US Market Open: Oil pushed lower after Trump gives two weeks to decide on Iran strikes

20 Jun 2025, 11:20 by Newsquawk Desk

- US President Trump offered Iran a two-week window to monitor negotiations before deciding on military action.

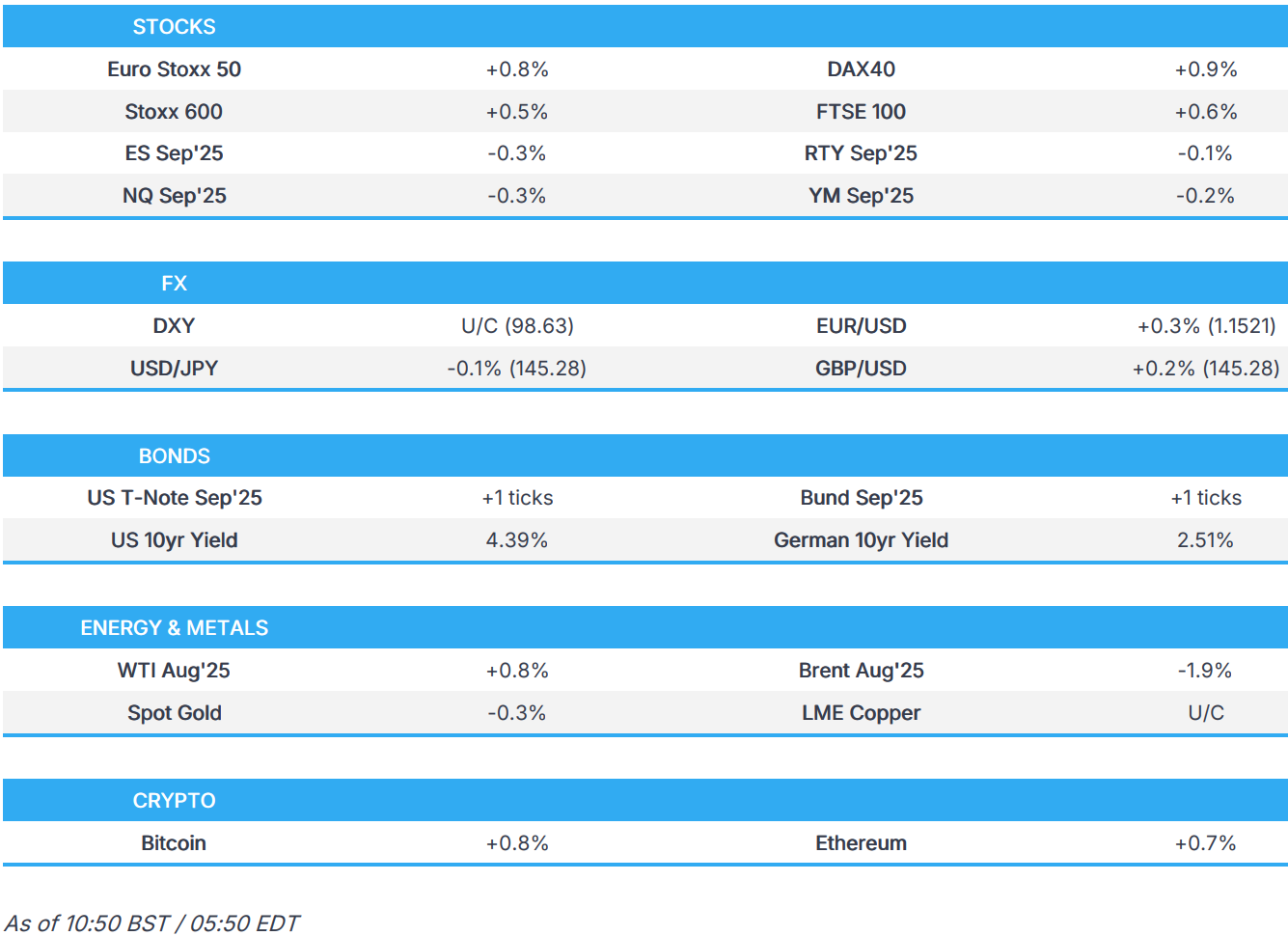

- European stocks benefit from geopolitical optimism whilst US futures are slightly lower.

- DXY flat, JPY mildly boosted by Y/Y Core CPI beat.

- Two-way action for JGBs after reports suggest Japan plans to cut FY25 superlong JGB issuance by JPY 3.2tln, Gilts gap higher on retail sales but fade.

- Crude curtailed by negotiating updates, European risk tone weighs on gold.

- Looking ahead, US Philly Fed Business Index, Leading Index Change, Canadian Producer Prices & Retail sales, EU Consumer Confidence, Quad witching, Iranian Foreign Minister Araghchi meets with European Ministers, Holidays in Sweden, Finland, New Zealand.

TRADE

- EU Economy Commissioner Dombrovskis said the EU was ready to take measures with the US if a solution could not be found, but noted that progress was being made in trade talks with Washington, according to Reuters.

- Canadian Prime Minister Carney said Canada would introduce a series of countermeasures to help it respond to Trump-era tariffs. He stated that Canada would adjust its existing counter-tariffs on US steel and aluminium products on 21 July. The level of Canadian counter-tariffs would depend on the progress of talks with the US on a new economic deal. He added that only Canadian producers and producers from trading partners offering Canada tariff-free reciprocal access would be eligible to compete for federal government procurement of steel and aluminium. Canada would adopt additional tariff measures to address risks associated with persistent global overcapacity and unfair trade in the steel and aluminium sectors. He also announced that Canada would establish new tariff rate quotas at 100% of 2024 levels on imports of steel products from non-free trade agreement partners, according to Reuters.

- Chinese Commerce Ministry says its Minister held a video meeting with EU Trade Commissioner on Thursday; had "in-depth" talks on remedy cases such as EVs

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) opened firmer, and are attempting to build on gains, benefiting from the positive mood surrounding geopolitical optimism.

- European sectors are almost entirely in the green, Energy is the sole loser, due to lower oil prices, which is to the benefit of travel and leisure, which gains. Banking stocks lead the charge, buoyed by fresh EU developments that see the European Investment Bank's annual lending ceiling raised to EUR 100bln.

- US equity futures find themselves marginally in the red, though this is more a function of a slight retreat from the gap-higher seen at the recommencement of trade from Thursday’s holiday as the benchmark digested geopolitical developments, rather than any bearish driver.

- Bloomberg Poll, Indices at end-2025: Euro Stoxx 50 seen at 5,439 (last 5,197.03); DAX 40 seen at 23,488 (last 23,057.38); FTSE 100 8,773 (last 8,791.80)

- Maersk (MAERSKB DC) says "we have made the decision to temporarily pause calling the port of Haifa with Maersk-operated vessels".

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is flat and trading in a very tight 98.53-98.70 range, after falling a touch overnight on geopolitical updates which has seen the Dollar lose its risk premia a little. In the prior session, the Dollar slipped after US President Trump offered Iran a two-week window to monitor negotiations before deciding on military action. This sparked a risk-on mood, as it helps to ease some nerves of an imminent attack on Iran and hence an escalation in the Middle East. Data docket today includes US Philly Fed Business Index and Leading Index Change.

- EUR is at the top of the G10 leaderboard, but ultimately just a little stronger vs the Dollar. No specific European-driver for the strength today, so likely on the geopolitical updates from Trump on Thursday (see above) – in brief, should the US choose not to attack Iran, this would be net-negative on crude prices and as such has lifted the Single-Currency today; gains are of course capped given the continued uncertainty. EUR/USD currently trading around the mid-point of a 1.1491-1.1532 range.

- JPY is essentially flat/modestly firmer today but did catch a slight bid following the region’s inflation report. Headline Y/Y printed in-line with expectations whilst the Core metric was a touch above expectations, and in-fact printed the fastest Y/Y pace since January 2023. Following the release of the Japanese CPI report, USD/JPY fell from 145.29 to a session trough of 145.16, but now trades around 145.30.

- GBP is incrementally firmer vs the USD but posts modest losses vs the EUR. Cable saw was mildly pressured on the release of a very weak Retail Sales report, whereby the M/M metrics fell beneath the most pessimistic of analysts’ forecasts; printing at -2.7% (exp. -0.5%). GBP/USD fell around 0.2% to make a fresh trough at 1.34470 in the hour after the Retail Sales report. Thereafter, the Pound has been trading relatively steady for most of the morning. Upside levels include its 21 DMA at 1.3518.

- Antipodeans are incrementally firmer/flat vs the Dollar in what has been a lacklustre session so far. Specifics for the Aussie and Kiwi have been on the lighter side overnight.

- PBoC set USD/CNY mid-point at 7.1695 vs exp. 7.1801 (prev. 7.1729); strongest CNY fix since March 17th

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs are essentially flat but did see some marked action in a 139.32 to 139.50 band as draft reporting and commentary emerges from the Ministry of Finance Meeting. In brief, Bloomberg citing a draft reported that Japan intends to cut super long issuance by JPY 3.2tln, by cutting JPY 100bln from 30yr and 40yr auctions and 200bln from the 20y; consensus was for 100bln in each tenor.

- USTs incrementally firmer/flat as it returns to Cash trade following Thursday's holiday. Contained overnight, but was then pressured in the European morning, potentially as traders continue to digest and factor in the latest geopolitical optimism. Downside limited so far, and USTs remain above Thursday’s 110-22+ base.

- Bunds were modestly firmer for much of the morning. Lifted by around 30 ticks on the UK retail metrics this morning (see Gilts). Peaked at a 131.33 high but has since been drifting and now finds itself back marginally below the figure, and by extension in proximity to the earlier 130.88 low; now essentially unchanged on the session.

- Gilts gapped higher by 18 ticks, following an abysmal set of retail data. The series saw sales volumes fall across the board, the most pronounced move was in food and while that is somewhat skewed by an unfavourable prior, the series is nonetheless dire. While bid initially, and to a 93.05 peak, the move proved somewhat short-lived as Gilts also digested the latest PSNB data. A series that featured the highest May borrowing on record, ex-COVID; metrics that offset the dovish impulse from Retail Sales. Overall, Gilts now near-enough flat and at the lower-end of the day’s limited 92.83 to 93.05 band.

- Japan plans to cut FY25 superlong JGB issuance by JPY 3.2tln, via Bloomberg citing a plan; Japan to cut 20yr bond issuance by JPY 200bln (exp. JPY 100bln); cut 30yr by JPY 100bln (exp. JPY 100bln); cut 40yr by JPY 100bln (exp. JPY 100bln), per auction. Japan to offset cuts by boosting the issue of 5yr and 2yr notes and T-bill.

- Japan Finance Ministry Official does not deny the possibility of considering buying back some JGBs; not in the process of implementing buybacks right now; will need to consider various factors if steps are decided.

- Click for a detailed summary

COMMODITIES

- Brent suffers losses of around USD 2/bbl on optimism of Middle-East negotiations, with Iran-E3 meetings today, and primarily after the two-week window Trump has provided. Note, while Brent is lower, WTI posts gains of USD 0.40/bbl, a discrepancy due to the lack of settlement amid the US holiday on Wednesday. Geopolitical updates this morning light, aside from, US Secretary of State Rubio telling his French counterpart that the US is ready for direct contact with the Iranians at any time, however the Iranian Foreign Minister noted that the nation would not speak with the US, while Israeli attacks continue.

- Spot gold is suffering from the generally positive risk environment, currently holding around the USD 3350/oz mark but has been USD 10/oz lower; given the geopolitical relief, mentioned in the crude section. XAU has taken out the 21-DMA at USD 3345/oz, the next level comes via the June 12th low of USD 3338/oz.

- Base metals are in the red and failing to benefit from the positive European mood after the red metal failed to coat-tail on the broadly firmer European risk tone. Copper currently tests the USD 9,600 mark, and resides within USD 9,565.45-9,654.6/t bounds.

- Citi said that if 1.1mln BPD of Iranian oil exports were disrupted—using May exports as a baseline—it estimated prices should rise by about 15–20%, compared with an average of USD 65/bbl in the month before the Iran-Israel conflict escalated on 12 June. A 1.1mln BPD disruption implied Brent prices should be in the USD 75–78/bbl range. Citi added that prices reaching USD 90/bbl—its current bullish case, short of a major escalation in oil transit—would imply a disruption of 3mln BPD over a multi-month period, according to Reuters.

- India restricted the import of alloys of palladium, rhodium, and iridium containing over 1% gold by weight, according to Reuters.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GfK Consumer Confidence (Jun) -18.0 vs. Exp. -20.0 (Prev. -20.0)

- UK Retail Sales MM (May) -2.7% vs. Exp. -0.5% (Prev. 1.2%, Rev. 1.3%); Ex-Fuel MM (May) -2.8% vs. Exp. -0.5% (Prev. 1.3%, Rev. 1.4%)

- UK Retail Sales YY (May) -1.3% vs. Exp. 1.7% (Prev. 5.0%, Rev. 5.0%); Ex-Fuel YY (May) -1.3% vs. Exp. 1.8% (Prev. 5.3%, Rev. 5.2%)

- UK PSNB, GBP (May) 17.686B GB vs. Exp. 16.2B GB (Prev. 20.155B GB, Rev. 20.052B GB)

- German Producer Prices MM (May) -0.2% vs. Exp. -0.3% (Prev. -0.6%); YY (May) -1.2% vs. Exp. -1.2% (Prev. -0.9%)

NOTABLE EUROPEAN HEADLINES

- BoE's Bailey says "we are living in a world of much larger economic shocks which have their origins outside economic causes".

NOTABLE US HEADLINES

- Punchbowl reports: Democratic staffers are meeting with the parliamentarian’s office today, GOP aides will also have their own meetings. After that, full Byrd Bath arguments with GOP and Democratic staffers will start Sunday, according to Punchbowl source.

GEOPOLITICS

EUROPEAN HOURS

-

E3/EU-Iran meeting in Geneva expected to occur "this afternoon", via WSJ's Norman.

- Israeli Defence Minister Katz has ordered the military to increase attacks on Iranian regime targets within Tehran.

- Iran's Foreign Minister says they will only hold nuclear talks in the E3 meeting.

- Russia's Kremlin says dialogue with Ukraine continues expect to agree next week on a date for the next round of talks Ukraine is unpredictable, continue "special military operation", though would prefer to reach goals by diplomatic needs.

APAC/US HOURS

US Involvement

- The White House said, “message directly from the President – based on the fact that there is a significant chance of negotiations with Iran in the near future – I will make a decision on whether to launch [an attack] in the next two weeks.”

- US President Trump had been briefed on both the risks and benefits of bombing Fordow and his mindset was that disabling it was necessary due to the risk of weapons being produced in a relatively short period of time, according to CBS.

- Broadcasting Authority, citing an Israeli source, reported that the US had asked Israel to defer its attack on the Fordow nuclear facility.

- Kann News reported that there was a "possible attack at Fordow": according to sources, the US had asked Israel to wait until negotiations with Iran had been exhausted.

- US President Trump is to attend a National Security Meeting at 11:00 EDT on Friday.

- US law enforcement officials had stepped up surveillance of Iran-backed operatives in the US, according to CBS sources.

- The White House said Iran was able to produce a nuclear bomb within "a couple of weeks".

- A White House official told Fox's Heinrich that the US military had no doubt about the efficacy of bunker busters in eliminating the site at Fordow, and also denied that any options—including tactical nuclear weapons—had been taken off the table.

- The White House Press Secretary said there were no signs that China was getting involved militarily in Iran, according to Reuters.

- The US reportedly believed Iran would build a nuclear bomb if Supreme Leader Khamenei were assassinated and the Fordow facility was attacked, according to The New York Times.

Strikes

- There were reports of Israeli strikes in the Lavizan area of Tehran, where Iranian Supreme Leader Khamenei was reportedly hiding in a bunker, according to i24 journalist Stein.

- An Israeli military spokesman said Israel had attacked the special forces headquarters of the internal security apparatus in Tehran within the last 24 hours, according to Reuters.

- Journalist Horowitz said on X that opposition sources were circulating "unconfirmed" reports claiming that the head of Iran's military, Abdolrahim Mousavi, had been killed in an Israeli strike.

- The Fars News Agency said Iran had used a new generation of precision missiles in its attack on Israel on Thursday morning, according to Fars.

- The Norwegian Foreign Ministry said an explosion had occurred on Thursday evening in Tel Aviv at the residence of the Norwegian ambassador to Israel, according to Reuters.

- The Jordanian army said an explosives-laden drone had fallen in the Azraq area after it “fell short of its range,” according to Al Hadath.

- Iranian media reported that air defences were activated in Isfahan, according to Al Arabiya.

Diplomacy

- Britain, France, and Germany are to hold talks with Iran’s Foreign Minister on Friday in a last-ditch effort to avert an escalation of conflict in the Middle East and a possible US intervention, according to FT.

- Iran's Foreign Minister had reached out to European foreign ministers, requesting a meeting with them on Friday, Jerusalem Post reported.

- Trump administration officials are pitching the president’s two-week timeline as an opportunity to allow diplomacy to play out. Special Envoy Witkoff and Iran’s Foreign Minister Araghchi had been in communication in recent days, though there were no plans for the two to meet yet, according to ABC.

- Trump's special envoy to the Middle East Witkoff will not attend the UK/France/Germany talks with Iran in Geneva on Friday, according to White House officials cited by NBC.

- An Iranian source denied reports of a phone call between Iranian Foreign Minister Araghchi and US presidential envoy Witkoff following Israel’s aggression, according to Iran Nuances.

- The White House Press Secretary said they would see how the EU meeting with the Iranians went tomorrow, according to Reuters.

- US officials said no date had been set for a meeting between US and Iranian officials yet, according to Axios.

US Military and Deployment

- Over the next 10 to 14 days, there were expected to be two aircraft carriers in the Middle East and a third operating in the Mediterranean Sea, according to ABC.

Iranian Actions

- A senior IRGC official said that before the Israeli airstrikes, all enriched uranium had been transferred from the nuclear sites to secret hiding locations, according to i24 journalist Stein.

- Iran’s Tasnim News Agency, quoting an Iranian official, said intelligence had thwarted a major Israeli plot against Iranian Foreign Minister Araqchi in Tehran, according to Sky News Arabia.

- Iraq’s Hezbollah threatened to target US bases and close the Strait of Hormuz if Washington joined strikes on Iran, according to Al Hadath.

- An Israeli official said Iran could likely sustain the current rate of missile fire at Israel for up to five months, provided their missile launchers were not destroyed, according to NBC.

- Israel anticipated attacks from Iran’s proxies across the Middle East, according to Israel Channel 14.

- An Israeli intelligence official said the imminent collapse of the Iranian regime was far from the truth, according to NBC.

OTHERS

- A Japanese destroyer sailed through the Taiwan Strait after a Chinese jet approached it, according to Nikkei.

- China President Xi met with New Zealand PM Luxon in Beijing, according to CCTV.

CRYPTO

- Bitcoin a little firmer and trades just shy of USD 106k.

- Norway Government will investigate a temporary ban on power-intensive crypto mining.

APAC TRADE

- APAC stocks initially saw directionless trade following a non-existent lead from Wall Street amid the Juneteenth market holiday. Nevertheless, geopolitics remained in the spotlight as US President Trump now has to decide whether or not to join Israel’s offensive against Iran’s nuclear facilities within the next two weeks, contingent on negotiations. Sentiment eventually turned mostly firmer with notable Israel-Iran newsflow on the lighter side.

- ASX 200 was subdued with miners dragging on the index whilst losses in financials also kept upside capped.

- Nikkei 225 was buoyed by recent JPY weakness but came off best levels in tandem with USD/JPY after Japanese Core CPI topped expectations, whilst stale BoJ minutes (from two meetings ago) were also released.

- Hang Seng and Shanghai Comp were initially choppy with the indices trimming modest earlier gains despite relatively quiet newsflow. The PBoC LPR setting was a non-event, with the central bank maintaining the 1-year and 5-year LPRs as expected.

NOTABLE ASIA-PAC HEADLINES

- The PBoC maintained its 1-year Loan Prime Rate (LPR) at 3.00% and its 5-year LPR at 3.50%, as expected, according to Reuters.

- Japanese Finance Minister Kato said they had observed spikes in super‑long JGB yields recently, according to Reuters.

- Minutes from the BoJ's 30 April – 1 May meeting showed that many members said they must carefully scrutinise each nation's trade policy and its developments, given the heightening downside risks to the economy and prices, according to Reuters.

- PBoC injected 161.2bln via 7-day reverse repos with the rate maintained at 1.40%.

- BoJ Governor Ueda says Japan's economy is recovering moderately albeit with some weakness, underlying inflation to gradually heighten after a pause.

DATA RECAP

- Japanese CPI, Core Nationwide YY (May) 3.7% vs. Exp. 3.6% (Prev. 3.5%); fastest Y/Y pace since Jan 2023.

- Japanese CPI, Overall Nationwide (May) 3.5% (Prev. 3.6%)

- South Korean PPI Growth YY (May) 0.3% (Prev. 0.9%, Rev. 0.8%)

- South Korean PPI Growth MM (May) -0.4% (Prev. -0.1%, Rev. -0.2%)