US Market Open: US equity futures lower, DXY makes a fresh WTD low, Crude falls on constructive Trump-Syria speak

14 May 2025, 11:20 by Newsquawk Desk

- White House economic adviser Hassett says the administration has more than 20-25 deals on the table and when President Trump returns, he will announce the next deal, according to a Fox interview.

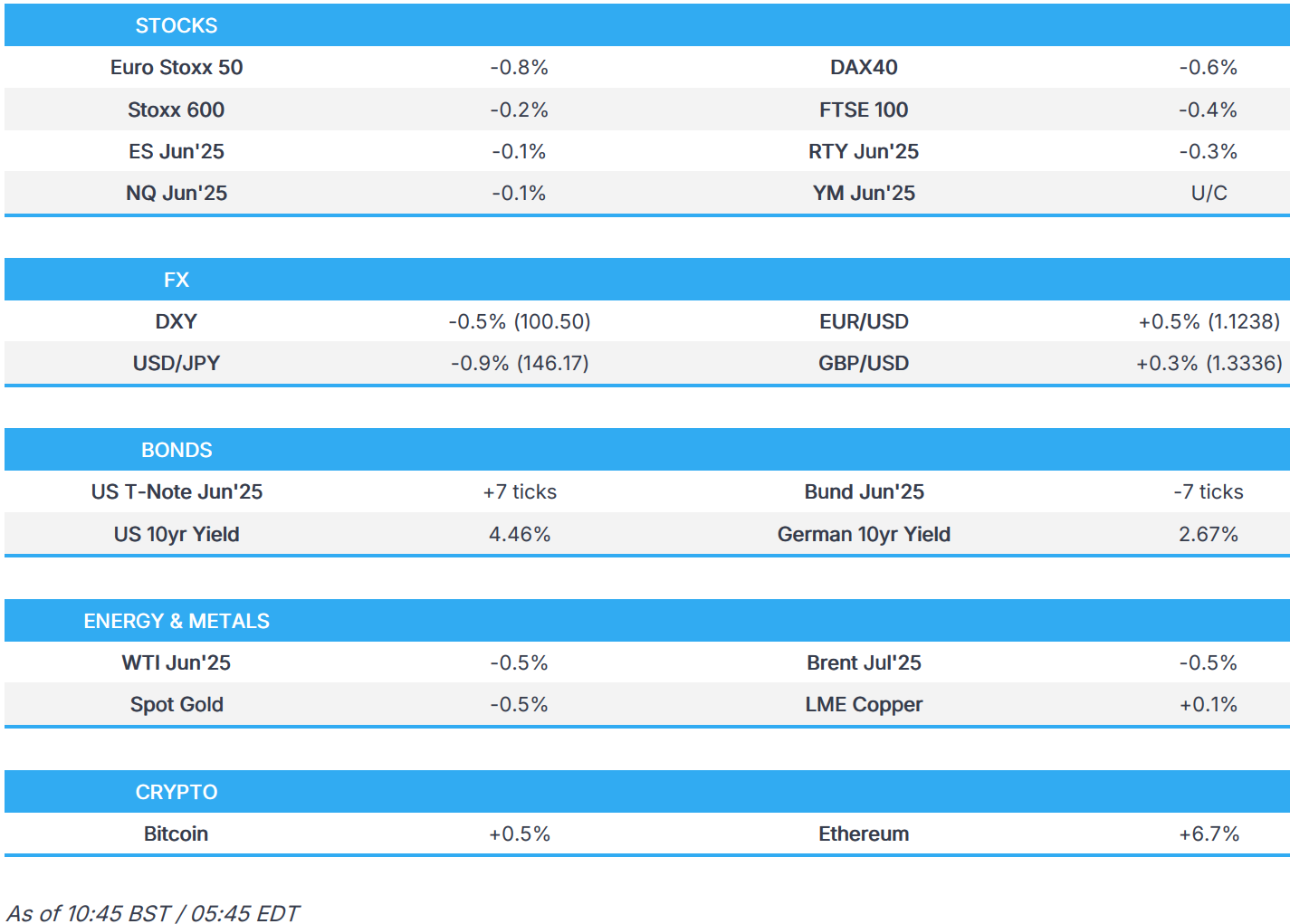

- Stocks opened mixed but now hold a downward bias as the risk tone dips; US futures flat/modestly lower.

- DXY is hit and makes a fresh WTD low, JPY leads.

- Bonds hold an upward bias as risk appetite deteriorates, Bunds see modest upside on a well-received German auction.

- Crude clipped as Trump speaks in Saudi, commodities fail to benefit from USD downside.

- Looking ahead, OPEC MOMR Speakers including ECB’s Cipollone, Fed’s Jefferson & Daly. Earnings from Cisco Systems, CoreWeave.

TARIFFS/TRADE

- White House economic adviser Hassett said the administration has more than 20-25 deals on the table with deals close to being finalised and when President Trump returns, he will announce the next deal, according to a Fox interview.

- US-China trade ceasefire is to drive early Black Friday and Christmas stockpiling with ports and shipping companies expecting a surge in demand as retailers take advantage of lower tariffs on Chinese imports, according to the FT.

- China criticised a trade deal between the UK and US that could be used to squeeze Chinese products out of British supply chains, according to the FT.

- Mexico's Economy Minister said they hope to start the USMCA review as soon as possible to give consumers and investors clarity.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) opened modestly mixed and on either side of the unchanged mark; since, the risk tone has deteriorated to display a mostly negative picture in Europe.

- European sectors opened mixed and with no clear theme or bias, and with the breadth of the market fairly narrow. Real Estate takes the top spot, joined closely by Telecoms and then Utilities to complete the top three. Autos sit towards the foot of the pile, driven by post-earning weakness in Daimler Truck (-1.1%).

- US equity futures are flat/modestly lower, attempting to hold onto the gains seen yesterday, strength which was in-part spurred by the plethora of deals announced/reported on during the Saudi event.

- Barclays raises its 2025 year-end price target for STOXX 600 to 540 (prev. 490, currently 545.09).

- Barclays European Equity Strategy downgrades Consumer Staples to Underweight; upgrades Consumer Discretionary to Market Weight (prev. Underweight).

- Goldman Sachs lifts its Stoxx 600 target for the next 12-months to 570 (prev. 520).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY began the European session on a modestly weaker footing, continuing to pare back some of the US-China induced upside. As the session progressed, some hefty Dollar pressure was seen, as the risk tone deteriorated and with some traders pointing towards a technical driven move. Some focus may also be on Deputy Finance Minister Choi's meeting with Kaproth of the US Treasury on May 5th to discuss FX. DXY currently towards the lower end of a 100.28-101.02 range. Data docket ahead is thin, focus will be on commentary from Fed Vice Chair Jefferson and Fed's Daly (2027 voter) - do note that in prepared remarks from Waller, he did not comment on monetary policy.

- EUR is on a firmer footing, largely benefiting from the broader Dollar weakness, rather than any EZ-specific updates, which have been lacking in today’s session. To recap, Spanish and German Final inflation figures were unrevised. Elsewhere, ECB's Nagel said "there is a good probability the inflation target will be maintained; current uncertainty will be the new "normal", central banks have to get used to manage it" - remarks which had little impact on the pair. The Single Currency has made a fresh WTD high at 1.1264.

- JPY is the best-performing G10 currency thus far; early morning strength was thanks to the broadly softer US yield environment, and with some modest deterioration in the risk tone (leading to broader Dollar weakness) USD/JPY managed to dip back below the 147.00 mark to a fresh low at 145.76, taking out the 50 DMA at 146.18.

- GBP is modestly firmer vs the broadly weaker Dollar, but is a little weaker vs EUR. Today has seen a few appearances from BoE members; starting with arch-hawk Mann, she noted that “UK labour market has been more resilient than expected. Worried that household inflation expectations have increased”. Elsewhere, Breeden released a text publication, but that focused more on supervision matters rather than on monetary policy. There was little price action sparked by both members.

- Antipodeans are modestly firmer vs the weaker Dollar; AUD/USD currently trading at the upper-end of a 0.6464-0.65 range; NZD/USD in a 0.5931-0.5968 parameter.

- PBoC set USD/CNY mid-point at 7.1956 vs exp. 7.1813 (Prev. 7.1991)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A similar setup to Tuesday morning as USTs find themselves marginally in the green while peers across the pond are a touch in the red. USTs find themselves at the upper-end of a very thin 110-01 to 110-09 band. Fed's Waller did not comment on monetary policy in prepared remarks; next up, Jefferson and Daly.

- Bunds are in-fitting with action at this time on Tuesday, a touch softer in narrow parameters with specifics for the bloc fairly light. No move to a handful of final data points from Germany and Spain. Elsewhere, ECB's Nagel said "there is a good probability the inflation target will be maintained; current uncertainty will be the new "normal", central banks have to get used to manage it" - remarks which had little impact on the pair. Some modest upside was seen as the risk tone was hit a little in European trade and currently trades in a 129.29-59 band. Some modest upside was seen following a well received Bund auction.

- Again, echoes of the dynamic on Tuesday as Gilts find themselves the modest fixed underperformer. Specifics for the UK are a touch light, remarks from BoE’s Breeden this morning largely stayed clear of monetary policy. Before Breeden, “activist” Mann was on the wires and expressed concern that the labour market has been more resilient than forecast and that household inflation expectations have increased; overall, her commentary was hawkish and may be factoring into the bearish bias for Gilts, but nothing overly surprising from the dissenter.

- UK to sell GBP 4.25bln 4.50% 2035 Gilt: b/c 3.13x (prev. 2.85x), average yield 4.673% (prev. 4.638%) & tail 0.3bps (prev. 0.4bps).

- Germany sells EUR 1.313bln vs exp. EUR 1.5bln 1.25% 2048 Bund and EUR 0.818 vs exp. EUR 1bln 2.50% 2054 Bund.

- Click for a detailed summary

COMMODITIES

- The crude complex is failing to benefit from the weaker dollar, as it gives back a little of Tuesday’s strength with today’s focus on US President Trump in Riyadh, where commentary has weighed on benchmarks, currently down by around USD 0.40/bbl on the day. Crude edged lower this morning amid constructive language regarding the Middle East from the US President, who announced the lifting of sanctions on Syria, expressed interest in normalizing relations, and emphasized a vision for a peaceful and prosperous region. WTI and Brent are just above session lows, in respective USD 62.86-63.68 and 65.82-66.59/bbl ranges.

- OPEC MOMR will be released at 13:00 BST (08:00 EDT).

- Spot Gold, like Crude, is failing to benefit from the weaker dollar, which sees the Dollar index lower by 0.4%. While pressured, the benchmark is in a thin c. USD 30/oz band and one that is essentially a repeat of the confines from Tuesday.

- Copper is modestly firmer, and trading at session highs as base metals are broadly benefitting from Dollar weakness. 3M LME Copper currently in a USD 9,562.6-9,638.45/t range.

- US Private Inventory Data (bbls): Crude +4.3mln (exp. -1.1mln), Distillate -3.7mln (exp. 0.1mln), Gasoline -1.4mln (exp. -0.6mln), Cushing -0.9mln.

- Click for a detailed summary

NOTABLE DATA RECAP

- German and Spanish Final Inflation metrics were unrevised.

NOTABLE EUROPEAN HEADLINES

- BoE's Mann says the UK labour market has been more resilient than expected. Worried that household inflation expectations have increased. Need to see a loss of pricing power by firms, however, goods price inflation is increasing. Trade aversion will result in lower global good prices. Firms will look for the opportunity to rebuild their margins. "Dollar is still king".

- BoE's Breeden: "A macro-prudential approach to the supervision of CCPs is essential given their central role in the financial system".

- ECB's Nagel says there is a good probability the inflation target will be maintained; current uncertainty will be the new "normal", central banks have to get used to manage it Very supportive of the new (German) fiscal debt brake, however, it is clear that Germany will need to return to fiscal rules in the future. USD is very important, but the EUR's role will become stronger as a reserve currency in the next few years.

- Hapag Lloyd (HLAG GY) CEO says they have seen an increase in orders for China-US shipments by more than 50% W/W; demand is considerably higher compared with the time before US tariffs.

NOTABLE US HEADLINES

- Fed's Goolsbee (2025 Voter) says some part of April inflation represents the lagged nature of data and the Fed is still holding its breath. It will take time for current inflation trends to show up in data. Right now is a time for the Fed to wait for more information and try get past the noise in the data. Cannot jump to conclusions about long-term trends given all the short term volatility.

- US House Speaker Johnson said the GOP will likely reach a deal on the state and local taxes cap on Wednesday.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Ministry spokesman said they have made it clear that no agreement will be reached with the US without concrete guarantees, according to Iran International. It was also reported that Iran is to hold talks with European parties on Friday in Istanbul, according to European and Iranian sources cited by Reuters.

- Israel's military said it identified the launch of a missile towards Israeli territory from Yemen which was intercepted.

- Jordanian army said a rocket of unknown origin landed in a desert area in the Ma'an, according to a source via X.

- US President Trump is meeting Syrian President al-Sharaa, via AP.

- US President Trump says the US wants to do a deal with Iran. Reiterates that Iran cannot have a nuclear weapon. Lifting sanctions on Syria. Exploring normalising relations with them. Wants a peaceful and prosperous Middle East. Special relationship with Saudi Arabia.

- Syria's President told US President Trump that they are inviting US firms to invest in Syria's oil and gas sector.

OTHER

- Senior Russian Lawmaker says the makeup of the Russian delegation to Istanbul for the Ukraine talks will be known on Wednesday evening, via Telegram

- China's Defence Minister met with the UN Secretary General on Tuesday and said that China will put forward new peacekeeping commitments, while China will support the reform and transformation of UN peacekeeping. Furthermore, the Minister said China is always a staunch supporter and constructive force for UN peacekeeping operations, according to Xinhua.

CRYPTO

- Bitcoin is on a slightly firmer footing and trades just above USD 103k; Ethereum continues to extend gains, currently higher by around +6%.

APAC TRADE

- APAC stocks traded somewhat mixed but with the region predominantly in the green following the momentum from the constructive performance on Wall St, where most major indices closed higher in the aftermath of the softer-than-expected US CPI data, although demand was contained overnight amid a lack of fresh major catalysts and as participants digested earnings releases.

- ASX 200 lacked firm direction as strength in energy and tech was counterbalanced by weakness in utilities and consumer stocks, while financials were rangebound despite Australia's largest bank CBA reporting an increase in profits.

- Nikkei 225 wiped out opening gains and briefly reverted to a sub-38,000 level with the list of worst performers in the index dominated by companies that had just reported earnings results.

- Hang Seng and Shanghai Comp gained amid strength in Chinese healthcare stocks and tech names leading the upside in Hong Kong ahead of Tencent and Alibaba earnings results scheduled for today and tomorrow, respectively, while the upside in the mainland was limited amid a lack of major fresh catalysts.

NOTABLE ASIA-PAC HEADLINES

- South Korea is preparing support measures for small and medium-sized firms expected to be hit by tariffs, according to Reuters citing the government.

- CATL (300750 CH/3750 HK) is reportedly to set a price of HKD 263/shr for its upcoming Hong Kong listing, via Reuters citing sources; to increase the HK listing size by 17.7mln shares.

- Foxconn (2317 TW) Q1 (TWD): net 42.12bln (exp. 37.9bln); operating 46.5bln (exp. 46.3bln), revenue 1.64tln (exp. 1.65tln); expects 2025 revenue to see significant growth Y/Y (prev. exp. to grow "strongly").

- Tencent (700 HK) Q1 (CNH) Revenue 180.02bln (exp. 175.6bln), Op. Profit 57.57bln (exp. 59.2bln), Adj. Net Income 61.33bln (exp. 59.68bln).

DATA RECAP

- Japanese Corp Goods Price MM (Apr) 0.2% vs. Exp. 0.2% (Prev. 0.4%); YY (Apr) 4.0% vs. Exp. 4.0% (Prev. 4.2%)

- Australian Wage Price Index QQ (Q1) 0.9% vs. Exp. 0.8% (Prev. 0.7%); YY (Q1) 3.4% vs. Exp. 3.2% (Prev. 3.2%)

- China April M2 +8% (exp. +7.3%); New Yuan Loans 280bln (exp. 700bln) end-April: Yuan Lending 7.2% (exp. 7.4%)