Europe Market Open: EU & US futures flat with catalysts sparse; fixed benchmarks extend onto gains and DXY lower after data

16 May 2025, 06:40 by Newsquawk Desk

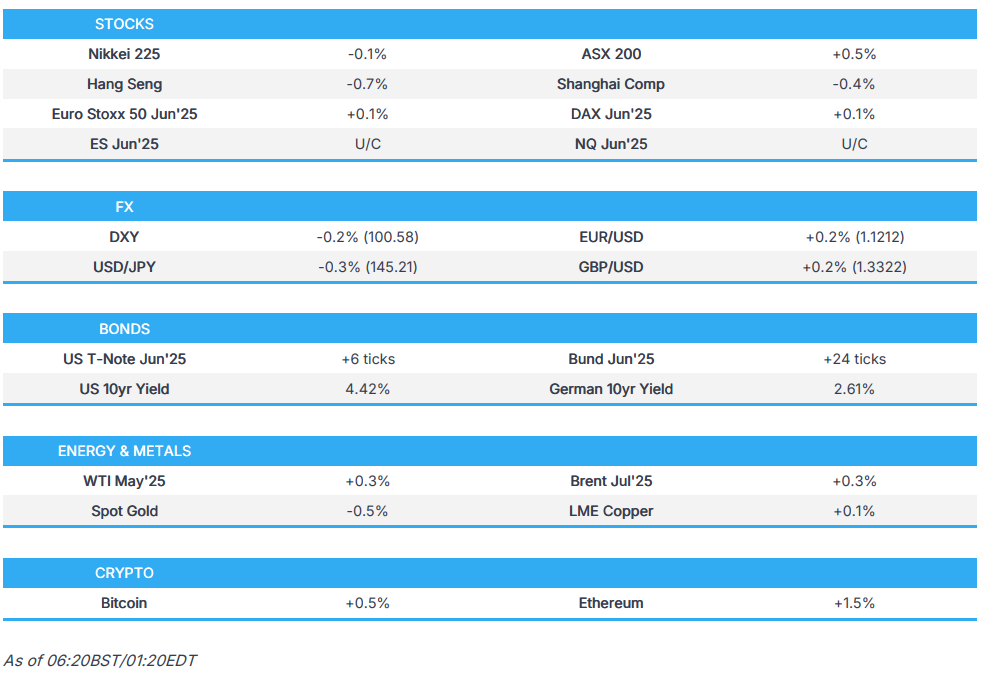

- Mixed APAC trade, US futures range bound while European futures point to a marginally firmer open.

- DXY remains lower after Thursday's data, EUR/USD marginally reclaimed 1.12, USD/JPY found support at 145.00.

- Fixed benchmarks extended/held on to recent gains.

- Crude benchmarks remain underpinned by the latest on US-Iran, metals marginally softer.

- Looking ahead, highlights include US Export/Import Prices, UoM Sentiment Survey, BoC SLOS, Speakers including ECB’s Lane, Cipollone & Fed’s Barkin.

- Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks finished mostly in the green after clawing back early losses, as participants reflected on a slew of data releases stateside including disappointing Retail Sales and softer-than-expected PPI data, which pressured yields and saw money markets return to fully pricing in two Fed rate cuts by year-end. Nonetheless, the other data releases were mixed as Initial Jobless Claims matched estimates and both Philly Fed and NY Fed surveys topped forecasts but remained in negative territory, while the major indices were predominantly higher aside from the Nasdaq as all Mag 7 names declined including Meta (META) which was further pressured in late trade as WSJ reported it had delayed the rollout of its flagship AI model, Behemoth.

- SPX +0.41% at 5,917, NDX +0.08% at 21,336, DJI +0.65% at 42,323, RUT +0.52% at 2,095.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump's administration is reportedly split on adding Chinese chip makers to export blacklists as some US officials fear the move could jeopardise trade talks with Beijing, while the Commerce Department has compiled a list of Chinese companies including memory chipmaker ChangXin Memory to add to the 'entity list' although the timing of the move has ben complicated by the recent agreement by China and the US to cut tariffs, according to sources cited by the FT.

- US President Trump’s administration targets Europe’s digital laws as a threat to basic rights and US business, according to WSJ. It was separately reported that the Trump administration told the EU it wants to discuss EU's agricultural food tariffs and non-tariff barriers in trade talks, while the US also wants to address economic security which is a term often used to refer to concerns about China's economic dominance in certain sectors and supply chains, alongside digital issues.

- US told Vietnam its trade deficit is unsustainable and a major concern amid tariff talks, according to Vietnam state media.

- Mexican President Sheinbaum spoke with Canadian PM Carney regarding the importance of USMCA in strengthening the competitiveness of the three North American countries, while they also discussed the continuity and strengthening of the seasonal agricultural worker program.

NOTABLE HEADLINES

- Fed's Barr (Vice Chair Supervision) said the US economy is on a solid footing with inflation heading to 2% although trade policies have clouded the outlook while he added the trade shock could be particularly hard on small businesses and trigger price increase if supply chains are affected or firms fail.

- US Deputy Treasury Secretary Faulkender said he is not concerned about persistent increases in prices, while he added that inflation will return to target levels and they are setting the foundation for the US economy to take off in H2.

- US House Budget Committee Chair Arrington may have enough 'No' votes to delay the tax/budget bill markup scheduled this Friday, according to Punchbowl.

- US House Speaker Johnson said they are very close to a SALT deal and remain on the path to pass the tax bill next week.

- Qatar wealth fund plans to invest USD 500bln in the US over the next 10 years, according to Bloomberg.

- Meta Platforms (META) is delaying the rollout of a flagship AI model, prompting internal concerns about the direction of its multibillion-dollar AI investments, according to WSJ.

APAC TRADE

EQUITIES

- APAC stocks traded mixed after the recent soft US data releases spurred Fed rate cut bets, while participants also digested weak data from Japan and earnings reports.

- ASX 200 was led by strength in miners and outperformance of gold producers after the recent rally in the precious metal.

- Nikkei 225 initially retreated amid recent currency strength and after GDP data for Q1 showed a steeper-than-expected contraction in Japan's economy, although the index gradually recovered and returned to flat territory as USD/JPY regained some composure and with the weak data effectively narrowing the scope for the BoJ to resume normalisation.

- Hang Seng and Shanghai Comp declined with sentiment dampened by earnings releases after Alibaba's results underwhelmed which pressured its Chinese blue-chip tech and ecommerce peers such as Tencent, Meituan and JD.com.

- US equity futures lacked direction and took a breather after ultimately climbing yesterday on Fed rate cut hopes.

- European equity futures indicate a slightly positive cash market open with Euro Stoxx 50 futures up 0.1% after the cash market closed with gains of 0.2% on Thursday.

FX

- DXY remained softer in the aftermath of the recent slew of data releases from the US including disappointing Retail Sales and softer-than-expected PPI data, which saw money markets revert to fully pricing two Fed rate cuts by year-end, while the latest comments from Fed officials including Powell provided very little to shift the dial.

- EUR/USD eked slight gains and tested the 1.1200 level but with the upside limited following the recent oscillations.

- GBP/USD remained afloat at the 1.3300 handle following the prior day's somewhat choppy mood as the underperformance in cyclical peers offset the data-related tailwinds.

- USD/JPY initially trickled lower amid initial haven flows into the yen and recent declines in US yields, but later bounced off support at the 145.00 level.

- Antipodeans nursed some of the losses from yesterday's underperformance but with the recovery limited by the mixed sentiment.

- PBoC set USD/CNY mid-point at 7.1938 vs exp. 7.2085 (Prev. 7.1963).

- Mexican Interest Rate (May) 8.5% vs. Exp. 8.5% (Prev. 9.0%) with the decision unanimous, while it estimates that it could continue calibrating the monetary policy stance and consider adjusting it in similar magnitudes.

FIXED INCOME

- 10yr UST futures extended on advances after catching a bid on the soft US PPI and downbeat Retail Sales data.

- Bund futures held on to the recent spoils following a resurgence to back above the 130.00 level.

- 10yr JGB futures tracked the gains in global peers with participants digesting weaker-than-expected Japanese GDP data.

COMMODITIES

- Crude futures struggled for direction after yesterday's two-way price action in which oil initially retreated on optimistic geopolitical-related commentary including from US President Trump who suggested the US was close to a nuclear deal with Iran. However, prices gradually rebounded off lows after comments from the Iranian side cast some doubts, as an official noted that they have not received any fresh US proposal to resolve outstanding issues in the nuclear dispute.

- Spot gold pulled back after the prior day's rally which was facilitated by soft data, lower yields and Fed rate cut bets.

- Copper futures mildly declined alongside the mixed risk appetite in the region and subdued mood in its largest buyer, China.

CRYPTO

- Bitcoin lacked conviction with price action choppy overnight on both sides of the USD 104,000 level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Board Member Nakamura said Japan's economy has recovered moderately, but some weakness has been seen, while he added the economy is facing mounting downward pressure due to the implementation of US tariff policies. Nakamura said the momentum for wage hikes has accelerated but could weaken depending on impact of US tariff policies and noted that it is appropriate to keep monetary policy steady for the time being. Furthermore, he said uncertainty over the economic outlook is heightening, so a cautious monetary policy approach is necessary and hiking rates prematurely when growth is slowing could curb consumption and capex.

- Japan's Economy Minister Akazawa said improvements in job and income conditions are likely to underpin moderate economic recovery, while he added must be mindful downside risk to the economy from US trade policy and the hit to consumption and household sentiment from sustained price rises also becoming a downside risk to Japan's economy.

DATA RECAP

- Japanese GDP QQ (Q1) -0.2% vs. Exp. -0.1% (Prev. 0.6%)

- Japanese GDP QQ Annualised (Q1) -0.7% vs. Exp. -0.2% (Prev. 2.2%, Rev. 2.4%)

- New Zealand 1yr Inflation Expectation (Q2) 2.4% (Prev. 2.2%)

- New Zealand 2yr Inflation Expectation (Q2) 2.3% (Prev. 2.1%)

GEOPOLITICS

MIDDLE EAST

- Israeli military said aerial defence systems were activated to intercept a missile launched from Yemen.

- There is concern in Israel over an emerging nuclear agreement between Iran and the US, while Israel's position is that Iran should not have enrichment abilities even for civilian use. Furthermore, there has been progress in the talks but no one knows for sure if it will end in an agreement, according to sources cited by The Jerusalem Post.

RUSSIA-UKRAINE

- Turkish Foreign Minister and US Secretary of State Rubio agreed during their meeting in Turkey that efforts for direct Ukraine-Russia talks would continue, according to Reuters citing a Turkish diplomatic source.

OTHER

- Pakistan’s PM said they want to give the message to India that they are ready to talk about peace.

EU/UK

NOTABLE HEADLINES

- EU leaders urged UK PM Starmer to improve mobility deal in last-ditch ‘reset’ talks, according to FT.

- World Economic Forum reportedly chasing ECB President Lagarde as its next leader after the WEF founder's abrupt exit, according to Bloomberg.