US Market Open: US-China to start trade talks this week & PBoC announced rate cuts; FOMC due

07 May 2025, 10:52 by Newsquawk Desk

- China's Ministry of Commerce confirmed US-China trade talks with Vice Premier He Lifeng to visit Switzerland from May 9th-12th and will visit France from May 12th-16th for economic and financial dialogue.

- PBoC Governor Pan announced to cut RRR by 50bps effective May 15th and to cut the policy interest rate by 10bps effective on May 8th with the 7-day reverse repo rate lowered to 1.40% and interest rates on Standing Lending Facility across all tenors lowered by 10bps. Pan stated that the policy rate cut will lead to a Loan Prime Rate cut of 10bps and the RRR cut will release about CNY 1tln in liquidity.

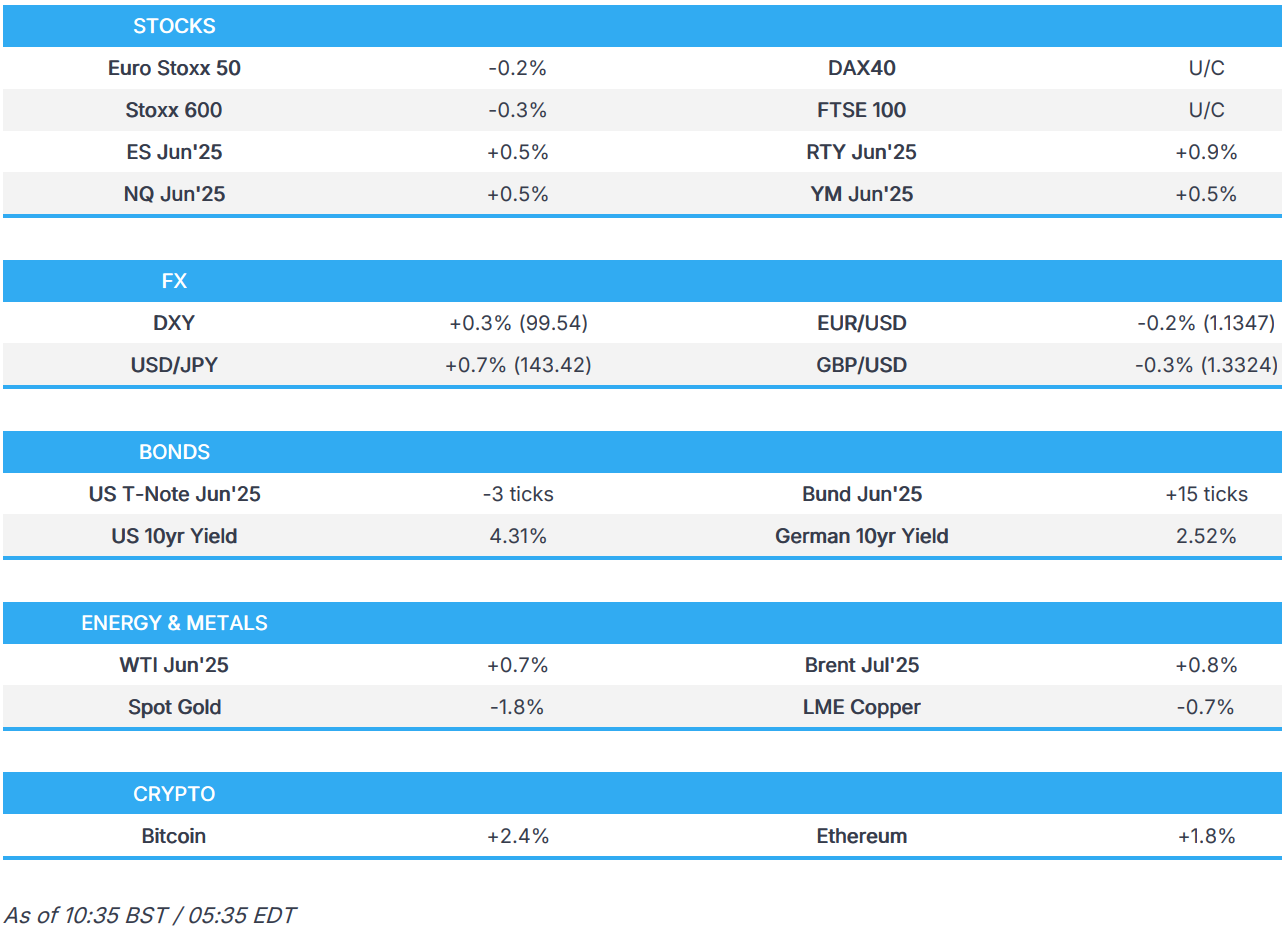

- European stocks mixed whilst US-Sino trade talks have been confirmed and as traders await the FOMC.

- USD stronger vs. peers as US-China meeting spurs trade hopes, JPY underperforms.

- Two way action for EGBs & Gilts but benchmarks ultimately firmer, aided by auctions. USTs more contained pre-FOMC.

- Crude firmer on China's monetary policy easing, US-China trade talks, and rising tensions between India and Pakistan.

- Looking ahead, Fed, NBP, CNB & BCB Policy Announcements, US Treasury Secretary Bessent, Fed Chair Powell's Presser, Supply from the US, Earnings from AppLovin, Carvana, Arm, DoorDash, AMC, Uber, Disney, Barrick Gold.

TARIFFS/TRADE

- China's Ministry of Commerce confirmed US-China trade talks with Vice Premier He Lifeng to visit Switzerland from May 9th-12th and will visit France from May 12th-16th for economic and financial dialogue.

- Chinese Foreign Ministry (on Geneva talks) says meeting was requested by the US; US should stop threatening if it wants a deal. holding tariff talks with the US before curb's removal, says, China's position has not changed.

- US Treasury Secretary Bessent and Trade Representative Greer are to meet with China's lead representatives on economic matters later this week in Switzerland, while Bessent confirmed he is meeting the Chinese team on Saturday in Switzerland and said they agreed to talk on Saturday and will agree on Sunday what they are going to talk about. Bessent said his sense is this will be about de-escalation and said they have got to de-escalate before they can move forward, as well as noted that the US doesn’t want to decouple from China over textiles and similar goods but does want to decouple over strategic industries. Furthermore, he said trade frictions can go down, Americans can get fairer deals, and everything is on the table.

- Mexico's agricultural minister said he met with US counterpart Rollins and reached agreements that will be beneficial to both countries.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.3%) opened mostly lower and has traded sideways throughout the morning thus far.

- There have been a few updates to keep traders busy; 1) US and China are set to hold talks in Switzerland over trade, 2) China announced new easing measures amid global economic uncertainty; the PBoC is to cut its RRR by 50bps and reduce its 7-day reverse repo by 10bps (other measures were also announced), 3) India launched air strikes on Pakistan.

- European sectors are mixed and with the breadth of the market fairly narrow aside from the top/bottom performers. Autos takes the top spot, lifted by post-earning strength in BMW (+3.5%). Healthcare is pressured as traders react to the FDA appointing Vinay Prasad as its new vaccine chief. Elsewhere, Novo Nordisk (+5%) gains despite reporting a mixed set of Q1 results, cutting guidance and said it would not be conducting a buyback programme in 2025.

- US equity futures are broadly in the green (ES & NQ +0.5%, RTY +0.9%), with sentiment lifted as the region reacts to the latest US-China trade updates and after China’s latest monetary policy package. Focus for the day will ultimately be on the FOMC.

- China's CPCA says Tesla (TSLA) sold 58,459 vehicles in April (March 78,828).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is attempting to claw back some of Tuesday's losses that were seen alongside a pullback in US yields. Recent optimism has been spurred by news that US and China trade talks are to take place in Switzerland from May 9th-12th. For today's US agenda, US Treasury Secretary Bessent is due to testify before the House. Thereafter, all eyes will be on the FOMC whereby expectations are for the Bank to stand pat on rates with Fed Chair Powell continuing to note that the Fed is well-positioned to wait for greater clarity before considering altering its policy stance. DXY is currently tucked within yesterday's 99.17-100.09 range.

- EUR is flat vs. the USD after a session of gains on Tuesday which saw the pair advance from an opening level of 1.1314 to a peak at 1.1381 alongside a softening in US yields. From a domestic perspective, CDU Leader Merz was elected Chancellor in the second-round parliamentary vote.

- JPY the laggard across the majors with USD/JPY back above the 143 mark. The domestic story for Japan is a quiet one as market participants returned from the four-day weekend. USD/JPY has ventured as high as 143.35 but is still some way off Tuesday's best at 144.27.

- GBP is a touch softer vs. the USD and EUR, giving back some of yesterday's gains which were triggered by a Reuters report that the EU and UK have agreed to hold annual summits to discuss their relationship. Shortly after, the UK reached a free trade agreement with India, with India set to cut tariffs on 90% of UK imports. Thereafter, reports suggested that the UK is closing in on US trade pact with lower tariff quotas for cars and steel. The totality of the potential deals underpinned Cable sending the pair to a 1.3402 peak before returning to a 1.33 handle; currently oscillating around the 1.3350 mark.

- Antipodeans are both softer vs. the USD and unable to benefit from the PBoC's decision to cut the RRR by 50bps, the 7-day reverse repo rate by 10bps and other easing measures. From a domestic perspective, NZ published mixed Employment data and a softer-than-expected Labour Cost Index but had little follow-through into NZD.

- PBoC set USD/CNY mid-point at 7.2005 vs exp. 7.2114 (Prev. 7.2008).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs traded without direction overnight but as traders digest the latest US-China trade talk updates and China's latest monetary policy package, US paper has been coming under some modest pressure. USTs are at the bottom end of a relatively narrow 111-04 to 111-11+ band. Focus for today will be on the FOMC (expected to keep rates steady).

- Bunds were initially firmer, but only modestly so and unable to make a foothold above the 131.00 handle. As such, Bunds are shy of Tuesday’s 131.08 best when Merz failed to become Chancellor in the first vote - but secured the role in a second vote. Similar to USTs, Bunds were pressured in the European morning and found themselves back towards their 130.79 base. Thereafter a strong outing from France saw Bunds bounce back towards a session high of 131.09.

- Gilts opened higher by a handful of ticks given the read across from peers at the time. However, the benchmark then waned in-line with peers but with magnitudes slightly less pronounced; nonetheless, Gilts briefly took out Tuesday’s 92.82 base to a 92.79 low. Before making its way back above 93.00 on a strong auction.

- France sells EUR 12bln vs. exp. EUR 10-12bln 3.20% 2035, 1.25% 2038, 4.50% 2041 OATs.

- UK sells GBP 4.5bln 4.375% 2030 Gilts: b/c 3.23x (prev. 2.95x), average yield 3.977% (prev. 4.142%) & tail 0.4bps (prev. 1.0bps).

- Click for a detailed summary

COMMODITIES

- Firm trade across the crude complex (albeit with futures recently waning off highs) despite a relatively quiet market, softer Dollar pre-FOMC, and amid modest gains across most equity bourses, with the gains largely facilitated by developments overnight in trade, geopolitics, and with China loosening its monetary policy. WTI resides in a USD 58.94-60.26/bbl range while Brent sits in a USD 62.41-63.25/bbl parameter.

- Spot gold reverted to beneath the USD 3,400/oz level with pressure seen shortly after futures trading resumed as markets were jolted by reports that US and Chinese officials are to conduct talks later this week in Switzerland. Spot gold trades in a USD 3,360.20-3,422.14/oz range at the time of writing vs Tuesday's USD 3,322.76-3,4335.06/oz parameter.

- Copper futures swung between gains and losses overnight and ultimately declined and remained subdued heading into European hours despite the PBoC's RRR and policy rate cut announcements, albeit following a short rally since the end of April. 3M LME currently resides in a USD 9,446.95-9,584.08/t range awaiting the FOMC in the absence of macro impulses.

- US Private inventory data (bbls): Crude -4.5mln (exp. -2.5mln), Distillate +2.2mln (exp. -2.7mln), Gasoline -2.0mln (exp. -1.5mln), Cushing -0.9mln.

- Venezuela restarted a key gasoline production unit at its second-largest refinery after being shut down for a year.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Retail Sales YY (Mar) 1.5% vs. Exp. 1.6% (Prev. 2.3%, Rev. 1.9%); Retail Sales MM (Mar) -0.1% vs Exp. 0.0% (Prev. 0.3%, Rev. 0.2%)

- EU HCOB Construction PMI (Apr) 46.0 (Prev. 44.8); German HCOB Construction PMI (Apr) 45.1 (Prev. 40.3); Italian HCOB Construction PMI (Apr) 50.1 (Prev. 52.4); French HCOB Construction PMI (Apr) 43.6 (Prev. 43.8)

- Swedish CPIF Ex Energy Flash YY (Apr) 3.1% vs. Exp. 3.3% (Prev. 3.0%); CPI YY Flash (Apr) 0.3% vs. Exp. 0.5% (Prev. 0.5%); CPI MM Flash (Apr) 0.1% vs. Exp. 0.3% (Prev. -0.7%); CPIF Flash YY (Apr) 2.3% vs. Exp. 2.5% (Prev. 2.3%); CPIF Ex Energy Flash MM (Apr) 0.5% vs. Exp. 0.7% (Prev. 0.0%); CPIF Flash MM (Apr) 0.2% vs. Exp. 0.4% (Prev. -0.5%)

- French Trade Balance, EUR, SA (Mar) -6.248B (Prev. -7.87B, Rev. -7.700B); Exports, EUR (Mar) 52.551B (Prev. 49.67B, Rev. 49.785B); Imports, EUR (Mar) 58.799B (Prev. 57.544B, Rev. 57.485B)

- Italian Retail Sales NSA YY (Mar) -2.8% (Prev. -1.5%); Retail Sales SA MM (Mar) -0.5% (Prev. 0.1%)

- UK S&P Global PMI Composite - Output (Apr) 48.4 (Prev. 51.0); S&P Global Construction PMI (Apr) 46.6 vs. Exp. 45.8 (Prev. 46.4)

NOTABLE EUROPEAN HEADLINES

- German Defence Minister Pistorius is reportedly seeking a drastic increase in German annual defence budget; aims for over EUR 60bln/year in defence spending from 2025, according to Reuters sources.

- Germany's BaFin says financial institutions are generally currently in a strong position; uncertainty is extremely high and will remain so; possibility that problems in the non-banking sector have an impact on banks cannot be ruled out.

- Germany's VDMA says March orders +4% Y/Y (domestic -3%, foreign +6%).

GEOPOLITICS

MIDDLE EAST

- US President Trump said Houthis decided that they don't want to do this anymore and that he told the military to stop attacks against Houthis, while he added that he is not planning to stop in Israel during his Middle East trip and they are talking to Israeli PM Netanyahu about a lot of things right now. Trump said it is crunch time for Iran and he hopes Iran does what is right, as well as stated that Iran will not have nuclear weapons.

RUSSIA-UKRAINE

- Explosions were heard in Kyiv after Ukraine's air force warned of a missile attack, while Ukraine's military reported apartments are on fire after a Russian drone attack.

INDIA-PAKISTAN

- An Indian missile attack on Pakistani-controlled territory has killed at least 26 civilians and left 46 injured, Pakistan officials have said, via Sky News.

- India launched 'Operation Sindoor' in which it hit terrorist infrastructure in Pakistan and Pakistan-occupied Jammu and Kashmir, while the Indian army announced that Pakistan violated the ceasefire agreement again in the Poonch-Rajouri area and it was responding appropriately in a calibrated manner. Furthermore, a Pakistan military spokesman noted there were exchanges of fire with Indian troops at multiple places along the ceasefire line in Kashmir and announced that five Indian aircraft were shot down.

- Pakistan's Army Chief said they will respond to India at the time, place and in a way of Pakistan's choice, via Sky News Arabia.

- Pakistan Government Security Committee says India has "ignited an inferno in the region", the responsibility for ensuing consequences shall lie squarely with India. Authorised the military to undertake corresponding action.

OTHER

- US ordered its intelligence agencies to step up spying on Greenland, according to WSJ.

CRYPTO

- Bitcoin is on a stronger footing and sits just of the USD 97k mark; Ethereum also firmer.

APAC TRADE

- APAC stocks traded mostly higher as participants digested the PBoC's announcement to loosen monetary policy and reports of upcoming US-China talks this week but with the gains capped amid geopolitical escalation between India and Pakistan.

- ASX 200 eked mild gains as outperformance in the commodity-related sectors was partially offset by losses in healthcare and tech, while the top-weighted financials industry was kept afloat post-NAB earnings.

- Nikkei 225 was underpinned at the open as Japanese markets reopened from the four-day weekend although momentum waned shortly after in the absence of any major pertinent catalysts for Japan.

- Hang Seng and Shanghai Comp were underpinned following reports that the US and China will meet for talks on Saturday involving US Treasury Secretary Bessent, USTR Greer and Chinese Vice Premier He Lifeng, while there was also encouragement from the briefing by Chinese officials where PBoC Governor Pan announced to cut RRR by 50bps and the policy interest rate by 10bps.

NOTABLE ASIA-PAC HEADLINES

- PBoC Governor Pan announced to cut RRR by 50bps effective May 15th and to cut the policy interest rate by 10bps effective on May 8th with the 7-day reverse repo rate lowered to 1.40% (from 1.50%) and interest rates on Standing Lending Facility across all tenors lowered by 10bps. Pan stated that the policy rate cut will lead to a Loan Prime Rate cut of 10bps and the RRR cut will release about CNY 1tln in liquidity. Pan also noted that they will cut the personal housing provision fund rate by 25bps and will set up CNY 500bln in re-lending loans for elderly care and service consumption. Furthermore, the total quota of two monetary policy tools to support capital markets will be raised to CNY 800bln and they will lower interest rates on structural policy tools by 25bps with re-lending rates lowered by 25bps effective today, while Pan also stated that China will use multiple policy tools to make dynamic adjustments and will guide commercial banks to lower deposit rates.

- China’s financial regulator said they will expand the pilot scheme to allow insurance companies to invest in stock markets and will take further steps to stabilise the property market, while they will guide financial institutions to maintain steady financing support for the property market, guide banks to provide financing support for foreign trade companies affected by US tariffs and will approve CNY 60bln in long-term insurance funds into the stock market.

- China’s securities regulator said US tariff policy has brought great pressure to China’s capital markets but added that they will consolidate good momentum in capital markets and that China will roll out reform measures for tech boards. Furthermore, they will forcefully promote long-term capital into the stock market and said ample preparations have been made for dealing with external shocks.

- RBNZ Financial Stability Report stated that risks to the financial system have increased over the past six months and while the global economic environment has become more volatile, New Zealand's financial institutions are in a strong position to support the economy. RBNZ also stated that banks have strong capital and liquidity buffers in place to maintain credit flows even if conditions deteriorate further.

- PBoC says FX reserves USD 3.282tln end-April (prev. USD 3.241tln), gold reserves USD 243.59bln end-April (prev. USD 229.59bln)

DATA RECAP

- New Zealand HLFS Job Growth QQ (Q1) 0.1% vs. Exp. 0.1% (Prev. -0.1%)

- New Zealand HLFS Unemployment Rate (Q1) 5.1% vs. Exp. 5.3% (Prev. 5.1%)

- New Zealand Labour Cost Index QQ (Q1) 0.4% vs. Exp. 0.5% (Prev. 0.6%)

- New Zealand Labour Cost Index YY (Q1) 2.5% vs. Exp. 2.7% (Prev. 2.9%)