Europe Market Open: Risk-on following NVIDIA beat & court tariff ruling

29 May 2025, 07:00 by Newsquawk Desk

- APAC stocks were mostly higher with sentiment underpinned following NVIDIA's earnings and after the Manhattan-based Court of International Trade blocked President Trump's Liberation Day tariffs.

- NVIDIA (NVDA) shares rose 4.9% after hours following earnings which beat on top and bottom lines despite incurring a USD 4.5bln charge in Q1; Q2 revenue outlook 45.0bln (exp. 46.4bln).

- US President Trump ordered US chip designers to stop selling to China, according to FT; US halts exporting aircraft engine technology and chip software to China, according to NYT.

- FOMC Minutes stated participants agreed they were well positioned to wait for more clarity on the outlook.

- European equity futures indicate a higher cash market open with Euro Stoxx 50 futures up 1.4% after the cash market closed with losses of 0.7% on Wednesday.

- Looking ahead, highlights include Spanish Retail Sales, Italian Industrial Sales, US GDP 2nd Estimate (Q1), Core PCE Prices (Q1), Jobless Claims, SARB Policy Announcement, Swiss & Scandinavian Holiday, Speakers including Fed’s Barkin, Goolsbee, Kugler & Daly, BoE's Bailey & Breeden, Supply from Italy & US Earnings from Marvell, Costco, Dell, Gap, ULTA, Foot Locker, Best Buy & Kohl's.

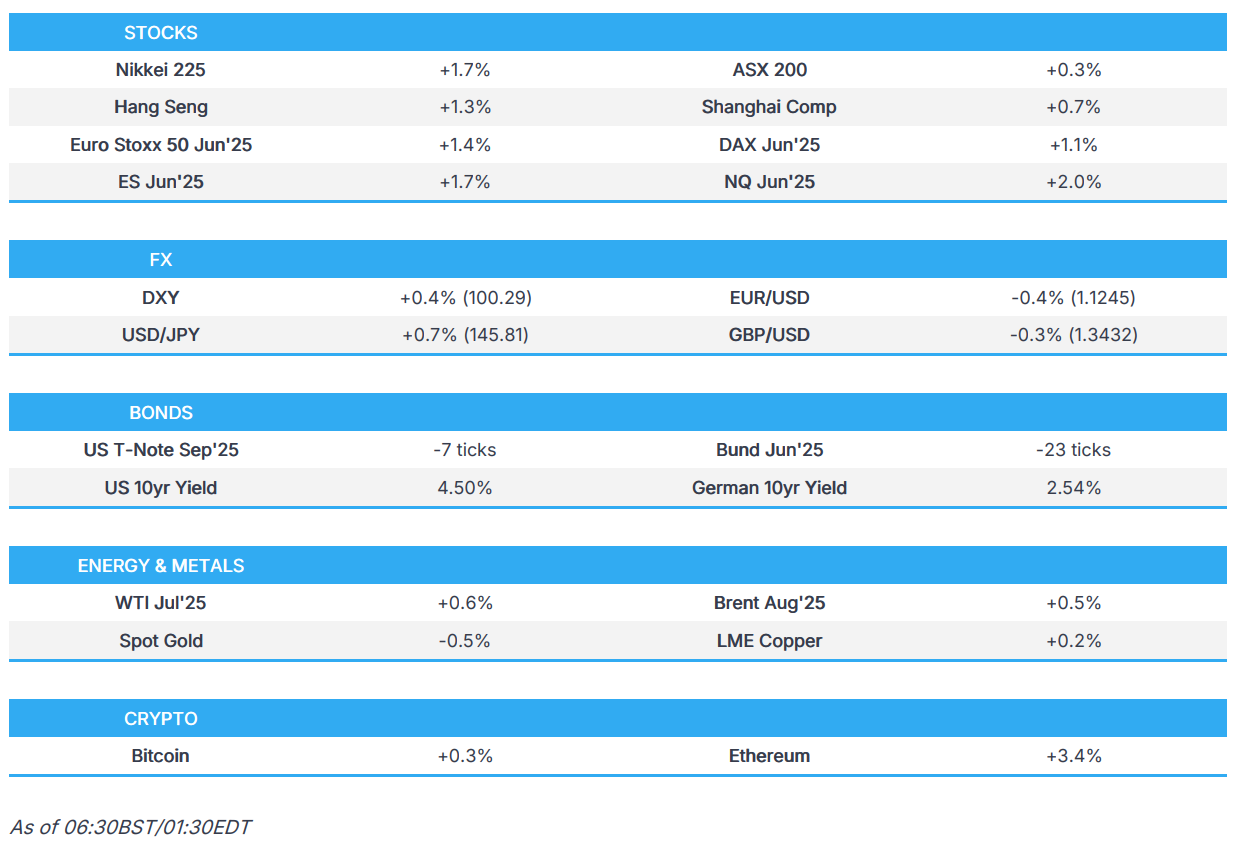

SNAPSHOT

US TRADE

EQUITIES

- US stocks were mildly pressured and the major indices all finished lower to give back some of this week's gains, while there were some headwinds from US-China frictions with pressure seen in the likes of Cadence Systems and Synopsys after it was reported that US President Trump ordered US chip designers to stop selling to China, while a US Commerce spokesperson said the US is reviewing exports of strategic significance to China and has suspended some export license while review takes place.

- Nonetheless, futures pared some of the losses after-hours following NVIDIA's earnings which beat on top and bottom lines despite incurring a USD 4.5bln charge in Q1.

- NVIDIA (NVDA) Q1 2026 (USD): Adj. EPS 0.96 (exp. 0.92), Revenue 44.1bln (exp. 43.28bln); Q2 revenue 45.0bln (exp. 46.4bln). Shares rose 4.9% after-market.

- SPX -0.56% at 5,889, NDX -0.45% at 21,318, DJI -0.58% at 42,099, RUT -1.08% at 2,068.

- Click here for a detailed summary.

FOMC MINUTES

- FOMC Minutes stated participants agreed they were well positioned to wait for more clarity on the outlook and these participants noted that a durable shift in such correlations or a diminution of the perceived safe-haven status of US assets could have lasting implications for the economy. Participants saw uncertainty about their economic outlooks as unusually elevated and noted they may face difficult trade-offs if inflation proved more persistent while outlooks for growth and employment weakened.

- Furthermore, almost all participants commented on the risk that inflation could prove more persistent than expected and participants agreed that uncertainty about the outlook had increased and it was appropriate to take a cautious approach to monetary policy.

TARIFFS/TRADE

- Manhattan-based Court of International Trade blocked President Trump's Liberation Day tariffs in a ruling related to a case brought on behalf of five small businesses that import goods from other countries. It was also reported that US President Trump's administration filed an appeal following the ruling by the Court of International Trade and the White House stated it is not for unelected judges to decide how to properly address a national emergency.

- Goldman Sachs noted that the ruling on Liberation Day tariffs gives the administration 10 days to halt tariff collection but does not affect sectoral tariffs and the admin can impose across-the-board tariff and country-specific tariffs under other legal authorities.

- US President Trump ordered US chip designers to stop selling to China, according to FT. Trump administration told US companies that offer software used to design semiconductors to stop selling their services to Chinese groups, in the latest attempt to make it harder for China to develop advanced chips. Several people familiar with the move said the Commerce Department told Electronic Design Automation groups, which include Cadence, Synopsys and Siemens EDA, to stop supplying their technology to China and in some cases, the Commerce Department has suspended existing export licenses or imposed additional license requirements while the review is pending.

- US Secretary of State Rubio said the US will begin revoking visas of Chinese students, including those with connections to the Chinese Communist Party or studying in critical fields and it will also revise visa criteria to enhance scrutiny of all future visa applications from the People's Republic of China and Hong Kong.

- US Commerce Department spokesperson said the US is reviewing exports of strategic significance to China and has suspended some export licenses while the review takes place.

- US halts exporting aircraft engine technology and chip software to China, according to NYT.

- UK is seeking to accelerate the implementation of trade deals with the US when Business Secretary Reynolds meets with US Commerce Secretary Lutnick next week, according to FT.

NOTABLE HEADLINES

- NY Fed said it will start morning standing repo facility operations on June 26th with offerings to take place between 08:15-08:30ET and will maintain afternoon standing repo facility offerings.

- White House plans to send a small package of DOGE spending cuts to Congress next week, according to Politico.

- Elon Musk said his scheduled time as a special government employee is coming to an end, while a White House official said Elon Musk leaving the administration is accurate and his off-boarding would begin on Wednesday night.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher with sentiment underpinned following NVIDIA's earnings and after the Manhattan-based Court of International Trade blocked President Trump's Liberation Day tariffs and deemed that the sweeping tariffs under the emergency powers law were unlawful. However, the Trump administration has since filed an appeal and has other tools it could apply to maintain such tariffs.

- ASX 200 was led higher by outperformance in energy, telecoms and tech although gains were capped with miners, real estate and defensives at the other end of the spectrum.

- Nikkei 225 outperformed and climbed back above the 38,000 level following the recent currency weakness and blow to Trump's tariff agenda.

- Hang Seng and Shanghai Comp conformed to the constructive mood although US-China frictions lingered after the Trump administration ordered US chip designers to stop selling to China and US Secretary of State Rubio announced to ‘aggressively’ revoke visas of Chinese students.

- US equity futures gained with Nasdaq futures front-running the advances after NVIDIA reported better-than-expected earnings and with sentiment also lifted by the latest tariff-related developments.

- European equity futures indicate a higher cash market open with Euro Stoxx 50 futures up 1.4% after the cash market closed with losses of 0.7% on Wednesday.

FX

- DXY extended on recent gains and climbed back above the 100.00 level as the dollar was gradually lifted following news that the Manhattan-based Court of International Trade blocked President Trump's Liberation Day tariffs, although the Trump administration has filed an appeal against the ruling. Conversely, US-China frictions lingered after the Trump administration ordered US chip designers to stop selling to China and US Secretary of State Rubio announced to ‘aggressively’ revoke visas of Chinese students, while there was a lack of fireworks from the FOMC Minutes which reinforced the wait-and-see message and noted that staff cited tariff policies as implying a larger drag on activity than policies they had assumed in their prior forecast.

- EUR/USD gave way to the firmer buck and slipped further beneath the 1.1300 handle with tariff developments in the spotlight, while participants also await trade talks with EU Trade Commissioner Sefcovic to speak with US Commerce Secretary Lutnick and USTR Greer on Thursday and then on every other day.

- GBP/USD remained lacklustre in the absence of any major fresh catalysts for the UK and ahead of comments from BoE's Bailey and Breeden.

- USD/JPY continued its recent advances and briefly reclaimed the 146.00 handle owing to the firmer buck and haven currency outflows.

- Antipodeans traded somewhat mixed in which AUD/USD was rangebound and largely unaffected by the private capex data, while NZD/USD gradually pared the gains from the recent hawkish RBNZ rate cut with the currency not helped by weaker NAB Business Confidence survey.

- PBoC set USD/CNY mid-point at 7.1907 vs exp. 7.2023 (Prev. 7.1894).

FIXED INCOME

- 10yr UST futures briefly dipped beneath the 110.00 level as risk sentiment was supported following the US court ruling on Trump's tariffs, while FOMC minutes were also recently in the spotlight but proved to be a damp squib.

- Bund futures gapped lower after hitting resistance at the 131.00 level and amid haven outflows.

- 10yr JGB futures clawed back opening losses and eked mild gains despite the lack of catalysts but follows the recent Japanese yield volatility.

COMMODITIES

- Crude futures remained firmer after gaining throughout the prior US session where there was a lack of fresh developments from the OPEC+ meeting with markets focused on the Saturday meeting between the eight members conducting voluntary cuts. Nonetheless, there was further upside overnight with prices underpinned after private inventory data showed a surprise drawdown in headline crude stockpiles and as sentiment was underpinned by reports that a US federal court deemed US President Trump's Liberation Day tariffs were unlawful.

- US Private Inventory Data (bbls): Crude -4.2mln (exp. +0.1mln), Distillate +1.3mln (exp. +0.5mln), Gasoline -0.5mln (exp. -0.5mln), Cushing -0.3mln.

- Iraqi Oil Minister urged commitment to agreements reached in the OPEC+ meeting and affirmed that unity of stance is crucial for the stability of oil markets, according to a statement.

- Kuwaiti Oil Minister affirmed support for efforts for the stability of global oil markets, according to the state news agency.

- Libya's eastern-based government may announce a force majeure on oil fields and ports citing repeated assaults on the National Oil Corporation.

- Spot gold trickled lower as the dollar strengthened and havens were shunned after the US trade court's tariff ruling.

- Copper futures rebounded off this week's trough amid the positive risk appetite but with the upside capped as US-China frictions lingered.

CRYPTO

- Bitcoin was ultimately flat after oscillating back and forth of the USD 108k level.

NOTABLE ASIA-PAC HEADLINES

- BoK cut the 7-day Repo Rate by 25bps to 2.50%, as expected, with the decision made unanimously. BoK said it will maintain its rate cut stance to mitigate downside risks to economic growth and will adjust the timing and pace of any further base rate cuts, while it is to closely monitor changes in domestic and external policy environments. The central bank also stated that South Korean exports are seen continuing to slow down and that a high degree of uncertainty in the trade environment is a risk to growth. Furthermore, BoK Governor Rhee said they see bigger room for further cuts given the downside risks to growth and noted that four board members saw room for further cuts for the next three months.

DATA RECAP

- Australian Capital Expenditure (Q1) -0.1% vs. Exp. 0.5% (Prev. -0.2%)

- Australian Private Capital Expenditure for 2024-25 (AUD)(Estimate 6) 187.6B (Prev. 183.4B)

- Australian Private Capital Expenditure for 2025-26 (AUD)(Estimate 2) 155.9B (Prev. 148.0B)

- New Zealand ANZ Business Outlook (May) 36.6% (Prev. 49.3%)

- New Zealand ANZ Own Activity (May) 34.8% (Prev. 47.7%)

GEOPOLITICS

MIDDLE EAST

- US President Trump said they are having good Iran talks and warned Israeli PM Netanyahu against Iran action which he said is not appropriate. Furthermore, he wants to go into Iran with inspectors and said Iran wants to make a deal, while he noted a deal could happen over the next few weeks and he told Netanyahu that they are close to a solution.

- Iran may agree to pause nuclear enrichment work temporarily if the US recognises Tehran's right to enrich Uranium for civilian uses, while any temporary halt to nuclear activity under a "political agreement" would also require the US to release frozen Iranian funds, according to Reuters citing sources. However, it was later reported that Tehran denied a Reuters report of halting uranium enrichment for a year and said the continuation of enrichment in Iran is a non-negotiable principle, according to Iran International.

RUSSIA-UKRAINE

- US President Trump said "can't tell you if Putin wants to end the war" and will find out soon, while he added that they will respond differently if Putin is playing them and it will take about a week to find out. Trump also stated he is disappointed in what happened in Ukraine and will sit down with Zelensky and Putin if necessary.

- Ukraine's Defence Minister said he handed over the Ukrainian version of the memorandum to the head of the Russian delegation and Russia continues to delay the delivery of their version, while Ukraine is not opposed to further meetings but waits for a memorandum from the Russian side.

- Russian Foreign Minister Lavrov proposed that the next round of Russia-Ukraine talks take place on June 2nd in Istanbul, according to Interfax. It was separately reported that Lavrov informed US Secretary of State Rubio of the preparation of concrete proposals to resolve the Ukrainian conflict, while Lavrov told Rubio of the proposed new round of talks between Russia and Ukraine.

EU/UK

NOTABLE HEADLINES

- ECB's Knot said near-term growth and inflation risks are to the downside, while the medium-term inflation outlook is more ambiguous.

- ECB's Villeroy said he does not see inflation picking up in Europe.