US Market Open: Stocks at highs, NQ +1.7% & DXY gains; reports suggest EU to focus on critical sectors in bid to avoid US tariffs

27 May 2025, 11:10 by Newsquawk Desk

- The EU set to focus on critical sectors in a bid to avoid US tariffs, according to Bloomberg sources.

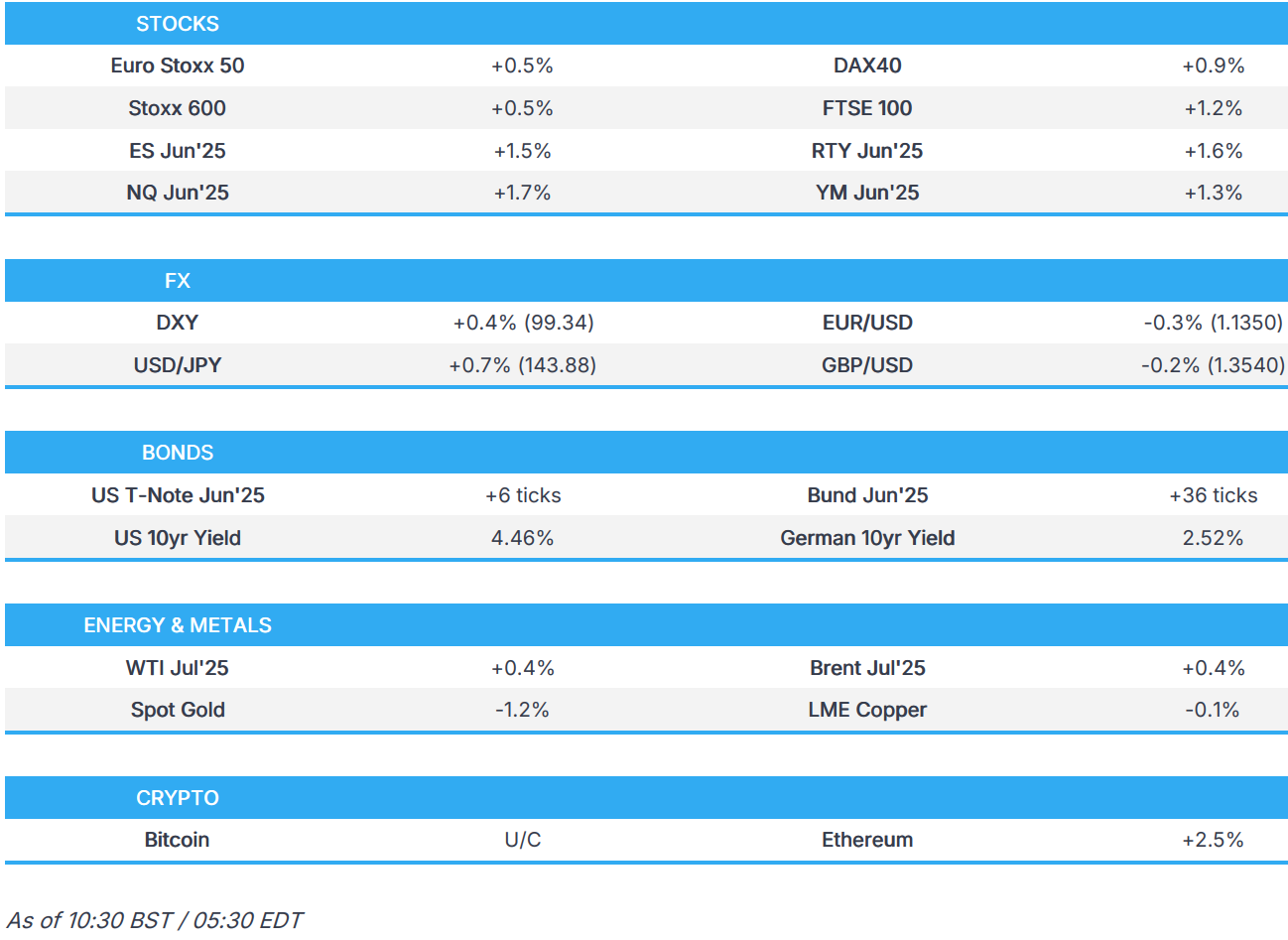

- Stocks in the green and generally at session highs; NQ +1.7%.

- USD attempts to atone for recent losses, JPY weighed on by a pullback in domestic yields.

- Bonds bid and yields slump on MOF sources, Gilts outperform on this & reports that the UK will be shifting to shorter-term borrowing in order to lower its interest bill.

- Crude uneventful ahead of OPEC+ whilst precious and base metals slip.

- Looking ahead, US Durable Goods & Consumer Confidence, NBH Policy Announcement, Supply from the US, Earnings from AutoZone.

TARIFFS/TRADE

- EU set to focus on critical sectors in a bid to avoid US tariffs, according to Bloomberg sources, EU Trade commissioner Sefcovic will lead political negotiations on industries such as steel and aluminium, autos, pharma, semiconductors and aircraft. Talks will happen in parallel with technical discussions on tariffs and non-tariff barriers

- European Industry Association sent a survey to firms on behalf of the European Commission requesting details on US investment plans, according to Reuters sources.

- European Trade Commissioner Sefcovic said he had a good call with US Commerce Secretary Lutnick on Monday and that the European Commission remains fully committed to constructive and focused efforts at pace towards an EU-US deal, while he added that they continue to stay in constant contact.

- South Africa offered to import LNG from the US for 10 years as part of the deal proposed to Washington which would include the US investing in gas infrastructure and cooperating on technology and fracking, according to a ministerial statement.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) opened incrementally firmer, but sentiment improved in tandem with a pick-up in US equity futures. Indices currently reside at session highs.

- European sectors hold a strong positive bias, with only a handful of industries residing in the red. Financials take the top spot, joined closely by Travel & Leisure and then Industrials. The latter buoyed by continued strength in Defence names, following Trump’s hawkish remarks on Putin following Russia’s large-scale attack on Ukraine over the weekend.

- US equity futures (ES +1.5% NQ +1.7% RTY +1.3%) are entirely in the green as US traders return from holiday. Price action this morning has really only been upwards, with contracts generally near session highs.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is attempting to recover recent losses after printing a fresh MTD trough on Monday at 98.69. There hasn't been a clear driver for the price action with fresh macro drivers out of the US on the light side. Focus remains on the trade front with FBN's Gasparino noting yesterday that a framework between the US and India is close to being announced; this could offer some reprieve. Elsewhere, remarks from Fed 2026 voter Kashkari stated that he finds arguments against looking through tariff-induced inflation as compelling. For today's docket, the notable highlights are Durable Goods and Consumer Confidence metrics.

- EUR/USD is on the backfoot and has returned to a 1.13 handle as the USD attempts to atone for recent losses. Focus remains on the trade front after US President Trump's decision over the weekend to announce a delay to the 50% tariff deadline on EU goods to July 9th. The latest reporting via Bloomberg states that the EU is set to focus on critical sectors in a bid to avoid US tariffs; key industries include steel, aluminium, autos, pharma, semiconductors and aircraft. On the data slate, French CPI metrics came in softer-than-expected ahead of next week's EZ-wide release. EUR/USD has delved as low as 1.1338 with little in the way of support until the 1.13 mark.

- USD/JPY initially retreated amid a softer dollar and the subdued risk appetite in Japan. There were also comments from BoJ Governor Ueda who stated that, to an extent, incoming data allows them to gain more confidence in the baseline scenario and that as economic activity and prices improve, they will adjust the degree of monetary easing as needed. Nonetheless, the pair eventually clawed back losses as the dollar rebounded off lows and as long-term JGB yields declined in response to source reporting via Reuters that Japan's MoF will consider tweaking the composition of its bond issuance plan.

- GBP on the backfoot vs. the USD but to a lesser extent than most peers. Cable is currently snapping its recent strong showing which saw it hit a multi-year peak on Monday at 1.3593. Fresh macro drivers for the UK are lacking as participants return from the long weekend.

- After a strong showing in early European trade on Monday on account of the positive risk tone, both are on the backfoot as the USD picks up steam. NZD/USD hit a fresh YTD high yesterday at 0.6031 before returning to a 0.59 handle.

- PBoC set USD/CNY mid-point at 7.1876 vs exp. 7.1842 (Prev. 7.1833)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs were initially weighed on by BoJ’s Ueda reiterating hiking plans. Action which, pushed JGBs to a 139.08 low overnight. Thereafter, the benchmark rallied on supply related sources to a 139.49 peak. Japan’s MOF is to consider tweaking its bond issuance composition, via Reuters citing sources. A tweak that could include the trimming of super long-term debt.

- The above has carried into US trade. Lifting USTs by 10 ticks at best to a 110-13 high. Yields lower across the US curve but, unsurprisingly, given the long-dated focus to the MOF reporting that area is leading the move down, sparking bull-flattening. Fed’s Kashkari stuck to the data-dependent approach that has characterised his commentary in recent days and weeks. Focus ahead now on US Durable Goods and Consumer Confidence due before a 2yr Note auction.

- Bunds were already subject to an upward bias given the JGB action, a bias which was extended on by a cooler-than-expected set of French preliminary inflation, a series that was sufficient to lift Bunds above the 131.00 mark. Further support stemmed from ECB’s Villeroy, who outlined that interest rate normalisation within the bloc is unlikely to have concluded. This added to the above bias and lifted Bunds to a 131.22 peak, where the benchmark remains. German paper was little moved by EZ Sentiment data were more-or-less in-line.

- Gilts are bolstered in sympathy with JGBs, and with two UK-specific factors also influencing. Firstly, the FT reports that the UK will be shifting to shorter-term borrowing in order to lower its interest bill amid elevated longer-dated yields which are pressuring the fiscal situation. Secondly, The Telegraph citing NIESR reports that Chancellor Reeves is “being forced towards” a tax raid of as much as GBP 30bln, due to increasing borrowing costs and benefit payments. Altogether, these factors caused Gilts to gap higher by 47 ticks (gapping from Friday’s close, owing to Monday’s Bank Holiday) and then extend another 43 to a 91.89 peak.

- Saudi Aramco mandates USD 5, 10 and 30yr benchmarks, according to IFR. IPTs (vs USTs): 5yr +115bps, 10yr +130bps, 30yr +18bps.

- Italy sells EUR 2.75bln vs exp. 2.5-2.75bln 2.55% 2027 BTP Short Term & EUR 2.0bln vs exp. EUR 1.5-2bln 1.80% 2036 & 1.25% 2032 BTPei

- Click for a detailed summary

COMMODITIES

- Crude price action has been uneventful and choppy within recent ranges in the run-up to the OPEC event on May 31st. WTI currently resides in a USD 61.08-62.14/bbl intraday range with its Brent counterpart in USD 64.36-64.98/bbl confines.

- Precious metals are posting losses in European hours, with early pressure seen as Shanghai commodities trade got underway, particularly for the yellow metal, amid several factors including 1) USD strength, caused in part (in more recent trade) by EUR losses after softer French Prelim CPI, 2) Unwinding of some risk premium as UK and US traders react to US delaying the EU tariffs, 3) technical factors with the yellow metal dipping under overnight support (USD 3,325/oz), yesterday's low (3,323.50/oz) and eventually, but briefly, the USD 3,300/oz.

- Base metals are subdued, and are sidelining the positive sentiment across equities, with the LME back up and running after the long weekend, whilst prices are pressured by the strengthening USD, irrespective of the constructive US-EU trade news from over the weekend. 3M LME copper remains above USD 9,500/t with a current intraday parameter between USD 9,561.95-9,640.00/t.

- The meeting of eight OPEC+ countries was brought forward to May 31st from June 1st, according to Reuters sources.

- Russian Deputy PM Novak said nothing has been discussed yet in response to a question about whether OPEC+ has discussed an oil output increase by another 411k bpd from July, and stated that OPEC+ will discuss the current market conditions and forecast, as well as make some adjustments if needed. Furthermore, Novak said the possible G7/EU tightening of Russia’s oil price cap is not acceptable and stated that price caps have not affected Russia’s oil exports, according to RIA.

- Ecuador's biggest oil refinery experienced a fire and halted operations as a precaution following the fire.

- Petrobras (PBR) CEO said if oil prices drop further, they will cut diesel, gasoline, and jet fuel prices, while he added that fuel prices are at a 'comfortable level' and that gasoline and diesel prices are below parity at the moment.

- China Steel Association said China is working to control steel capacity to resolve the mismatch between supply and demand.

- Ukraine has approved the gas transportation mechanism via the Transbalkan pipeline from Greece, awaiting approval from other corresponding nations.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Selling Price Expec (May) 7.9 (Prev. 11.0, Rev. 10.6); Cons Infl Expec (May) 23.6 (Prev. 29.6, Rev. 29.4); Services Sentiment (May) 1.5 vs. Exp. 1.0 (Prev. 1.4, Rev. 1.6); Consumer Confid. Final (May) -15.2 vs. Exp. -15.2 (Prev. -15.2); Industrial Sentiment (May) -10.3 vs. Exp. -10.5 (Prev. -11.2); Economic Sentiment (May) 94.8 vs. Exp. 94.0 (Prev. 93.6)

- French CPI (EU Norm) Prelim MM (May) -0.2% vs. Exp. 0.1% (Prev. 0.7%); CPI Prelim YY NSA (May) 0.7% vs. Exp. 0.9% (Prev. 0.8%); CPI Prelim MM NSA (May) -0.1% vs. Exp. 0.1% (Prev. 0.6%); CPI (EU Norm) Prelim YY (May) 0.6% vs. Exp. 0.9% (Prev. 0.9%)

- UK BRC Shop Price Index YY (May) -0.1% (Prev. -0.1%)

- German GfK Consumer Sentiment (Jun) -19.9 vs. Exp. -19.8 (Prev. -20.6, Rev. -20.8)

- Swiss Trade (Apr) 6.358B CH (Prev. 6.350B CH, Rev. 6.290B); Swiss Watch Exports +18.2% (vs +1.5% Y/Y in March)

- Swedish Overall Sentiment (May) 93.6 (Prev. 94.8)

NOTABLE EUROPEAN HEADLINES

- UK government will spend a record GBP 3bln to boost training opportunities as part of a broader strategy to train locals to fill gaps in the labour market and reduce reliance on migrant workers.

- UK Chancellor Reeves is "being forced towards" a tax raid of up to GBP 30bln by benefit giveaways and her struggle with increasing borrowing costs, according to The Telegraph, citing the NIESR.

- UK government is shifting to shorter term borrowing to lower its interest bill as a global debt sell-off adds to the pressure on its tax and spending plans, according to FT.

- ECB's Villeroy says interest rate normalisation within the EZ is probably incomplete.

- German Chamber of Commerce (DIHK) expects inflation at 2.1% in 2025 (vs 2.2% in 2024); German economy expected to contract by 0.3% in 2025 (vs prev. forecast of -0.5%); exports are expected to decline by 2.5% in 2025.

- French PM Bayrou says will unveil budget-cutting proposals in early July, according to BFM TV.

- EU Ministers approve the EUR 150bln Euro arms fund to give loans for defence projects, says Polish European Affairs Minister.

NOTABLE US HEADLINES

- Fed's Kashkari (2026 voter) says there is a healthy debate amongst FOMC member over whether to "look through" the inflationary impact of new tariffs. Personally finds arguments against looking through tariff-induced inflation more compelling. These arguments support the Fed's stance of keeping rates on hold until there is more clarity on the path for tariffs and their effects.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said on Monday regarding hostage deal negotiations that he hopes they will have news regarding the hostages today or tomorrow.

RUSSIA-UKRAINE

- Russia's Kremlin says work on Russia-US POW swap continues; on reports of possible US sanctions, says it is aimed at wrecking Ukraine peace talks. Ukrainian attacks on Russia do not facilitate peace process.

- US President Trump is said to be eyeing sanctions against Moscow this week as he grows frustrated by Russian President Putin’s continued attacks on Ukraine and the slow pace of peace talks, according to people familiar with Trump’s thinking cited by WSJ.

- Western allies of Ukraine, including the UK and US have agreed to lift all range restrictions on weapons in Ukraine, according to The Times.

- Ukrainian President Zelensky said Russian mass attacks are Russian President Putin’s political choice and that Putin is playing with diplomacy, while he added that more pressure and sanctions must be applied on Russia.

- Authorities in Ukraine’s Sumy region said Russian forces captured several villages in the region.

OTHER

- Guangzhou public security authorities said a technology company in China's Guangzhou was attacked by a foreign hacker organisation and the initial investigation found that the cyberattack was by a hacker organisation 'supported by' Taiwan's DPP authorities.

CRYPTO

- Bitcoin is essentially flat and trading just shy of USD 110k; Ethereum moves a little higher and sits just above USD 2.6k.

- Trump Media & Technology (DJT) plans to raise USD 3bln to spend on cryptocurrencies, according to FT.

APAC TRADE

- APAC stocks traded mixed with price action relatively rangebound amid a lack of major fresh catalysts and in the absence of a lead from Wall St owing to Memorial Day.

- ASX 200 edged marginally higher as strength in tech, energy and financials atoned for the underperformance in the mining and resources sectors.

- Nikkei 225 was subdued amid a firmer currency and after BoJ Governor Ueda reiterated the central bank's policy normalisation rhetoric, although the downside was stemmed following a lack of deviation in Services PPI data, which matched the prior reading, and as long-end JGB yields declined.

- Hang Seng and Shanghai Comp were lacklustre with price action in Hong Kong choppy and with the mainland constrained as focus turned to earnings releases and despite a slight acceleration in Chinese Industrial Profits, while a firm PBoC liquidity operation also failed to inspire.

NOTABLE ASIA-PAC HEADLINES

- Chinese Premier Li said China and Cambodia are to jointly respond to external uncertainties, according to Xinhua.

- China's Mofcom summoned industry associations and automakers such as BYD (1211 HK) and Dongfeng Motor (489 HK) to a meeting on Tuesday afternoon and intends to discuss matters including the emergence of used cars on the market that have never been driven.

- BoJ Governor Ueda said while many of his G7 colleagues looked relieved by the progress made in the fight against inflation, they also acknowledged new challenges such as heightened trade policy uncertainty and dealing with more frequent supply side shocks, while he added they are still grappling in Japan with the challenge of achieving the 2% inflation target in a sustainable manner and are now closer to the inflation target than any time during the last few decades, but are not quite there. Furthermore, he said to an extent, incoming data allows them to gain more confidence in their baseline scenario, and as economic activity and prices improve, they will adjust the degree of monetary easing as needed to ensure achievement of sustainable 2% inflation target.

- Japan Ministry of Finance will consider tweaking the composition of its bond issuance plan that could involve trimming issuance of super long debt, according to sources cited by Reuters.

DATA RECAP

- Chinese Industrial Profits YY (Apr) 3.0% (Prev. 2.6%); YTD (Apr) 1.4% (Prev. 0.8%)