US Market Open: Sentiment improves as US refrains from any Middle-East involvement, FOMC ahead

18 Jun 2025, 11:20 by Newsquawk Desk

- Firing between Israel and Iran continued overnight. Iran used a hypersonic missile, while no attacks were seen from the US. Risk recovered and oil waned off highs.

- US officials signalled that the next 24 to 48 hours would be critical in determining whether a diplomatic solution with Iran is possible -- or if the president might resort to military action instead, according to ABC.

- European bourses tread water amid geopolitical updates and the looming FOMC rate decision; US equity futures are modestly higher.

- USD gives back some of Tuesday’s gains; Antipodeans lead whilst the CHF underperforms.

- Gilts initially pressured after CPI. More recently, modest bid into the green awaiting rhetoric from Iran’s Supreme Leader.

- Crude softer as traders await updates from the US; XAU also on the backfoot.

- Looking ahead, US Building Permits, Housing Starts, Jobless Claims, Fed & BCB Policy Announcements, speakers include ECB’s Nagel, Elderson, Lane, de Guindos, BoC’s Macklem; Fed Chair Powell.

TRADE/TARIFFS

- Mexican President Sheinbaum said she had a very good phone conversation with US President Trump; they agreed to work together to reach an agreement on diverse topics that worry them, according to Reuters.

- White House said US President Trump will sign an additional executive order this week to keep TikTok running; the extension will last 90 days.

- South Korea and the US are to hold the third round of trade talks next week, according to Maeil.

- Japanese PM Ishiba agreed with US President Trump to continue ministerial-level tariff talks; Ishiba said Japan will continue to work intensely to achieve a trade deal with the US.

EUROPEAN TRADE

EQUITIES

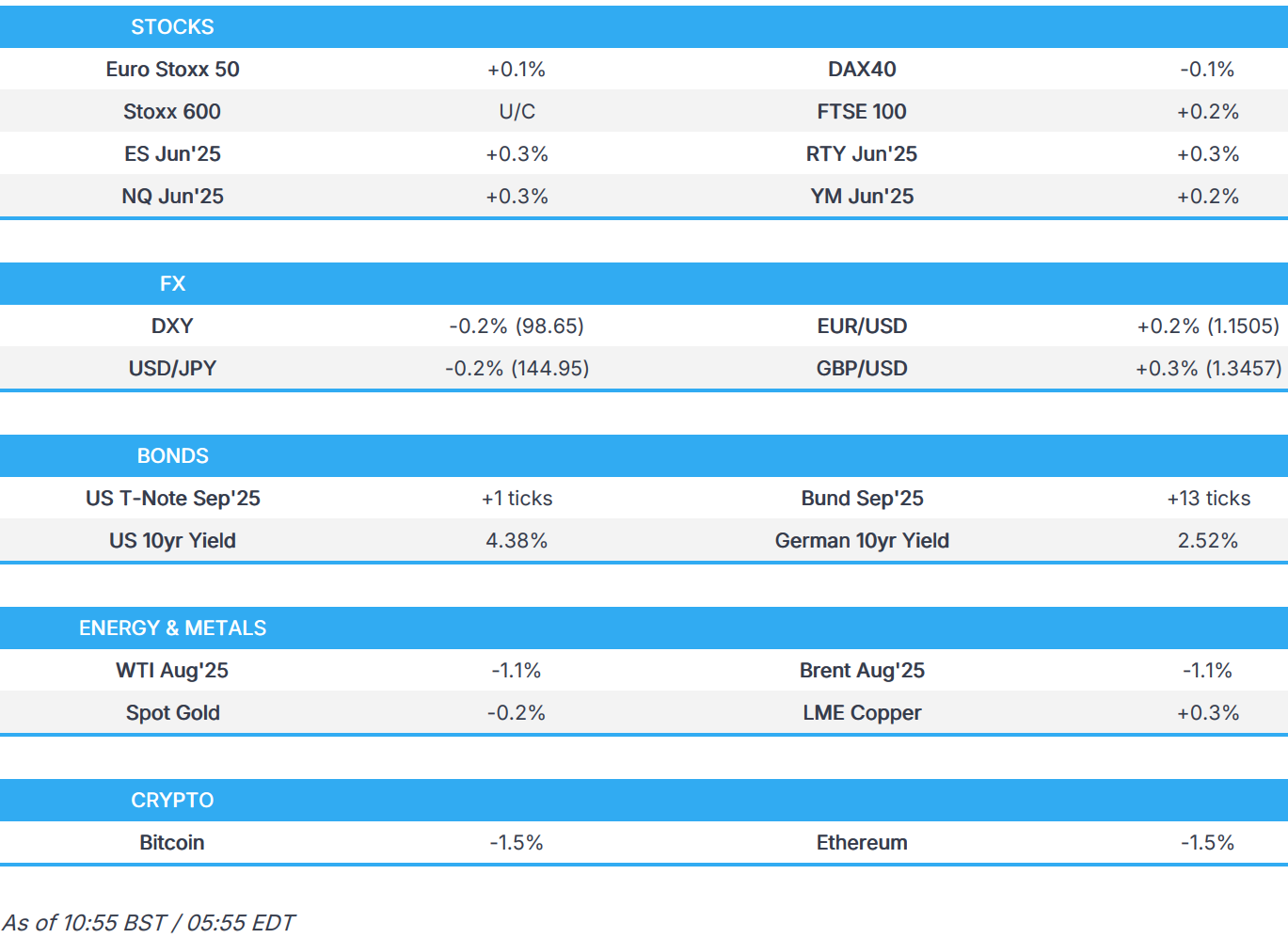

- European bourses (STOXX 600 U/C) opened mixed on either side of the unchanged mark, before grinding ever so slightly higher as the morning progressed. More recently, however, indices have waned off best levels to now show a mixed picture in Europe.

- European sectors are mixed, in-fitting with the indecisive risk tone seen so far. Utilities takes the top spot, followed closely by Real Estate and then Insurance to complete the top three, whilst Healthcare lags.

- US equity futures (ES +0.3% NQ +0.3% RTY +0.3%) are incrementally firmer today, attempting to stabilise from the losses seen in the prior session. Gains are ultimately capped given the uncertain environment in the Middle East and ahead of the FOMC Policy Announcement.

- Barclays has introduced a 2026 Stoxx 600 year-end target of 620 (vs. current level of 542; implies 14.4% upside).

- Boeing (BA) 787's emergency-power system was likely active before the Air India crash, according to WSJ; investigators to probe if engines failed during take off.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has given back some of Tuesday's geopolitically-induced gains, given the lack of updates out of the region this morning. More focus on the FOMC announcement later with officials set to stand pat on policy given the highly uncertain economic outlook. There is a chance that the 2025 FFR dot may be tweaked to show just 25bps of loosening this year vs. the prior forecast of 50bps (it would only take two forecasters adjusting their call to shift the median view). DXY has delved as low as 98.50, comfortably above Tuesday's trough at 98.02.

- Incremental macro drivers for the Eurozone remain on the light side. Tuesday's better-than-expected outturn for German ZEW - adding to the recent run of encouraging Eurozone data - failed to have a durable impact on the EUR, with the pair dictated more by price action in the broader USD. Docket today has included a few ECB speakers (reiterated the Bank's meeting-by-meeting approach) and EZ HICP Finals (unrevised). EUR/USD briefly matched Tuesday's low at 1.1474 but has since reclaimed its footing on a 1.15 handle.

- JPY is firmer vs. the USD but to a lesser degree than peers on account of the recent upside in energy prices (Japan is a notable net importer of crude) and a lack of progress on the trade front. These effects appear to have limited JPY's role as a safe-haven on Tuesday. USD/JPY briefly eclipsed yesterday's high at 145.38, topping out at 145.44 before returning to levels closer to 145.

- GBP firmer vs. the broadly weaker USD and flat vs. the EUR. Little sustained follow-through has been seen following the latest UK inflation metrics which matched Refinitiv expectations but was a touch above Bloomberg's; the Services figures came in shy of expectations. The release saw incremental upside in the GBP but ultimately failed to sustain. GBP/USD is currently towards the bottom end of Tuesday's 1.3415-1.3592 range.

- Antipodeans are both attempting to claw back some of Tuesday's risk-induced losses as high-beta FX tracks the recovery in sentiment after geopolitical updates quietened down overnight and the US has (for now) refrained from joining Israel's attack on Iran. From a macro perspective, focus this week will be on NZ Q1 GDP metrics on Wednesday and Australian labour market data on Thursday.

- SEK is net weaker vs. the EUR following the Riksbank's decision to cut rates by 25bps and provide a rate path forecast which "entails some probability of another rate cut in 2025".

- PBoC set USD/CNY mid-point at 7.1761 vs exp. 7.2027 (prev. 7.1746)

- Chilean Central Bank maintains benchmark interest rate at 5.00%, as expected, with the decision unanimous.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs were exhibiting a modest bearish bias throughout the morning, given the improvement in the risk tone seen as the US is yet to get directly involved in the Iran-Israel conflict. However, this has been limited in nature with USTs only lower by at most 4+ ticks, and now has now edged just above the unchanged mark as broader peers rise. The upside seemingly stemming from a bit of a haven bid, amid reports that the Iranian Supreme leader is to speak shortly, via ISNA. The docket today is headlined by the FOMC, but before that May’s Building Permits/Housing Starts and Weekly Claims are due; latter expected at 245k (prev. 248k).

- Bunds spent most of the morning in the red, but have flicked into positive territory in recent trade. German paper was moving higher into a 2054 & 2046 Bund auction, and then took another leg higher given its strong demand. Holding towards the upper-end of a 130.58-92 band. The low for the session printed alongside the UK CPI release (see Gilts), though the move in Bunds proved short lived and the benchmark quickly climbed back towards unchanged levels. Overall, the benchmark is in a holding pattern into the FOMC (see USTs) and updates on the geopolitical and/or trade fronts.

- Gilts opened lower by a handful of ticks and then slipped to a 92.48 low with downside of 20 ticks on the session. A bearish open that was driven by the lead from fixed peers, as the risk tone continues to recover, and following the digestion of UK data. In brief, CPI came in broadly unchanged from the prior in May, given the offsetting influences of air fares, fuel costs and food prices. Pertinently for the BoE, the services metrics were cooler than forecast and markedly so M/M. After the initial move lower, Gilts are now higher by 11 ticks, in-fitting with peers.

- Germany sells EUR 1.408bln vs exp. EUR 1.5bln 2.50% 2054 and sells EUR 0.988bln vs. exp. EUR 1.0bln 2.50% 2046 Bund

- Click for a detailed summary

COMMODITIES

- Crude futures are in the red, after a tentative overnight session awaiting further colour on US involvement in the Israel-Iran conflict. On energy commentary from within the region; Israeli Energy Minister Cohen said Israel's energy sector is operating normally; Iranian Oil Minister said fuel supplies are currently stable, there are currently no issues - no move on these comments. Thereafter, Kazakhstan's Energy Minister says it is not considering exiting OPEC+ agreement, which sparked some very modest pressure in oil prices. Brent Aug'25 currently trades towards the bottom end of a USD 75.32-77.00/bbl band.

- Spot gold is attempting to return to the green, after an overnight session spent mostly in negative territory. Overnight, the haven attempted to move beyond the USD 3,400 mark, where it stalled at USD 3399.99/oz, though it now trades at USD 3,384/oz.

- Copper futures are modestly in the green, helped by a softer dollar ahead of the FOMC meeting. The red metal has waned in recent trade, and fell from session highs of USD 9,735/t, moving in tandem the USD attempting to pare some losses.

- Kazakhstan's Energy Minister says it is not considering exiting OPEC+ agreement.

- Russian Deputy PM Novak says there is no shortage of oil due to Middle East conflict, no risk of Russian oil exports declining due to the conflict.

- Israeli Energy Minister Cohen says Israel's energy sector is operating normally; perhaps gas exports will resume in coming hours or days.

- Iranian Oil Minister says fuel supplies are currently stable, there are currently no issues.

- Private inventory data (bbls): Crude -10.133mln (exp. -0.6mln), Distillate +0.32mln (exp. -0.1mln), Gasoline -0.2mln (exp. +0.2mln), Cushing -0.8mln.

- Brent crude's premium to Dubai at its highest since September 2023, according to sources and data cited by Reuters.

- Qatar set June-loading Al-Shaheen crude term premium at USD 2.48/bbl, highest in a year, according to Reuters sources.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK CPI YY (May) 3.4% vs. Exp. 3.4% (Prev. 3.5%); MM (May) 0.2% vs. Exp. 0.2% (Prev. 1.2%)

- UK CPI Services MM (May) -0.10% vs. Exp. 0.10% (Prev. 2.20%); YY (May) 4.70% vs. Exp. 4.80% (Prev. 5.40%)

- UK Core CPI YY (May) 3.5% vs. Exp. 3.5% (Prev. 3.8%); MM (May) 0.2% vs. Exp. 0.2% (Prev. 1.4%)

- UK RPI YY (May) 4.3% vs. Exp. 4.2% (Prev. 4.5%); MM (May) 0.2% vs. Exp. 0.1% (Prev. 1.7%); YY (May) 4.1% (Prev. 4.2%); RPI-X (Retail Prices) MM (May) 0.2% (Prev. 1.8%)

- EU Current Account SA, EUR (Apr) 19.8B (Prev. 50.9B); NSA, EUR (Apr) 19.3B (Prev. 60.1B)

- EU HICP Final YY (May) 1.9% vs. Exp. 1.9% (Prev. 1.9%)

NOTABLE EUROPEAN HEADLINES

- ECB's Panetta says the ECB will continue to take decisions on a meeting-by-meeting basis, without pre-committing to defined monetary policy course Macro risk arise from conflicting signals in US trade policy and recent escalation of Israel-Iran conflict. Macro outlook remains subject to substantial and difficult-qualify risks.

- ECB's Villeroy says Trade wars are unfortunate, they are nonsense because they add divisions, via Econostream.

NOTABLE US HEADLINES

- US President Trump posted "U.S. Wage Growth BEST IN 60 YEARS!", via Truth Social

- US plans to ease capital rule limiting banks’ Treasury trades, according to Bloomberg. Bank regulators plan to propose decreasing the Supplemental Leverage Ratio for the largest banks.

GEOPOLITICS

EUROPEAN SESSION

- Iranian Supreme leader to speak shortly, according to ISNA.

- Iranian ambassador to the UN, says, if we come to the conclusion that the US is directly involved in attacks on Iran, we will start responding to the US

OVERNIGHT

US Involvement

- US officials signalled that the next 24 to 48 hours would be critical in determining whether a diplomatic solution with Iran is possible - or if the president might resort to military action instead, according to ABC.

- "Western sources: We have indications that the US will attack Iran soon", according to Kann News.

- US embassy in Jerusalem will be closed Wednesday through Friday, according to the US State Department.

- US President Trump is considering a range of options when it comes to Iran, including a possible US strike on the country, according to multiple officials cited by NBC.

- Israel Channel 12 journalists report US could join the war against Iran Tuesday night, via Faytuks News citing a telegram post.

Strikes Headlines

- Iranian Revolutionary Guards said Iran's Fattah missiles broke through Israeli defences, giving it 'complete domination' over Israeli airspace.

- "Israel's Channel 12: Army attacks Tehran's refineries", according to Al Arabiya.

- Israeli military said it attacked a centrifuge production site and several weapons production sites of the Iranian regime last night.

- IDF Spokesman said the Iranian regime still has great capabilities that allow it to harm them, Al Jazeera reports. They attacked the IRGC headquarters and killed Iran's Chief of Staff. "When we finish our mission, we will announce it and will not allow the existential threat against us to continue".

- Iran has reportedly prepared for strikes on US bases if the US joins the war, according to NYT; Officials suggest that in the event of an attack, Iran could begin to plant mines in the Strait of Hormuz.

- Iranian Supreme Leader Khamenei said The battle has begun, via Al Hadath.

- Iranian state media claimed that tonight (Tuesday night) will "hold a surprise the world will remember for centuries", according to multiple reports.

- "IRGC: Attacks on Israel will continue continuously and gradually", according to Sky News Arabia.

Diplomacy Headlines

- "Source familiar says there are no plans for a meeting this week between Witkoff and Araghchi", according to an Al-Monitor journalist.

CRYPTO

- Bitcoin is on a weaker footing and slips below USD 105k; Ethereum also lower to a similar degree but manages to hold above USD 2.5k.

- US Senate had enough votes for stablecoin bill passage, according to Bloomberg.

APAC TRADE

- APAC stocks were mostly lower following the softer handover from Wall Street, with stocks in the US spooked by what seemed like an imminent US involvement in Israel's offensive against Iran. However, sentiment in APAC hours recovered as news surrounding US involvement quietened down overnight, with oil also coming off its best levels amid no signs of an American military attack. Ranges remained narrow ahead of the FOMC announcement.

- ASX 200 traded subdued with sectors overall mixed, but gold miners provided headwinds for the index.

- Nikkei 225 was modestly firmer and underpinned by recent losses in the JPY, while Japanese PM Ishiba agreed with US President Trump to continue ministerial-level tariff talks. Ishiba added that Japan would continue to work intensely to achieve a trade deal with the US.

- Hang Seng and Shanghai Comp traded lower but to varying degrees with underperformance in Hong Kong, although with limited news from the region, and attention focused on geopolitics.

NOTABLE ASIA-PAC HEADLINES

- PBoC governor said they will improve the monetary policy toolbox, according to Reuters.

- Chinese FX regulator said exports have maintained resilience; recent buying of onshore stocks has increased; will continue to implement proactive macro policy; will keep yuan basically stable at reasonable and balanced levels, according to Reuters.

- PBoC injected CNY 156.3bln via 7-day reverse repos with the rate maintained at 1.40%

- China will issue the rest of consumer goods trade-in funds in an orderly manner; is guiding local governments to use the funds in a stable pace. Has allocated CNY 162bln out of CNY 300bln in special treasury funds under the trade-in scheme to local governments.

DATA RECAP

- Japanese Trade Balance Total Yen (May) -637.6B vs. Exp. -892.9B (Prev. -115.8B, Rev. -115.6B)

- Japanese Exports YY (May) -1.7% vs. Exp. -3.8% (Prev. 2.0%)

- Japanese Machinery Orders YY * (Apr) 6.6% vs. Exp. 4.0% (Prev. 8.4%)

- Japanese Machinery Orders MM * (Apr) -9.1% vs. Exp. -9.7% (Prev. 13.0%)

- Japanese Imports YY (May) -7.7% vs. Exp. -6.7% (Prev. -2.2%)

- New Zealand Current Account- Annual (Q1) -24.662B vs. Exp. -24.8B (Prev. -26.401B)

- New Zealand Current Account/GDP (Q1) -5.7% vs. Exp. -5.8% (Prev. -6.2%)

- New Zealand Current Account - Qtrly (Q1) -2.324B vs. Exp. -2.2B (Prev. -7.037B)