US Market Open: US Futures subdued and Fixed edges higher into a heavy data slate and Powell; Crude slips on Iran deal optimism

15 May 2025, 10:55 by Newsquawk Desk

- European equities are subdued awaiting US data and Fed Chair Powell; US equity futures also tilt lower (ES -0.6%).

- DXY is subdued and contained whilst havens seen some inflows amid the broader risk tone.

- Fixed income benchmarks trade slightly firmer into US data and Fed Chair Powell's speech.

- Crude futures are curtailed by Trump suggesting the US is getting close to a deal with Iran, while metals await data & Powell.

- Looking ahead, highlights include US NY Fed Manufacturing, Jobless Claims, Philly Fed Index, PPI, Retail Sales & Industrial Production, IEA OMR, Speakers include ECBʼs de Guindos; Fed Chair Powell & Barr, BoEʼs Dhingra. Earnings from Applied Materials, Take-Two, Alibaba, Walmart, Deere.

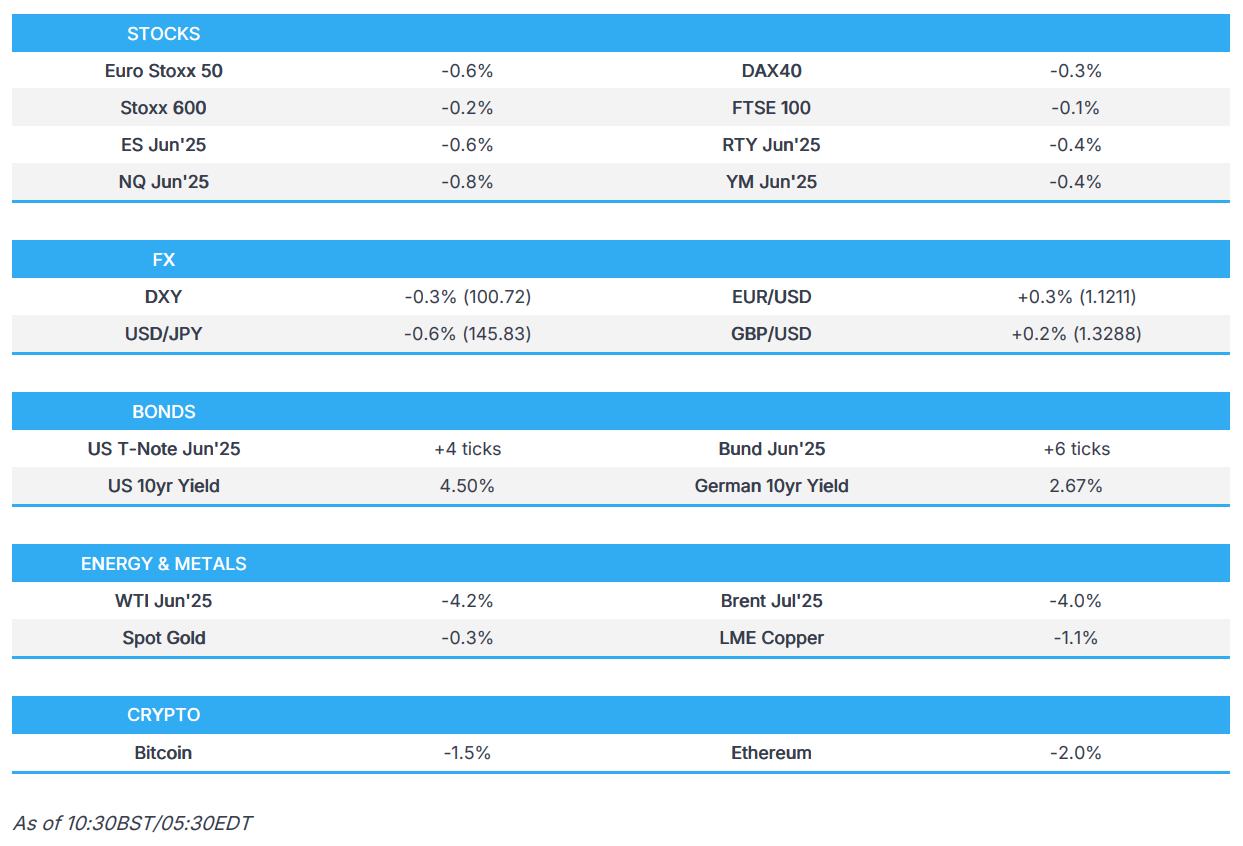

SNAPSHOT

TARIFFS/TRADE

- EU Trade Commissioner Sefcovic says the US and EU have agreed to intensify trade talk contacts.

- WTO chief warned that US bilateral tariff deals could put trade principles at risk and said global trade was in a crisis despite the recent de-escalation of the US-China tariff war, according to FT.

- US Treasury secretary Bessent says they can accomplish "a lot" over the next 90 days; will have a series of negotiations to prevent escalation with China again.

EUROPEAN TRADE

EQUITIES

- Subdued sentiment across Europe after the predominantly lower APAC handover, and following the mixed handover from Wall St, where the major indices were somewhat choppy and small caps underperformed as yields edged higher.

- Newsflow this morning has been light but earnings picked up, whilst current focus remains on geopolitical ongoings with US President Trump in the Middle East, consolatory language from Iran, and a likely no-show from Russia President Putin in Russia-Ukraine peace talks in Turkey.

- Sectors are mostly a defensive bias and in line with the cautious mood across the markets.

- US equity futures are also subdued as participants await the raft of US data including US NY Fed Manufacturing, Jobless Claims, Philly Fed Index, PPI, Retail Sales & Industrial Production, whilst markets also await commentary from Fed Chair Powell. Notable corporate earnings reports due today include: BABA, DE, WMT, AMAT, TTWO.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY subdued and contained within Wednesday's confines amid a lack of fresh catalysts overnight, n a 100.58-101.05 range at the time of writing, within yesterday's 100.27-101.14 parameter.

- EUR ekes mild gains and trades on either side of the 1.1200 level after recent fluctuations, and with ECB speakers scheduled later, although data and speakers today are not likely to shift the dial much.

- GBP is slightly firmer following better-than-expected UK GDP data; GBP/USD resides within yesterday's 1.3250-1.3360 range.

- USD/JPY retreated overnight as the underperformance in Japanese stocks spurred some haven flows into the yen.

- Antipodeans are subdued in-fitting with the broader risk tone; mild support was seen in AUD/USD following the stronger-than-expected employment data from Australia.

- PBoC set USD/CNY mid-point at 7.1963 vs exp. 7.2217 (Prev. 7.1956).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Another contained start for fixed income with USTs marginally in the green while peers across the pond resided slightly in the red in the early morning.

- USTs at a 109-26 peak with gains of a handful of ticks. While firmer, the benchmark remains markedly shy of peaks from the last three sessions at 110-09+, 110-15 and 110-19+ respectively.

- Bunds find themselves attempting to make a footing above the break-even mark at the top-end of a 129.13 to 129.47 band.

- Gilts gapped higher by 17 ticks, before then slipping to a shortlived 91.02 low given the readacross from EGBs at the time. Currently, at the mid-point of a 91.02-22 band.

- UK sells (via tender) GBP 2.0bln 0.125% 2028 Gilt: b/c 3.52x, average yield 3.768% & tail 0.7bps

- Click for a detailed summary

COMMODITIES

- WTI and Brent are suffering losses of USD 2/bbl, with commentary surrounding Iran applying steady pressure overnight and through the morning so far. US President Trump said the US is getting close to a deal with Iran, and they are in serious peace negotiations, adding that Iran has "sort of" agreed to the terms of a deal. This constructive commentary surrounding the nation pushed benchmarks to fresh session lows, adding to overnight losses. Losses overnight also stemmed from geopolitics, following a report that Iran is ready to sign an agreement with certain conditions in exchange for the lifting of sanctions and would commit to never making nuclear weapons and getting rid of its stockpiles of highly enriched uranium. The aforementioned lows for WTI and Brent are currently USD 60.65 and 63.63/bbl.

- Spot Gold is extending on recent losses with demand subdued as it sits below the USD 3,200/oz mark. The trend seen for most of this week remains intact, with the metal continuing to be hit by higher yields, particularly on the short end.

- Copper Futures are lower by a percent, mostly owing to a downbeat risk sentiment in APAC hours. It currently trades towards session lows of USD 9,467/t, after being modestly pressured around the time of Trump commentary.

- IEA lifts 2025 average oil demand growth forecast by 20k BPD to 740k BPD on upward revision to GDP growth forecast and lower oil prices; sees global oil demand growth dropping to 650k BPD for remainder of 2025, from 990k BPD in Q1. “Increased trade uncertainty is expected to weigh on the world economy and by extension oil demand,”. IEA sees oil inventories rising by around 720k BPD in 2025 as global supply rises expected to considerably outpace demand growth. IEA hikes 2025 global supply growth forecast to 1.6mln BPD, up by 380k BPD from previous month's report on higher Saudi production outlook. IEA raises 2026 average oil demand growth forecast to 760k BPD (prev forecast 690k BPD).

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (Mar) 0.2% vs. Exp. 0.0% (Prev. 0.5%); YY (Mar) 1.1% vs. Exp. 1.0% (Prev. 1.4%); 3M/3M (Mar) 0.7% vs. Exp. 0.6% (Prev. 0.6%)

- EU GDP Flash Estimate QQ (Q1) 0.3% vs. Exp. 0.4% (Prev. 0.4%)

- EU Industrial Production YY (Mar) 3.6% vs. Exp. 2.5% (Prev. 1.2%, Rev. 1.0%)

- EU Industrial Production MM (Mar) 2.6% vs. Exp. 1.8% (Prev. 1.1%)

- EU GDP Flash Estimate YY (Q1) 1.2% vs. Exp. 1.2% (Prev. 1.2%)

NOTABLE EUROPEAN HEADLINES

- Plans for a reset of UK-EU relations hit trouble due to fishing rights and youth mobility as EU member states demanded further concessions from the UK, according to the FT.

NOTABLE US HEADLINES

- Fed's Daly (2027 voter) said monetary policy is well-positioned and moderately restrictive, while she added businesses are cautious but are not stalling out and Fed policy can respond to whatever in the economy. Daly said patience is the word of the day and that uncertainty is not depressing activity but could affect the economy if it persists.

- US President Trump says they will upgrade the F-35 to an F-55; will do an F-22 super, an upgrade on the F-22.

GEOPOLITICS

- Russian Kremlin spokesperson Peskov says no chance Russian President Putin will take part in Turkey talks, according to Ria.

- "Israeli Chief of Staff: We will use all means to reach the perpetrators of the attack in the West Bank yesterday", according to Sky News Arabia.

MIDDLE EAST

- Qatar's PM said Israeli attacks in Gaza this week send a signal that they are not interested in negotiating a ceasefire, while he added that a US humanitarian plan for Gaza is not necessary and the UN should be allowed to deliver aid, according to CNN.

- Gaza Humanitarian Foundation announced it will launch operations in the Gaza Strip before the end of the month and stated that Israel has agreed to expand the number of distribution sites to serve the entire population of Gaza.

- US President Trump said Qatar is working with the US on negotiating an Iran deal and he wants to see Iran thrive.

- Iranian President Pezeshkian said Iran will not bow to any bullying from US President Trump who he suggested thinks that he can come to the region, chant slogans, and scare them.

- Iran is ready to sign an agreement with certain conditions in exchange for the lifting of sanctions and would commit to never making nuclear weapons, as well as getting rid of its stockpiles of highly enriched uranium, according to a top advisor to the Supreme Leader cited by NBC News.- US President Trump says the US getting close to doing a deal with Iran; in serious negotiations to achieve peace; don't want to take a second step and threaten Iran. Want to end Iran in an intelligent way, not destructive

RUSSIA-UKRAINE

- Russian President Putin was not on a list of negotiators the Kremlin published for talks with Ukraine in Istanbul on Thursday.

- US President Trump says he will go to the Russia-Ukraine talks if appropriate.

OTHER

- China's Hainan Maritime Safety Administration warned of military training taking place in an area of the South China Sea from May 15th to 16th and prohibited entry, while it noted there were some drills near Vietnam and China's Hainan.

- Russia sent a fighter jet to "check the situation" as Estonia was attempting to detain a Russian shadow fleet tanker, according to the Estonian Foreign Minister; jet violated NATO territory for "around a minute".

CRYPTO

- Bitcoin eventually dipped under USD 103k amid the ongoing cautious tone across the market.

- US Democrats are pushing for details on interactions between President Trump's administration and Binance CEO Zhao, via WSJ.

APAC TRADE

- APAC stocks were predominantly lower following the mixed handover from Wall St, where the major indices were somewhat choppy and small caps underperformed as yields edged higher.

- ASX 200 traded indecisively but eventually eked mild gains in the aftermath of the stronger-than-expected jobs data from Australia.

- Nikkei 225 underperformed following recent currency strength and as earnings results remained in the spotlight in Japan.

- Hang Seng and Shanghai Comp were lacklustre amid little in the way of fresh catalysts to spur momentum, while Tencent shares traded indecisively post-earnings and Alibaba results are scheduled for release today.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi hopes the Danish Chamber of Commerce in China and member companies will continue to role as a bridge between China and Denmark and between China and Europe, according to Xinhua.

- PBoC Governor Pan said China welcomes more outstanding Latin American market players to issue Panda bonds in China and share market development opportunities, while he added that China and Latin America should promote financial cooperation in a wider range of fields and a deeper level.

DATA RECAP

- Australian Employment (Apr) 89.0k vs. Exp. 20.0k (Prev. 32.2k)

- Australian Unemployment Rate (Apr) 4.1% vs. Exp. 4.1% (Prev. 4.1%)

- Australian Participation Rate (Apr) 67.1% vs. Exp. 66.8% (Prev. 66.8%)