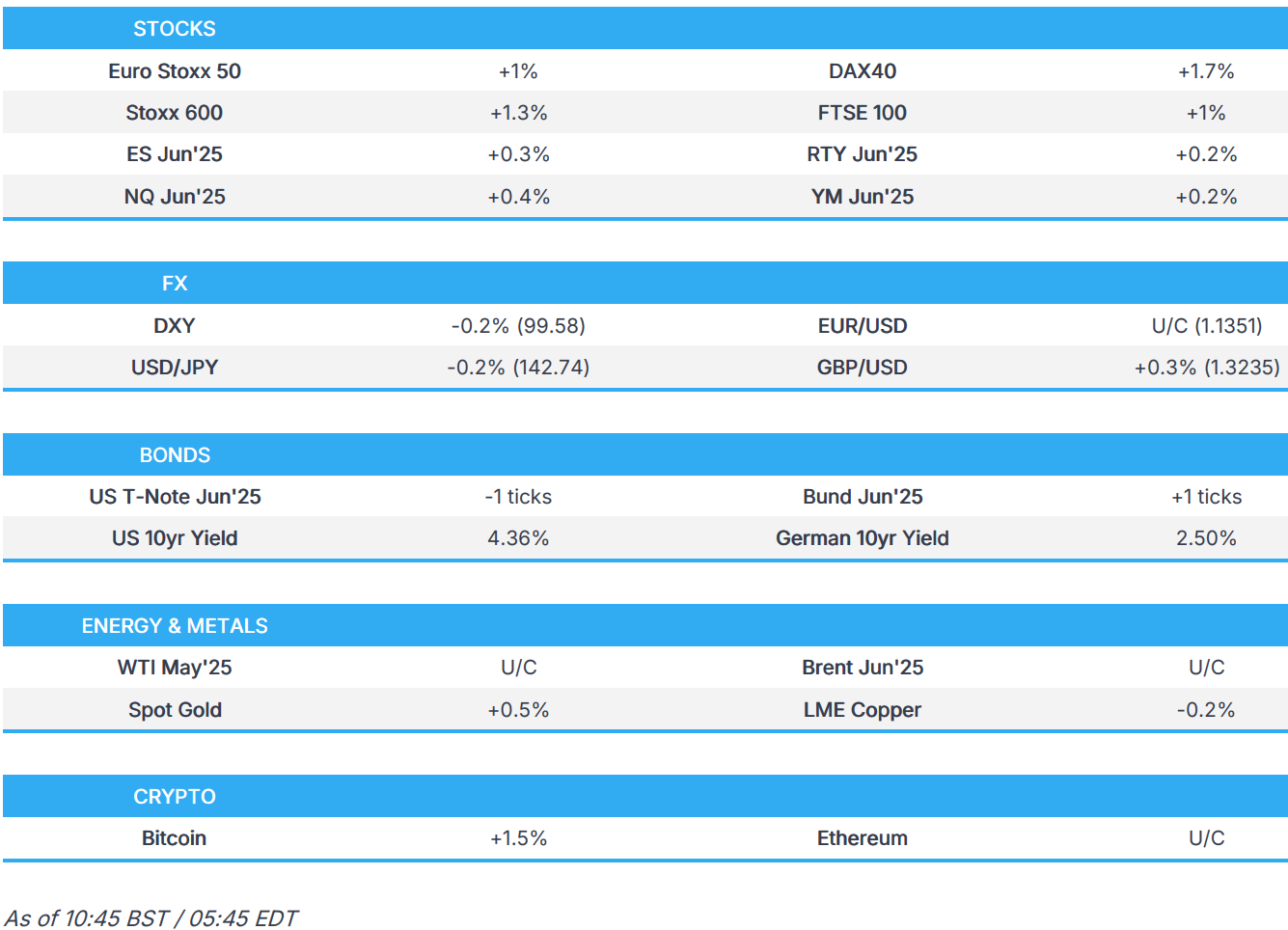

US Market Open: Generally positive sentiment but with recent pressure seen after China seeks to halt Boeing deliveries

15 Apr 2025, 11:15 by Newsquawk Desk

- China orders a halt to Boeing (BA) jet deliveries as the trade war expands, according to Bloomberg citing sources.

- US President Trump said they will put tariffs on imported pharmaceuticals in the not-too-distant future.

- European indices at session highs, LVMH -7% after weak results; US futures are modestly higher.

- DXY holds a downward bias whilst Antipodeans outperform.

- Initial fixed divergence eroded by China-Boeing. Bunds subsequently hit by a poor Bobl auction

- Gold lifted, Crude pushed into the red and Copper dented amid China trade retaliation.

- Looking ahead, US Import/Export Prices, Canadian CPI, Fed Discount Rate Minutes, Comments from ECB President Lagarde.

TARIFFS/TRADE

- China orders a halt to Boeing (BA) jet deliveries as the trade war expands, according to Bloomberg citing sources. Beijing has asked that Chinese carriers halt any purchases of aircraft-related equipment and parts from US companies Delivery paperwork and payment on some of these jets may have been completed before the reciprocal tariffs announced by China on April 11 took effect on April 12, and those planes may be allowed to enter China on a case-by-case basis, some of the people said.

- India Trade Official says the US and India have signed terms of reference for a trade deal; next round of India-EU talks are in May; India-UK trade negotiators are working to resolve pending issues

- Pakistan considers buying US crude to ease trade imbalance, via Reuters citing sources

- US President Trump said they will put tariffs on imported pharmaceuticals in the not-too-distant future and noted they do not make their own drugs, while he reiterated the EU is taking advantage of the US and has to come to the table which they're trying to. Trump also said he is looking to help car companies and there will maybe be some things coming up.

- US Treasury Secretary Bessent said US President Trump and Chinese President Xi have a very good relationship and noted that tariffs on China are big numbers and that no one thinks they are sustainable and wants them to remain. Bessent stated that tariffs on China are not a joke and that there doesn't have to be decoupling with China, but there could be and noted the US will negotiate tariff rates with partners in good faith and will run a robust process.

- US Secretary of Commerce initiated an investigation to determine the effects of national security of imports of pharmaceuticals and pharmaceutical ingredients and initiated Section 232 national security investigation of imports of semiconductors and semiconductor manufacturing equipment, according to the Federal Register.

- US Department of Commerce announced its intent to withdraw from the 2019 suspension agreement of fresh tomatoes from Mexico and with termination of the agreement, the Commerce Department will institute an anti-dumping duty order on July 14th, resulting in duties of 20.91% on most imports of tomatoes from Mexico.

- Argentina's President Milei says we understand the reciprocal tariffs from the US and are ready to sign a trade agreement along these lines.

- Chinese senior official for Hong Kong Affairs said the US tariff war goal is not to take Hong Kong's tariffs, "they want our life" and 145% tariff on Hong Kong is "brutally unreasonable, extremely shameless".

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +1%) are almost entirely in the green, as the mostly positive risk tone in the APAC session reverberates into Europe. Price action so far has really only been one way today, and that’s up; as its stands, indices reside at highs.

- European sectors hold a strong positive bias, in-fitting with the positive risk tone. Consumer Products is the sole industry in the red today – thanks to the Luxury sector, which has been hampered by poor LVMH (-7.7%) results. Autos parks itself in top spot after US President Trump said he is looking to help car companies and that there will maybe be some things coming up.

- US equity futures (ES +0.3%, NQ +0.4%, RTY +0.2%) are entirely in the green, benefiting from the risk tone which can ultimately be pinned to the recent US tariff exemptions and dovish commentary from Fed’s Waller in the prior session. Some modest downticks were seen following a Bloomberg report which noted that China orders a halt to Boeing jet deliveries amid the trade war; Boeing -3% in pre-market trade.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- The Dollar initially kicked off the session relatively contained with US (and global) tariff policy showing some stability after recent toing and froing. However, the index adopted more of a downside bias in early European trade. DXY briefly dipped under 99.50 following reports that China ordered a halt to Boeing (BA) jet deliveries as the trade war expands, according to Bloomberg citing sources. Ahead, there is little of note for the Dollar on the docket during the European session, with the focus turning (in the absence of tariff updates) to Fed Chair Powell's speech tomorrow on the economic outlook. As it stands, DXY currently resides in a 99.47-99.97 band.

- EUR is modestly firmer/flat. EUR/USD currently trades in a 1.1314-1.1378 range, well within Monday's 1.1188-1.1473 parameter. German ZEW was mixed with Current Conditions missing forecasts and Economic Sentiment contracting. ZEW highlighted that erratic changes in US trade policy are weighing heavily on German expectations. EUR saw short-lived two-way action on the data before returning to pre-announcement levels.

- JPY was modestly lower in early portion of the morning largely as a function of the positive risk environment. Though some modest strength in the JPY was seen around the aforementioned China/Boeing reporting, which weighed on risk sentiment, a move which has since continued to a current 142.69 low for USD/JPY.

- A positive session for Sterling as it remains underpinned by the softer Dollar, whilst trade updates on the US-UK front have been constructive. UK government sources via BBC have suggested that recent talks with the US on a trade deal have been making good progress. Elsewhere, UK jobs data was mixed and resulted in no immediate reaction for the Pound. GBP/USD has topped the peak from 3rd April (1.3207) and trades in a current 1.3165-1.3227 range.

- The Loonie is mildly firmer this morning as traders look ahead to the Canadian CPI prints later today which could shape expectations for tomorrow's BoC confab. Y/Y CPI is forecast at 2.6% (prev. 2.6%) whilst the Median and Trim metrics are seen ticking up to 3.0% from 2.9%.

- Antipodeans are both firmer benefitting from another leg lower in the Dollar coupled with hopes of Chinese stimulus to cushion the blow from US tariffs. The overall positive risk tone and the firmer PBoC reference rate setting also underpins the high-beta FX. The latest RBA minutes provided little fresh clues as it stated it was not yet possible to determine the timing of the next move in rates and it was not appropriate at this stage for policy to react to potential risks.

- PBoC set USD/CNY mid-point at 7.2096 vs exp. 7.3094 (Prev. 7.2110).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are in the red, with some modest pressure seen in early European trade as the general risk tone improved - this took USTs to a 110-17 low. However, the tone was clipped by a BBG source report that China has ordered a halt to Boeing deliveries, a report which lifted USTs from the mentioned trough to just above opening levels of 110-21+; as such, USTs are closer to unchanged on the session with yields slightly mixed but the curve still flatter.

- Bunds were in the green but now flat having been pulling back from its 131.57 overnight high throughout the morning as the risk tone improves, as outlined above. Down to an initial 131.18 low but was lifted off that by around 15 ticks by the aforementioned China and Boeing update. Thereafter, a weak German 2030 Bobl outing led Bunds down to a fresh 131.02 trough.

- Gilts are firmer, gapped higher by 23 ticks to 91.72 before pulling back modestly to a 91.67 trough as the tone improved. However, the discussed Boeing-China report moved the benchmark above opening levels and to a 91.93 peak. Follows the morning’s labour market data, the series didn’t really spark much movement in GBP at the time. In brief, the series points to a continued cooling of the labour market and while the employment metrics are net-dovish for the BoE, the cooling is yet to materialise significantly in wages which remain elevated. Nonetheless, the series has been superseded by more timely tariff updates. The 2035 auction was broadly in-line with the prior, a slightly lower yield on offer which tailed a touch less than last time though the cover was softer.

- UK sells GBP 4bln 4.5% 2035 Gilt: b/c 2.85x (prev. 2.92x), average yield 4.638% (prev. 4.679%), and tail 0.4bps (prev. 0.5bps).

- Germany sells EUR 3.549bln vs exp. EUR 4.5bln 2.40% 2030 Bobl: b/c 1.4x (prev. 1.90x), Average yield 2.06% (prev. 2.44%) & retention 21.1% (prev. 23.76%)

- Click for a detailed summary

COMMODITIES

- Crude began the European session modestly firmer, with upside facilitated by a softer Dollar and broadly positive risk-tone. However, more recently, the complex has gradually edged lower and now resides just off session lows. Some of the pressure could be attributed to China halting Boeing jet deliveries (hitting sentiment) and the IEA cutting its 2025 oil demand forecast. Brent Jun'25 currently towards the lower end of a USD 64.66-65.40/bbl range.

- Precious metals are mixed, with spot silver a little lower whilst spot gold edges higher. XAU currently higher by around USD 20/oz and sits above USD 3,230/oz in a USD 3,210.05-3,232.72/oz range.

- Mixed trade across base metals as traders weigh the demand impact from a US-Sino trade war with expected Chinese stimulus. That being said, some desks expected the base metals complex to continue trending lower, contingent on the scope of tariffs and the time in force. 3M LME copper resides in a 9,154.35-9,249.05/t range.

- EU is reportedly exploring legal options for ending Russian gas deals, according to FT.

- IEA OMR: cuts 2025 oil demand forecasts amid tariffs; sees 2026 surplus; cuts 2025 forecast to 730k BPD from 1.03mln BPD. Escalating trade tensions have negatively impacted the economic and oil demand outlook IEA, in first detailed look at balances for 2026, says world oil demand growth to slow further in 2026 to 690k BPD IEA cuts 2025 global supply growth forecast by 260k BPD to 1.2mln BPD due to a decrease in US and Venezuelan output

- Click for a detailed summary

NOTABLE DATA RECAP

- UK ILO Unemployment Rate (Feb) 4.4% vs. Exp. 4.4% (Prev. 4.4%); Employment Change (Feb) 206k vs. Exp. 174k (Prev. 144k); Claimant Count Unem Chng (Mar) 18.7k (Prev. 44.2k, Rev. 16.5k); HMRC Payrolls Change (Mar) -78k (Prev. 21k, Rev. -8k)

- UK Avg Earnings (Ex-Bonus) (Feb) 5.9% vs. Exp. 6.0% (Prev. 5.9%, Rev. 5.8%); Avg Wk Earnings 3M YY 5.6% vs. Exp. 5.7% (Prev. 5.8%, Rev. 5.6%)

- UK BRC Retail Sales YY (Mar) 0.9% (Prev. 0.9%); Total Sales YY (Mar) 1.1% (Prev. 1.1%)

- EU ZEW Survey Expectations (Apr) -18.5 (Prev. 39.8)

- German ZEW Economic Sentiment (Apr) -14.0 vs. Exp. 9.5 (Prev. 51.6); ZEW Current Conditions (Apr) -81.2 vs. Exp. -86.8 (Prev. -87.6)

- EU Industrial Production MM (Feb) 1.1% vs. Exp. 0.3% (Prev. 0.8%, Rev. 0.6%); Industrial Production YY (Feb) 1.2% vs. Exp. -0.8% (Rev. -0.5%)

- German Wholesale Price Index MM (Mar) -0.2% (Prev. 0.6%); YY 1.3% (Prev. 1.6%)

- French CPI (EU Norm) Final YY (Mar) 0.9% vs. Exp. 0.9% (Prev. 0.9%)

NOTABLE EUROPEAN HEADLINES

- Barclaycard UK March Consumer Spending rose 0.5% Y/Y (prev. +1.0%). It was also reported that UK consumers plan to 'buy British' amid Trump's trade war with around 71% of respondents in a survey by Barclays wanting to support UK businesses by buying items that were "made in Britain", according to FT.

- ECB Bank Lending Survey: Credit standards for loans to firms tightened slightly further, and net loan demand moved back into slightly negative territory

NOTABLE US HEADLINES

- Fed's Bostic (2027 voter) said the range of possible outcomes has multiplied and the boundaries of what he thought could be possible have been blown up. Bostic stated the labour market is effectively at full employment and inflation is still much higher than the target, as well as noted that they still have a ways to go on inflation and it is not in a position to boldly move in any direction with more clarity needed.

- US Treasury Secretary Bessent said he does not think there is a dumping of US assets in the bond market and said this is one of those occasional shocks you get in the trading community. Bessent said the US still has the global reserve currency and a strong dollar policy, as well as noted it is a long way from needing contingency plans. Furthermore, he is pleasantly surprised at how quickly the tax bill is moving along and noted that they are thinking about a successor for Fed Chair Powell with the interviewing of candidates to begin in the fall.

- White House NEC Chair Hassett said the US is in the 'sweet spot' of growth and that President Trump wants to see tariff money up front, while he does not see a recession at all, according to a Fox Business interview.

- US State Department is expected to propose an unprecedented overhaul of the US government’s diplomatic footprint overseas, including the elimination of entire embassies and consulates, according to Punchbowl

GEOPOLITICS

MIDDLE EAST

- "IRGC says Iran's military capabilities are 'red lines' in any talks with US", according to Sky News Arabia

- US State Department said Secretary of State Rubio spoke to the Turkish Foreign Minister about dangers to regional security and stability posed by Iran and its proxies.

- White House Envoy Witkoff said the conversation with Iran will be about verification on the enrichment program and then ultimately verification on weaponisation.

- Houthi media reported US warplanes launched two raids on Al-Abdiya district in Marib and three raids on the areas of Al-Juhf and Al-Qadeer in Al-Hazm District in Al-Jawf Governorate in Yemen.

- Yemeni pro-government militias are planning a ground offensive against Houthis in an attempt to take advantage of a US bombing campaign that has degraded the militant group's capabilities, according to WSJ citing Yemeni and US officials.

- "Iran is expected to oppose a US plan to transfer its stockpile of highly enriched uranium to a third country such as Russia", according to Sky News Arabia.

- Next round of Iran-US talks will be held in Muscat, Oman, on April 19th, according to IRNA. Reporting on Monday intimated that the next round would be in Italy

RUSSIA-UKRAINE

- Russian Defence Ministry says Ukraine Carried out six attacks on Russian Energy infrastructure over the past 24 hours, via Ria.

- Russia's Head of the Foreign Intelligence Service Naryshkin says in the event of NATO aggression against Russia or Belarus, damage will be inflicted on NATO as a whole; Poland and Baltic states will suffer first, according to Ria.

- Russia's Head of the Foreign Intelligence Service Naryshkin says Russia continues to comply with the moratorium on energy infrastructure strikes, according to Ria

- US President Trump said thinks they will get some very good proposals on stopping the Ukraine war very soon..

- Blasts reportedly shook the Russian city of Kursk near the Ukrainian border and damaged residential buildings.

- "Russian Foreign Minister: It is not easy to agree with the United States on the main aspects of a possible peace agreement to end the war in Ukraine", via Sky News Arabia.

OTHER

- China's embassy in Argentina said it is strongly dissatisfied and firmly opposes US Treasury Secretary Bessent's remarks about China which it said "maliciously slandered, smeared" China for carrying out normal cooperation with other countries, while it added that some people with ulterior motives are trying to sow discord between China and Argentina. Furthermore, it said they advise the US to adjust its mindset instead of spending time repeatedly smearing and attacking China, as well as meddling in the foreign cooperation of regional countries.

- China's Harbin Public Security Bureau said US NSA agents are on the wanted list for being involved in a cyberattack on the Asian Winter Games, while it traced down the three agents and two US universities involved in the implementation of cyber attacks.

CRYPTO

- Bitcoin is a little firmer and trading just shy of the USD 86k mark; Ethereum is essentially flat and trading around USD 1.6k.

APAC TRADE

- APAC stocks traded with a predominantly positive bias following on from the gains on Wall St where sentiment was underpinned by the recent US tariff exemptions and dovish comments by Fed's Waller.

- ASX 200 was led higher by strength in healthcare and financials but with the gains capped by a lack of fresh drivers and with very few clues from the RBA Minutes regarding when the next rate move will occur.

- Nikkei 225 outperformed with automakers among the best performers in the index after US President Trump suggested on Monday that he might temporarily exempt the auto industry from tariffs to give carmakers time to adjust their supply chains.

- Hang Seng and Shanghai Comp lagged with participants cautious after the US announced probes into pharmaceuticals and semiconductors, while local press noted domestic markets face liquidity pressures with more than CNY 570bln in reverse repo and MLF funds maturing this week, although the PBoC is expected to assist with liquidity.

NOTABLE ASIA-PAC HEADLINES

- RBA Minutes from the March 31st-April 1st meeting stated it is not yet possible to determine the timing of the next move in rates and it is not appropriate at this stage for policy to react to potential risks. RBA also commented that the May meeting would be an opportune time to reconsider and the decision was not predetermined, while it stated it is possible that global uncertainty over US tariffs could have a significant impact and the board saw risks on both the upside and downside for the Australian economy and inflation.