US Market Open: Sentiment hit after HKMA says it is diversifying into non-US assets, Bunds volatile on Merz

06 May 2025, 11:04 by Newsquawk Desk

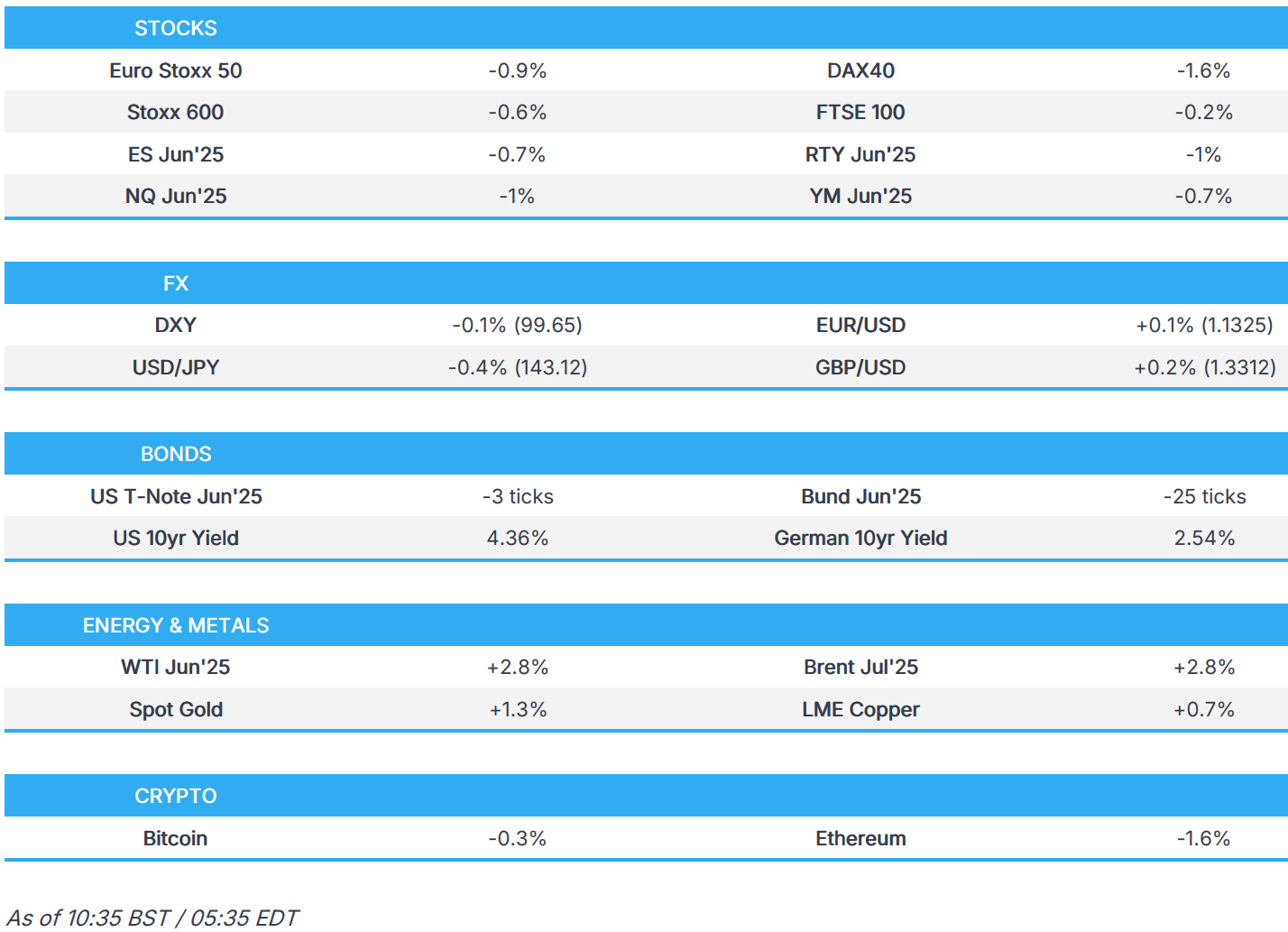

- Sentiment in the equities complex hit after HKMA said it has been lowering its duration in US treasury holdings; the exchange fund has been diversifying into non-US assets; ES -0.7%, NQ -1%.

- Germany's CDU leader Merz fails to be elected as Chancellor, a decision which has sparked pressure in European bourses leading to underperformance in the DAX 40.

- USD on the backfoot, JPY leads the majors, EUR upside stalled in reaction to Merz updates.

- Bunds boosted on Merz, though the move has since pared, Gilts underperform.

- Crude and gold remain firm amid escalating geopolitics.

- Looking ahead, US International Trade, Canadian Exports/Imports, NZ HLFS Unemployment Rate, EIA STEO, Comments from BoE's Breeden, Supply from the US. Earnings from AMD, Supermicro, Rivian, Tempus AI, Celsius, Datadog, Constellation Energy, UniCredit, Intesa Sanpaolo & Ferrari.

TARIFFS/TRADE

- EU Trade Commissioner Sefcovic says another EUR 170bln of US exports may be impacted by tariffs; EU-US tariff situation is not acceptable.

- US President Trump said he will announce pharmaceutical tariffs over the next two weeks, while he signed an order to reduce regulatory barriers to domestic pharmaceutical manufacturing and will have an announcement next week related to the cost of medicines.

- US Commerce Secretary Lutnick said the first trade deal has got to be with a top 10 economy, while he commented the USMCA pact is okay for now and responded it is really complex when asked if a deal with Canada is possible, according to a Fox Business interview.

- US Agricultural Secretary Rollins is to visit Japan, India and Vietnam and will discuss tariffs during Asia tour.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.6%) opened mostly firmer/flat and traded tentatively on either side of the unchanged mark. Thereafter, the risk tone soon slipped after the HKMA said it says has been lowering its duration in US treasury holdings and as Germany's Merz failed to secure enough votes to become Chancellor; DAX 40 -1.8%.

- The HKMA update sparked some modest pressure in US equity futures (ES -0.9%, NQ -1%); ahead of a handful of earnings and meetings between the US and Canadian Presidents.

- As for sectors, its a mixed picture in Europe. Food Beverage & Tobacco takes the top spot, joined closely by Utilities. To the downside, Basic Resources sits right at the foot of the pile – losses largely driven by Anglo American after Peabody said it may terminate its deal for its coal mine assets.

- For the Pharma industry; US President Trump said he will announce pharmaceutical tariffs over the next two weeks, while he signed an order to reduce regulatory barriers to domestic pharmaceutical manufacturing and will have an announcement next week related to the cost of medicines.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- After an attempted recovery last week, the USD has continued to ebb lower after DXY failed to sustain a move above the 100 mark, despite a solid showing for US ISM services. HKMA said it has been lowering its duration in US treasury holdings and has been diversifying into non-US assets. DXY is currently towards the lower end of Monday's 99.46-100.05 range.

- EUR is firmer vs. the broadly weaker USD as Eurozone-specific newsflow remains on the light side. ECB-dove Stournaras noted he does not see inflation if the EU tariff reaction is selective and it seems the ECB will continue with rate cuts. EUR/USD has gained a firmer footing on a 1.13 handle but is yet to approach Monday's high at 1.1364 with some of the upward momentum for the currency stalled in recent trade after Germany's CDU leader Merz fell short of a majority needed to become Chancellor in the first round of voting in parliament.

- USD/JPY traded indecisively overnight and failed to sustain a brief return to the 144.00 level with price action largely driven by the dollar amid the continued absence of Japanese participants. In European trade, downside was seen for the pair as global equity futures ebbed lower. USD/JPY has delved as low as 142.91 with the next target coming via the 1st May low at 142.88.

- GBP is mildly firmer vs. the USD as UK participants return to market. UK newsflow remains light with markets looking ahead to Thursday's BoE policy announcement. Cable has ventured as high as 1.3333 but is yet to test yesterday's 1.3336 peak.

- Diverging fortunes for the antipodeans with AUD towards the bottom-end of the G10 leaderboard. Overnight trade saw a larger-than-expected contraction in Australian building approvals and a disappointing Chinese services PMI. However, the cause for underperformance vs. NZD is otherwise unclear.

- PBoC set USD/CNY mid-point at 7.2008 vs exp. 7.2518 (Prev. 7.2014).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are holding around the unchanged mark in a 110-27+ to 111-03 band. Came under modest pressure overnight on the return of China and generally supportive tone, despite weak Chinese PMI; though, once again, Japan was on holiday and as such conditions were thinner than normal with no cash trade. Into the European morning, USTs began to pick up alongside fixed income generally amidst commentary from the HKMA that they are diversifying into non-US assets. The update had more of an impact on US equity futures and the DXY than it did on Treasuries. Ahead, supply is the main scheduled event stateside in the form of a 10yr tap. Follows Monday’s 3yr sale which was much better than the prior.

- Bunds were initially under pressure in-fitting with the bias from USTs overnight. Thereafter, the benchmark began to lift off lows and was largely unaffected by modest upward revisions to Final PMIs for April. More recently, Bunds jumped by almost 30 ticks to breach the 131.00 mark as Germany's CDU/CSU leader Merz fell just six votes short of a Bundestag majority in the vote to appoint him as Chancellor. Upside in Bunds comes as Merz not securing a majority presents risks to his Chancellorship, the CDU/CSU-SPD coalition and possibly the implementation of recent fiscal reform. The upside has now almost entirely been pared, from 131.08 to current 130.88, potentially as traders await clarity on the timing of the next vote; as it stands, it looks unlikely to occur today, but could be as soon as Wednesday.

- Gilts are the clear underperformer in catch-up play from Monday’s UK Bank Holiday. Gapped lower by 29 ticks at 92.88, the session high, before slipping to a 92.32 base in short order. Currently holding just off that low but in close proximity to it. PMIs for April were subject to modest upward revisions, but in-fitting with EGBs spurred no real reaction in the benchmark.

- Germany sells EUR 3.48bln vs exp. EUR 4.5bln 2.40% 2030 Bobl: b/c 1.2x (prev. 1.40x), average yield 2.07% (prev. 2.06%) & retention 22.67% (prev. 21.1%).

- Click for a detailed summary

COMMODITIES

- Firm gains across the crude complex, with prices rebounding from the earlier OPEC-induced downside, with most of Asia also returning to the market from the long weekend. The upside could be at least partially attributed to the geopolitical developments yesterday, in which Israel expanded its Gaza operation and suggested that it plans to occupy the territory, marking a major escalation from its initial plans of destroying Hamas and its capabilities. WTI resides in a USD 57.03-58.52/bbl range while Brent sits in a USD 60.18-61.64/bbl parameter.

- Precious metals are higher across the board amid a softer Dollar, the return of APAC players, ongoing tariff woes, and escalating geopolitics. Spot gold has almost reversed the losses seen during the final week of April with the yellow metal current in a USD 3,322.75-3,387.02/oz parameter as it eyes USD 3,400/oz to the upside.

- The base metals complex ekes mild gains with the aid of a softer Dollar and alongside the return of some demand as most APAC markets returned from their long weekend. 3M LME copper has waned off best levels but resides around the middle of a USD 9,366.50-9,487.53/t intraday band.

- European Commission is to make a legal proposal to ban Russian gas and LNG imports by end-2027 and ban new Russian gas deals and existing spot contracts by end-2025; plans will be announced on Tuesday, legal proposals due in June, via an EU official.

- EU Commission will present a legal proposal in June to ban all imports under Russian gas deals and existing spot contracts by end-2025, via Reuters citing a Commission document In June, will present trade measures aimed at making imports of Russian enriched Uranium economically less viable.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HCOB Composite Final PMI (Apr) 50.4 vs. Exp. 50.1 (Prev. 50.1); HCOB Services Final PMI (Apr) 50.1 vs. Exp. 49.7 (Prev. 49.7)

- French HCOB Services PMI (Apr) 47.3 vs. Exp. 46.8 (Prev. 46.8); HCOB Composite PMI (Apr) 47.8 vs. Exp. 47.3 (Prev. 47.3)

- Italian HCOB Services PMI (Apr) 52.9 vs. Exp. 51.5 (Prev. 52); HCOB Composite PMI (Apr) 52.1 (Prev. 50.5)

- German HCOB Composite Final PMI (Apr) 50.1 vs. Exp. 49.7 (Prev. 49.7); HCOB Services PMI (Apr) 49 vs. Exp. 48.8 (Prev. 48.8)

- UK S&P Global Service PMI (Apr) 49 vs. Exp. 48.9 (Prev. 48.9); S&P Global PMI: Composite Output (Apr) 48.5 vs. Exp. 48.2 (Prev. 48.2)

- Swiss Unemployment Rate Adj. (Apr) 2.8% vs. Exp. 2.8% (Prev. 2.8%)

NOTABLE EUROPEAN HEADLINES

- Germany's CDU leader Merz falls short of a majority needed to become Chancellor in first round of voting in parliament; secured 310 Bundestag votes, 316/630 required. On the second round of voting for German Chancellor Merz, Handelsblatt citing sources reports "The second round of voting could be postponed until Friday because the approval of the AfD is necessary for an immediate ballot". There will not be a second vote on Merz becoming German Chancellor today, via Handelsblatt citing numerous reports and the CDU Secretary General.

- EU is set to make it easier for UK professionals to work in the bloc, according to FT.

- SNB Chairman Schlegel says is committed to its price stability mandate; biggest challenge at present is uncertainty. Ready to intervene in the FX market as necessary. Swiss inflation is expected to come down. Not ruled out negative rates. Nobody likes negative rates but if have to, are prepared to do it again.

NOTABLE US HEADLINES

- HKMA says has been lowering its duration in US treasury holdings; exchange fund has been diversifying into non-US assets Has been diversifying currency exposure in its investment portfolio to manage risks.

- US House Speaker Johnson said House Republicans remained on pace to pass the Trump agenda by Memorial Day or shortly thereafter and stated the Trump agenda is not facing a setback in the US House.

- US Defense Secretary Hegseth ordered a reduction in 4-star positions in the military, according to a US official.

- Taiwanese central bank says 80% of FX reserves are US bonds. Taiwan Central Bank FX official says they feel the market has returned to a more stable situation today.

GEOPOLITICS

MIDDLE EAST

- Palestinian media reported that the Israeli army blew up residential buildings east of Gaza City.

- "Israeli army: Our forces are deployed in southern Syria and are in a state of readiness to prevent the entry of any hostile forces into the area or to Druze villages", according to Sky News Arabia.

- "Hamas: The Israeli occupation's approval of plans to expand its operation in the Gaza Strip is an explicit decision to sacrifice Israeli prisoners", according to Al Jazeera.

- Israeli National Unity chairman Benny Gantz says "We must be ready and have the ability to attack Iran's nuclear facilities", via Sky News Arabia

RUSSIA-UKRAINE

- Ukraine attack damaged a power substation in Russia's Kursk region, according to the regional governor.

- Russian defence units destroyed five Ukrainian drones flying towards Moscow and Russia's aviation watchdog announced flights were halted at Moscow's major airports following reports of drones, but later announced that airports reopened.

CRYPTO

- Bitcoin is a little lower and trades just above USD 94k.

- SNB's Chairman Schlegel says cryptocurrencies have too high price volatility to preserve value as an FX reserve.

APAC TRADE

- APAC stocks were mostly higher as Chinese participants returned from the Labor Day holiday but with the gains capped following disappointing Chinese Caixin Services PMI data and as markets in Japan and South Korea remained closed.

- ASX 200 traded little changed as strength in the commodity-related sectors were predominantly offset by underperformance in financials and defensives, while the larger-than-expected contraction in building approvals clouded over risk appetite.

- Hang Seng and Shanghai Comp gained on return from the extended weekend and took their opportunity to react to the recent China tariff rhetoric from US President Trump who said that he is willing to lower tariffs on China at some point, while the miss on Caixin Services PMI data did little to derail the positive sentiment in China.

NOTABLE ASIA-PAC HEADLINES

-

Chinese President Xi is prepared to work with EU leaders to expand mutual openness and properly handle frictions and differences, according to Xinhua Calls on the EU and China to safeguard fairness and justice.

- China said 314mln domestic trips were made during the May holiday which was up 6.4% Y/Y and travel expenditure of domestic tourists rose 8% Y/Y to 180.3bln, according to CCTV.

- US House intensified its legislative push against Beijing on Monday in which it advanced a slate of China-related bills targeting industrial espionage, export controls, national security threats and alleged human rights abuses.

- Fast fashion platforms Shein and Temu boosted digital advertising in Europe with the most growth seen in France and the UK, while they see increased app downloads in France and the UK as US tariffs hit and Shein also boosted advertising in Brazil where it manufactures goods for Latin America.

- HKMA intervened in which it bought USD 7.8bln against the HKD at 7.7500 after the HKD hit the strong end of the trading range.

DATA RECAP

- Chinese Caixin Services PMI (Apr) 50.7 vs. Exp. 51.7 (Prev. 51.9); Composite PMI (Apr) 51.1 (Prev. 51.8)

- Australian Building Approvals (Mar) -8.8% vs. Exp. -0.6% (Prev. -0.3%, Rev. -0.2%)