Europe Market Open: Positive APAC session capped by disappointing Caixin PMI, Eurostoxx +0.1%, ahead of EZ inflation data

03 Jun 2025, 06:45 by Newsquawk Desk

- APAC stocks traded mostly higher as the region took impetus from the rebound on Wall St; gains capped by disappointing Chinese Caixin Manufacturing data.

- US President Trump's administration wants countries' "best offer" by Wednesday in tariff talks, according to Reuters.

- White House Press Secretary said US President Trump and Chinese President Xi will likely talk this week.

- European equity futures indicate a slightly positive cash market open with Euro Stoxx 50 futures up 0.1% after the cash market closed with losses of 0.2% on Monday.

- DXY is a touch higher after yesterday's session of losses, EUR/USD remains on a 1.14 handle, antipodeans lag.

- Looking ahead, highlights include Swiss CPI, EZ HICP, Unemployment Rate, US Durable Goods, JOLTS Job Openings, RCM/TIPP Economic Optimism, Fed’s Goolsbee, Logan & Cook, ECB's Lagarde, BoE's Bailey, Breeden, Dhingra & Mann, Supply from UK & Germany.

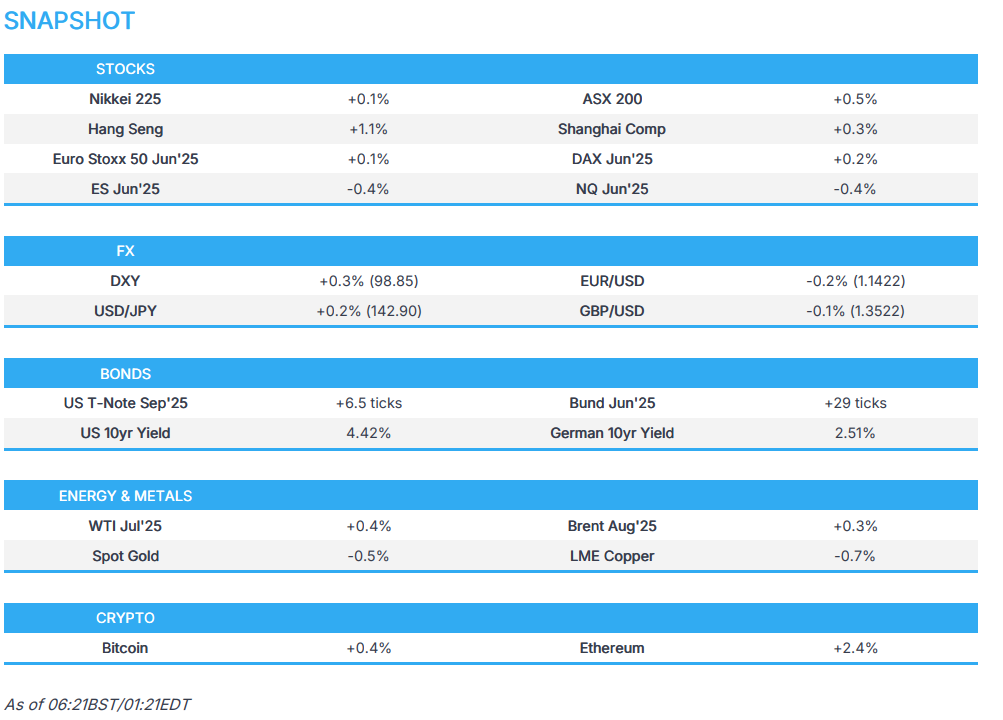

SNAPSHOT

US TRADE

EQUITIES

- US stocks ultimately closed the session in the green with the Nasdaq leading the gains as outperformance in the tech sector kept indices bid once cash equity trade was underway, while energy stocks were also supported following the OPEC+ 8 decision and geopolitical escalation over the weekend including Ukraine's strike on Russian bombers with drones well inside of Russia and Iran dismissed the US proposal for a nuclear deal as "unrealistic".

- SPX +0.41% at 5,936, NDX +0.71% at 21,492, DJI +0.08% at 42,305, RUT +0.19% at 2,070.

- Click here for a detailed summary.

TARIFFS/TRADE

- US reportedly extends the tariff pause on some Chinese goods to August 31st, according to Bloomberg.

- US President Trump's administration wants countries' "best offer" by Wednesday in tariff talks, according to Reuters citing a draft of the request.

- US President Trump posted "If other Countries are allowed to use Tariffs against us, and we’re not allowed to counter them, quickly and nimbly, with Tariffs against them, our Country doesn’t have, even a small chance, of Economic survival."

- US President Trump posts on Truth "Because of Tariffs, our Economy is BOOMING!"

- White House Press Secretary said US President Trump and Chinese President Xi will likely talk this week, while she also commented that the EU came to the table due to President Trump's tariff threat.

- UK Trade Minister Reynolds will meet USTR Greer on Tuesday to discuss the implementation of a trade deal that has been complicated by the announcement of fresh US tariffs on steel, according to Reuters.

- China's Chamber of Commerce to the EU expressed disappointment and serious concerns about the EU's move to limit Chinese enterprises' participation in the healthcare sector.

- India and Europe are said to have agreed on almost half of trade deal talk chapters, according to FT.

- Japan's trade negotiator Akazawa said they are aiming to have cabinet discussions towards a US trade deal and are seeking to accelerate talks ahead of the mid-June G7 talks.

NOTABLE HEADLINES

- Fed's Goolsbee (2025 voter) said so far they've had excellent inflation reports and surprisingly little direct impact of tariffs and don't know if that will remain true in the next 1-2 months. Furthermore, he said he is a little gun-shy about arguing that tariffs will have a transitory effect on inflation and noted that the recent PCE inflation print may have been the 'last vestige' of pre-tariff impact.

- US President Trump posted on "Passing THE ONE, BIG, BEAUTIFUL BILL is a Historic Opportunity to turn our Country around after four disastrous years under Joe Biden. We will take a massive step to balancing our Budget by enacting the largest mandatory Spending Cut, EVER, and Americans will get to keep more of their money with the largest Tax Cut, EVER, and no longer taxing Tips, Overtime, or Social Security for Seniors".

APAC TRADE

EQUITIES

- APAC stocks traded mostly higher as the region took impetus from the rebound on Wall St but with gains capped following disappointing Chinese Caixin Manufacturing data and as trade uncertainty lingered.

- ASX 200 edged higher amid strength in mining stocks but with further upside limited as defensives lagged and after mixed data releases including a surprise contraction in net exports contribution to GDP.

- Nikkei 225 kept afloat but lacked firm conviction after recent currency fluctuations and after a deluge of comments from BoJ Governor Ueda who reiterated they will continue to raise interest rates if the economy and prices move in line with forecasts, but also noted there was no preset plan for rate hikes and that they will raise interest rates only if the economy and prices turn up again and outlooks are likely to be realised.

- Hang Seng and Shanghai Comp were underpinned after the US reportedly extended the tariff pause on some Chinese goods to August 31st, while the White House Press Secretary stated that US President Trump and Chinese President Xi will likely talk this week, although the upside was restricted in the mainland given the lack of confirmation by Beijing regarding Trump-Xi talks and as participants also digested disappointing Caixin Manufacturing PMI data which showed its first contraction in eight months and printed its weakest since September 2022.

- US equity futures (ES -0.4%, NQ -0.3%) mildly retreated following yesterday's rebound and amid the ongoing tumultuous trade-related environment.

- European equity futures indicate a slightly positive cash market open with Euro Stoxx 50 futures up 0.1% after the cash market closed with losses of 0.2% on Monday.

FX

- DXY regained some composure after the prior day's selling pressure which was spurred by soft data and ongoing trade uncertainty following recent punchy US-China rhetoric, although there have been some more amicable reports with the US extending exemptions from Section 301 tariffs for some Chinese goods including Covid-related and solar manufacturing products, while the White House Press Secretary stated that President Trump and Chinese President Xi will likely talk this week, although the Chinese side have yet to confirm or acknowledge this.

- EUR/USD faded some of yesterday's gains but remained at the 1.1400 territory after having benefitted on Monday from the dollar's demise, while participants also look ahead to Eurozone HICP data and Unemployment Rate scheduled for today, as well as the ECB meeting later in the week.

- GBP/USD pulled back from recent highs with price action largely influenced by the moves in the greenback and as the latest comments from BoE's Mann provided little to shift the dial, while UK Trade Minister Reynolds is set to meet with USTR Greer on Tuesday to discuss the implementation of a trade deal that has been complicated by the announcement of fresh US tariffs on steel.

- USD/JPY reclaimed the 143.00 handle amid the recovery in the dollar, the mostly positive risk appetite and a slew of comments from BoJ Governor Ueda.

- Antipodeans retreated after mixed data releases from both sides of the Tasman and as the RBA Minutes noted that the Board considered keeping rates unchanged and cutting by 25bps or 50bps, but decided the case for a 25bps cut was the stronger one and preferred for policy to be cautious and predictable.

- PBoC set USD/CNY mid-point at 7.1869 vs exp. 7.1872 (Prev. 7.1848).

FIXED INCOME

- 10yr UST futures gradually edged higher following the recent choppy performance amid trade uncertainty and soft US data, while participants now look ahead to more data releases stateside and several Fed speakers.

- Bund futures continued to edge higher after yesterday's whipsawing and with a Schatz auction scheduled later today.

- 10yr JGB futures were initially subdued with little reaction seen to a slew of comments from BoJ Governor Ueda although prices were later supported following stronger demand at the latest 10yr JGB auction which resulted in the highest bid-to-cover in more than a year.

COMMODITIES

- Crude futures remained afloat amid the mostly positive risk environment and the current geopolitical backdrop with Iran dismissing the US proposal for a nuclear deal as "unrealistic".

- Spot gold pulled back as the dollar rebounded and after yesterday's rally stalled shy of the USD 3,400/oz level.

- Copper futures retreated despite the return to market of its largest buyer with prices not helped by the disappointing Chinese Caixin Manufacturing PMI data.

CRYPTO

- Bitcoin ultimately declined but saw two-way price action on both sides of the USD 106k level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Governor Ueda said Japan's economy is modestly recovering despite some weakness seen, corporate profits are improving and business sentiment is solid, but noted the slowdown in the overseas economy pressures corporate profits and the pace of economic growth is expected to slow down. Ueda reiterated that they will continue to raise interest rates if the economy and prices move in line with forecasts and they will conduct monetary policy appropriately depending on price, and economic developments to achieve the 2% target in a stable and sustainable manner. However, he noted it is important to make judgments without any preset ideas and that they said in the Outlook Report that the baseline scenario could change significantly, as well as stated there is no preset plan for rate hikes and they will raise interest rates only if the economy and prices turn up again and outlooks are likely to be realised. Furthermore, Ueda said they will review bond taper plans at the next policy meeting taking into account the opinions of bond market participants and he is aware of the market view that some investors' appetite for super-long JGBs has declined.

- RBA Minutes from the May meeting stated the Board considered keeping rates unchanged and cutting by 25bps or 50bps but decided the case for a 25bps cut was the stronger one and preferred policy to be cautious and predictable. RBA said inflation is still not at the mid-point of the target band and the labour market is still tight, while the Board agreed developments in the domestic economy alone warranted a rate cut and progress on inflation meant policy did not need to be as restrictive. Furthermore, it was stated that a larger move might offer more insurance against adverse global scenarios although the Board was not persuaded that 50bps was needed and US tariffs had not yet affected the Australian economy, while it would be challenging for businesses and households if aggressive easing had to be reversed and the Board judged it was not yet time to move monetary policy to an expansionary setting.

DATA RECAP

- Chinese Caixin Manufacturing PMI Final (May) 48.3 vs. Exp. 50.6 (Prev. 50.4)

- Australian Current Account Balance (AUD)(Q1) -14.7B vs. Exp. -13.1B (Prev. -12.5B)

- Australian Net Exports Contribution (Q1) -0.1% vs Exp. 0.0% (Prev. 0.2%)

- Australian Business Inventories (Q1) 0.8% vs. Exp. 0.1% (Prev. 0.1%)

- Australian Gross Company Profits (Q1) -0.5% vs. Exp. 1.3% (Prev. 5.9%)

GEOPOLITICS

MIDDLE EAST

- US President Trump posted on Truth Social "The AUTOPEN should have stopped Iran a long time ago from “enriching.” Under our potential Agreement — WE WILL NOT ALLOW ANY ENRICHMENT OF URANIUM!"

- US nuclear deal offer allows Iran to enrich uranium at low levels and doesn't include full dismantlement of the nuclear facilities, according to Axios. However, it was separately reported that an Iranian official said the US proposal is unrealistic, according to CNN.

- US State Department said Secretary of State Rubio spoke with Saudi's Foreign Minister and discussed Ukraine and Russia talks, stabilisation in Syria and the situation in Gaza.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Ukraine and Russia agreed to exchange 1000 military servicemen each and there could be an additional swap of 200 each, while Ukraine and Russia are to exchange lists for the POW exchange this week.

- Ukrainian President Zelenskiy's Chief of Staff said Russia is doing everything possible to continue the war and urges new sanctions now.

- Russia sees the beginning of a complete withdrawal of Ukrainian troops from Russian territory, including Donetsk, Luhansk, Zaporizhzhia and Kherson regions, as one of the options for establishing a ceasefire, according to Interfax citing the memorandum. The first part of the Russian memorandum envisages the lifting of all existing and the rejection of new economic sanctions and restrictive measures between Russia and Ukraine, while Russia proposes recognition of Crimea, Luhansk, Donetsk, Zaporizhzhia, and Kherson regions as part of Russia and complete withdrawal of Ukrainian military units from these territories.

- Russian-controlled parts of Zaporizhzhia in Ukraine lost power as a result of Ukraine's attacks although the power cut-off had not affected the Zaporizhzhia nuclear power plant, according to Russian agencies.

EU/UK

NOTABLE HEADLINES

- BoE's Mann said must consider interactions of QT and rate decisions, while she added that the BoE cannot exactly offset high long-term rates caused by QT by cutting the bank rate further and extra cuts to short rates to compensate for QT could run counter to the need to purge structural rigidities in the UK labour and product markets. Furthermore, she expects these issues will be part of MPC considerations before the September QT decision.