US Market Open: Bonds bid, DXY firmer and Equities deep in the red after Commerce Secretary Lutnick said there is no postponing tariffs

07 Apr 2025, 11:15 by Newsquawk Desk

- US Commerce Secretary Lutnick said there is no postponing tariffs and April 9th tariffs are coming; tariffs are going to stay in place for days and weeks.

- US NEC Director Hassett said more than 50 countries have reached out to the White House to begin trade negotiations.

- Stocks continue to sink as risk-off sentiment continues, reports that China is mulling accelerating stimulus measures fails to life the complex; NQ -4%.

- Havens lead, activity currencies lag as the Trump trade agenda continues to dominate.

- EGBs & USTs climb as Central Bank easing bets increase on stagflation/recession concerns.

- Crude continues to sink, XAU/copper incrementally lower.

- Looking ahead, US Employment Trends & President Trump.

TARIFFS/TRADE

US

- US President Trump said China has been hit much harder than the US and that it is not even close, while he told Americans to ‘hang tough’ and it won’t be easy, but the end result will be historic. Trump separately commented that unless they solve the trade deficit with China, he is not making a deal, while he noted the Chinese trade surplus is unsustainable and he was not intentionally engineering a market selloff. Furthermore, he said he has spoken to European and Asian leaders on tariffs.

- US President Trump posted on Truth "We have massive Financial Deficits with China, the European Union, and many others. The only way this problem can be cured is with TARIFFS, which are now bringing Tens of Billions of Dollars into the U.S.A. They are already in effect, and a beautiful thing to behold. The Surplus with these Countries has grown during the “Presidency” of Sleepy Joe Biden. We are going to reverse it, and reverse it QUICKLY. Some day people will realize that Tariffs, for the United States of America, are a very beautiful thing!"

- US Commerce Secretary Lutnick said there is no postponing tariffs and April 9th tariffs are coming, while he stated tariffs are going to stay in place for days and weeks, according to CBS News.

- US NEC Director Hassett said he would expect that job numbers are going to go up back and forth now that tariffs are in place, while he added that more than 50 countries have reached out to the White House to begin trade negotiations. Hassett also stated that President Trump decided not to apply tariffs to Russia due to continuing negotiations over the war in Ukraine, according to ABC News.

ASIA

- China’s government said China has taken and will continue to take resolute measures to safeguard its sovereignty, security and development interests, while it added there are no winners in trade wars and added the US should stop using tariffs as a weapon, according to Xinhua.

- China is reportedly considering frontloading stimulus in order to counter the tariff hit, via Bloomberg.

- Central Huijin, a Chinese Sovereign Fund, is actively taking measures to stabilise the capital market, via Reuters citing China's State Media.

- Taiwan pledged more investment in the US and the removal of trade barriers after Trump tariffs, while it said it will proactively resolve non-tariff trade barriers that have existed for many years and has no plans of tariff retaliation.

- Japanese PM Ishiba said they are looking into non-tariff barriers pointed out by the US, while he added that Japan has created the biggest investment and jobs in the US and has never done anything unfair.

- South Korea's Trade Minister is to visit the US on Tuesday-Wednesday and will meet with US Trade Representative Greer to discuss lowering 25% US tariff rates.

- India is unlikely to immediately retaliate against US President Trump’s reciprocal tariffs and is focusing efforts on negotiating a bilateral trade deal with the US to bring down duties, according to a government official cited by Economic Times.

EU/UK

- EU wants India to remove tariffs on auto imports under a trade deal, according to Reuters sources. India is opening to reducing auto import tariffs to 10% from over 100% to seal an EU trade deal. Carmakers in India are lobbying to retain auto import duties at a minimum 30% and no reduction on EVs until 2029.

- EU's Sejourne "We could decide to withdraw all American companies from European public markets. It’s the economic bazooka, but it’s one of the topics on the table.", via BFM

- German Economy Minister Habeck says the EU response must be united. Need to avoid a trade war. Could increase pressure on the US in pharmaceuticals.

- Spanish Economy Minister says the EU will discuss which US products will get tariffs in response to the Trump metal tariffs, talks will happen today.

- UK PM Starmer spoke with Canadian PM Carney and they agreed on the importance of free and open trade between like-minded nations, while Carney reaffirmed his commitment to Canada playing a role in the coalition of the willing and they both agreed that an all-out trade war is in no-one’s interest.

- UK PM Starmer and French President Macron agreed a trade war was in nobody’s interests but added nothing should be off the table, while they shared their concerns about the global economic and security impact, particularly in Southeast Asia.

- Economists believe the UK is well-placed to secure a trade deal with the US which could further reduce tariffs and boost the economy, according to Bloomberg.

- EU’s Von der Leyen said following a phone call with UK PM Starmer that US tariffs harm all countries and the EU is committed to negotiations with the US and is ready to defend itself with proportionate countermeasures.

- EU Industrial Commissioner Sejourne reaffirms that the EU response to the US will be united and proportionate. Europe also has cards up its sleeve to put pressure on America re. response to Trump tariffs. List of products in the response to be announced in the coming days.

- France suggested targeting Big Tech’s data use in response to US tariffs and is also considering taxing digital services, according to POLITICO citing French Economy and Finance Minister Eric Lombard.

EUROPEAN TRADE

EQUITIES

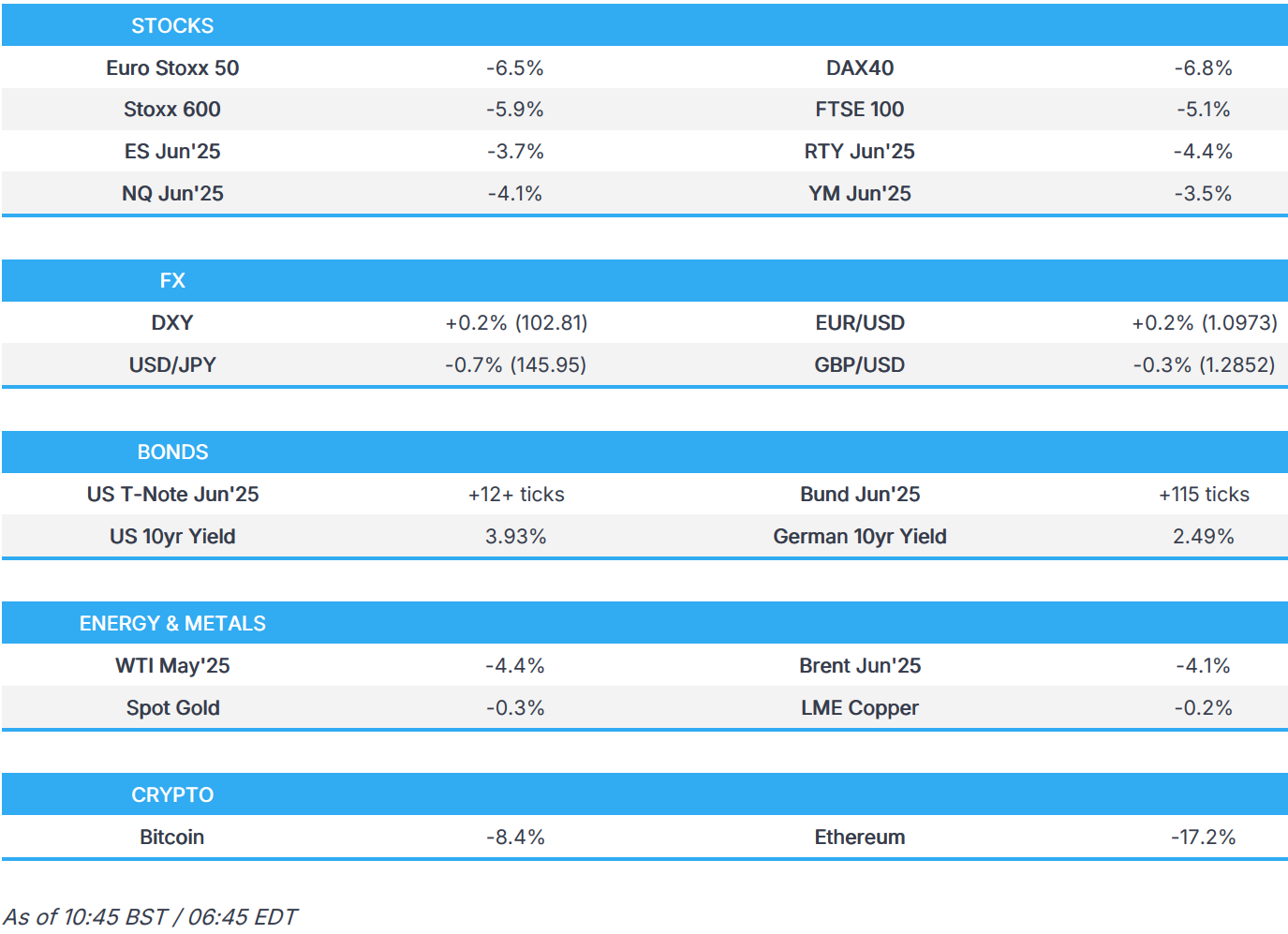

- European bourses (STOXX 600 -5.8%) are entirely in the red as risk sentiment continues to get hammered, with focus still on Trump’s tariffs, China’s retaliatory measures and the associated economic growth woes. Indices have managed to improve a touch off worst levels, but still remain firmly in negative territory.

- European sectors are entirely in the red, in-fitting with the broader risk tone; as it stands, every sector is lower by more than 4%. Tech is unsurprisingly the laggard today, given the risk tone; Industrials, Energy and Consumer Products follow closely behind.

- US equity futures (ES -3.7%, NQ -4.1%, RTY -4.4%) are entirely in the red, with the ES and NQ having gapped lower by 4.5% and 4.9% respectively, at the reopen of futures trading – price action since has seen a slight pick-up, though futures remain near worst levels.

- Click for US Equity Market Circuit Breakers

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is net softer vs. the majors but showing a mixed performance vs. peers (weaker vs. havens but stronger vs. activity currencies). Trump's tariff agenda very much remains the key driving force in the market with the President not looking to back down from the measures announced last week. Agenda today is relatively light aside from US Employment Trends and some appearances from US President Trump. DXY has picked up in recent trade and is towards the top end of Friday's 101.54-103.18 range.

- EUR is firmer vs. the broadly softer USD and remains underpinned despite the current risk environment. ING attributes the support to the EUR's "role as a liquid alternative to the dollar and the fact that the euro runs a 3% current account surplus". However, the open and trade-focused nature of the Eurozone economy clearly remains a risk. EUR/USD has ventured as high as 1.1050 but failed to sustain a move above the 1.10 mark.

- JPY is firmer vs. the USD and one of the best performers across the G10 complex. Support for JPY has been provided by the risk-aversion across the market with Japanese stocks hit particularly hard overnight (Nikkei 225 -7.7%). Elsewhere, commentary out of Japan has seen PM Ishiba is to speak with President Trump at 08:00ET, whilst Kyodo News reported that the PM is reportedly instructing the compilation of an extra budget as soon as this month. Furthermore, the Japanese business lobby chair has stated that it needs to be examined whether reducing rates could be effective with real interest rates remaining still far from neutral.

- GBP is steady vs. the broadly softer USD with UK-specific newsflow on the light side aside from weekend calls between PM Starmer are other world leaders over the trade situation.

- Antipodeans are both softer vs. the USD and at the bottom of the G10 leaderboard alongside the risk-off price action in the market. AUD/USD has extended on the downside seen on Friday in the wake of China's retaliation to the US tariff measures, which sank the pair to its lowest level since April 2020. AUD has been unable to materially benefit from a Bloomberg report that China is considering frontloading stimulus in order to counter the tariff hit.

- PBoC set USD/CNY mid-point at 7.1980 vs exp. 7.3162 (Prev. 7.1889).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer, at best have been above the 114-00 handle to a 114-10 peak, a high that printed just after the re-opening of trade when the selling in Asia was at its most pronounced and saw the Nikkei 225 hit circuit breakers. The main development this morning came from China, with reports via Bloomberg sources that they are considering frontloading stimulus. An update which prompted a bit of a pullback from highs for fixed, though only modest at the time. Thereafter, as the risk tone came off worst levels, USTs pulled back to a 113-12+ low. Though, still firmer on the session with the 10yr yield still just below 4%; Friday’s base was 3.86%.

- Bunds are in-fitting with USTs, notched a 132.02 peak around the European cash equity open when sentiment for the morning was at its worst. Since, as the tone improves, a pullback has occurred with Bunds down to 131.35 though still markedly clear of Friday’s close. Markets are still awaiting the EU's response; the Industrial Commissioner Sejourne reaffirmed that the EU response to the US will be united and proportionate, Sejourne also indicated that we should hear the response in the next few days. The 132.02 high in Bunds is just a tick shy of the peak from the week of Germany’s fiscal reform and is a significant bounce from the 126.53 low that printed in the days after. EZ Sentix Index printed below the forecast range and at its lowest since October 2023 - no impact on German paper.

- Gilts are in-fitting with the above, opened higher by 69 ticks and then extended further to a 94.50 peak before pulling back from best in-fitting with EGBs and USTs. However, the pullback has been more pronounced with Gilts slipping into the red.

- JGBs opened higher given the risk tone and continued to climb to a 142.61 peak with the odds of tightening by the BoJ trimmed further with just 5bps of tightening implied for the remainder of 2025.

- Click for a detailed summary

COMMODITIES

- Crude is on the backfoot continuing last week's hefty downside as Trump's tariff woes continues to weigh on sentiment; further fuelling downside is Saudi Arabia cutting its oil prices to Asia to their lowest in four months. Price action in the European morning has been fairly rangebound, given the lack of recent energy-specific updates and despite a slight pick up in risk tone across markets.

- WTI and Brent lower by in excess of 4% at worst, but as the tone improves from lows this has moderated to downside of just over 3%.

- Spot gold remains subdued, but is off overnight lows which saw the yellow-metal slip below the USD 3k mark to a USD 2,970/oz low. Trade throughout the European morning has been fairly lacklustre; currently trading around USD 3035/oz in a USD 2,972.94-3,055.22/oz range.

- Base metals are broadly lower given the risk tone; 3M LME Copper is incrementally lower/flat and currently trades in a USD 8,153.85-9,074.25/oz range.

- OPEC+ JMMC meeting made no changes to oil output policy and stressed the need to ensure full compliance.

- Saudi Arabia cut oil prices to Asia to their lowest in four months with May Arab Light Crude set at a premium of USD 1.20/bbl vs Oman/Dubai, while it set May Arab Light Crude official selling price NW Europe at + USD 2.55/bbl vs ICE Brent and to US at + USD 3.60/bbl vs ASCI

- Qatar set May marine crude OSP at a premium of USD 0.60/bbl vs Oman/Dubai and set land crude at a premium of USD 0.50/bbl vs Oman/Dubai.

- Chile’s government plans to cut the 2025 estimated average price of copper to USD 3.90-4.00/lb from the current USD 4.25/lb projection. It was also reported that the Chilean Mining Minister said copper could reach a technical support price at USD 3.90/lb amid uncertainty.

- US is reportedly closing in on a critical mineral deal with the Democratic Republic of the Congo.

- Morgan Stanley cuts its Brent forecast to USD 65/bbl (prev. 70/bbl) for Q2.

- Citi has cut its 0-3 month Brent forecast to USD 60/bbl.

- Citi has cut its 0-3 month copper and aluminium forecasts to USD 8k/tonne and USD 2.2k/tonne respectively.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Halifax House Prices YY (Mar) 2.8% vs. Exp. 3.5% (Prev. 2.90%, Rev. 2.8%); MM (Mar) -0.5% vs. Exp. 0.1% (Prev. -0.1%, Rev. -0.2%)

- German Trade Balance, EUR, SA (Feb) 17.7B vs. Exp. 17.0B (Prev. 16.0B); Imports MM SA (Feb) 0.7% vs. Exp. 0.1% (Prev. 1.2%); Exports MM SA (Feb) 1.8% vs. Exp. 1.5% (Prev. -2.5%)

- EU Sentix Index (Apr) -19.5 vs. Exp. -10.0 (Prev. -2.9)

- EU Retail Sales YY (Feb) 2.3% vs. Exp. 1.9% (Prev. 1.5%, Rev. 1.8%); Retail Sales MM (Feb) 0.3% vs. Exp. 0.4% (Prev. -0.3%)

NOTABLE EUROPEAN HEADLINES

- French PM Bayrou warned that Trump tariffs could cut France’s GDP growth by 0.5 percentage points.

- German Chancellor-in-waiting Merz’s key ally voiced optimism regarding talks with the SPD on forming the next government.

- ECB’s Schnabel said some people had the view that ‘Liberation Day” could be the day of peak uncertainty although she is not entirely sure that is the case and noted that they face a dramatic surge in uncertainty.

- ECB's Stournaras said Trump tariffs risk large Euro-area demand shock and warned the looming global trade war was likely to weigh heavily on Europe's economic growth, while he added the negative impact on Euro-area growth could be anything between 0.5 and 1ppt, according to FT.

NOTABLE US HEADLINES

- US Treasury Secretary Bessent sees no reason to anticipate a recession based on Trump tariffs and downplayed the stock market drop which he said was a short-term reaction, according to NBC News.

- US Senate passed the budget blueprint for US President Trump’s tax cuts and border agenda, sending the measure to the House.

- JP Morgan now expects real US GDP to contract under the weight of the tariffs, and for the full year (4Q/4Q), JPM now looks for real GDP growth of -0.3%, down from 1.3% previously. The recession in economic activity is projected to push the unemployment rate up to 5.3%.

- Goldman Sachs expects the Federal Reserve to begin a series of interest rate cuts in June (previously, it saw cuts in July, September, November). Under its base case, which assumes the US avoids a recession, GS now sees the Fed delivering three consecutive 25bps cuts, bringing the federal funds rate down to a range of 3.5-3.75%. GS also lifted its probability of a US recession to 45% from 35%

GEOPOLITICS

MIDDLE EAST

- Israel and UAE foreign ministers met in Abu Dhabi and discussed efforts to achieve a ceasefire in Gaza and secure the release of hostages.

- White House official said Israeli PM Netanyahu is visiting Washington on Monday.

RUSSIA-UKRAINE

- Ukraine's team will reportedly travel to the US this week to discuss the minerals deal, via Reuters citing a Ukrainian source

- Russia reportedly launched its biggest attack on Kyiv in weeks. It was separately reported that Russian troops were pushing into Ukraine’s Sumy region and troops captured Basivka in Eastern Ukraine. Furthermore, Russia's Defence Ministry said Ukraine attacked Russian energy infrastructure.

- Poland scrambled an aircraft to ensure airspace security after Russia launched strikes over Ukraine.

- Russian court cut the sentence of a jailed US soldier to three years and two months from nearly four years, according to RIA.

OTHER

- G7 Foreign Ministers expressed deep concern about China’s provocative actions, particularly recent large military drills around Taiwan.

CRYPTO

- Bitcoin has been whacked alongside the broader risk tone; currently trading around USD 75k. Ethereum posts losses to a much larger magnitude, currently below USD 1.5k.

APAC TRADE

- APAC stocks resumed last week's heavy selling as the trade war and growth concerns continued to unhinge investor sentiment, while Chinese markets slumped as the broad selling pressure rolled over into Greater China following the extended weekend and Beijing's tariff retaliation.

- ASX 200 declined heavily amid notable losses across all sectors with energy and mining stocks the worst hit owing to demand and growth-related concerns.

- Nikkei 225 slumped after futures triggered circuit breakers heading into the Tokyo open although the index was slightly off today's worst levels amid currency moves.

- Hang Seng and Shanghai Comp were hit on return from the long weekend with the former suffering double-digit losses as participants reacted to Beijing's retaliation against Trump's reciprocal tariffs in which China announced to impose tariffs of 34% on all US goods from April 10th.

NOTABLE ASIA-PAC HEADLINES

- Central Huijin, a Chinese Sovereign Fund, has added to ETF holdings and vows to increase them, via Bloomberg citing a statement.

- Japan's Keidanren Chair says they need to examine if reducing rates could be effective with real interest rates remaining still far from neutral.

- Taiwan’s financial regulator announced limits on the number of short-selling of stocks and will raise the minimum short-selling margin ratio to 130% from 90%.

- BoJ Osaka branch manager says they must scrutinise the impact of each nation's trade policy, and impact on the global economy a well as markets. Firms int he region plan solid wage hikes, proceeding with cost pass-through, hard to say how tariffs impact.

- Japanese PM Ishiba is to speak with US President Trump today at approximately 13:00BST/08:00ET.

DATA RECAP

- Chinese FX Reserves (Mar) 3.241T vs. Exp. 3.252T (Prev. 3.227T)

- Japanese Overall Labour Cash Earnings (Feb) 3.1% vs. Exp. 3.0% (Prev. 2.8%)