US Market Open: Stocks gain and DXY tops 100.00 ahead of Trump's UK-US trade announcement; BoE due

08 May 2025, 10:35 by Newsquawk Desk

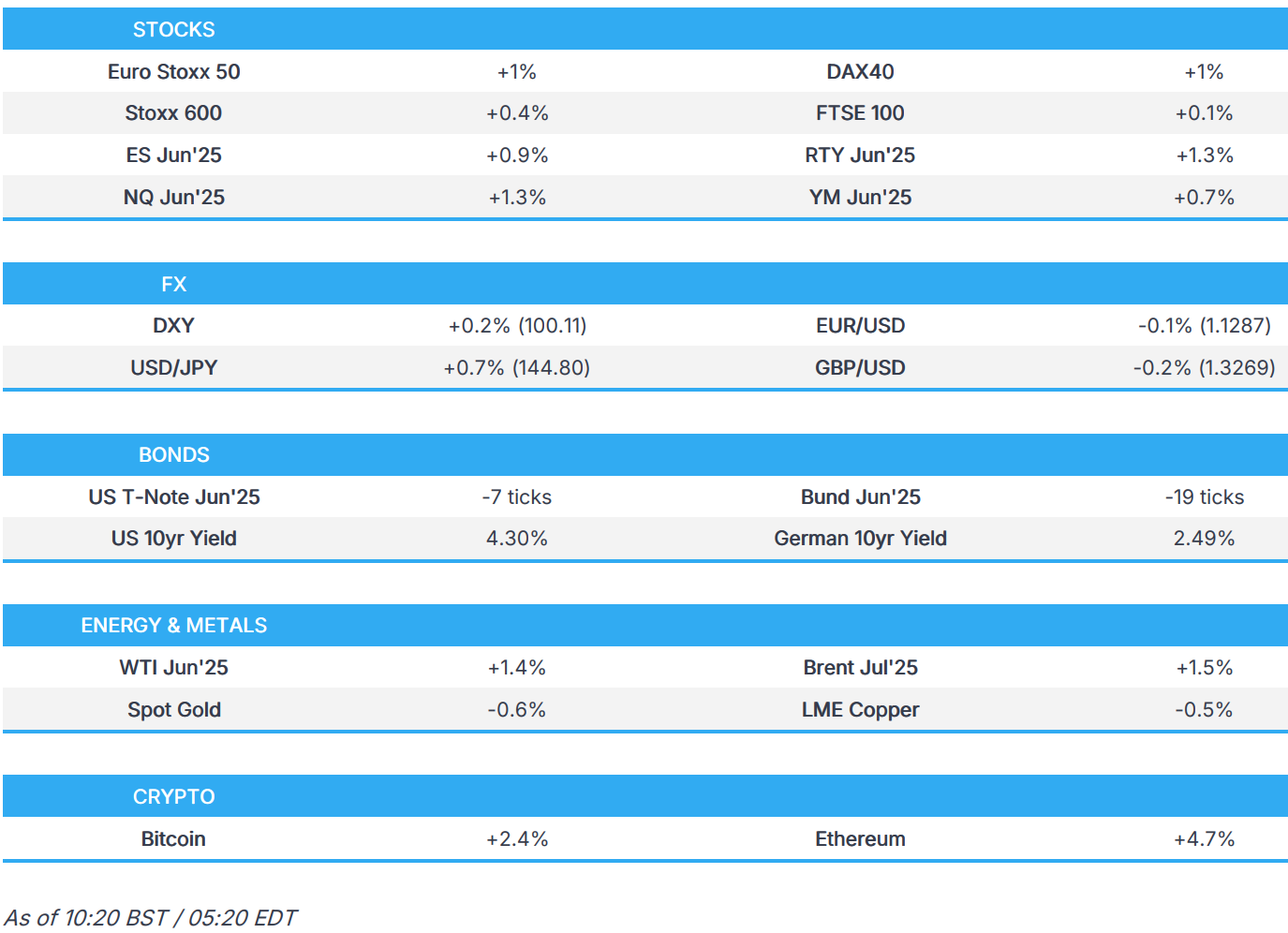

- Equities complex broadly positive in anticipation of US President Trump’s deal announcement; NQ +1.3%.

- DXY back above 100, EUR/USD slips onto a 1.12 handle, GBP eyes UK-US trade deal and BoE.

- Gilts edge higher into the BoE and Trump's announcement, USTs & Bunds slip slightly.

- USD pickup weighs on gold whilst crude remains focused on geopolitical developments.

- Looking ahead, US Jobless Claims, Wholesale Sales & NY Fed SCE, BoE Policy Announcement, BoE DMP, BoE’s Bailey & BoC’s Macklem, Supply from the US. Earnings from Coinbase, Cloudflare, Draftkings, Affirm, Shopify, ConocoPhillips, Warner Bros Discovery.

TARIFFS/TRADE

- US President Trump posted on Truth "Big News Conference tomorrow [Thursday] morning at 10:00 A.M., The Oval Office, concerning a MAJOR TRADE DEAL WITH REPRESENTATIVES OF A BIG, AND HIGHLY RESPECTED, COUNTRY. THE FIRST OF MANY!!!". It was reported shortly after by NYT that the US is to announce a trade deal with the UK on Thursday.

- EU capitals reportedly want retaliation against US President Trump to be delayed to avoid a NATO clash, according to the FT.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) opened mostly firmer and have traded with an upward bias throughout the European morning.

- European sectors are mixed; Tech takes the top spot, joined closely by Industrials whilst Healthcare lags. Tech benefits from post-earning strength in Infineon (+3%) - despite missing on headline metrics and highlighting that it sees 2025 rev. slightly lower Y/Y due to tariff impact.

- US equity futures (ES +0.8%, NQ +1%) are broadly in the green, in-fitting with the broader risk tone as markets await Trump’s trade announcement.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY saw an uptick in early European trade, taking the index back above the 100 threshold; no obvious driver was seen behind the move at the time. Last night's FOMC policy announcement had little follow-through into the USD with the Fed keeping rates unchanged as expected whilst noting that risks to the economic outlook increased further and risks to both sides of the mandate have risen. From a trade perspective, attention is on the details of the expected upcoming UK trade deal announcement whereby the agreement will be eyed as a proxy of what is to come. DXY has hit a new high for the week at 100.20.

- EUR is fractionally softer vs. the USD with Eurozone newsflow on the light side. On the trade front, the EU is set to announce today a provisional list of tariffs against the US which will be enforced if talks with the US fail. EUR/USD has reverted back to a 1.12 handle and hit a fresh low for the week at 1.1271.

- JPY is softer on account of the positive risk sentiment which has stemmed from hopes on the trade front. BoJ Minutes was a non-event given it recaps the March meeting. USD/JPY has ventured as high as 144.51.

- GBP is a touch softer vs. the USD but to a lesser degree than peers amid increased optimism on the trade front with the US and UK expected to announce a trade deal later today. That being said, it is worth noting that the announcement is set to be a "heads of terms" agreement, rather than a full deal, but substantive, according to Sky News. Attention now turns to Thursday's BoE meeting, which is expected to see policymakers deliver a 25bps rate cut; focus will be on any potential tweaks to guidance. Morgan Stanley expects the "gradual and careful" language to be removed to provide the MPC “space to accelerate cuts if needed”.

- Antipodeans are both slightly softer vs. the USD with domestic newsflow from Australia and New Zealand on the light side.

- SEK is a touch softer in the aftermath of the Riksbank policy announcement which saw the central bank stand pat on rates as expected. The accompanying statement noted that "it is somewhat more probable that inflation will be lower than that it will be higher than in the March forecast", adding that this "could suggest a slight easing of monetary policy going forward". However, the Bank did stress the uncertainty surrounding the outlook. EUR/SEK has been as high as 10.9424 but is yet to approach its 50DMA to the upside at 10.9491.

- Little follow-through seen in the NOK after the Norges bank stood pat on rates at 4.5% as expected. The accompanying statement noted that restrictive monetary policy is still needed, adding that, if the policy rate is lowered prematurely, prices may continue to rise rapidly. However, the outlook implies that the policy rate will most likely be reduced in the course of 2025.

- PBoC set USD/CNY mid-point at 7.2073 vs exp. 7.2385 (Prev. 7.2005).

- Brazil Central Bank hiked the Selic rate by 50bps to 14.75%, as expected with the decision unanimous, while it stated that additional caution is needed for the next meeting and the scenario also demands flexibility to incorporate data that impact the inflation outlook. Furthermore, the BCB said it will remain vigilant and the calibration of the appropriate tightening of the monetary policy will continue to be guided by the objective of bringing inflation back to the target in the relevant horizon.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- The Fed's decision to keep rates steady (as expected) and Powell stressing a wait-and-see approach to policy, sparked some two-way action in USTs - before then extending a little lower into the APAC session. As for today, US President Trump saying he will announce a trade deal (with the UK) today has managed to boost the risk tone. USTs currently a touch into the red but above yesterday’s low in a 111-11 to 111-19 band. Ahead, weekly jobless claims are due before the NY Fed SCE, in March it showed an increase in near-term inflation expectations and a slight moderation further out alongside an expected deterioration in the labour market. A 30yr auction is also scheduled.

- Gilts opened bang on the unchanged mark and despite an initial slip to a 93.35 low, comfortably above Wednesday’s 92.79 base, the benchmark has since been on a gentle grind higher despite the constructive risk tone as participants prepared for upcoming UK-specific risk events. Holding around its 93.54 session peak. Awaiting Trump’s 15:00BST press conference for details on a trade announcement which has since been confirmed to be between the US and UK. But before that, attention will be on the BoE where rates are expected to be cut by 25bps in a unanimous decision though the magnitude could be subject to dovish dissent.

- Bunds are softer, in-fitting with USTs and the constructive risk tone. In contrast to the US and UK, newsflow for the bloc has been a little lighter. No move to a surprisingly strong set of German Industrial data for March this morning. At the low end of a 131.35 to 131.65 band.

- Spain sells EUR 6.2bln vs. Exp. EUR 5.5-6.5bln 2.40% 2028, 2.70% 2030, 4.00% 2054 Bono & EUR 0.672bln vs. Exp. EUR 0.25-0.75bln 1.00% 2030 I/L

- Click for a detailed summary

COMMODITIES

- Crude is bid, but off best as the USD fights back in the European morning (see FX). Currently holding around the mid-point of today’s parameters which are just under USD 1/bbl in size and in very familiar levels from the last few days/weeks. At best, WTI and Brent got just above the USD 58.50/bbl and USD 61.50/bbl marks but failed to make any further ground as the DXY picked back up above the 100.00 mark.

- Gold is under pressure as the risk tone is supported by Trump’s trade announcement, an event we now know relates to the UK, and also the discussed recovery in the USD. Currently trading in a USD 3,320.68-3,414.50/oz range.

- Copper has been rangebound since APAC trade after the pressure seen on Wednesday with 3M LME Copper basically holding at the bottom end of yesterday’s USD 9.36-9.47k band.

- PBoC is reportedly to allow local lenders to purchase more USD to fund increased gold import quotas, via Reuters citing sources.

- Citi revises its 0-3 month point price for Brent to USD 55/bbl (prev. 60/bbl). No US-Iran deal and escalatory action could see prices return to USD +70/bbl.

- Iraq sets the June Barah medium crude OSP to Asia at plus USD 0.45/bbl to Oman/Dubai average, Europe minus USD 3.20bbl vs. dated Brent, North and South America minus USD 0.75/bbl vs. ASCI, according to SOMO.

- Kazakhstan (Apr) oil and condensate daily output +6.5% to 277k tons, according to Interfax; production in May seen at similar levels to April.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK RICS Housing Survey (Apr) -3.0 vs. Exp. -5.0 (Prev. 2.0)

- UK Halifax House Prices YY (Apr) 3.2% vs. Exp. 2.60% (Prev. 2.80%, Rev. 2.9%); MM (Apr) 0.3% vs. Exp. -0.1% (Prev. -0.5%)

- UK BBA Mortgage Rate (Apr) 7.21% (Prev. 7.23%)

- German Trade Balance, EUR, SA (Mar) 21.1B vs. Exp. 19.1B (Prev. 17.7B); Imports MM SA (Mar) -1.4% vs. Exp. 0.4% (Prev. 0.7%); Exports MM SA (Mar) 1.1% vs. Exp. 1.0% (Prev. 1.8%); Industrial Output MM (Mar) 3.0% vs. Exp. 0.8% (Prev. -1.3%)

- Spanish Ind Output Cal Adj YY (Mar) 1.0% (Prev. -1.9%)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer is expected to promise on Thursday that his government will deliver a defence dividend for voters, framing an increase in military spending forced by a US shift away from underwriting Europe's security, as an economic opportunity, according to Reuters.

- Sky's Coates says his sources are confirming that the US-UK trade deal claims are correct. Will be a "heads of terms" agreement, rather than a full deal, but substantive.

- NIESR lowered its UK 2025 GDP growth forecast to 1.2% from 1.5%, while it said Chancellor Reeves looks set to miss her budget targets again, partly due to the economic impact from her tax increase on employers, which raises the prospect of more tax hikes.

- Swedish Riksbank Rate 2.25% vs. Exp. 2.25% (Prev. 2.25%); it is somewhat more probable that inflation will be lower than that it will be higher than in the March forecast. This could suggest a slight easing of monetary policy going forward.

- Norges Bank Key Policy Rate 4.5% vs. Exp. 4.5% (Prev. 4.5%); outlook implies that the policy rate will most likely be reduced in the course of 2025.

NOTABLE US HEADLINES

- US President Trump's big announcement is regarding a Medicare drug plan, according to Politico.

- US President Trump posted "We are making great progress on “The One, Big, Beautiful Bill.” Our Economy is doing well, but it’s going to BOOM in a way never seen before. We are going to do NO TAX ON TIPS, NO TAX ON SENIORS’ SOCIAL SECURITY, NO TAX ON OVERTIME, and much more. It will be the biggest Tax Cut for Middle and Working Class Americans by far, and it is time for Main Street to WIN. MAKE AMERICA GREAT AGAIN!"

- White House said the Treasury and Commerce departments have formulated plans for a sovereign wealth fund, but no final decisions have yet been made.

GEOPOLITICS

- "The Trump administration has held talks in recent days with Arab countries to promote a humanitarian aid distribution project in the Gaza Strip, according to two Western diplomats speaking to the Post.", via Amichai Stein on X

- Ukraine Air Force said Russia launched guided bombs at Ukraine's Sumy region on three occasions on Thursday.

- South Korea reported that North Korea fired multiple short-range missiles and that North Korea's missile launch may have been to test performance for export.

CRYPTO

- Bitcoin is on a stronger footing today and has climbed to around USD 99.5k; next eyeing the round USD 100k mark.

APAC TRADE

- APAC stocks were mostly higher amid some trade optimism and following the mildly positive handover from Wall St where price action was choppy in the aftermath of the FOMC meeting as the Fed kept the FFR at 4.25-4.50%, as expected, and noted that risks to the economic outlook increased further, while Fed Chair Powell reiterated a wait-and-see approach and ruled out a pre-emptive cut during the presser.

- ASX 200 marginally gained amid strength in gold miners, industrials and tech but with the upside capped by weakness in the top-weighted financial sector after Big 4 bank ANZ's earnings.

- Nikkei 225 was underpinned by recent currency weakness and trade deal optimism, although a return to the 37,000 level remained elusive.

- Hang Seng and Shanghai Comp remained positive following the previous day's PBoC's policy loosening, but with further upside in the mainland limited after recent comments from US President Trump, who was unwilling to lower tariffs to get China to the table.

NOTABLE ASIA-PAC HEADLINES

- HKMA maintained its base rate at 4.75%, as expected, in lockstep with the Fed.

- BoJ Minutes from the March 18th-19th Meeting reiterated they are to raise rates if the economic outlook is realised and a member said it's appropriate to pay close attention to the new US policies and their impact on the global economy. Furthermore, a member said the BoJ would need to be particularly cautious when considering the timing of the next rate hike as downside risks stemming from US policies had rapidly heightened, while a member said that even with heightened uncertainties, it did not warrant BoJ to be always cautious and the BoJ may face a situation where it should act decisively.

- China is weighing housing market overhaul to curb pre-sales, via Bloomberg