US Market Open: USD softer whilst US equity futures gain ahead of US NFP, AMZN/AAPL dip post-earnings

02 May 2025, 10:57 by Newsquawk Desk

- China is said to be conducting an assessment on US trade negotiations and urged the US to demonstrate sincerity for trade talks, while it urged the US to correct mistakes regarding tariffs and noted it is currently evaluating possible US trade talks.

- US Secretary of State Rubio said the Chinese want to meet and talk, while he added those talks will come up soon and there's a broader question about how much we should buy from China going forward

- Japanese Finance Minister Kato said Japan's huge US Treasury holdings are among the tools it can wield in trade negotiations with the US but added that whether Japan wields that card is a different question.

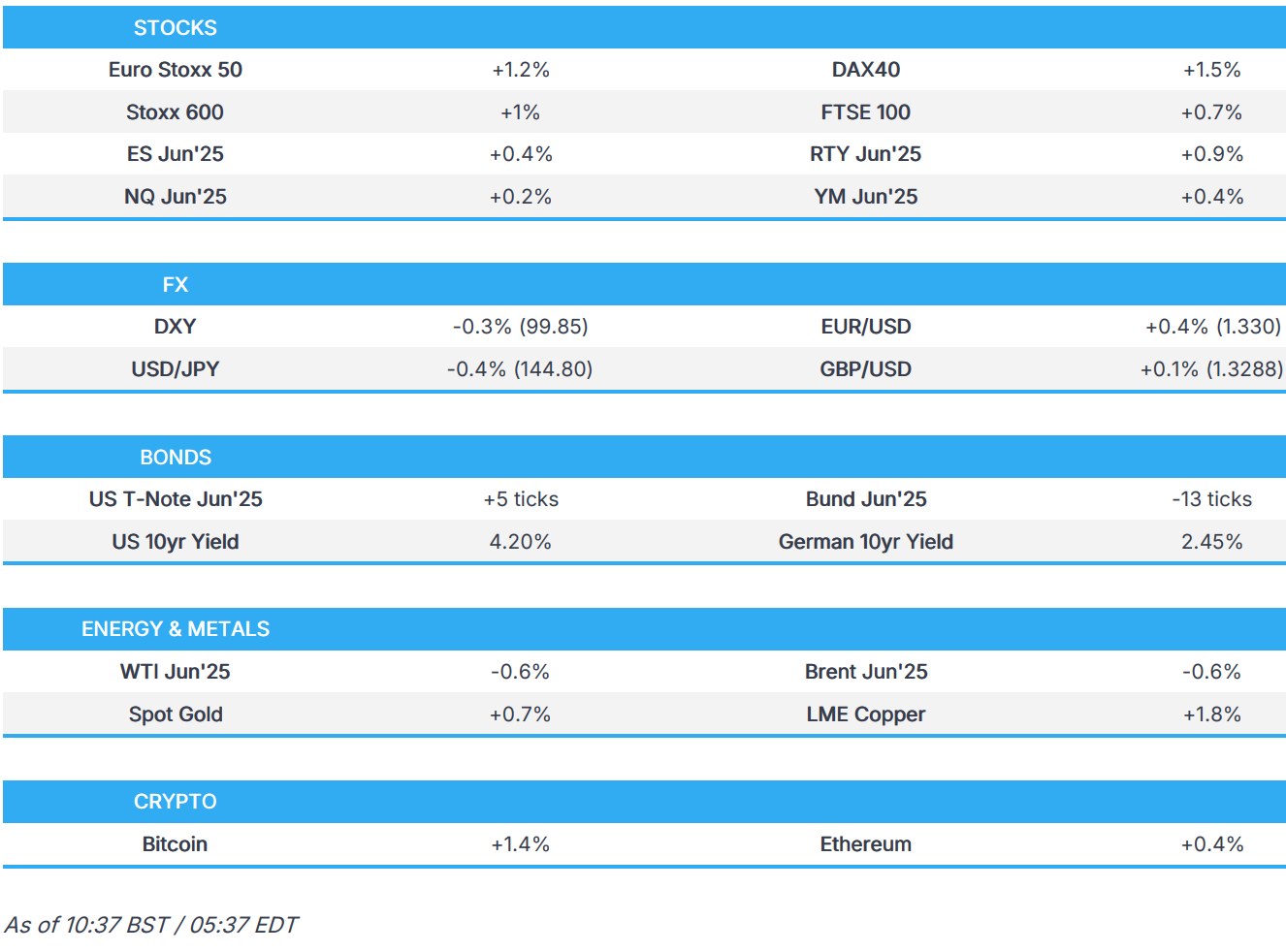

- European bourses are entirely in the green as the region returns from holiday; US equity futures gain, AMZN -2% & AAPL -2.7% pre-market.

- USD's recovery pauses for breath as markets brace for NFP, AUD outperforms.

- Gilts outperform, EGBs largely unaffected by HICP, USTs digest trade updates & Kato's remarks into NFP.

- Crude is on the backfoot, whilst XAU and base metals benefit from the softer Dollar.

- Looking ahead, US NFP & Durable Goods, Earnings from Exxon Mobil, Chevron, Apollo, Brookfield.

TARIFFS/TRADE

- US Department of Commerce launched the Section 232 steel and aluminium inclusions process which allows US manufacturers and trade associations to request the inclusion of new derivative articles under Section 232 steel and aluminium tariffs, according to a statement cited by Reuters.

- De minimis exception for products from China and Hong Kong imported to the US is now voided, as scheduled.

- US Secretary of State Rubio said the Chinese want to meet and talk, while he added those talks will come up soon and there's a broader question about how much we should buy from China going forward.

- China is said to be conducting an assessment on US trade negotiations and urged the US to demonstrate sincerity for trade talks, while it urged the US to correct mistakes regarding tariffs and noted it is currently evaluating possible US trade talks.

- China's MOFCOM said the tariff and trade war was unilaterally initiated by the US and the US should show its sincerity in talks, while it added the US has repeatedly expressed its willingness to negotiate with China on the tariff issue and has recently taken the initiative to convey information to the Chinese side through relevant parties on several occasions, hoping to talk with the Chinese side. MOFCOM added that China’s position has always been the same: 'talk, the door is open,' as well as noted the US should show sincerity if it wants to talk and that in any possible dialogue or meeting if the US does not correct its unilateral tariff measures, it has no sincerity at all. Furthermore, it stated the US should be prepared to take action in correcting erroneous practices and cancelling unilateral tariffs.

- Japanese PM Ishiba said there is no change at all to Japan’s stance of requesting the US to cancel tariffs, while he added they are not in a situation where common ground has been found yet but he received a report from Economic Minister Akazawa that talks were forward-looking. Furthermore, Ishiba commented that reaching a deal in haste is not necessarily in the best interest.

- Japanese Finance Minister Kato said Japan's huge US Treasury holdings are among the tools it can wield in trade negotiations with the US but added that whether Japan wields that card is a different question.

- Japan's Economic Minister Akazawa said that US tariff negotiations lasted for 130 minutes and they were able to have a thorough discussion in which repeated its request for a review of tariffs on Japan, while they talked about how Japan can expand trade, non-tariff measures and economic security with the US. Akazawa said they told the US that tariff measures are regrettable and they want to hold the next meeting after mid-May, while they asked the US to review tariff measures on auto parts and the negotiation was handled as a package. Furthermore, they did not talk about China during the talks and he understands that the US wants to reach some kind of agreement within the 90-day window with various countries.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +1%) are entirely in the green as the region returns from holiday; sentiment today has been boosted following a strong session on Wall Street in the prior session, and mostly positive APAC trade overnight. Price action has been relatively rangebound and near recent highs, with traders ultimately cautious ahead of the day's key US NFP report.

- European sectors hold a strong positive bias; Tech tops the pile, followed closely by Industrials (lifted by post-earning strength in Airbus) whilst Utilities is found at the foot of the pile.

- A number of banks reported today; Standard Chartered (+1%, strong Q1 results), ING (+4.5%, reported record deposit growth and launched EUR 2bln share buyback), Danske Bank (+4%, strong results across the board and guidance range topped expectations), NatWest (+1.9%, Q1 headline figures beat expectations and suggested 2025 income to be at top-end of guidance range).

- US equity futures are firmer but with modest underperformance in the NQ vs. peers as traders digest the latest earnings from Apple and Amazon.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

NOTABLE EARNINGS

- Apple Inc (AAPL) Q2 2025 (USD): EPS 1.65 (exp. 1.62), Revenue 95.36bln (exp. 94.53bln), authorises USD 100bln buyback, Greater China rev. 16bln (exp. 16.97bln); Shares -2.7% premarket

- Amazon.com Inc (AMZN) Q1 2025 (USD): EPS 1.59 (exp. 1.38), Revenue 155.7bln (exp. 154.88bln). Q2 25 revenue view 159-164bln (exp. 161.62bln); Shares -2% premarket

- Airbnb (ABNB) Q1 2025 (USD): EPS 0.24 (exp. 0.23), Revenue 2.3bln (exp. 2.26bln); Shares -4.5% premarket

- Reddit Inc (RDDT) Q1 2025 (USD): EPS 0.13 (exp. 0.01), Revenue 392.4mln (exp. 369.0mln); Shares +6.5% premarket

- Shell (SHEL LN) Q1 (USD) Adj. EPS 0.92 (exp. 0.95), Adj. profit 5.58bln (exp. 5.09bln), Adj. EBITDA 15.25bln (exp. 15.06bln). Shell announces a USD 3.5bln buyback. Net debt 41.52bln (exp. 38.98bln)

FX

- USD is currently softer vs. all major peers with DXY snapping a run of 3 consecutive sessions of gains which have in part been driven by the recent recovery in US risk assets. This in part has been driven by the performance of corporate America in Q1 earnings season and hopes of a US-China trade deal. On the former, reports suggest that China is conducting an assessment on US trade negotiations and evaluating possible US trade talks. DXY currently sits within Thursday's 99.61-100.37 range.

- EUR firmer vs. the USD and one of the better performers across the majors. From a fundamental perspective, attention has been on comments from EU negotiator Sefcovic who said Europe is ready to make US President Trump an offer, in which Brussels wants to increase purchases of US goods by EUR 50bln to address the “problem” in the trade relationship. On the data front, EZ HICP Flash metrics incrementally topped expectations, but ultimately had little impact on the Single-Currency.

- USD/JPY initially extended on the prior day's BoJ-spurred upward momentum but then pulled back from resistance just shy of the 146.00 level. There was little reaction seen following reports of US-Japan tariff talks or comments from Japanese Finance Minister Kato who said Japan's huge US Treasury holdings are among tools it can wield in trade negotiations with the US but added whether Japan wields that card is a different question. More recently, a report in the Nikkei suggested that US trade negotiators presented a framework for an agreement with Japan, however, Japan strongly opposed the proposal. In recent trade USD/JPY has dipped below the 145.00 mark.

- GBP is firmer vs. the USD but modestly so and below the opening levels of the week despite the notable rally on Monday. Price action for Cable has largely been at the whim of the Greenback with incremental macro drivers for the UK exceptionally light aside from some upbeat commentary on the prospects of a UK-US trade deal.

- Antipodeans are both firmer and supported by the current risk-environment which has been underpinned by hopes of a potential US-China trade deal (China is both nation's largest trading partner). AUD has overlooked disappointing Australian Retail Sales data and is looking ahead to Saturday's federal election with PM Albanese seen as likely to secure a second term.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are contained into NFP. The headline is expected to show a marked cooling in the pace of Payrolls to 130k (prev. 228k), with a range of 25-195k. The report will be scoured for signs of Trump’s tariffs and associated reciprocal measures impacting the US labour market. USTs holding around 112-00 in 111-23+ to 112-01+ confines, a tick below Thursday’s base but some way clear of that session’s 112-20 peak; the high occurred in the early US morning, before the ISM release. On the trade front, US trade relations with constructive reports in the FT around EU concessions to address the trade deficit with the US in addition to reports that the US has reached out to China to seek talks alongside constructive MOFCOM language.

- Elsewhere, the Japanese Finance Minister stated that Japan’s holdings of USTs could be “among such cards” used in trade negotiations, though Kato added “whether we actually use that card, however, is a different question”. Little move was seen in USTs at the time.

- Bunds opened near enough unchanged at 131.75 after the Labour Day holiday. Just after the resumption of trade they lifted to a 131.81 peak for the session before slipping as low as 131.34 in the early European morning as participants reacted to the US-China updates overnight. Thereafter, lifted around 25 ticks from that low but remained in the red and held around that mark into data. EZ HICP came in hotter across the board and the ex-Food & Energy measures eclipsed the forecast range alongside Services jumping to 3.9% (prev. rev. 3.5%); Bunds knee jerked lower but remained well within earlier confines and have since pared the entire move and are back to holding off lows but remain in the red by around 10 ticks.

- Gilts opened lower by around 20 ticks, catching up to the slight bearish bias in APAC hours on the points outlined in USTs. Thereafter, the benchmark began to inch its way higher and is currently modestly outperforming at the top-end of a 93.30-91 band, just eclipsing Thursday’s 93.88 high. In terms of the slight outperformance, there isn’t a clear or overt headline driver behind it and instead it may be a function of Gilts not being capped/weighed on in the way that USTs and EGBs are by progress on trade talks.

- Click for a detailed summary

COMMODITIES

- The crude complex opened with a positive bias, continuing the upside seen in the prior session, which stemmed from the broader risk-on sentiment and after Trump's latest Iran threats. As the session progressed, the complex has been gradually cooling off those highs, to currently trade lower by around USD 0.40/bbl. Brent July'2025 currently trades in a USD 61.72-62.72/bbl range.

- Precious metals are broadly in the green, benefiting from the softer Dollar. XAU/USD is firmer today, attempting to make back some of its recent losses; currently higher by around USD 21/oz, in a USD 3,227.67-3,263.36/oz range.

- Base metals hold a strong positive bias, benefitting from the positive risk tone and the softer Dollar. Sentiment has also been boosted as both US and China suggested a willingness by the other side for talks. 3M LME Copper currently +1.8%, and trading within a USD 9,241.95-9,411.15/t range.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HICP Flash YY (Apr) 2.2% vs. Exp. 2.1% (Prev. 2.2%); services inflation 3.9% (prev. 3.5%)

- EU HICP-X F, E, A, T Flash MM (Apr) 1.00% (Prev. 1.00%); HICP-X F&E Flash YY (Apr) 2.7% vs. Exp. 2.5% (Prev. 2.5%); HICP-X F,E,A&T Flash YY (Apr) 2.7% vs. Exp. 2.5% (Prev. 2.4%)

- EU Unemployment Rate (Mar) 6.2% vs. Exp. 6.1% (Prev. 6.1%, Rev. 6.2%)

- EU HCOB Manufacturing Final PMI (Apr) 49.0 vs. Exp. 48.7 (Prev. 48.7)

- German HCOB Manufacturing PMI (Apr) 48.4 vs. Exp. 48.0 (Prev. 48.0)

- French HCOB Manufacturing PMI (Apr) 48.7 vs. Exp. 48.2 (Prev. 48.2)

- Italian HCOB Manufacturing PMI (Apr) 49.3 vs. Exp. 47.0 (Prev. 46.6)

- Swiss Manufacturing PMI (Apr) 45.8 vs. Exp. 48.6 (Prev. 48.9)

- French Budget Balance (Mar) -47.03B (Prev. -40.3B)

- Italian Unemployment Rate (Mar) 6.0% vs. Exp. 6.0% (Prev. 5.9%)

NOTABLE EUROPEAN HEADLINES

- UK by-election: Reform wins Runcorn and Helsby by a margin of six votes with 38.7% of the total vote.

NOTABLE US HEADLINES

- US President Trump is planning to release his FY 2026 budget on Friday, according to Axios. It was separately reported that President Trump is to propose slashing USD 163bln in government programs in budget blueprint, according to WSJ.

- US Envoy told NATO allies that US President Trump may skip the NATO summit, via Spiegel; Trump may not attend if there is no 5% spending target agreement

GEOPOLITICS

MIDDLE EAST

- "Israel understood from Washington that if it decides to strike Iran, it will most likely do so alone as long as the nuclear negotiations continue", according to Sky News Arabia citing AP quoting an Israeli official

- Israeli PM Netanyahu said Israel attacked a target last night near the Syrian presidential palace in Damascus.

- Israeli Home Front said Northern Israel is under rocket attack from Yemen, according to Al Jazeera.

- Houthi-affiliated media reported US warplanes targeted the Yemeni capital Sana'a, according to Sky News Arabia.

- US Secretary of State Rubio said this is the best opportunity for Iran and that Iran should not be afraid of inspectors including Americans, according to a Fox News interview.

RUSSIA-UKRAINE

- Ukrainian PM says two of the three documents on US minerals deal will not need ratification, according to a member of parliament.

- Ukraine's Parliament plans ratification vote on US minerals deal on May 8th, according to a lawmaker cited by Reuters.

- US VP Vance said Russia's war in Ukraine is not going to end anytime soon. It was separately reported that US Secretary of State Rubio said Ukraine and Russia's positions are still a little far apart, while he added it's going to take a breakthrough soon on Ukraine to make this possible or else the President will have to decide how much time to dedicate to this.

CRYPTO

- Bitcoin is on a stronger footing and holds just above USD 96.5k; Ethereum edges higher and resides around USD 1.8k.

- UK FCA plans to stop retail investors from borrowing money to invest in crypto, according to the FT.

APAC TRADE

- APAC stocks traded mostly higher as many regional participants returned from the Labor Day holiday and with some hopes for US-China trade talks.

- ASX 200 gained with the advances led by outperformance in the energy sector following the upside in oil prices and with a continuation of the status quo seen as the outcome in tomorrow's federal election with Australian PM Albanese highly favoured to win a second term.

- Nikkei 225 rallied at the open but is off intraday highs after stalling near the 37,000 level and following a surprise increase in Japan's unemployment rate.

- Hang Seng outperformed on return from the holiday closure and despite the continued absence of mainland participants, while there were reports that China is currently evaluating possible US trade talks and noted that the US has repeatedly expressed its willingness to negotiate with China on the tariff issue, although it urged the US to demonstrate sincerity for trade talks and correct its unilateral tariff measures.

NOTABLE ASIA-PAC HEADLINES

- China-linked group was accused of meddling in Australia's election with the Chinese Communist Party-linked Australia Hubei Association said to have mobilised volunteers to support an independent candidate ahead of Saturday's federal election in Australia, according to Nikkei.

DATA RECAP

- Japanese Unemployment Rate (Mar) 2.5% vs. Exp. 2.4% (Prev. 2.4%); Jobs/Applicants Ratio (Mar) 1.26 vs. Exp. 1.25 (Prev. 1.24)

- Australian PPI QQ (Q1) 0.9% (Prev. 0.8%); YY (Q1) 3.7% (Prev. 3.7%)

- Australian Retail Sales MM Final (Mar) 0.3% vs. Exp. 0.4% (Prev. 0.2%)

- Australian Retail Trade (Q1) 0.0% vs. Exp. 0.3% (Prev. 1.0%)