Europe Market Open: Fed maintained rates and noted risks to both sides of the mandate have risen

08 May 2025, 06:40 by Newsquawk Desk

- Fed kept rates unchanged; noted that risks to the economic outlook increased further and risks to both sides of the mandate have risen.

- President Trump said he is unwilling to lower tariffs to get China to the table; also reported that Trump is to rescind global chip curbs.

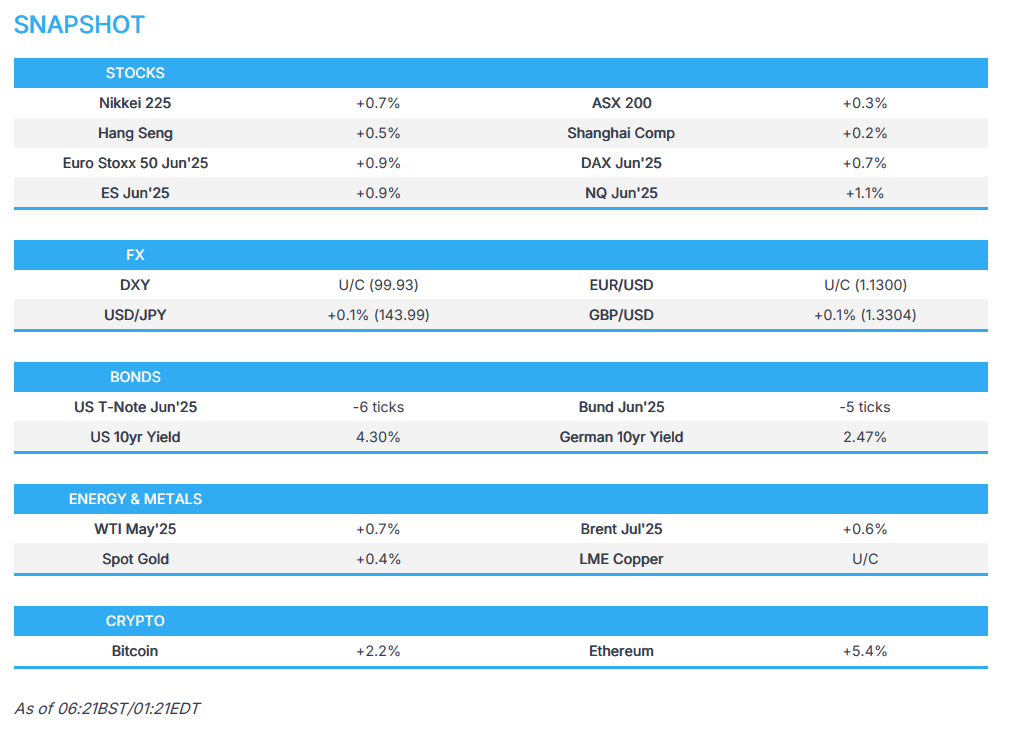

- APAC stocks were mostly higher following the mildly positive handover from Wall St; European stocks are set to open higher.

- DXY is steady with the USD mixed vs. peers, antipodeans lead, GBP underpinned by an expected trade deal with the US (to be announced today).

- Looking ahead, highlights include German Trade Balance, US Jobless Claims, Wholesale Sales & NY Fed SCE, BoE, Norges & Riksbank Policy Announcements, BoE DMP, BoE’s Bailey & BoC’s Macklem, Supply from Spain & US.

- Earnings from Coinbase, Cloudflare, Draftkings, Affirm, Shopify, ConocoPhillips, Warner Bros Discovery, Zealand Pharma, Maersk, Henkel, Lanxess, Rheinmetall, Infineon, Heidelberg Materials, Siemens Energy Leonardo, Mediobanca, Prysmian, Poste Italiane, Enel & BMPS.

US TRADE

EQUITIES

- US stocks were ultimately higher on the day but with gains capped and price action choppy in the aftermath of the FOMC decision which was largely as expected as the Fed kept rates unchanged although the accompanying statement noted that risks to the economic outlook increased further and that risks to both sides of the mandate have risen. Furthermore, Fed Chair Powell reiterated the wait-and-see approach, while trade related headlines were somewhat mixed with President Trump unwilling to lower tariffs to get China to the table and it was reported that President Trump is to rescind global chip curbs amid AI restrictions debate although this was regarding scrapping a Biden-era "AI diffusion rule" that was set to take effect on May 15th and would have restricted how US tech is exported.

- SPX +0.43% at 5,631, NDX +0.39% at 19,868, DJI +0.70% at 41,114, RUT +0.33% at 1,990.

- Click here for a detailed summary.

FOMC

- Fed kept rates on hold at 4.25-4.50%, as expected, in a unanimous decision and said economic outlook uncertainty has increased further (prev. uncertainty around the economic outlook has increased), while it added that the risks of higher unemployment and higher inflation have risen. Fed said the economy continues to expand at a solid pace despite swings in net exports affecting the data, and it maintained language that unemployment has stabilised at a low level and labour market conditions remain solid.

- Fed Chair Powell said the economy is in a solid position and inflation has come down a great deal, which is running somewhat above the 2% goal, while he added that the current stance of policy leaves the Fed well positioned to respond in a timely way. Powell also stated that tariffs so far are significantly bigger than expected, and as the economy continues to evolve, the Fed will determine the appropriate policy stance. Furthermore, he repeated if dual mandate goals are in tension, they will consider the distance from the goal and the time to close gaps, but stated it is time to wait before adjusting policy.

- Fed Chair Powell said during the Q&A it is too early to say which way risks will shake out when asked about what side of the mandate is in greater risk and he thinks policy is in a good place until they get more data to determine which way to go, while he added that policy is moderately restrictive and there is no hurry. Powell said it is appropriate to be patient and when things develop, they can move quickly if appropriate. Powell also said there are cases in which rate cuts would be appropriate this year, and cases where rate cuts would not be appropriate, while he cannot confidently say he knows the appropriate rate path and noted that Trump's pressure for rate cuts does not affect the Fed's job at all. Powell also commented that his gut tells him that uncertainty is extremely elevated, downside risks have increased, and that risks of higher unemployment and higher inflation have risen but are not yet in the data. Furthermore, when asked about March projections for two rate cuts, he said that he can't make a projection now and they have to wait until June, as well as stated that they are not in a situation where they can be pre-emptive and need to see more data.

TARIFFS/TRADE

- US President Trump posted on Truth "Big News Conference tomorrow [Thursday] morning at 10:00 A.M., The Oval Office, concerning a MAJOR TRADE DEAL WITH REPRESENTATIVES OF A BIG, AND HIGHLY RESPECTED, COUNTRY. THE FIRST OF MANY!!!". It was reported shortly after by NYT that the US is to announce a trade deal with the UK on Thursday.

- US President Trump told the US envoy to China to 'say hello' to Chinese President Xi and to handle consequential and complex issues, while he is confident the US envoy to China will do an exceptional job. Trump said they will take a look at exemptions, but is unsure on exemptions and he is not open to pulling back 145% tariffs, while he also stated that China should reassess who asked for a meeting and he is unwilling to lower tariffs to get China to the table. Furthermore, Trump said he might be easing chip policy to the Gulf.

- US President Trump is to rescind global chip curbs amid AI restrictions debate, according to sources cited by Bloomberg. The Trump administration will not enforce the so-called AI diffusion rule when it takes effect on May 15th and instead plans to develop a new rule that would strengthen the control of chips abroad, while "One element of the move to repeal the diffusion rule will be to impose chip controls on countries that have diverted chips to China, including Malaysia and Thailand, according to one of the sources".

- EU capitals reportedly want retaliation against US President Trump to be delayed to avoid a NATO clash, according to the FT.

NOTABLE HEADLINES

- US President Trump's big announcement is regarding a Medicare drug plan, according to Politico.

- US President Trump posted "We are making great progress on “The One, Big, Beautiful Bill.” Our Economy is doing well, but it’s going to BOOM in a way never seen before. We are going to do NO TAX ON TIPS, NO TAX ON SENIORS’ SOCIAL SECURITY, NO TAX ON OVERTIME, and much more. It will be the biggest Tax Cut for Middle and Working Class Americans by far, and it is time for Main Street to WIN. MAKE AMERICA GREAT AGAIN!"

- US Treasury Secretary Bessent said the unfettered ability to borrow has made the US more prolific and the market may discipline them one day, which they are working to avoid. Bessent said the conditions for a strong dollar are important for confidence and the Fed should focus on both price and employment goals.

- White House said the Treasury and Commerce departments have formulated plans for a sovereign wealth fund, but no final decisions have yet been made.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher amid some trade optimism and following the mildly positive handover from Wall St where price action was choppy in the aftermath of the FOMC meeting as the Fed kept the FFR at 4.25-4.50%, as expected, and noted that risks to the economic outlook increased further, while Fed Chair Powell reiterated a wait-and-see approach and ruled out a pre-emptive cut during the presser.

- ASX 200 marginally gained amid strength in gold miners, industrials and tech but with the upside capped by weakness in the top-weighted financial sector after Big 4 bank ANZ's earnings.

- Nikkei 225 was underpinned by recent currency weakness and trade deal optimism, although a return to the 37,000 level remained elusive.

- Hang Seng and Shanghai Comp remained positive following the previous day's PBoC's policy loosening, but with further upside in the mainland limited after recent comments from US President Trump, who was unwilling to lower tariffs to get China to the table.

- US equity futures (ES +0.8%, NQ +1.2%) benefited amid trade optimism after President Trump announced there will be a news conference on Thursday concerning a major trade deal with a big and highly respected country, while The New York Times reported the US will be announcing a trade deal with the UK.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.9% after the cash market closed with losses of 0.6% on Wednesday.

FX

- DXY gave back some of the prior day's spoils after strengthening in the aftermath of the FOMC meeting where the Fed held the FFR at 4.25-4.50% as expected in a unanimous decision, while the accompanying statement noted that members viewed the uncertainty around the economic outlook as having increased further from the March meeting and that risks of higher unemployment and higher inflation have increased. Furthermore, Fed Chair Powell maintained recent rhetoric in the press conference in which he advocated a wait-and-see/patient approach and stated they are not in a situation where they can be pre-emptive. Nonetheless, the uplift in the dollar index petered out after stalling just shy of the 100.00 level and as the focus shifted back to trade with President Trump flagging a major trade deal with a highly respected country, while the NYT reported that the US is to announce a trade deal with the UK.

- EUR/USD struggled to recoup some of its post-FOMC losses after rebounding from support around the 1.1300 level, while the EU is set to announce a provisional list of tariffs against the US, which will be enforced if trade talks fail.

- GBP/USD benefited from reports that the US is to announce a trade deal with the UK, but with further upside capped heading into a widely expected rate cut by the BoE at today's meeting.

- USD/JPY slightly pulled back from resistance at the 144.00 level in the absence of any major catalysts for Japan and with the BoJ Minutes from the March meeting a non-event given that there was a more recent meeting last week where the BoJ pushed back its timing to achieve the price goal.

- Antipodeans rebounded from yesterday's trough but have further to go to recover from the slide seen in the aftermath of the PBoC rate cuts.

- PBoC set USD/CNY mid-point at 7.2073 vs exp. 7.2385 (Prev. 7.2005).

- Brazil Central Bank hiked the Selic rate by 50bps to 14.75%, as expected with the decision unanimous, while it stated that additional caution is needed for the next meeting and the scenario also demands flexibility to incorporate data that impact the inflation outlook. Furthermore, the BCB said it will remain vigilant and the calibration of the appropriate tightening of the monetary policy will continue to be guided by the objective of bringing inflation back to the target in the relevant horizon.

FIXED INCOME

- 10yr UST futures were contained after stalling post-FOMC, given the lack of fresh clues on policy from Fed Chair Powell.

- Bund futures were uneventful but held on to recent gains after the prior day's momentum and as German trade data looms.

- 10yr JGB futures initially extended on its rebound from a weekly low but was later pressured by a weak 10yr JGB auction.

COMMODITIES

- Crude futures nursed some of the prior day's losses after sliding alongside economic uncertainty and demand concerns.

- Iran's oil minister said they continue to support OPEC+ decisions aimed at ensuring market stability.

- Spot gold was underpinned by a softer dollar and briefly reclaimed the USD 3,400/oz status.

- Copper futures were rangebound after yesterday's decline but were off the lows seen in the aftermath of the FOMC decision and presser where Fed Chair Powell ruled a pre-emptive rate cut.

CRYPTO

- Bitcoin edged higher throughout the session and returned to above the USD 99,000 level.

NOTABLE ASIA-PAC HEADLINES

- HKMA maintained its base rate at 4.75%, as expected, in lockstep with the Fed.

- BoJ Minutes from the March 18th-19th Meeting reiterated they are to raise rates if the economic outlook is realised and a member said it's appropriate to pay close attention to the new US policies and their impact on the global economy. Furthermore, a member said the BoJ would need to be particularly cautious when considering the timing of the next rate hike as downside risks stemming from US policies had rapidly heightened, while a member said that even with heightened uncertainties, it did not warrant BoJ to be always cautious and the BoJ may face a situation where it should act decisively.

GEOPOLITICS

MIDDLE EAST

- Yemen's Houthis said they targeted Israel with drones and the group will not hesitate to carry out strikes against the US if US strikes on Yemen resume.

RUSSIA-UKRAINE

- Ukraine Air Force said Russia launched guided bombs at Ukraine's Sumy region on three occasions on Thursday.

- European Commission proposed to add 15 new entities and individuals to its Russia hybrid attack sanctions framework and proposed sanctions on Russian individuals for chemical weapons use in the Ukraine war, according to Reuters citing EU sources.

- Polish PM Tusk said Poland and Germany will keep supporting Ukraine and they should work to maintain Schengen, while he added that they should cooperate on NATO infrastructure and that all of Europe, including Germany, should protect the border with Belarus and Russia.

OTHER

- South Korea reported that North Korea fired multiple short-range missiles and that North Korea's missile launch may have been to test performance for export.

EU/UK

NOTABLE HEADLINES

- UK PM Starmer is expected to promise on Thursday that his government will deliver a defence dividend for voters, framing an increase in military spending forced by a US shift away from underwriting Europe's security, as an economic opportunity, according to Reuters.

- NIESR lowered its UK 2025 GDP growth forecast to 1.2% from 1.5%, while it said Chancellor Reeves looks set to miss her budget targets again, partly due to the economic impact from her tax increase on employers, which raises the prospect of more tax hikes.

- UK and the European Union are deeply split over the terms of a youth mobility scheme that is a key part of a post-Brexit “reset” agreement, according to the FT citing fresh negotiating documents.

DATA RECAP

- UK RICS Housing Survey (Apr) -3.0 vs. Exp. -5.0 (Prev. 2.0)