US Market Open: Positive risk tone with stocks in the green, TSLA +6.5% after CEO Musk signals a step back from DOGE

23 Apr 2025, 11:05 by Newsquawk Desk

- US President Trump said the Fed should lower interest rates and would like the Fed chair to be early or on time, adds no intention of firing the Fed chair and wants Powell to be more active on rates.

- European bourses move higher as US Treasury Secretary Bessent and the latest Trump comments on Powell boost sentiment; TSLA +6.3% in pre-market trade after Musk signals stepping back from DOGE following dismal earnings.

- USD mixed vs. peers with Antipodeans leading given the positive risk tone.

- US and German paper diverges on account of trade updates and Trump comments on Powell.

- Industrial commodities higher on optimism, spot gold unwinds risk premium.

- Looking ahead, highlights include US PMIs, IMF/World Bank Spring Meeting, Speakers including BoE’s Bailey & Breeden, ECB's Lane & Cipollone, Fed's Goolsbee, Musalem & Hammack, RBA's Bullock, Supply from the US.

- Earnings include, Boeing, AT&T, Vertiv, Phillip Morris, GE Vernova, Alaska Air, IBM, Chipotle, ServiceNow, Texas Instruments & Lam Research.

TRADE

TARIFFS/TRADE

- "China: Door wide open for trade talks with US", according to Sky News Arabia

- US President Trump said they are doing fine with China and are going to be very nice with China, while he added that they have to make a deal and if they don't, the US will set a deal. Trump also stated the tariff on China will not be as high as 145% and will not be anywhere near that level but it won't be zero.

- US is preparing negotiating terms for UK trade talks and will aim for the UK to reduce its automotive tariff from 10% to 2.5%, while the US will also push the UK to relax rules on agricultural imports from the US, including beef and revise rules of origin for goods from each nation, according to Wall Street Journal citing sources.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +1.8%) are entirely in the green and with clear outperformance in the DAX 40, which benefits from upside in SAP (+9%) after its Q1 results. A slew of EZ PMIs and the latest ECB Wage Tracker had little impact on the complex.

- Sentiment in Europe has been lifted in continuation of the upside on Wall Street, in the prior session. The strength follows some positive trade related updates, including; a) US Treasury Secretary Bessent expecting the tariff standoff with China to de-escalate, b) US President Trump saying he has no intention to fire Fed Chair Powell.

- European sectors hold a clear cyclical bias, in-fitting with the risk tone. Tech is the clear outperformer, with the industry lifted by post-earning strength in SAP. Optimised Personal Care and Utilities, two defensive sectors, find themselves at the foot of the pile.

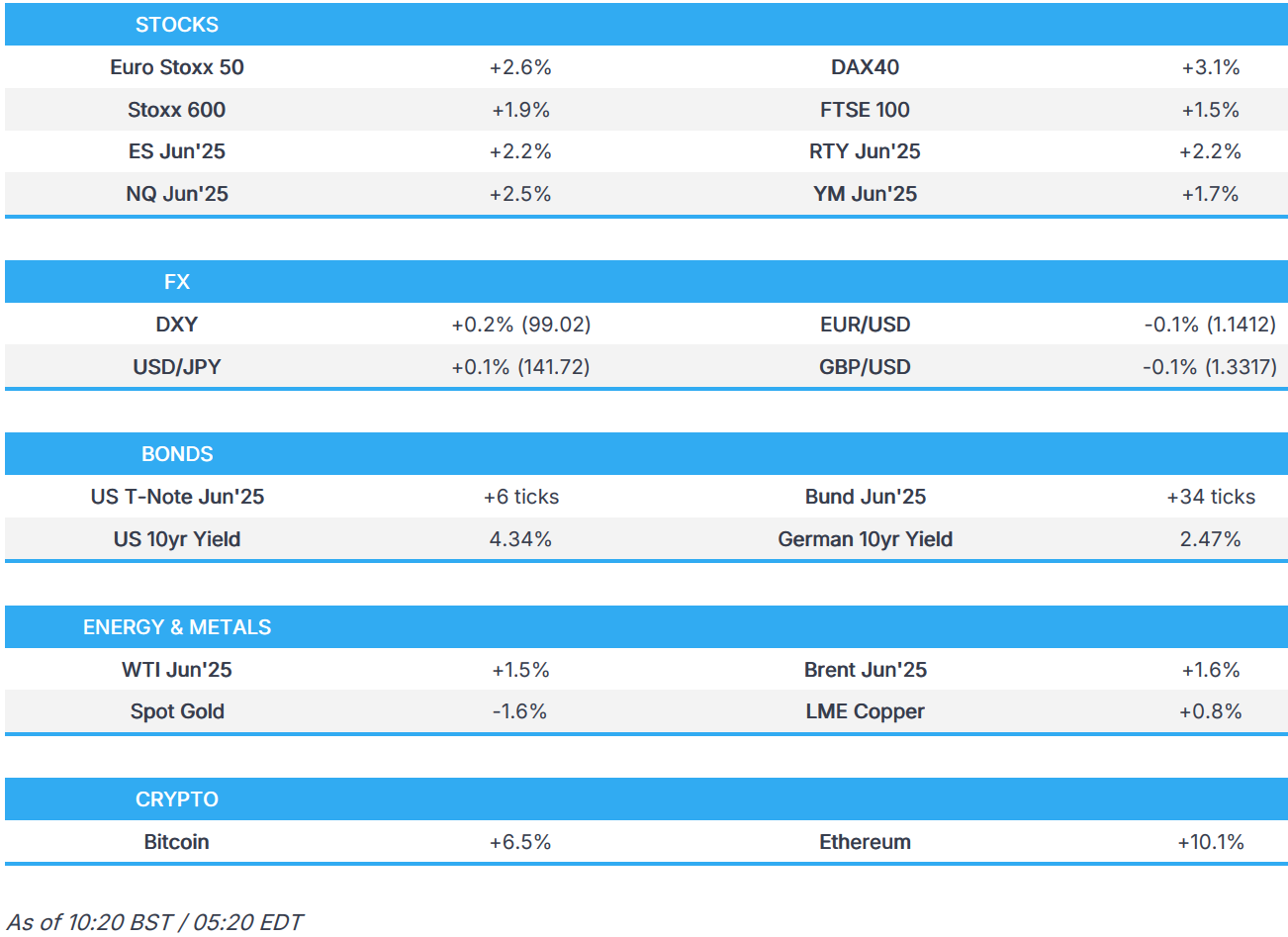

- US equity futures (ES +2.2% NQ +2.5% RTY +2.2%) are entirely in the green today, with modest outperformance in the NQ as the risk-tone improves and after Tesla gains post-earnings; currently higher by around 6.3% in pre-market trade.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is up vs. most peers (ex-Antipodeans) with markets encouraged by two primary inputs. 1) optimism around the trade war following more upbeat comments from US President Trump overnight, reporting yesterday suggesting that Treasury Secretary Bessent sees the current levels of tariff on China as unsustainable and comms from the White House that it is nearing deals with China and India. 2) comments by US President Trump overnight that whilst we wishes for the Fed to lower rates, he is not looking to fire Powell. For today's docket, focus will be on US PMI data and Fed speak from Goolsbee, Musalem, Waller, Hammack. DXY sits towards the top end of Tuesday's 98.01-99.65 range.

- EUR is on the backfoot vs. the USD on account of the current trade optimism with the EUR suffering as its viewed as a liquid alternative to the USD. PMI metrics this morning from France, Germany and the Eurozone have all conformed to the same picture of beats on manufacturing, services and composite missed. EUR/USD has delved as low as 1.1309 before recovering to levels closer to 1.14.

- JPY is a touch softer vs. the USD but notably less so than seen during APAC hours where the pair hit a peak at 143.21 overnight as markets reacted to the positivity on the trade front and comments by US President Trump on Fed Chair Powell. On the trade front, it remains the case that Japan is front of the queue at the White House and comms suggest that a trade agreement to stave off large US tariffs is nearing. USD/JPY is currently holding above the top end of Tuesday's 139.88-141.67 range.

- GBP is on the backfoot vs. the USD with losses briefly exacerbated by a soft outturn for UK PMI metrics which saw the services print unexpectedly slip into contractionary territory, dragging the composite reading with it. Elsewhere, on the trade front, reports state that the US is preparing negotiating terms for UK trade talks and will aim for the UK to reduce its automotive tariff from 10% to 2.5%, while the US will also push the UK to relax rules on agricultural imports from the US. Cable delved as low as 1.3235 overnight before recovering to levels just above the 1.33 mark.

- Antipodeans are the G10 outperformers vs the Dollar, benefiting from the broader risk tone. AUD/USD is yet to reapproach Tuesday's YTD peak at 0.6439. If breached, the 200DMA sits at 0.6470. Similar price action for NZD/USD which sits below yesterday's YTD high at 0.6029.

- PBoC set USD/CNY mid-point at 7.2116 vs exp. 7.3466 (Prev. 7.1980).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are bid with markets encouraged by two primary inputs. 1) optimism around the trade war following more upbeat comments from US President Trump overnight, reporting on Tuesday suggesting that Treasury Secretary Bessent sees the current levels of tariff on China as unsustainable and comms from the White House that it is nearing deals with China and India. 2) comments by US President Trump overnight that whilst we wishes for the Fed to lower rates, he is not looking to fire Powell. Focus now turns to US PMI, a slew of Fed speakers and 2yr FRN and 5yr auctions - as a reminder, Tuesday's 2yr outing was soft. Jun'25 contract has ventured as high as 111.00+ with the next resistance point coming from the 21st April peak at 111.09.

- Bunds are diverging from their US peers on account of the more encouraging risk tone and increased positivity on the trade front. From a data perspective, PMI metrics this morning from France, Germany and the Eurozone have all conformed to the same picture of beats on manufacturing, services and composite missed. A couple of ECB speakers are on the docket, with focus also on a 2035 Bund auction. Jun'25 Bunds briefly slipped below Tuesday's low at 131.46 before stabilising above the 131.50 mark.

- Gilts are diverging from European peers following the latest update from the DMO which saw it cut GBP 10.4bln from its planned sales of long-dated Gilts and increase sales of short Gilts by GBP 5.6bln. Upside was briefly extended following a soft outturn for UK PMI metrics which saw the services print unexpectedly slip into contractionary territory, dragging the composite reading with it. Jun'25 Gilts have been as high as 92.85 with little in the way of resistance until 93.00. From a yield perspective, the 10yr has bottomed out at 4.515%, failing to test 4.50% to the downside.

- UK DMO revises its 2024/25 Gilt remit to GBP 299.1bln (prev. 299.2bln); cuts GBP 10.4bln from planned sales of long-dated Gilts, increases sales of short gilts by 5.6bln; increases unallocated portion of Gilt issuance remit by GBP 4.7bln Increases net T-bill issuance to GBP +10bln (prev. +5bln).

- Click for a detailed summary

COMMODITIES

- Firmer trade across the crude complex with optimism was facilitated by the more sanguine language from the US regarding China, whilst US President Trump also dialled down his tone regarding the dismissal of Fed Chair Powell, which, in turn, boosted risk sentiment. WTI currently resides in a USD 63.76-64.84/bbl range while its Brent counterpart trades in a USD 67.68-68.63/bbl parameter.

- Mixed trade across precious metals, with spot silver outperforming following yesterday's underperformance. Investors are unwinding some risk premium from gold following the more sanguine language from the US regarding China, whilst US President Trump also dialled down his tone regarding the dismissal of Fed Chair Powell, in turn boosting risk sentiment. Spot gold trades in a USD 3,291.73-3,386.77/oz range.

- Firmer trade across base metals amid the constructive risk tone, although gains overnight were limited by the unambitious performance in Chinese equities. 3M LME copper currently resides in a USD 9,380.60-9,483.73/t range.

- IEA Executive Director Birol said oil prices may see further downward pressure, via Bloomberg TV; expects oil demand to slow down.

- Shanghai Futures Exchange to adjust the transaction fees for Gold's June future contract.

- Azerbaijan said average oil price seen at USD 70bbl in 2025 (prev. forecast USD 77bbl).

- Norway's Prelim March oil production 1.757mln BPD (prev. 1.723mln BPD); Gas production 10.9bcm (prev. 9.9bcm).

- Iran set May Iranian light crude price to Asia at Oman/Dubai plus USD 1.65/bbl.

- Peru's Antamina copper mine reported the death of an operations manager in an incident at the mining camp, while Antamina launched a total shutdown for security as it investigates the accident.

- Corporation National del Cobre de Chile market intelligence and strategy specialist Eric Medel said the upside potential of copper has been reduced and copper prices are likely to remain bearish in the short term amid trade war risks.

- Click for a detailed summary

NOTABLE DATA RECAP

-

EU HCOB Composite Flash PMI (Apr) 50.1 vs. Exp. 50.3 (Prev. 50.9); HCOB Manufacturing Flash PMI (Apr) 48.7 vs. Exp. 47.5 (Prev. 48.6); HCOB Services Flash PMI (Apr) 49.7 vs. Exp. 50.5 (Prev. 51).

- French HCOB Manufacturing Flash PMI (Apr) 48.2 vs. Exp. 48.0 (Prev. 48.5); HCOB Services Flash PMI (Apr) 46.8 vs. Exp. 47.6 (Prev. 47.9); HCOB Composite Flash PMI (Apr) 47.3 vs. Exp. 47.8 (Prev. 48).

- German HCOB Composite Flash PMI (Apr) 49.7 vs. Exp. 50.4 (Prev. 51.3); HCOB Manufacturing Flash PMI (Apr) 48.0 vs. Exp. 47.6 (Prev. 48.3); HCOB Services Flash PMI (Apr) 48.8 vs. Exp. 50.2 (Prev. 50.9).

- ECB Wage Tracker: 2025 Estimate 3.055% (prev. estimate 3.251%). Q1 4.640% (prev. estimate 4.820%). Q2 3.879% (prev. estimate 4.442%). Q3 2.133% (prev. estimate 2.249%). Q4 1.620% (prev. estimate 1.547%).

- UK Flash Manufacturing PMI (Apr) 44.0 vs. Exp. 44 (Prev. 44.9); Composite PMI (Apr) 48.2 vs. Exp. 50.4 (Prev. 51.5); Flash Services PMI (Apr) 48.9 vs. Exp. 51.5 (Prev. 52.5).

- UK PSNB Ex Banks GBP (Mar) 16.444B GB vs. Exp. 16.0B GB (Prev. 10.71B GB, Rev. 12.310B GB); PSNB, GBP (Mar) 16.444B GB vs. Exp. 16.0B GB (Prev. 10.71B GB, Rev. 12.310B GB); PSNCR, GBP (Mar) 2.694B GB (Prev. 6.357B GB, Rev. 6.360B GB).

NOTABLE EUROPEAN HEADLINES

- UBS lowers its 2025 global GDP growth forecast to 2.5% (prev. forecast 2.9%)

NOTABLE US HEADLINES

- US President Trump said the Fed should lower interest rates and would like the Fed chair to be early or on time, while he has no intention of firing the Fed chair and wants Powell to be more active on rates.

- Fed's Kugler (voter) said tariff increases are significantly larger than previously expected and economic effects of tariffs and uncertainty will likely be larger than anticipated. Kugler added that Fed policy is well-positioned for macroeconomic changes and she supports holding the policy rate steady as long as upside risks to inflation continue, whilst economic activity and employment remain stable.

GEOPOLITICS

MIDDLE EAST

- Israeli army said it monitored the launch of a missile from Yemen towards Israeli territory and air defence systems were activated, according to Sky News Arabia.

- Iranian Foreign Ministry Spokesperson said the new US energy sanctions contradict Washington's claims of dialogue with Tehran.

RUSSIA-UKRAINE

- UK government said Ukraine peace talks with international foreign ministers have been postponed, via AFP.

- Ukrainian Foreign Ministry said the Chinese ambassador was summoned and told of 'serious concern' over Chinese involvement on Russia's side in the war.

- US President Trump's "final offer" for peace requires Ukraine to accept Russian occupation, according to Axios. It was also reported that the US proposed recognising Crimea as Russian as peace talks ramp up and proposals include eventually lifting sanctions against Russia under a future accord, according to WaPo.

- UK Foreign Secretary Lammy said the UK is working with the US, Ukraine and Europe for peace and to put an end to Russian President Putin's illegal invasion, while he added that talks continue at a pace and officials will meet in London today.

- Russian President Putin reportedly offered to halt the invasion of Ukraine across the current front line as part of efforts to reach a peace deal with US President Trump, according to FT.

- Russia launched a large drone attack on east, south and central Ukraine, which damaged civilian infrastructure, according to regional officials.

CRYPTO

- Bitcoin is a strong footing and now sits comfortably above USD 93.5k; Ethereum also extends gains and looks to test USD 1.8k to the upside.

- US President Trump said crypto needs regulatory certainty and newly appointed SEC chair Atkins is perfect for certainty in regulating cryptocurrency. It was also reported that US SEC Chairman Atkins said it is time for SEC to end waywardness and keep politics out of securities laws, while he added there are clear rules of the road and the top priority is to have a firm foundation for digital assets.

APAC TRADE

- APAC stocks rallied amid tailwinds from the US owing to trade deal hopes and after US President Trump softened his rhetoric on Fed Chair Powell in which he stated he has no intention of firing the Fed chair.

- ASX 200 was led higher by outperformance in energy and tech with the former supported by a rebound in oil prices and after a quarterly production update from Woodside Energy, while gold miners suffered after the precious metal dropped as the risk-on mood sapped haven demand.

- Nikkei 225 benefitted from initial currency weakness and briefly surged to above the 35,000 level shortly after the open before fading some of its advances.

- Hang Seng and Shanghai Comp were varied as the Hong Kong benchmark joined in on the broad rally and the mainland was contained despite the encouraging comments from Treasury Secretary Bessent who noted the tariff standoff with China is unsustainable and expects the situation to de-escalate, while President Trump said they are going to be very nice with China and that the tariff on China will not be anywhere near the 145% level.

NOTABLE ASIA-PAC HEADLINES

- Chinese Foreign Ministry said the US cannot say that it wishes to reach an agreement whilst on the other hand maintaining extreme pressure; this is not the correct way to deal with China.

- BoJ Financial System Report said Japan's financial system has been maintaining stability as a whole; Considering that Japanese banks have a certain amount of market risk associated with stockholdings, developments in asset prices warrant attention Since the beginning of April, financial markets at home and abroad have fluctuated significantly. Financial institutions need to be vigilant against materialization of various risks.

- China's Commerce Ministry said China received the EU side's appeal request on intellectual property rights case and will handle it in accordance with relevant rules, while China will work with other multi-party interim arbitration arrangement participants to firmly uphold the rules-based multilateral trading system.

DATA RECAP

- Japanese JibunBK Manufacturing PMI Flash SA (Apr) 48.5 (Prev. 48.4)

- Japanese JibunBK Services PMI Flash SA (Apr) 52.2 (Prev. 50)

- Japanese JibunBK Composite Op Flash SA (Apr) 51.1 (Prev. 48.9)

- Australian S&P Global Manufacturing PMI Flash (Apr) 51.7 (Prev. 52.1)

- Australian S&P Global Services PMI Flash (Apr) 51.4 (Prev. 51.6)

- Australian S&P Global Composite PMI Flash (Apr) 51.4 (Prev. 51.6)