US Market Open: Stocks broadly firmer in stale morning trade; USD very modestly softer into data

16 May 2025, 10:50 by Newsquawk Desk

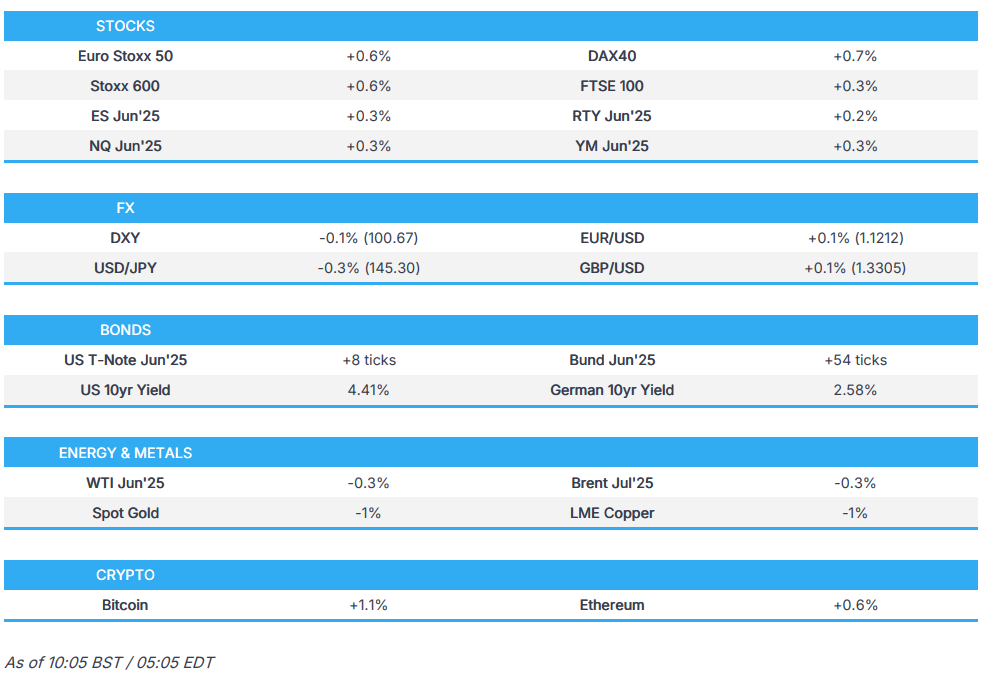

- Stocks are broadly in positive territory; US equity futures are modestly higher ES +0.3%.

- USD on the backfoot but only marginally so, EUR & GBP pivot 1.12 & 1.33 vs the USD.

- Bonds are firmer but are currently set to end a tumultuous week back where they started.

- Crude is awaiting geopolitical updates from numerous regions/conflicts, XAU dips.

- Looking ahead, US Export/Import Prices, UoM Sentiment Survey, BoC SLOS, Speakers including ECB’s Lane, Cipollone & Fed’s Barkin.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- US President Trump's administration is reportedly split on adding Chinese chip makers to export blacklists as some US officials fear the move could jeopardise trade talks with Beijing, while the Commerce Department has compiled a list of Chinese companies including memory chipmaker ChangXin Memory to add to the 'entity list' although the timing of the move has been complicated by the recent agreement by China and the US to cut tariffs, according to sources cited by the FT.

- US told Vietnam its trade deficit is unsustainable and a major concern amid tariff talks, according to Vietnam state media.

- Mexican President Sheinbaum spoke with Canadian PM Carney regarding the importance of USMCA in strengthening the competitiveness of the three North American countries, while they also discussed the continuity and strengthening of the seasonal agricultural worker program.

- Greenland's Foreign Minister has suggested that she wants to deepen bilateral ties with the EU, highlighting Greenland's mineral resources as an area for collaboration, via Politico.

- Japan has reportedly indicated that it is prepared to hold out for a better deal with the US, pushing for the full removal of the 25% duty on car imports, via FT.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.6%) opened modestly firmer across the board, and have traded with an upward bias this morning.

- European sectors hold a strong positive bias, with only a handful of industries in negative territory. Healthcare takes the top spot, with gains in the sector seemingly broad based. In terms of stock specific stories, Sanofi (+2.2%) gains after it received FDA orphan designation for treating sickle cell disease. Bayer (+3.5%) benefits from an FT report which suggested it is seeking a Roundup settlement.

- US equity futures are very modestly in positive territory, continuing a similar theme seen in the prior session. In terms of pre-market movers; Take-Two (-2.9%) dips after reporting in-line results, with more focus on USD 3.55bln impairment charges. Elsewhere, Applied Materials (-5.5%) slips after missing on rev. expectations due to uncertainty regarding export controls.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- Dollar is on the backfoot, continuing the pressure seen following Thursday’s disappointing Retail Sales and softer-than-expected PPI data. As a reminder, this led money markets to fully price in two Fed cuts by year-end; currently pricing in roughly 57bps. DXY currently sits in a 100.52-78 range. Further downside for the index will see a potential test of the week’s trough at 100.27 – should that be taken out, 100.00 will be next in focus. Ahead, US Import Prices, UoM Survey and commentary from Fed's Barkin.

- EUR is modestly firmer vs the Dollar, with specific for the Bloc very light today – Final Italian inflation metrics were revised marginally lower but ultimately had little impact on the Single-Currency. Commentary via ECB’s Kazaks and Villeroy this morning has not added too much to the agenda; the former reiterated the need for a meeting-by-meeting approach and highlighted the uncertainty around trade. This morning EUR has climbed back above the 1.12 mark and has traded in a busy 1.1182-1.1219 range.

- JPY is slightly firmer vs the Dollar after choppy price action overnight, which saw USD/JPY initially trickle lower amid initial haven flows into the yen and recent declines in US yields, but later bounced off support at the 145.00 level. USD/JPY was little moved following weaker-than-expected GDP data. USD/JPY currently trading around 145.30 in a 144.93-145.68 range

- GBP is flat/incrementally firmer vs the Dollar and holds just above the 1.33 mark, in a very thin 1.3300-1.3320 range. UK-specific updates have been lacking today. Some focus has been on an FT article which suggested that EU leaders are urging UK PM Starmer to improve the region’s mobility deal – particularly for EU students.

- Antipodeans are the best performers vs the Dollar, nursing some of the losses seen in the prior session. The Kiwi is the best G10 performer today; overnight, New Zealand 1yr and 2yr inflation expectations are both seen higher, which may explain some of the outperformance in today’s session. Do note that the NZD is outmuscling the AUD in the AUD/NZD cross; some traders may be focused on next week’s RBA meeting, where markets widely expect the Bank to deliver a 25bps cut.

- PBoC set USD/CNY mid-point at 7.1938 vs exp. 7.2085 (Prev. 7.1963).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Firmer start to the day as USTs continue the data-induced upside from Thursday with newsflow since a little light and markets largely awaiting updates on numerous geopolitical situations. At the top-end of a 110-10 to 110-20 band. As it stands, on track to end the week almost flat, opened the week at 110-18, despite the marked pressure seen in the first half on US-China progress. Trade developments that sparked notable hawkish action Monday through Wednesday, before being offset by Thursday’s data deluge. Ahead, the docket is comparably light but does feature Building Permits/Housing Starts, Import Prices (factor into PCE) and the prelim. Uni. of Michigan series for May.

- Bunds are in-fitting with USTs, but with action slightly more pronounced as EGBs experienced a marginal rally early doors as European players entered the fray and reacted to the bullish bias of APAC trade. Specifics light. A few ECB officials on the wire but nothing that has fundamentally shifted the narrative. Bunds just off highs in a 130.11-50 confine and, as with USTs, near-enough on track to end the week flat despite a WTD range in excess of 135 ticks.

- Gilts are outperforming slightly, likely on account of the marginal underperformance vs Bunds seen at points this week and as such, the UK is catching up on the final session of the week. As above, Gilts are also set to end the week essentially unchanged, currently just off highs in a 91.84-92.00 band. Resistance at 92.59 from mid-April and thereafter 93.00 before highs from the last few weeks, beginning at 93.59.

- Click for a detailed summary

COMMODITIES

- A hesitant start for WTI and Brent as geopolitics dominates ahead of the weekend. WTI and Brent traded largely flat through the morning but are currently down by around USD 0.10/bbl, nearing overnight lows.

- In terms of Iran-related headlines, crude prices whipsawed on conflicting media reports yesterday and mixed signals from US and Iranian officials. This morning, Iran's Foreign Minister stated that negotiations will continue as long as the other party remains engaged, maintaining that no formal proposal from the US has been received.

- On Russia-Ukraine, talks are underway in Istanbul, with the Trilateral meeting between Turkey-US-Ukraine supposedly concluded. We are yet to hear the readout from it. Ahead, there will be another trilateral meeting, this time with Russia taking the place of the US.

- Spot gold is continuing losses, pulling back from yesterday’s gains after soft data, lower yields and Fed rate cut bets aided the yellow metal. At the time of writing, the yellow metal trades towards the upper end of a USD 3,205.49-3,252.17/oz range.

- Base metals are softer after the subdued mood in its largest buyer, China, overshadows the positive sentiment in Europe this morning. 3M LME Copper currently rests within, but at the lower-end of, a USD 9,474.9-9,591.42/t range.

- Shanghai Copper warehouse stocks +27.44k/T (prev. -8.60k/T), Aluminium stocks -13.59k/T (prev. -6.19k/T)

- ADNOC Chief says the UAE and the US plan investment of USD 440bln in the energy sector through 2035.

- Click for a detailed summary

NOTABLE DATA RECAP

- Italian CPI (EU Norm) Final YY (Apr) 2.0% vs. Exp. 2.1% (Prev. 2.1%); Consumer Prices Final YY (Apr) 1.9% vs. Exp. 2.0% (Prev. 2.0%); Consumer Prices Final MM (Apr) 0.1% vs. Exp. 0.2% (Prev. 0.2%); CPI (EU Norm) Final MM (Apr) 0.4% vs. Exp. 0.5% (Prev. 0.5%)

- Italian Trade Balance EU (Mar) -2.453B EU (Prev. -0.361B EU); Global Trade Balance (Mar) 3.657B EU (Prev. 4.466B EU)

- EU Eurostat Trade NSA, Eur (Mar) 36.8B EU (Prev. 24.0B EU)

NOTABLE EUROPEAN HEADLINES

- ECB's Villeroy says "we are not currently in a currency wars situation but rather a trade war situation".

- ECB's Kazaks says a meeting by meeting approach at the ECB is right and notes a lot of uncertainty around trade measures, according to CNBC.

NOTABLE US HEADLINES

- US Deputy Treasury Secretary Faulkender said he is not concerned about persistent increases in prices, while he added that inflation will return to target levels and they are setting the foundation for the US economy to take off in H2.

- US President Trump says deals from his trip are worth USD 12-13tln, includes deals already announced and some that will be outlined "very shortly". Will be sending out letters to nations for trade deals soon.

- BofA card spending, week to May 10th: -1.3% (1.0% April average), spending has seen a recovery from the Easter slowdown.

CRYPTO

- Bitcoin is on a slightly firmer footing and holds just above USD 103k.

GEOPOLITICS

- US President Trump says he is willing to meet with Ukrainian President Zelensky and Russian President Putin as soon as arrangements can be made; going to take care of Gaza; will make good progress on geopolitical situations in the next two or three weeks In one way or another, will take care of Iran.

- Iranian Foreign Minister says the nation's position is clear and we are ready to build confidence and adopt transparency in our Nuclear Programme in exchange for the lift of sanctions. Not received any agreement proposal from the US; is possible will be informed via a meditator

- Hamas is reportedly holding direct negotiations with the US Administration, according to a senior Hamas official cited by Al Arabiya.

APAC TRADE

- APAC stocks traded mixed after the recent soft US data releases spurred Fed rate cut bets, while participants also digested weak data from Japan and earnings reports.

- ASX 200 was led by strength in miners and outperformance of gold producers after the recent rally in the precious metal.

- Nikkei 225 initially retreated amid recent currency strength and after GDP data for Q1 showed a steeper-than-expected contraction in Japan's economy, although the index gradually recovered and returned to flat territory as USD/JPY regained some composure and with the weak data effectively narrowing the scope for the BoJ to resume normalisation.

- Hang Seng and Shanghai Comp declined with sentiment dampened by earnings releases after Alibaba's results underwhelmed which pressured its Chinese blue-chip tech and ecommerce peers such as Tencent, Meituan and JD.com.

NOTABLE ASIA-PAC HEADLINES

- BoJ Board Member Nakamura said Japan's economy has recovered moderately, but some weakness has been seen, while he added the economy is facing mounting downward pressure due to the implementation of US tariff policies. Nakamura said the momentum for wage hikes has accelerated but could weaken depending on impact of US tariff policies and noted that it is appropriate to keep monetary policy steady for the time being. Furthermore, he said uncertainty over the economic outlook is heightening, so a cautious monetary policy approach is necessary and hiking rates prematurely when growth is slowing could curb consumption and capex.

- Japan's Economy Minister Akazawa said improvements in job and income conditions are likely to underpin moderate economic recovery, while he added must be mindful downside risk to the economy from US trade policy and the hit to consumption and household sentiment from sustained price rises also becoming a downside risk to Japan's economy.

DATA RECAP

- Japanese GDP QQ (Q1) -0.2% vs. Exp. -0.1% (Prev. 0.6%)

- Japanese GDP QQ Annualised (Q1) -0.7% vs. Exp. -0.2% (Prev. 2.2%, Rev. 2.4%)

- New Zealand 1yr Inflation Expectation (Q2) 2.4% (Prev. 2.2%)

- New Zealand 2yr Inflation Expectation (Q2) 2.3% (Prev. 2.1%)