US Market Open: Crude sinks after OPEC+ hikes supply, US equity futures & USD lower into ISM Services

05 May 2025, 11:35 by Newsquawk Desk

- US President Trump said he is willing to lower tariffs on China at some point. He answered no when asked if he plans to speak with Chinese President Xi this week.

- US President Trump reiterated that the Fed should lower interest rates and said he won’t remove Fed Chair Powell.

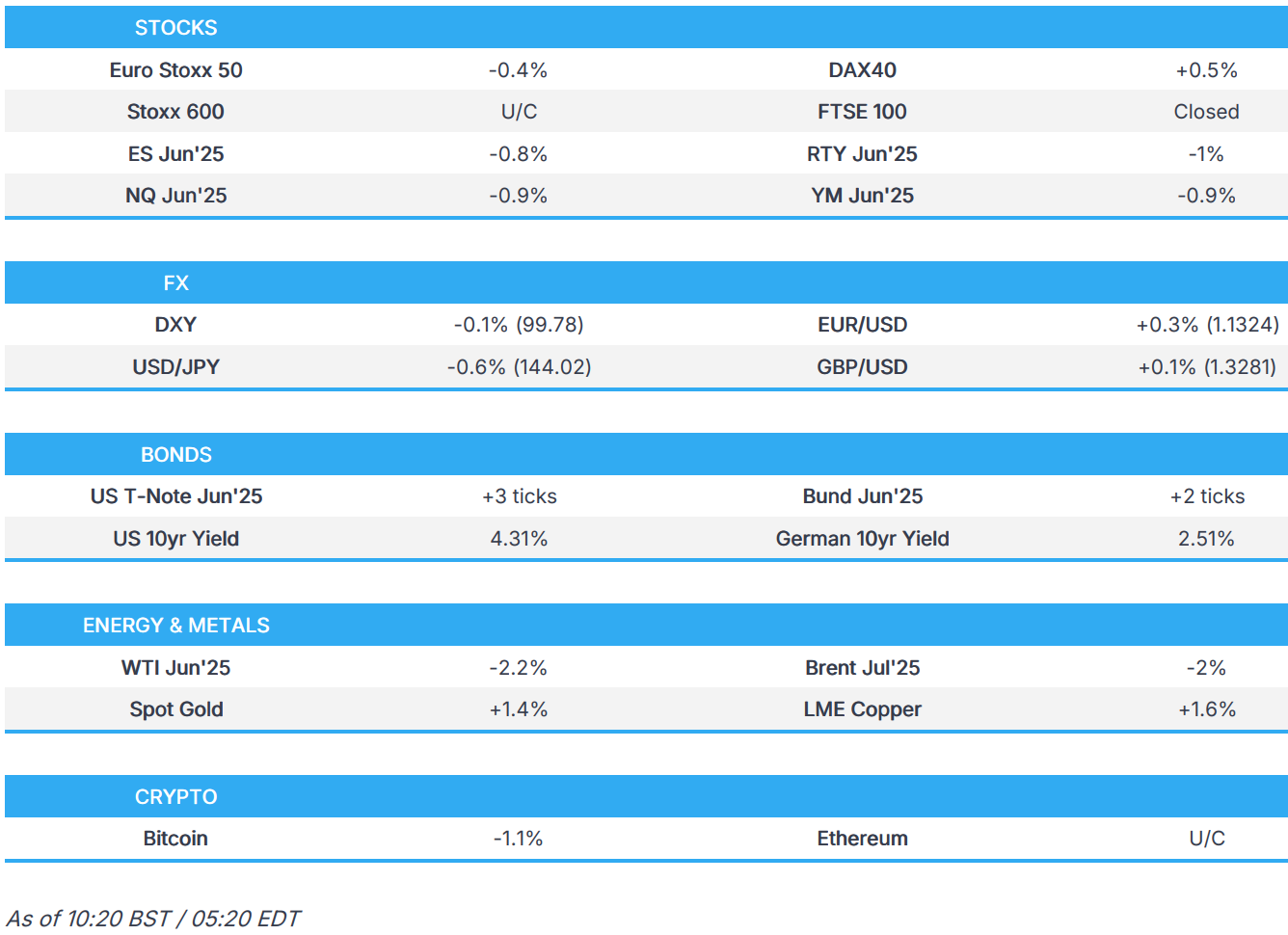

- European bourses are mixed but with price action fairly rangebound; FTSE 100 closed, with the UK on holiday; US futures entirely in the green.

- USD kicks the week off on the backfoot, EUR/USD returns to a 1.13 handle, APAC currencies in focus.

- USTs rangebound with price action subdued amidst a number of holidays.

- Crude slips on OPEC+; precious and base metals catch and hold a bid.

- OPEC+ members agreed to raise oil output by 411k bpd in June, a source report noted the group will likely approve another accelerated hike of 411k bpd for July.

- Looking ahead, US Employment Trends, ISM Services, Supply from the US, Earnings from Palantir, Him & Hers, Ford, Realty, Tyson Foods.

TARIFFS/TRADE

- US President Trump’s 25% tariffs on engines, transmissions and other key auto parts took effect on Saturday.

- US President Trump posted that he is "authorizing the Department of Commerce, and the United States Trade Representative, to immediately begin the process of instituting a 100% Tariff on any and all Movies coming into our Country that are produced in Foreign Lands".

- US President Trump answered no but stated that China and his people are talking about different things when asked if he plans to speak with Chinese President Xi this week, while he replied could well be when asked if any trade deals are coming this week. Furthermore, Trump said he wants a fair trade deal with China and they are meeting with many countries, including China, on trade deals.

- US President Trump said he is willing to lower tariffs on China at some point because the levies now are so high that the world's two largest economies have essentially stopped doing business with each other, although he also noted that he would need to keep at least some tariffs on foreign goods in place to convince businesses to move production to the US, according to Bloomberg and Axios citing an interview with NBC News.

- US President Trump’s trade adviser Navarro warned the UK against deepening trade ties with China, potentially complicating tariff talks between the UK and the US, according to Bloomberg which cited comments by Navarro to The Telegraph.

- Fox Business’s Gasparino posted on X that he is getting guidance from Wall Street sources close to the White House that a bunch of trade deal “frameworks” can be expected in the coming weeks, while they might trickle out sooner such as deals with India, South Korea or Japan and it is always possible they could be as early as this week as people have been forecasting. However, he was told that delays involved the time-consuming nature of getting various foreign sign-offs on all the details in the agreements.

- Japanese Finance Minister Kato said on Sunday that Japan has no intention of using the possibility of selling its US Treasury holdings for advantage in trade negotiations with the US, according to Nikkei.

- Chinese exporters are reportedly increasing efforts to avoid US tariffs by shipping their goods via third countries to conceal where they originated from, according to FT.

- Malaysia's PM Anwar said they will finalise negotiations to improve the free trade agreement between the ASEAN regional bloc and China in the near future, while he stated tariff talks with the US are to continue and there is a chance of reducing levies

- Mexican President Sheinbaum said she rejected an offer from US President Trump to send US troops to Mexico to help combat drug trafficking.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) opened mixed and have traded rangebound throughout the morning thus far. Note: The FTSE 100 remains shut on account of the Early May Bank Holiday.

- European sectors hold a slight positive bias, with Insurance and Healthcare leading whilst Energy is the clear laggard. Healthcare is buoyed by strength in Novo Nordisk (+2.1%) after the FDA accepted the Co’s application for oral Semaglutide 25mg, which if approved, would be the first oral GLP-1 treatment for obesity. Energy is by far the clear laggard today, given the slump in oil prices, following the recent supply hike from OPEC+.

- Shell Plc is evaluating a potential acquisition of BP – though talks are still at an early stage. Shell is reportedly waiting for further declines in stock and oil prices before deciding whether to proceed with a bid.

- US equity futures (ES -0.8%, NQ -0.9%, RTY -1%) are broadly in negative territory after a strong session on Friday; the RTY underperforms marginally vs peers.

- In terms of stock specifics, Berkshire Hathaway (-2.5%) moves lower in the pre-market after the Co. fell short on Q1 headline metrics due to California wildfires and FX-driven headwinds – pressure will also stem from Warren Buffett stepping down from his CEO position at the end of the year.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD has kicked the week off on the backfoot after last week's attempted recovery and alongside a pullback in US equity futures. The USD has been notably weaker vs. APAC currencies with particular attention on the TWD which saw its largest one-day gain vs. the USD on Friday since 1988. On the trade front, US President Trump said he is willing to lower tariffs on China at some point but answered "no" when asked if he plans to speak with Chinese President Xi this week. DXY is currently caged within Friday's 99.39-100.32 range. US ISM Services is due later.

- EUR is stronger vs. the broadly weaker USD with incremental newsflow lacking and nothing of note on the trade front after the EU made the US a EUR 50bln trade offer last week. EZ Sentix data saw an improvement to -8.1 from -19.5 with the accompanying release noting that "one month after the massive shock that rocked investors with US tariff policy and sent sentix economic data into free fall, the smoke is clearing". EUR/USD has made its way back onto a 1.13 handle with a current session peak at 1.1347.

- JPY is currently the best performer across the majors with USD/JPY briefly breaching 144 to the downside. Hopes of a trade deal with the US remain high with Fox Business’s Gasparino reporting that a "bunch" of trade deal “frameworks” can be expected in the coming weeks; Japan was mentioned in the post. Furthermore on the trade front, Japanese Finance Minister Kato said on Sunday that Japan has no intention of using the possibility of selling its US Treasury holdings for advantage in trade negotiations with the US, according to Nikkei.

- GBP mildly firmer vs. the USD after a quiet period of UK-specific newsflow last week, but with focus now firmly on the BoE on Thursday. Cable struggled to hold above the 1.33 mark and returned to a 1.32 handle with a session peak at 1.3306.

- CHF is softer vs. the EUR and the worst performer across the majors in the wake of soft Swiss inflation data which saw both M/M and Y/Y readings print at 0%; both were forecast at 0.2%. Note, the March SNB projection pencilled in a Q2 average inflation rate of 0.2% Y/Y. As such, odds of a 25bps rate cut to 0% at the June meeting have risen to 100% vs. circa 80% on Friday. Despite the magnitude of the release, EUR/CHF is currently tucked within Friday's 0.9311-83 range.

- Antipodeans are both firmer vs. the USD and near the top of the G10 leaderboard, in tandem with the gains in the Asia FX space including CNH after President Trump suggested a willingness to lower tariffs on China at some point. For AUD specifically, Australian PM Albanese’s Labor Party won an increased majority in the election on Saturday with at least 87 seats in the 150-seat parliament.

- Taiwan Central Bank says the US did not ask the TWD to appreciate; urges market commentators not to speculate on TWD issue Taiwan does not manipulate the exchange rate. Taiwan's trade surplus with the US has widened in the recent years, mainly due to an increase in US demand for Taiwan's information and comms tech, rather than exchange rate factors. Volatility of TWD vs USD has widened, as foreign fund inflows to Taiwan stocks and companies' expectations of TWD appreciating. Governor stresses that the central bank did not attend US-Taiwan tariff talks, meaning no discussion of foreign exchange rate. Taiwan Central Bank Governor says expectations of strong appreciation are big, intervened appropriately.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are trading in a very narrow 111-06 to 111-13+ band and essentially unchanged on the session. Currently entirely within Friday’s relatively expansive 111-02 to 112-01+ band. A quiet start to the week in terms of price action as Japan was away overnight and as such, there was no cash trade. Furthermore, the European session is devoid of the UK given the nation's early-May Bank Holiday. On the trade front, Trump said he is willing to lower the tariffs on China at some point as the current levels have essentially stopped trade. Elsewhere, the US announced 100% tariffs on movies produced in “foreign lands”; of note for China, the world’s second largest film maker. US ISM Services is due later.

- Bunds are also contained but in a slightly more expansive 130.69 to 131.14 band, the low just about took out last week’s 130.83 base. The low print occurred in the early European morning, as volumes picked up from very thin overnight levels as European players entered the fray. The EZ docket is light, Sentix for May came in much better than expected but still remains well into negative territory. No reaction to the data.

- French PM Bayrou reportedly wants to call a referendum to seek public support for a radical response to the budget deficit and levels of debt, wants to submit a comprehensive plan to cut the deficit, via Le Monde citing JDD. Any such referendum could only be decided upon by President Macron. Such a referendum would allow the PM to circumvent the blockage they would face in the National Assembly due to him controlling only 210/577 seats. Bayrou reaffirms that any solution "does not lie in new taxes"

- Click for a detailed summary

COMMODITIES

- Hefty losses across the crude complex following this weekend's OPEC+ confab, which saw an acceleration of production increases. To recap, OPEC+ countries with voluntary cuts agreed to raise oil output by 411k bpd in June in a virtual meeting held on Saturday. It was also reported that OPEC+ would likely approve in June another accelerated oil production hike of 411k bpd for July.

- Prices are off worse levels; WTI currently resides in a USD 55.30-57.10/bbl range while its Brent counterpart sits in a USD 58.50-60.24/bbl parameter.

- Precious metals trade in the green at the time of writing despite a relatively stable dollar, but amid ongoing uncertainty surrounding tariffs and geopolitics, coupled with recent losses in the complex as spot gold pulled back from record highs set on 22nd April. Spot gold resides in a current USD 3,237.79-2,374.71/oz range.

- Copper futures edge higher with the upside capped amid the holiday closures including its largest buyer, China. Sentiment this morning is mixed across the regions as participants await further macro newsflow. 3M LME copper resides in a USD 9,241.95-9,460.65/t range at the time of writing.

- OPEC+ countries with voluntary cuts agreed to raise oil output by 411k bpd in June in a virtual meeting held on Saturday. It was also reported that OPEC+ will likely approve in June another accelerated oil production hike of 411k bpd for July and could unwind voluntary cuts of 2.2mln bpd through October 2025 if compliance with quotas doesn’t improve as Saudi Arabia looks to punish some members for exceeding quotas, according to sources cited by Reuters. Furthermore, it was also reported that eight OPEC+ countries are to meet next on June 1st.

- UAE’s ADNOC set June Murban crude OSP at USD 67.73/bbl.

- UBS expects further seasonal increases in global oil demand in the next few months, given US driving season and increasing Middle-East temperatures. Sees Brent at USD 68/bbl in the coming months.

- EU plans to propose banning Russian gas imports by the end of 2027, according to Bloomberg.

- Russian Oil product exports from Black Sea Port of Tuapse planned at 0.81mln tons in May (prev. scheduled 0.864mln tons in April), via Reuters citing sources.

- Goldman Sachs does not expect silver to catch up with the gold rally amid higher central bank gold demand which has structurally lifted the gold-silver price ratio If recession occurs, GS estimates that acceleration in ETF inflows would lift gold price to USD 3,880 by year-end. With Chinese solar production now slowing amid oversupply, high recession risk, central bank gold buying remaining strong in 2025, GS expects gold to continue "outglittering" silver. "We reiterate our structural bullish gold view with a base case of USD 3,700/toz by year-end and of USD 4,000 by mid-2026."

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Sentix Index (May) -8.1 vs. Exp. -12.5 (Prev. -19.5)

- Swiss CPI YY (Apr) 0.0% vs. Exp. 0.2% (Prev. 0.3%); MM 0.0% vs. Exp. 0.2% (Prev. 0.0%)

- Turkish CPI MM (Apr) 3.0% vs. Exp. 3.1% (Prev. 2.46%)

NOTABLE EUROPEAN HEADLINES

- EU is reportedly eyeing closer ties to the trans-Pacific CPTPP bloc to defend the rules-based global system, according to FT.

- French PM Bayrou reportedly wants to call a referendum to seek public support for a radical response to the budget deficit and levels of debt, wants to submit a comprehensive plan to cut the deficit, via Le Monde citing JDD Any such referendum could only be decided upon by President Macron. Such a referendum would allow the PM to circumvent the blockage they would face in the National Assembly due to him controlling only 210/577 seats. Bayrou reaffirms that any solution "does not lie in new taxes"

NOTABLE US HEADLINES

- US President Trump said he is not worried about a US recession and that anything can happen, but he thinks they are going to have the greatest economy in history. Trump reiterated that the Fed should lower interest and said he won’t remove Fed Chair Powell. He also said he doesn’t know if people in the US deserve due legal process which is guaranteed by the constitution as he criticized the judiciary for opposing his plans to deport undocumented immigrants, according to an interview with NBC News.

- US President Trump administration officials are exploring ways of challenging the tax-exempt status of non-profits, according to WSJ.

- Apple (AAPL) plans an iPhone release schedule shake-up and new styles, according to The Information.

- Warren Buffet is to step down as CEO of Berkshire Hathaway (BRK/A) by year-end with Greg Abel to succeed Buffet as CEO later this year.

GEOPOLITICS

MIDDLE-EAST

- A missile fired by Yemen’s Houthis hit the grounds of Israel’s Ben Gurion Airport after interception failed, while six were reportedly injured, but none seriously, according to The Times of Israel. It was separately reported that Yemen’s Houthis said they are working on imposing a comprehensive air blockade on Israel by targeting its airports.

- Israeli PM Netanyahu said Israel will respond to Houthis and their 'Iranian terror masters' at a time and place of its choosing, while it was also reported that Israel’s army chief issued an order for reservists to expand operations in Gaza.

- Israel is readying a "massive response" to Houthis and Iran after the airport missile attack, according to the Washington Examiner.

- Iran’s Defence Minister warned they will respond with force if Iran is attacked and said if a war is initiated by the US or Israel, Iran will target their interests, bases and forces wherever they may be and whenever deemed necessary, according to state TV.

- Israel's cabinet unanimously approved the expansion of the army's operation in the Gaza Strip.

- Israel called on Qatar to stop playing both sides with its double talk and decide if it is on the side of civilisation or if it is on the side of Hamas, according to the Israeli PM’s office.

- Israeli PM Netanyahu "made it clear that the [new] plan differs from its predecessors in that [Israel is] moving from the method of raids to occupying the territories and remaining in them," according to a statement by the PM office.

- "Iran denies aiding Yemen's Houthis, after missile strike on Israeli airport", according to AFP.

- Israel's scaled up offensive within Gaza could go as far as the seizing of the entire enclave, via Reuters citing an Israeli official.

- Iranian Foreign Ministry says "We await Oman's point of view as the sponsor of dialogue on the resumption of talks with Washington and we are ready for that", via Al Jazeera.

RUSSIA-UKRAINE

- Ukraine launched drone attacks targeting Moscow, according to the mayor of Moscow. It was also reported that the Russian aviation watchdog closed one of Moscow's key airports after reports of a drone attack targeting the Russian capital.

- US President Trump said they had some very good discussions about Russia and Ukraine over the weekend.

- Russian President Putin said they have enough strength and the means to bring the conflict with Ukraine to a logical conclusion, while he said there has been no need to use nuclear weapons in the conflict and hopes there never will be.

- Russia’s Kremlin said President Putin’s offer to Ukraine of a 3-day ceasefire to coincide with World War Two commemorations was a test to assess Kyiv’s readiness for peace and Ukraine’s refusal to agree shows ‘neo-Nazism’ lies at the foundation of the Ukrainian government.

- Russian senior security official Medvedev said US President Trump’s claim that the US did more than any other country to win World War Two is pretentious nonsense, according to TASS.

- Chinese President Xi will conduct a state visit to Russia and attend a war victory celebration on May 7th-10th, while Chinese President Xi and Russian President Putin are to discuss the development of a comprehensive strategic partnership.

OTHER

- US Army Pacific Commander General Clark said the region is more dangerous now due to China’s aggressive behaviour and that China’s rehearsals of a Taiwan blockade ‘leave you speechless’.

CRYPTO

- Bitcoin is a little lower and sits just shy of USD 95k; Ethereum is essentially flat and holds around USD 1.8k.

APAC TRADE

- APAC stocks were ultimately mixed in holiday-thinned trade with most major markets in the region shut including in Japan, South Korea, China and Hong Kong, while tariff concerns lingered after 25% tariffs on auto parts took effect on Saturday and President Trump announced a 100% tariff for foreign films but had also noted a willingness to lower tariffs on China at some point because the levies now are so high that the world's two largest economies have essentially stopped doing business with each other.

- ASX 200 was led lower by weakness in the energy sector following a decline in oil prices due to the OPEC+ decision for another accelerated oil output increase, and with the top-weighted financial sector also hit post-Westpac's earnings, while the landslide victory by Australian PM Albanese's Labor party had little impact.

- TAIEX retreated with Taiwan-listed US Treasury ETFs heavily pressured amid headwinds from the recent surge in the local currency.

NOTABLE ASIA-PAC HEADLINES

- Australian PM Albanese’s Labor Party won an increased majority in the election on Saturday with at least 87 seats in the 150-seat parliament, while the opposition Liberal-National Coalition leader Dutton lost his seat which he had held for 24 years.

- Singapore’s ruling PAP won in 29 out of 32 constituencies contested in the election on Saturday and was confirmed the winner of 87 of 97 House seats.

- US President Trump said he would extend the TikTok deadline if there is still no deal.

- Foxconn (2317 TT) April revenues 25.54% Y/Y (prev. 23.4% Y/Y); on current visibility, operational outlook for Q2 anticipates Q/Q and Y/Y growth Impact of evolving global political and economic conditions will need continued close monitoring. The cloud and networking products segment is expected to maintain its growth momentum in Q2. The current period is traditionally an off-season, and primary product lines are entering a product transition period.

- PBoC Governor Pan has called on Asian nations to work against US tariffs, says global economic uncertainties are rising.