US Market Open: US equity futures & USD modestly firmer with focus on reports of Trump easing auto tariff impact, Canada’s Liberals win election

29 Apr 2025, 11:15 by Newsquawk Desk

- US President Trump is expected to soften the impact of his automotive tariffs, according to WSJ citing sources.

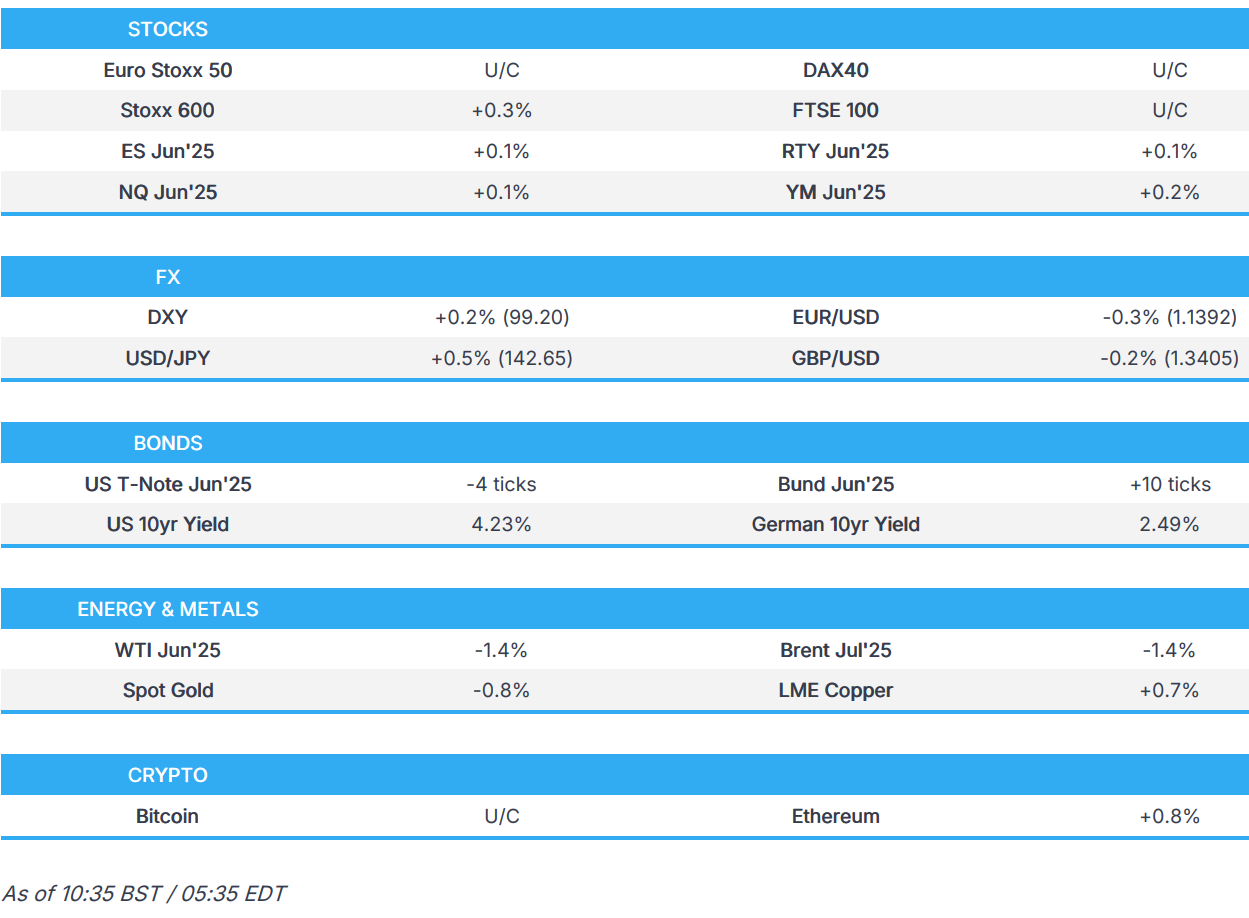

- European bourses are mixed, whilst US equity futures trade incrementally higher, ahead of a slew of earnings.

- USD attempts to claw back some of Monday’s losses, CHF & JPY lags whilst the Loonie fares better post-election.

- Canada's ruling Liberals, led by Mark Carney, won the national election but will need to form a minority government.

- Fixed benchmarks are relatively contained into a packed US session.

- Crude complex is on the backfoot, continuing recent losses, while base metals diverge.

- Looking ahead, US Consumer Confidence, Advance Goods Trade, JOLTS Job Openings, Speakers including BoE’s Ramsden, SNB’s Martin & US Treasury Secretary Bessent.

TARIFFS/TRADE

- US President Trump is expected to soften the impact of his automotive tariffs by preventing duties on foreign-made cars from stacking on top of other tariffs he imposed and easing some levies on foreign parts used to manufacture cars in the US, according to WSJ citing sources. Furthermore, a White House official said those actions are expected on Tuesday and Commerce Secretary Lutnick said President Trump is building an important partnership with both the domestic automakers and American workers, while Lutnick added this deal rewards companies who manufacture domestically, as well as provides a runway to manufacturers who have expressed commitment to invest in America and expand their domestic manufacturing.

- Chinese Foreign Minister Wang Yi said concession and retreat will only make the bully more aggressive.

- China's MOFCOM said on the report that Boeing flew back three 737 MAX planes to be delivered to Chinese airlines, that China and the US have maintained long-term mutually beneficial cooperation in the field of civil aviation, while it added the US wielded the big stick of tariffs to seriously impact the stability of global industrial and supply chains, and many enterprises were unable to carry out normal trade and investment activities.

- Italian PM Meloni says times are not mature yet for an EU-US summit, according to Corriere Della Sera.

EUROPEAN TRADE

EQUITIES

- European bourses opened modestly firmer/flat, but some modest pressure crept into the complex as the morning progressed – with indices generally off best levels, to show a mixed picture in Europe.

- European sectors hold a slight positive bias, albeit with the breadth of the market fairly narrow. Basic Resources takes the top spot, followed closely by Media and Banks. Energy is found at the foot of the pile, dragged down by post-earning losses in BP (-4%); the continued pressure in the crude complex is also not helping.

- Autos find themselves towards the middle of the bunch. For the sector more generally, US President Trump is expected to soften the impact of his automotive tariffs, by preventing duties on foreign-made cars from stacking on top of other tariffs he imposed and easing some levies on foreign parts used to manufacture cars in the US, via WSJ. For stock specifics, Porsche AG (-5%) dips after it cut FY25 guidance; Volvo Car (-8.3%) reported a significant miss on its EBIT and Revenue figure and launched a SEK 18bln cost and cash action plan.

- US equity futures are incrementally firmer, following a tentative trading session in the prior day. In terms of key pre-market movers; NXP Semiconductor (-7%, Q2 guidance light and CEO to retire), Nucor (-0.5%, Q1 beat and positive Q2 guidance).

- Earnings include: HSBC (+1.8%) beat, buyback & dividend; AstraZeneca (-2.5%) mixed, reiterates guidance; BP (-4%) miss and soft vs. prior, buyback at lower-end of forecasts; Adidas (+0.5%) in-line with prelim, cannot produce almost any product in the US currently; Deutsche Bank (+1.6%) beat; Porsche AG (-5%) cuts guidance; Novartis (+0.9%) beat, strong momentum, lifts guidance; Carlsberg (-1.5%) slight miss, affirms guide; Volvo Cars (-8.3%) miss, withdraws guidance.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is attempting to claw back some of yesterday's losses that were in part driven by a soft outturn for Dallas Fed Manufacturing data. On the trade front, US President Trump is expected today to announce measures to soften the impact of his automotive tariffs by preventing duties on foreign-made cars from stacking on top of other tariffs, according to WSJ. DXY has risen as high as 99.31 but is yet to venture near Monday's best at 99.83.

- EUR/USD has faded some of its recent gains and failed to sustain the 1.1400 status with recent price action largely driven by moves in the greenback. Spanish CPI metrics which printed hotter-than-expected on a Y/Y, M/M and core basis. EUR/USD is currently contained within Monday's 1.1329-1.1425 range.

- USD/JPY marginally rebounded from support around the 142.00 level after sliding yesterday owing to the early initial risk aversion and lower US yield environment but with the recovery limited in the absence of Japanese participants. USD/JPY has ventured as high as 142.57 but is some way off Monday's opening level at 143.57.

- GBP is a touch softer after Monday's session of outperformance which didn't appear to be driven by any obvious catalyst. BoE's Ramsden is due later; Cable matched its YTD high printed yesterday at 1.3444 before pulling back.

- Antipodeans are both softer vs. the greenback amid a lack of pertinent newsflow out of Australia and New Zealand. That will change tomorrow for AUD with Australian Q1 CPI due on deck.

- CAD in focus after Canada's ruling Liberals, led by Mark Carney, won the national election. However, the outcome was closer than predicted by polls and will require the party to form a minority government. Accordingly, initial support for CAD has faded as markets reprice away from expectations of a majority government. USD/CAD currently sits towards the bottom end of yesterday's 1.3816-92 range.

- Canada's ruling Liberals led by Mark Carney won the national election but will need to form a minority government, according to CTV.

- PBoC set USD/CNY mid-point at 7.2029 vs exp. 7.2781 (Prev. 7.2043).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained start for fixed income given the Japanese holiday (Showa Day) overnight, meaning that there was no cash trade. USTs currently at the lower-end of a very thin 111-22 to 111-30 band and one that is within Monday’s 111-10 to 111-31 confines. Focus ahead is on, US Consumer Confidence, Advance Goods Trade and JOLTS Job Openings.

- Bunds is modestly firmer. On the data front, Spain’s inflation printed hotter-than-expected across the board and sent Bunds to a 131.16 low with Alphabet’s presence in the market perhaps also weighing. Thereafter, Bunds have recovered a touch and are back into the green and just off a 131.46 session high; a high that printed as the European risk tone came under a little bit of pressure after the Russian Kremlin said Ukraine has not responded to its latest ceasefire proposal.

- Gilts are flat given the lack of leads from sparse overnight trade and a European morning that has been devoid of UK-specifics aside from earnings. At the lower end of a 92.96 to 93.25 band, comfortably within Monday’s 92.79 to 93.33 range. BoE's Ramsden is due later.

- UK sells GBP 900mln 1.25% 2054 I/L Gilt: b/c 3.31x (prev. 3.06x) & real yield 2.175% (prev. 2.126%).

- Italy sells EUR 7.5bln vs exp. EUR 6.5-7.5bln 2.95% 2030, 3.60% 2035 BTP & EUR vs exp. EUR 1.5-2.0bln 2033 CCTeu.

- Alphabet (GOOGL) kicks of debut sale of EUR debt 4yr IPTs mid-swaps +85bps area. 8yr IPTs mid-swaps +105bps area. 12yr IPTs mid-swaps +125bps area.

- Click for a detailed summary

COMMODITIES

- Crude is on the backfoot, extending on the prior day's losses; there has been little by way of fresh oil-specific newsflow, so focus has been on updates out of Russia/Ukraine; most recently, Russia's Kremlin suggested Ukraine had not responded to offers to commence negotiations. Brent July'25 currently trades in a USD 63.62-64.81/bbl range.

- TTF is lower on the day, after finishing Monday’s session modestly higher, surrounding a number of updates including the blackout in Spain and a three-day ceasefire proposal from Russia. With Spain and Portugal’s blackout almost fully resolved today’s attention now shifts to Russia's ceasefire proposal, announced for May 8th-11th. As it stands, Russia says Ukraine is not responding to the proposal.

- Spot gold continues its reversal from recent record highs, with a number of risk events ahead including US consumer confidence and pivotal speakers such as Commerce Secretary Lutnick and Treasury Secretary Bessent who are likely to speak on auto tariffs. Thus far, today’s low has been recorded at USD 3,314/oz, with a high of USD 3,359/oz.

- Copper is a little firmer after a broad base metals bid this morning, lifting it from near session lows of USD 9,368/t, to session highs of USD 9,455/t, currently holding just off best levels.

- Spain's PM said the government will release 3 days worth of strategic oil reserves, while the grid operator later restored nearly all power.

- China's copper supplies are on track to be depleted in just a few months as the market suffers one of the greatest tightening shocks due to fears of US tariffs, according to commodities trading house Mercuria cited by FT.

- Kazakhstan Q1 oil exports +7% Y/Y to 1.63mln BPD, according to Reuters calculations and official data.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK BRC Shop Price Index YY (Apr) -0.1% vs Exp. -0.2% (Prev. -0.4%)

- German GfK Consumer Sentiment (May) -20.6 vs. Exp. -26.0 (Prev. -24.5, Rev. -24.3)

- Spanish HICP Flash MM (Apr) 0.6% vs. Exp. 0.4% (Prev. 0.70%); CPI MM Flash NSA (Apr) 0.6% vs. Exp. 0.4% (Prev. 0.10%)

- Spanish CPI YY Flash NSA (Apr) 2.2% vs. Exp. 2.0% (Prev. 2.30%); Core 2.4% (prev. 2.0%)

- EU Money-M3 Annual Growth (Mar) 3.6% vs. Exp. 4.0% (Prev. 4.0%); Loans to Non-Fin (Mar) 2.3% (Prev. 2.2%); Loans to Households (Mar) 1.7% (Prev. 1.5%)

- EU Services Sentiment (Apr) 1.4 vs. Exp. 2.2 (Prev. 2.4, Rev. 2.2); Economic Sentiment (Apr) 93.6 vs. Exp. 94.5 (Prev. 95.2, Rev. 95.0); Industrial Sentiment (Apr) -11.2 vs. Exp. -10.1 (Prev. -10.6, Rev. -10.7); Consumer Confid. Final (Apr) -16.7 vs. Exp. -16.7 (Prev. -16.7); Selling Price Expec (Apr) 11.0 (Prev. 11.4, Rev. 11.3); Cons Infl Expec (Apr) 29.6 (Prev. 24.4, Rev. 24.5)

- Italian Manufacturing Business Confidence (Apr) 85.7 vs. Exp. 85.4 (Prev. 86.0, Rev. 86.0); Consumer Confidence (Apr) 92.7 vs. Exp. 94.0 (Prev. 95.0)

- Italian Industrial Sales YY WDA (Feb) -1.5% (Prev. 1.7%); Industrial Sales MM SA (Feb) -0.4% (Prev. 3.8%)

NOTABLE EUROPEAN HEADLINES

- ECB Consumer Expectations Survey: March: See inflation in next 12 months at 2.9% (prev. 2.6%); 3y ahead sees 2.5% (prev. 2.4%); 12-month is highest since April 2024. Economic growth expectations for the next 12 months were stable in March, standing at -1.2%.

- ECB's Cipollone says that ECB staff estimates suggest that the recently observed increase in financial market volatility might imply lower GDP growth of about 0.2ppts in 2025.

NOTABLE US HEADLINES

- US President Trump posted on Truth "As we reach our Historic First 100 Days, I am proud to announce that the Presidential Personnel Office has surpassed 80% of all Political Hires across our largest Departments, including the United States Department of Justice, State, Defense, Treasury, Veterans Affairs, and Commerce." Trump also posted "The USA lost Billions of Dollars A DAY in International Trade under Sleepy Joe Biden. I have now stemmed that tide, and will be making a fortune, very soon. Stay tuned as we MAKE AMERICA GREAT AGAIN!!!"

- White House said US President Trump wants tax cuts in this reconciliation package, while it was separately reported that Treasury Secretary Bessent said he hopes the Trump tax bill can be done by July 4th.

- US Treasury Financing Estimates (Q2): expects to borrow USD 514bln in privately-held net marketable debt, assuming end of June cash balance of 850bln (prev. guided USD 123bln, assuming end of June cash balance USD 850bln).

GEOPOLITICS

MIDDLE EAST

- US President Trump intends to extend the two-month deadline allocated for US-Iran negotiations, according to Israel Hayom citing Israeli officials

- Gaza talks in Cairo are said to be witnessing a "significant breakthrough" and parties agreed on a number of issues including consensus on a long-term ceasefire in Gaza, although some sticking points remain including Hamas arms, according to Reuters citing two Egyptian sources.

RUSSIA-UKRAINE

- Explosions were heard in Kyiv after the Ukraine air force issued air raid alerts and air defence systems were engaged in repelling a Russian air attack.

- Russian Kremlin says Ukraine has not responded to many offers by President Putin to commence negotiations without any preconditions, according to Tass Direct talks with Ukraine need to commence, adding this is primary and the legitimacy of Zelensky is secondary. 30-day ceasefire is impossible without settling all the nuances.

CRYPTO

- Bitcoin is a little firmer and trading around USD 94.8k; Ethereum holds around USD 1.8k.

APAC TRADE

- APAC stocks were mostly in the green but with some of the gains capped following the choppy performance stateside and in holiday-thinned conditions with Japanese markets closed for a holiday, while reports that US President Trump is expected to soften the impact of his automotive tariffs saw a muted reaction.

- ASX 200 gained amid outperformance in the energy, tech and resources sectors, while miners were also lifted as participants digested output updates.

- Hang Seng and Shanghai Comp were varied as the mainland lagged owing to uncertainty from the US-China trade war with US Treasury Secretary Bessent recently commenting that it is up to China to de-escalate and that he has an "escalation ladder in his back pocket", while China's Foreign Ministry reiterated its denial regarding a Trump-Xi call and Foreign Minister Wang Yi warned that compromise and backing down would only embolden the bully.

NOTABLE ASIA-PAC HEADLINES

- Japan and Malaysia are reportedly exploring broader economic ties including AI and automotive.

- Alibaba (9988 HK) introduced Qwen3 to set a new benchmark in open-source AI with hybrid reasoning.

- Earthquake of magnitude 5.0 strikes China's Tibet region, via CENC.

- Agricultural Bank (1288 HK) Q1 (CNH) Revenue 186bln (exp. 185bln), Net Income 72.1bln (exp. 73.95bln), +2.2% Y/Y, NII 140.6bln (exp. 142.7bln), CET1 11.23%.

- Industrial and Commercial Bank of China (1398 HK) Q1 (CNH) NII 156.78bln (exp. 161.29bln), Net Income 84.70bln, -4% Y/Y.

- China Construction Bank (939 HK) Q1 (CNH) NII 141.92bln, NIM 1.41%.

- Bank of China (3988 HK) Q1 (CNY) Net 54.36bln (exp. 57.4bln), NIM 1.29%, Operating Income 165bln (exp. 155bln)