US Market Open: NQ benefits after strong TSMC results, USD firmer whilst EUR slips ahead of ECB

17 Apr 2025, 11:30 by Newsquawk Desk

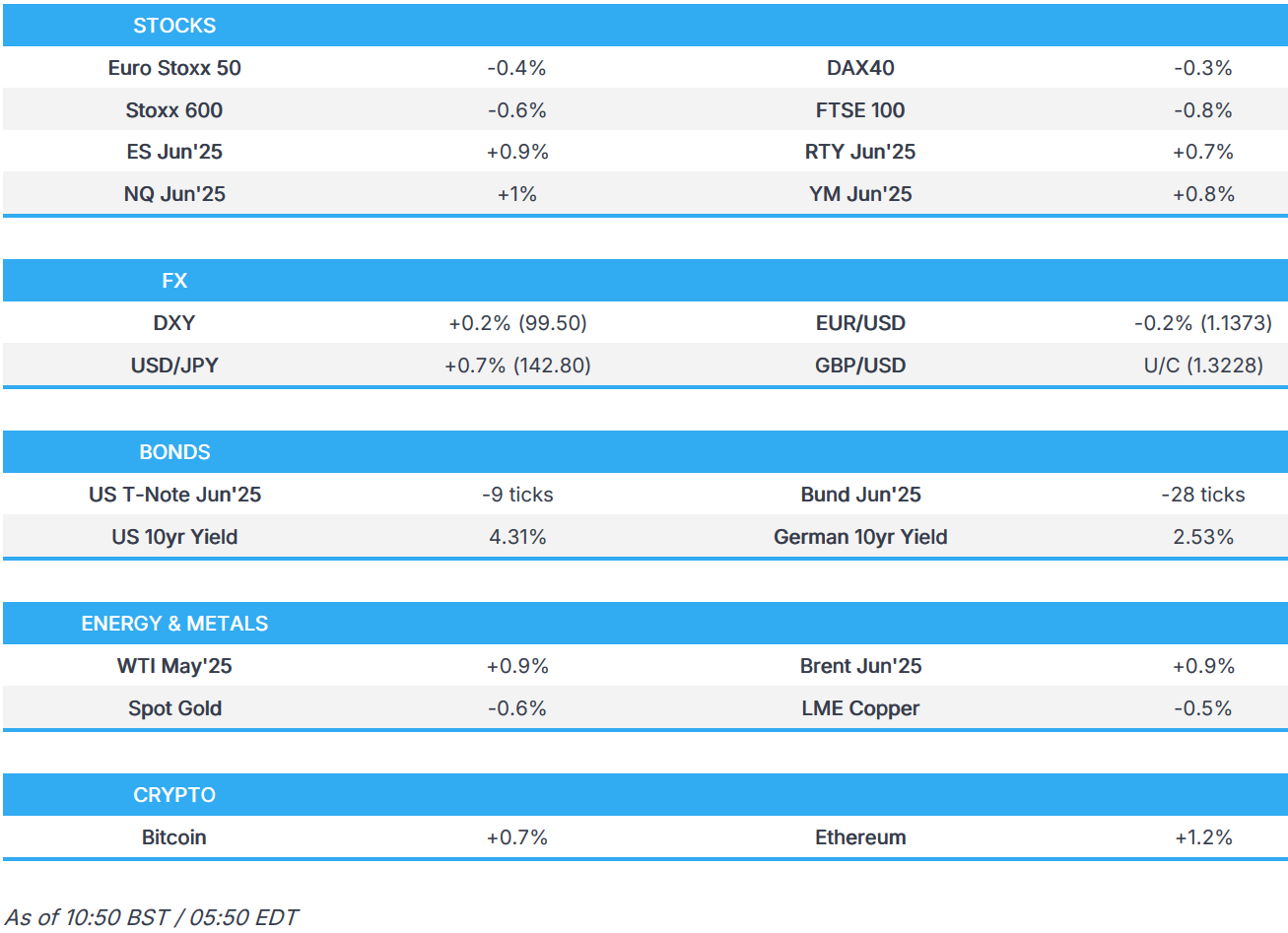

- European bourses opened mixed, but gradually slipped lower as the morning progressed; US futures positive after strong TSMC results.

- USD is attempting to claw back some of Wednesday’s losses. EUR awaits ECB rate cut.

- Bonds are softer following the robust macro tone, EGBs await the ECB.

- Crude extends on recent strength, XAU/Copper moves lower.

- Desk Closure (Good Friday Related): The desk will operate its usual schedule until Thursday April 17th 21:30BST at which point, the desk will close.

- Looking ahead, Highlights include US Jobless Claims, Philly Fed Index, ECB & CBRT Policy Announcements, Speakers including ECB President Lagarde, Fed’s Barr & Williams, Supply from the US. Earnings from TSMC, UnitedHealth, American Express, DR Horton, Netflix.

TARIFFS/TRADE

- US President Trump posted on Truth Social "A Great Honor to have just met with the Japanese Delegation on Trade. Big Progress!".

- Japanese Economy Minister Akazawa said he told US negotiation counterparts that Japan wants the best solution as soon as possible for both nations and strongly requested the revocation of tariffs on Japan. Akazawa said they agreed to hold a second meeting this month and he believes the US wants a deal within the 90-day window but added that he has no idea how talks will progress going forward.

- Japanese PM Ishiba said the Economy Minister reported to him that constructive talks were held with the US, while Ishiba added that of course talks will not be easy going forward and he will visit the US at an appropriate time to meet with US President Trump.

- Intel (INTC) told Chinese clients last week that chips would require a licence for exporting to China if the chips met certain requirements, according to FT.

- UK officials are said to be tightening security when handling sensitive trade documents to shield them from the US amid the tariff war, according to Guardian sources.

- White House officials believe a trade deal with Britain can be finalised within three weeks, according to Telegraph sources.

- China's MOFCOM says it is willing to expand a mutual opening up with Europe, maintaining normal communication with US counterparts, China is open to negotiations with the US in economic and trade areas.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.5%) opened mixed, but have gradually succumbed to selling pressure to display a negative picture in Europe. Positive updates related to US-Japan trade and strong TSMC results have failed to lift sentiment.

- European sectors hold a negative bias, in-fitting with the broader risk tone. Consumer Products is towards the top of the pile, as traders digest the latest Luxury updates. There have been earnings releases from three high-fashion brands today; Moncler (-1.8%, Q1 topped expectations amid strong Asia demand), Brunello Cucinelli (U/C, in-line figures and maintained guidance), Hermes (-1.9%, Q1 beat but said will implement price hikes in US to offset tariffs).

- US equity futures (ES +0.9%, NQ +1%, RTY +0.7%) are entirely in the green, attempting to pare back some of the hefty losses seen in the prior session. Sentiment today in the US has also been lifted by a positive Q1 earnings report from TSMC.

- TSMC (2330 TT / TSM) Q1 (TWD) Net Profit 361.6bln (exp. 354.6bln), Op. Profit 407.1bln (prev. 249bln Y/Y), Revenue 839.3bln (prev. 592.6bln Y/Y). Forecasts Q2 revenue between USD 28.4-29.2bln (exp. 26.4bln); sees Q2 gross margin 57-59% (prev. 58.8% in Q1); sees Q2 operating margin 47-49% (prev. 48.5% in Q1); says overseas fabs will impact TSMC margins. Not seen any change in customer behaviour because of US tariffs. FY Guidance maintained. Notes of very strong AI demand from US customers like Apple (AAPL), need to expand capacity in the US.

- NVIDIA (NVDA) CEO Huang says China is a very important market for NVIDIA, hope to continue to cooperate with China, via CCTV. Elsewhere, CEO Huang reportedly met clients in Beijing, including DeepSeek founder, to discuss new chip designs for Chinese customers, according to FT sources; he then held separate talks with Chinese Vice Premier Li. CEO says US tightening of chip export controls has a significant impact on the company's business, via Chinese State media; will resolutely provide services to the Chinese market.

- LVMH (MC FP) CEO says 2025 started well but worsened from March amid economic turmoil linked to tariffs

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is attempting to claw back some of Wednesday's lost ground. Markets continue to digest Wednesday's remarks by Fed Chair Powell who noted that the Fed wishes to wait for greater clarity before considering any change to its policy stance. For today's docket, weekly claims data will be eyed for signs of labour market weakening. DXY sits towards the bottom-end of Wednesday's 99.17-100.104 range.

- EUR softer vs. the USD in the run-up to the ECB policy announcement which is widely expected to see policymakers pull the trigger on a 25bps reduction in the Deposit Rate to the upper end of its neutral rate at 2.25%. EUR/USD sits towards the top end of yesterday's 1.1281-1.1412 range.

- USD/JPY has re-emerged from beneath the 142.00 level after dipping to a fresh seven-month low overnight at 141.62 with the rebound supported by the positive APAC risk appetite and after weaker-than-expected Japanese exports and imports data. Overnight, BoJ Governor Ueda stated that Japan's real interest rates remain very low and the BoJ is expected to keep raising interest rates if the economy and prices move in line with projections made in the quarterly report.

- GBP is flat vs. the USD and more resilient than peers. Fresh macro drivers for the UK are on the light side asides from a report in The Telegraph that UK PM Starmer is reportedly closing in on a new partnership with the EU that could put a trade deal with the White House at risk. GBP/USD is currently steady on a 1.32 handle and in a 1.3204-56 range.

- Antipodeans are both softer vs. the broadly stronger USD after a solid showing yesterday. AUD saw little follow-through from a mixed Australian labour market report in which employment change fell short of expectations and the unemployment rate came in below consensus.

- PBoC set USD/CNY mid-point at 7.2085 vs exp. 7.3083 (Prev. 7.2133).

- Click for a detailed summary

FIXED INCOME

- USTs are softer, with benchmarks coming under pressure early doors as the general risk tone improved after strong TSMC numbers. Prior to this, a bearish bias was already in-play as APAC shrugged off the Wall St. lead and climbed, with focus on Trump’s positive commentary on trade with Japan. The US-Japan progress weighed on JGBs, resulting in them briefly underperforming overnight alongside a long-dated JGB liquidity auction. Currently at a 111-02+ low and around 15 ticks from the overnight high. Ahead, Weekly Claims, Philly Fed, Building Permits/Housing Starts & Baker Hughes.

- Bunds are directionally in-fitting with the above. EGBs await the ECB where a 25bps cut is expected and entirely priced. Focus for the meeting will be on how Lagarde and Co. approach the tariff uncertainty, and the two-way impulses on growth and inflation. Bunds are at a 130.91 base, around 30 ticks from overnight highs and just below Wednesday’s 131.02 low. To the downside, support factors at 130.75, 130.24 and 129.92 from the three sessions prior.

- Gilts are tracking the above, UK specifics and the docket ahead on the lighter side as markets focus on events within Europe and the US. On the trade front, the only update for the UK has been a piece in The Telegraph whose sources report that the White House believes a trade deal with Britain can be finalised within around three weeks.

- France sells EUR 12bln vs exp. EUR 10-12bln 2.40% 2028, 2.70% 2031, 2.00% 2032 OAT

- Click for a detailed summary

COMMODITIES

- Crude is firmer with prices extending on Wednesday's gains after the US issued fresh Iran-related sanctions targeting oil tankers, while Treasury Secretary Bessent noted that the Trump administration has made it clear that they will apply maximum pressure on Iran and disrupt the regime’s oil supply chain and exports. WTI resides in a USD 62.61-63.51/bbl range while Brent sits in a USD 65.95-66.77/bbl parameter.

- Softer price action across precious metals following yesterday's run higher. Spot gold mildly pulled back after recently printing a fresh record high with the precious metal above the USD 3,300/oz level in a current 3,314.30-3,357.77/oz range - the top end being another record high.

- Copper futures are choppy but ultimately faded some of the recent gains as risk sentiment in its largest buyer lagged overnight. 3M LME copper resides in a 9,134.00-9,237.85/t range.

- Click for a detailed summary

NOTABLE DATA RECAP

- German Producer Prices MM (Mar) -0.7% vs. Exp. -0.1% (Prev. -0.2%); YY -0.2% vs. Exp. 0.4% (Prev. 0.7%)

NOTABLE US HEADLINES

- US House Energy and Commerce Committee is targeting May 7th, for a markup of its portion of the Republican reconciliation package, via Punchbowl citing sources

- BofA Week-April 12th Total Card Spending +2.3% Y/Y (vs +1.1% on avg. in March); notes that the increase could be due to a dual boost from the upcoming easter and front-loading due to tariff uncertainty.

- Fed's Schmid (2025 voter) said there is a lot of nervousness in the agricultural sector from tariffs but noted he's an optimist and they need to be patient to see how it plays out, while he said they will react to disruptions that might affect mandates.

- White House seeks to cut USD 40bln in funding for the Department of Health and Human Services, according to The Washington Post.

GEOPOLITICS

- "Lebanese media: Low flight of Israeli drones in the airspace of the capital Beirut and the southern suburbs", according to Sky News Arabia.

- "Iranian media: Saudi defense minister arrives today in Tehran for talks with senior Iranian officials", according to Sky News Arabia.

- "The response to the Israeli proposal will confirm the rejection of any partial agreement to stop the war", via Asharq News.

- US President Trump waved off a planned Israeli strike on Iranian nuclear sites in favour of negotiating a deal with Iran to limit its nuclear program, according to the New York Times.

CRYPTO

- Bitcoin is on a firmer footing and trades just above the USD 84k mark; Ethereum currently around USD 1.6k.

APAC TRADE

- APAC stocks shrugged off the negative handover from Wall St. but with gains capped amid a lack of bullish drivers and as trade uncertainty lingered.

- ASX 200 was led higher by strength in energy and mining stocks following recent gains in underlying commodity prices and as participants digest quarterly updates from the likes of BHP, South32 and Santos.

- Nikkei 225 reclaimed the 34,000 status amid favourable currency moves and with US President Trump suggesting big progress was made in US-Japan trade talks.

- Hang Seng and Shanghai Comp conformed to the positive mood but with the gains in the mainland limited by the ongoing US-China trade frictions, while officials from MOFCOM, MIIT and the PBoC are set to hold a briefing on Monday where China will announce an expansion plan for its service sector.

NOTABLE ASIA-PAC HEADLINES

- China is to announce an expansion plan for its service sector at a briefing on Monday with officials from MOFCOM, MIIT and the PBoC to attend the briefing, while the Finance Ministry held a meeting with experts on international economic conditions.

- US House panel is probing whether DeepSeek used restricted NVIDIA (NVDA) chips, according to FT

- BoJ Governor Ueda said Japan's economy is recovering moderately albeit with some weak signs, while he added that Japan's economy and prices moving roughly in line with their forecasts but they must be vigilant to heightening uncertainty including from each country's trade policy. Ueda also stated that Japan's real interest rates remain very low and the BoJ is expected to keep raising interest rates if the economy and prices move in line with projections made in the quarterly report. Furthermore, he said when the BoJ raised rates in January, the US economy was in solid shape and markets had been stable but added that uncertainty surrounding US policy, particularly on tariffs, has heightened sharply recently, as well as noted that US tariffs could exert downward pressure on the economy and reiterated that keeping low rates even when underlying inflation is accelerating could result in a situation where we would be forced to hike rapidly.

- BoJ's Nakagawa said US tariff policy, as well as overseas economic and market developments, are among risks to Japan's economic outlook, while uncertainty over US tariffs could affect household and corporate sentiment, and Japan's economy and prices.

- Bank of Korea kept its base rate unchanged at 2.75%, as expected, with the rate decision not unanimous as board member Shin Sung-Hwan dissented and saw a need to respond to the worsening economic outlook. BoK said uncertainties to the growth path are higher and headwinds to economic growth are seen bigger than previously expected, while it will determine the timing and pace of any further base rate cuts and noted that monetary easing policy stance is to continue. BoK Governor Rhee said most board members saw lower interest rates in the three months ahead and they will factor in the interest rate differential with the US for the next rate decision. Furthermore, Rhee said they will assess in May whether the policy rate needs to go below 2.25% by year-end.

DATA RECAP

- Japanese Trade Balance (JPY)(Mar) 544.1B vs. Exp. 485.3B (Prev. 584.5B, Rev. 590.5B)

- Japanese Exports YY (Mar) 3.9% vs. Exp. 4.5% (Prev. 11.4%)

- Japanese Imports YY (Mar) 2.0% vs. Exp. 3.1% (Prev. -0.7%)

- Australian Employment (Mar) 32.2k vs. Exp. 40.0k (Prev. -52.8k)

- Australian Unemployment Rate (Mar) 4.1% vs. Exp. 4.2% (Prev. 4.1%)

- New Zealand CPI QQ (Q1) 0.9% vs. Exp. 0.7% (Prev. 0.5%)

- New Zealand CPI YY (Q1) 2.5% vs. Exp. 2.3% (Prev. 2.2%)

- New Zealand RBNZ Sectoral Factor Model Inflation Index YY (Q1) 2.9% (Prev. 3.1%)