Europe Market Open: APAC stocks firmer following a strong handover; US to cut de minimis on China to 54% from 120%

13 May 2025, 06:50 by Newsquawk Desk

- APAC stocks traded mostly higher following the rally on Wall St owing to the US-China trade war de-escalation after both sides agreed to cut tariffs by 115ppts for an initial period of 90 days, although some of the gains were capped as the euphoria began to moderate.

- White House Executive Order said US will cut the minimum tariff on China shipments from 120% to 54%, and a minimum flat fee of USD 100 is to remain.

- DXY took a breather and gave back some of yesterday's firm gains; 10yr UST futures traded rangebound after recently suffering from a lack of haven appeal

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.2% after the cash market finished with gains of 1.6% on Monday.

- Looking ahead, highlights include UK Jobs, German ZEW, US CPI, Speakers include US President Trump, BoE’s Pill, Bailey & ECB’s Rehn, Supply from Netherlands, UK, Italy & Germany, Earnings from JD.Com, Intuitive Machines, On, Munich Re, Hannover Re, Bayer, K+S, Leg, Ferrovial & A2A.

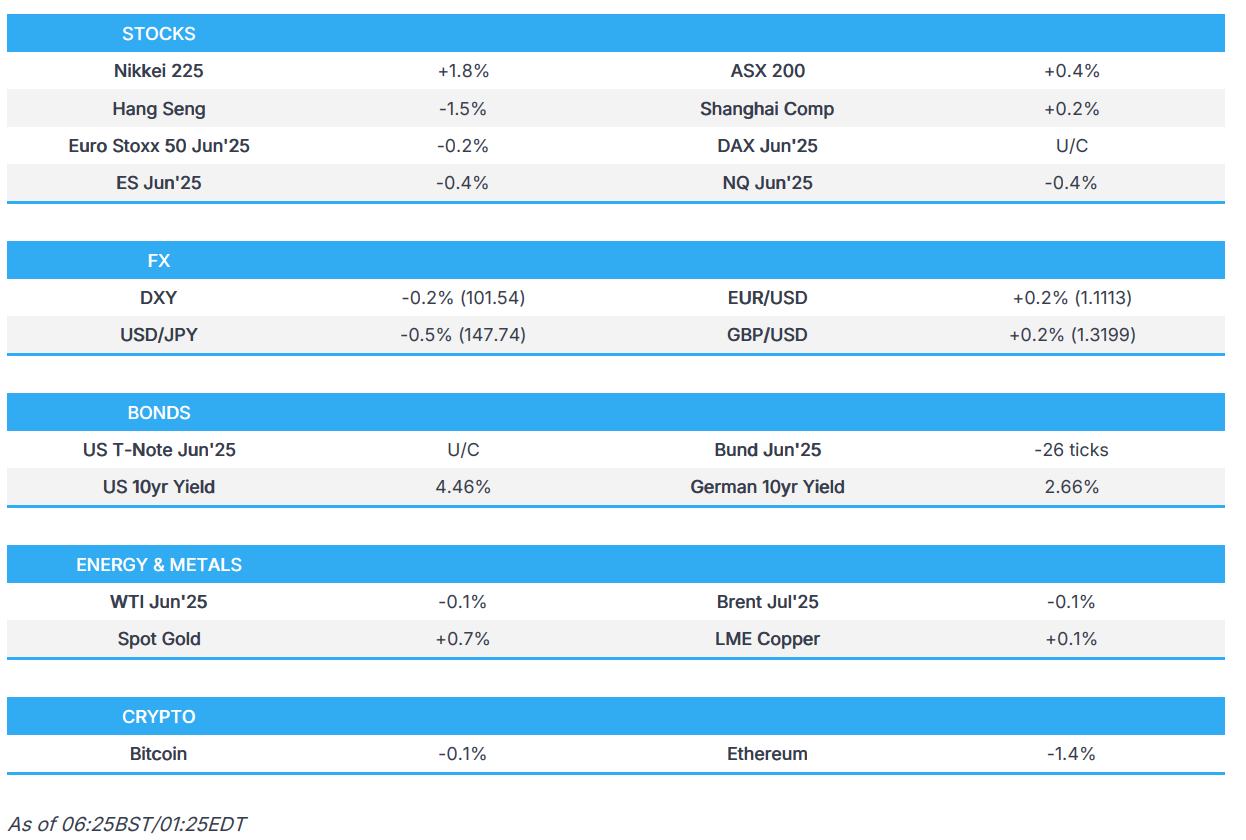

SNAPSHOT

US TRADE

EQUITIES

- US stocks rallied following the positive trade developments between the US and China, which both agreed to cut tariffs on each other by 115ppts for an initial period of 90 days in what was a much larger than expected roll back. The combined 145% US tariffs on China and China's levies on US goods will drop to 30% and 10%, respectively. The announcement spurred global risk-on trade with upside in the Dollar, US equities, and crude, while havens sold off.

- SPX +3.26% at 5,844, NDX +4.02% at 20,868, DJI +2.81% at 42,410, RUT +3.42% at 2,092.

- Click here for a detailed summary.

TARIFFS/TRADE

- White House Executive Order said US will cut the minimum tariff on China shipments from 120% to 54%, and a minimum flat fee of USD 100 is to remain.

- USTR Greer said the outcome of US-China tariffs talks was seen as pragmatic, while he added China has agreed to remove countermeasures and noted if things don't work out, China tariffs can go back up.

- Chinese President Xi said there are no winners in tariff wars and trade wars, while he added that only when various countries work together can they maintain world peace, stability and promote global development. Xi said bullying and tyranny will only isolate oneself, and noted that China supports Latin America and the Caribbean in expanding their influence in the multilateral arena with China willing to deepen cooperation with Latin America in infrastructure, agriculture, food, energy and minerals.

- Canadian PM Carney and UK PM Starmer agreed to strengthen trade, commercial and defence ties in a phone call, according to a statement from Canada.

- China removes ban on Boeing (BA) deliveries after US trade truce, via Bloomberg.

NOTABLE HEADLINES

- Fed's Goolsbee (2025 voter) said tariffs would still have a stagflationary impulse and the temporary nature of the deal would weigh on the economy, while he added that the bar for action has to be high. Furthermore, he endorsed the waiting approach again due to uncertainty and said the Fed could afford to take time for policy decisions, according to NYT.

- Fed SLOOS stated US banks reported a drop in demand for C&I loans in Q1, while it was the weakest for large firms since Q3.

- WSJ's Timiraos posted that Goldman Sachs shifted the timing of its next expected Fed cut to December from July, while it stated "In light of these developments and the meaningful easing in financial conditions over the last month, we are raising our 2025 growth forecast by 0.5pp to 1% Q4/Q4 and reducing our 12-month recession odds to 35%" and "lowered our core PCE inflation path to peak at 3.6% (vs. 3.8% previously)".

- US President Trump posted "We are going to slash the cost of prescription drugs, and we will bring fairness to America. Drug prices will come down—We're gonna cut out the middlemen and facilitate the direct sale of drugs at the most favored nation price directly to the American citizen!"

- US President Trump posted "This week the Republicans are meeting in the Tax, Energy, and Agriculture Committees on major pieces of “THE ONE, BIG, BEAUTIFUL BILL.”

- US House tax committee proposed to end consumer EV tax credit by end of year instead of 2032 and proposed to phase out of key clean energy tax credit (45y), with expiry in 2031, while it seeks to end in two years the 'transferability' of IRA tax credits that allow developers to sell credits to raise project funds. It was also reported that the House Republicans' bill would exempt workers' tips from income tax with exceptions and includes a tax break on overtime through 2028, while the SALT deduction cap would be increased to USD 30k for joint filers (prev. 10k), according to the bill text.

APAC TRADE

EQUITIES

- APAC stocks traded mostly higher following the rally on Wall St owing to the US-China trade war de-escalation after both sides agreed to cut tariffs by 115ppts for an initial period of 90 days, although some of the gains were capped as the euphoria began to moderate.

- ASX 200 edged higher amid outperformance in tech and energy but with further advances contained by weakness in defensives and gold miners.

- Nikkei 225 rallied to above the 38,000 level following the cooling in US-China trade tensions but with the index off intraday highs amid some profit-taking and a slight pullback in USD/JPY, while BoJ rhetoric continued to signal future hikes if prices and the economy improved.

- Hang Seng and Shanghai Comp lagged despite the de-escalation in the US-China trade war which the Hong Kong benchmark already had its opportunity to react to yesterday, while questions lingered on what will happen during the 90-day reprieve as the trade deficit remains and the current 30% tariff on Chinese goods still a relatively high level.

- US equity futures mildly pulled back following yesterday's surge and with participants also awaiting the incoming US CPI data.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 0.2% after the cash market finished with gains of 1.6% on Monday.

FX

- DXY took a breather and gave back some of yesterday's firm gains which were spurred by the de-escalation in the trade war following the US-China agreement to reduce tariffs by 115ppts on each other's goods, which resulted in the largest gain in the DXY since November last year. Aside from trade headlines, updates were relatively light and the remarks from Fed officials provided little incrementally, while the attention now turns to US CPI data.

- EUR/USD saw some slight reprieve from the prior day's selling pressure and just about returned to the 1.1100 handle, but with the rebound in the single currency limited following renewed criticism from US President Trump who stated the EU has been brutal on drug prices, was the most difficult on drug subsidies, and is nastier than China.

- GBP/USD gradually attempted to reclaim the 1.3200 status in quiet trade as the recent rhetoric from BoE officials provided little to shift to dial and with participants looking ahead to incoming UK employment and wages data.

- USD/JPY mildly pulled back following its recent ascent above the 148.00 level which was facilitated by haven outflows and as US yields climbed on the US-China trade war de-escalation, while the latest rhetoric from the BoJ continued to signal expectations for further hikes if the economy and prices improve.

- Antipodeans nursed some of their recent losses with the help of a firmer PBoC reference rate setting and the mostly positive risk environment.

- PBoC set USD/CNY mid-point at 7.1991 vs exp. 7.2188 (Prev. 7.2066).

FIXED INCOME

- 10yr UST futures traded rangebound after recently suffering from a lack of haven appeal but with downside cushioned by support near the 110.00 level.

- Bund futures languished around Monday's lows after slipping beneath the 130.00 level with prices not helped ahead of incoming supply and ZEW data.

- 10yr JGB futures took a hit following the US-China trade war de-escalation and with demand also constrained after an uneventful BoJ Summary of Opinions release which noted that a member said the central bank is likely to continue raising interest rates in line with improvements in the economy and prices, while the results of the latest 30yr JGBs auction were mixed and showed a higher b/c but lower accepted prices.

COMMODITIES

- Crude futures were mildly lower after pulling back from the peaks seen in the aftermath of the US-China tariff rollback announcement, while there was little fresh in terms of energy-related catalysts and participants look ahead to whether the Ukraine-Russia talks will go ahead in Turkey later this week.

- Spot gold remained lacklustre after declining yesterday alongside the trade-related optimism and ahead of the latest US inflation data.

- Copper futures traded sideways after retreating yesterday despite the positive tariff developments with prices subdued by recent dollar strength.

CRYPTO

- Bitcoin faded some of its recent gains with prices back beneath the USD 102k level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Summary of Opinions from the April 30th-May 1st meeting stated that one member said the central bank is likely to continue raising interest rates in line with improvements in the economy and prices, while a member said the BoJ must make policy decisions without preconception as uncertainty over the outlook is very high. There was also the opinion of no change to the BoJ's rate-hike stance as real interest rates are deeply negative, but risks must be scrutinised and the BoJ has little choice but to take a wait-and-see stance until developments surrounding US trade policy stabilise to some extent. Furtheremore, a member said that uncertainty surrounding economy and price outlook is high and the likelihood of achieving price goal is not as high as in the past, while it was stated that the BoJ will enter a temporary pause in rate hikes but shouldn't slide into excessive pessimism and must guide policy nimbly and flexibly.

DATA RECAP

- Australian Westpac Consumer Sentiment (May) 92.1 (Prev. 90.1)

- Australian NAB Business Confidence (Apr) -1.0 (Prev. -3.0)

- Australian NAB Business Conditions (Apr) 2.0 (Prev. 4.0)

GEOPOLITICS

MIDDLE EAST

- US Secretary of State Rubio said the State Department is sanctioning three Iranian nationals and one Iranian entity with ties to Iran's organisation of defensive innovation and research.

RUSSIA-UKRAINE

- Russian Foreign Minister Lavrov discussed with his Turkish counterpart issues related to May 15th direct talks with Ukraine.

- US State Department said Secretary of State Rubio discussed a path to peace and a ceasefire in Ukraine with French, German, Polish and Ukrainian foreign ministers as well as the EU High Representative.

EU/UK

NOTABLE HEADLINES

- BoE's Taylor said erosion of business confidence in the UK has continued in REC and PMI surveys, while he added the tariff shock was bigger than anyone expected and there is a sense of precaution and concern. Furthermore, he said wage settlements data is coming in line with expectations for slower wage growth.

- Barclaycard UK April Consumer Spending rose 4.5% Y/Y, which was the biggest increase since June 2023.

- ECB strategy review will largely endorse past policies, including QE, despite some policymakers’ criticisms, while the ECB is to keep reference to ‘forceful action’ when rates and inflation are low following the review, according to sources cited by Reuters.

- ECB's Escriva said they must be humble in assessing the current situation.

- ECB's Nagel said they shouldn't overreact to individual announcements.

DATA RECAP

- UK BRC Retail Sales YY (Apr) 6.8% (Prev. 0.9%)

- UK BRC April Total Retail Sales 7.0% (Prev. 1.1%)