight turn in fortunes in comparison to the gains seen in the prior session.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is on a firmer footing and topped 107.00 in early European trade, to currently trade at the top-end of a 107.05-106.69 range. Should the upside continue, the Dollar index could see a potential test of the prior day’s best at 107.16, and then 107.18 from Friday 13th December. The North American day sees the release of US retail sales, which are expected to rise +0.5% M/M in November.

- EUR is on the backfoot vs the Dollar, after posting modest gains in the prior session. German Ifo figures were mixed, with the Business Climate and Expectations components printed below expectations whilst the Current conditions improved a touch. Overall the figures only further confirmed the dire situation in the region. German ZEW was a little more optimistic, which helped to lift the Single-Currency a touch, but ultimately proved fleeting. Currently trading near session troughs at 1.0480.

- GBP is on a firmer footing and one of the better G10 performers today, as traders trim their bets for more cuts in the coming year following today’s hot jobs reports, with particular focus in the wages components which surpassed the top end analyst expectations. Cable briefly topped 1.27 before then paring the upside to a current 1.2687.

- The JPY is the best G10 performer thus far, in contrast to the losses seen in the prior day. USD/JPY currently trades in a 153.76-154.34 range, and just within the confines made on Monday.

- Antipodeans are on the backfoot and in-fact the worst G10 performers, given the subdued risk sentiment and losses in commodity prices.

- PBoC sets USD/CNY mid-point at 7.1891 vs exp. 7.2842 (prev. 7.1882)

- RBI likely sold USD via state-run banks at 84.92-84.93, according to Reuters citing traders.

- Barclays Month- & Quarter-end Rebalancing: USD neutral.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are in the red but only modestly so, moving in tandem with the morning’s data release out of the UK and Germany but in relatively thin 109-21 to 109-29+ parameters. US Retail Sales precedes a 20yr auction later today.

- Bunds came under pressure on the morning’s UK wage data (see Gilts for details) with leads bearish in-fitting with contained/softer UST action overnight. However, this proved relatively short-lived as Bunds were sent back into positive territory to a 134.94 session high on Germany’s 13% Y/Y lower 2025 issuance intentions, and the mixed but ultimately softer German Ifo release. On the data front, Ifo figures were poor whilst the ZEW was a little more optimistic on the economy and helped to spark some short-lived upside.

- Gilts are underperforming after the day's jobs data, with the wages components have taken centre stage with the hot metrics essentially removing any chance of easing on Thursday with just 1bps implied (c. 4bps pre-release. Though, we await CPI on Wednesday. A release which caused Gilts to gap lower by 47 ticks at the open and then slip further to an initial 93.27 trough. The 2029 outing saw a softer cover than the prior, which led Gilts down to a new 93.23 trough.

- German Finance Agency intends to issue around EUR 380bln via Federal debt sales in 2025, -13% Y/Y. Plus two syndications.

- Italy PM calls for discussions on common EU bonds to fund defence spending.

- UK sells GBP 3.75bln 4.125% 2029 Gilt: 2.9x (prev. 3.05x), avg yield 4.348% (prev. 4.148%) & tail 0.8bps (prev. 0.8bps)

- Click for a detailed summary

COMMODITIES

- WTI and Brent came under pressure early-doors despite a lack of fresh fundamental drivers at the time. Pressure which took the benchmarks to fresh lows for the week and back towards the troughs from Friday; though, well within last week’s circa. USD 5/bbl parameters. Brent'Feb 25 currently sits near session lows at USD 73.35/bbl.

- Gold is softer, pressured by continued USD advances which has taken the DXY above the 107.00 mark. Yellow metal has been waning gradually in European hours, as the region's risk tone meanders higher. Thus far, down to a USD 2641/oz base.

- Base metals spent APAC trade in very thin ranges but have since slipped to the lower-end of those and modestly into the red. Pressure which comes despite the modest inch higher in the European risk tone.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Avg Wk Earnings 3M YY (Oct) 5.2% vs. Exp. 4.6% (Prev. 4.3%, Rev. 4.4%); Ex-Bonus) (Oct) 5.2% vs. Exp. 5.0% (Prev. 4.8%, Rev. 4.9%)

- UK ILO Unemployment Rate (Oct) 4.3% vs. Exp. 4.3% (Prev. 4.3%); Employment Change (Oct) 173k vs. Exp. 2k (Prev. 219k)

- UK HMRC Payrolls Change (Nov) -35k (Prev. -5k, Rev. 24k)

- German Ifo Business Climate New (Dec) 84.7 vs. Exp. 85.6 (Prev. 85.7); Ifo Current Conditions New (Dec) 85.1 vs. Exp. 84.0 (Prev. 84.3); Ifo Expectations New (Dec) 84.4 vs. Exp. 87.5 (Prev. 87.2)

- German ZEW Current Conditions (Dec) -93.1 vs. Exp. -93.0 (Prev. -91.4); ZEW Economic Sentiment (Dec) 15.7 vs. Exp. 6.5 (Prev. 7.4); ZEW says economic outlook is improving; experts still expect further interest rate cuts for the coming year; experts assess the recent rise in inflation as a temporary phenomenon

- EU ZEW Survey Expectations (Dec) 17 (Prev. 12.5)

NOTABLE EUROPEAN HEADLINES

- French Central Bank Forecasts: 2024 Growth seen at 1.1% (unchanged), 2025 seen at 0.9% (prev. 1.2% in Sept.); 2026 at 1.3% (prev. 1.5%), 2027% at 1.3%. HICP inflation 1.6% in 2025, 1.7% in 2026 and 1.9% in 2027.

- ECB's Rehn says data to decide speed and scale of rate cuts; scale and speed of rate cuts will be determined in each meeting on the basis of incoming data and comprehensive analysis; Euro area inflation starting to stabilise at ECB's 2% target. Monetary policy will cease to be restrictive in the later winter, early spring period (i.e. between January and June 2025)

- ECB's Kazimir says inflation risks are well balanced, via Bloomberg. Will discuss the neutral rate when they approach 2.5%.

- ECB keeps capital requirements broadly steady for 2025, reflecting strong bank performance amid heightened geopolitical risks

GEOPOLITICS

MIDDLE EAST

- "The IDF has approved plans for major strikes in Yemen, and is prepared to act pending government approval", via Open Source Intel citing N12 News

- US military said it conducted an airstrike against Houthis in Yemen, according to Reuters.

- Syria's rebel leader said factions would be 'disbanded' and fighters would join the army, according to AFP.

OTHER

- Russia may increase the frequency of missile testing as external threats grow, according to Russian state news agencies citing the commander of Russian strategic missile forces. Russia may also increase the number of nuclear warheads on deployed carriers in response to similar actions by the US. Mobile-based missile systems, the commander noted, will be decisive means of inflicting devastating enemy damage in a potential retaliatory nuclear attack. Russia’s strategic missile forces plan maximum-range launches as part of state testing of prospective new systems. Additionally, Russia and the US give each other at least a day's warning about planned launches of intercontinental ballistic missiles.

- Russian lieutenant general Kirillov and his associate killed in explosion in Moscow, according to RT sources; Kirillov is listed as Chief of Radiological, Chemical and Biological Defence of Russian Armed Forces.

- Senior US officials say Turkey and its militia allies are building up forces along the border with Syria, raising alarm that Ankara is preparing for a large-scale incursion into territory held by American-backed Syrian Kurds, according to WSJ.

CRYPTO

- Bitcoin is firmer and holds around the USD 107k mark.

APAC TRADE

- APAC stocks eventually traded mixed after the region initially showed a positive bias, taking cues from Wall Street, and in the absence of macro newsflow with looming risk events.

- ASX 200 firmed with banks underpinning the index, with Westpac among the gainers while its CFO announced plans to retire.

- Nikkei 225 trimmed earlier upside as traders were cautious ahead of the BoJ, with the decision contingent on the FOMC's announcement hours beforehand.

- Hang Seng and Shanghai Comp traded within narrow parameters in uneventful trade amid quiet newsflow, with participants remaining non-committal ahead of major risk events.

NOTABLE ASIA-PAC HEADLINES

- China is to maintain a growth target of "around 5%" for 2025, according to Reuters sources. China is to target a budget deficit of 4% in 2025 (vs 3% initially). More stimulus will be funded through issuing off-budget special bonds, sources added.

- New Zealand sees 2024/25 operating balance before gains, losses at NZD -17.32 bln (budget NZD -13.37 bln), according to Reuters.

- New Zealand Debt Management Office says 2024/25 gross bond issuance increases to NZD 40 bln from NZD 38 bln in May, according to Reuters.

- Alibaba Group (9988 HK/ BABA) sells Intime; Expected gross proceeds to Alibaba from Intime sale is approximately RMB 7.4bln; Alibaba expects to record losses of approximately RMB 9.3bln as a result of the sale of Intime.

- PBoC injected CNY 355.4 bln via 7-day reverse repos with the rate maintained at 1.50%, according to Reuters.

- South Korean acting President Han says South Korea is to implement the budget on Jan 1st; South Korea to allocate budget promptly for economic revitalisation, according to Reuters.

- Magnitude 7.4 quake has struck Port-Vila in the Vanuatu region, according to USGS.

DATA RECAP

- New Zealand RBNZ Offshore Holdings (Nov) 58.6% (Prev. 59.2%)