Europe Market Open: Europe set for a modestly firmer open as Middle-East tensions cool, ahead of NATO summit

25 Jun 2025, 06:40 by Newsquawk Desk

- APAC stocks traded stronger following the firm lead from Wall Street, with gains capped as traders were cautious amid the fragility of the Israel-Iran ceasefire.

- Geopolitical newsflow was relatively light in APAC hours, with no hostile incidents seen between Israel and Iran; “There have been no [US] sanctions lifted on Iran,” said Fox Business' Lawrence, in reference to President Trump's post suggesting China could continue to buy oil from Iran.

- Fed Chair Powell said they would expect to see meaningful inflation effects from tariffs in June, July, and August. He added that if those effects failed to materialise, it could lead to an earlier rate cut.

- BoJ board member Tamura said that if upward price risks heightened, the BoJ could face a situation where it would need to raise rates decisively, even if uncertainty remained high, adding that he does not see 0.5% as a barrier for BoJ rate hikes.

- Fox's Gasparino posted that Team Trump said it was close to announcing a handful of trade deals. The major ones the White House claimed progress on involved Japan, South Korea, and Vietnam.

- Looking ahead, highlights include US Building Permits, CNB Policy Announcement; NATO Summit, Fed SLR meeting, BoE’s Lombardelli, Pill, Greene; Fed's Powell; US President Trump, Supply from Italy, UK, US, and Earnings from General Mills, Paychex, Micron, Babcock.

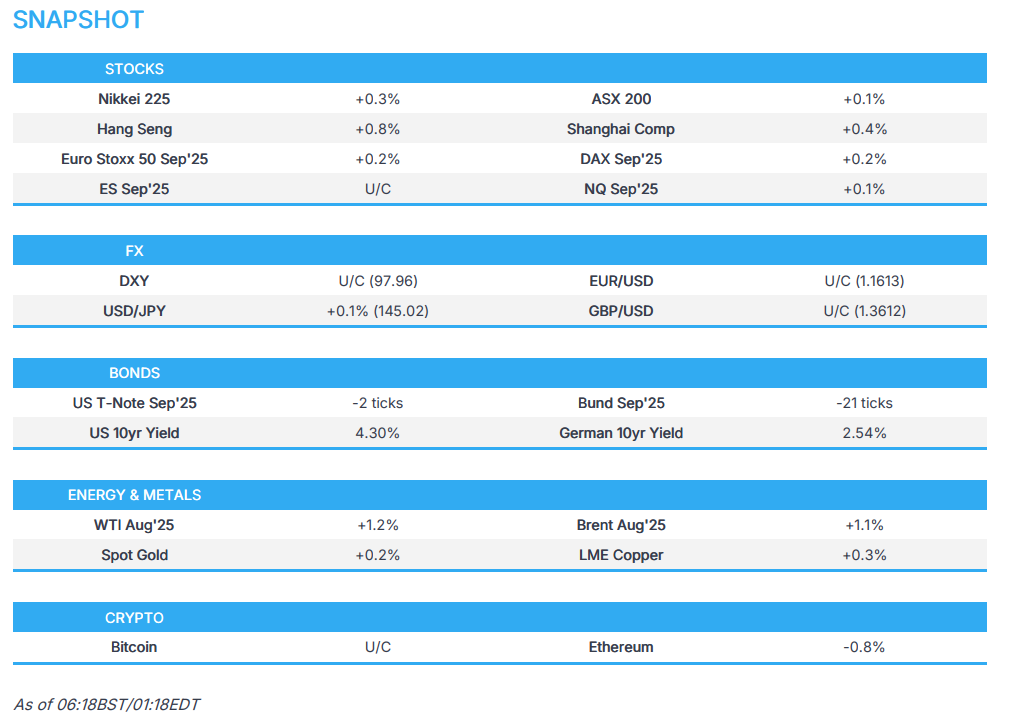

SNAPSHOT

US TRADE

EQUITIES

- US stocks were in risk-on mode following the announced ceasefire from US President Trump between Israel and Iran. Despite reports of both Iran and Israel breaching the agreement and Trump expressing discontent, risk appetite remained intact, with major US indices closing over 1% higher and the S&P 500 trading within ~1% of all-time highs.

- Sectors ex-Energy were broadly in the green, led by gains in Financials, Tech, and Communications, while Energy lagged amid a continued slump in crude prices.

- SPX +1.11% at 6,092, NDX +1.53% at 22,191, DJI +1.19% at 43,089, RUT +1.34% at 2,161

- Click here for a detailed summary.

NOTABLE HEADLINES

- Senate Majority Leader Thune planned a Friday Senate vote on the Trump tax bill, according to Axios.

- Several Senate committees expect the updated reconciliation text as soon as Wednesday morning, according to Punchbowl sources, to reflect modifications based on initial parliamentarian rulings.

- US Treasury Secretary Bessent said they are on track for a vote, hopefully on Friday, and noted that the X-date for the debt ceiling could change if courts interfered with Trump. He expressed confidence that the US House would pass the Senate bill and said they were in a good spot.

- New York Independent System Operator said it had issued an energy warning for June 24 due to a decline in operating reserves, according to Reuters. The grid was operating normally at the time, but emergency operations might be initiated to maintain system reliability.

- A US judge blocked the Trump administration from withholding funds awarded to 14 states for EV charger infrastructure, according to a court filing.

- Key member of Musk's DOGE resigned from government, according to the New York Times.

- Andrew Cuomo conceded in the New York City mayoral Democratic primary.

GEOPOLITICS

- “There have been no [US] sanctions lifted on Iran,” said Fox Business' Lawrence, in reference to President Trump's post suggesting China could continue to buy oil from Iran. A senior White House official added: “The President was simply calling attention to the fact that because of his decisive actions to obliterate Iran’s nuclear facilities and broker a ceasefire between Israel and Iran, the Strait of Hormuz will not be impacted, which would have been devastating for China. The President continues to call on China and all countries to import our state-of-the-art oil rather than import Iranian oil in violation of US sanctions.”

- Iranian Foreign Minister Araqchi said the nuclear programme continues, according to Al Arabiya.

- White House Middle East envoy Witkoff said the US and Israel had achieved their goals in Iran, according to Fox News. He described talks with Iran as encouraging and stated it was time to sit with Iran and make a comprehensive deal.

- Iran's Revolutionary Guards denied there was any drone attack in the northwestern city of Tabriz following reports air defences were activated in the area, according to Iranian news sites.

- Early US intelligence assessment suggested that the strikes on Iran did not destroy core nuclear sites, CNN reported. According to three sources briefed on the DIA’s findings, US military strikes on three Iranian nuclear facilities last weekend likely set the programme back by only a few months. The initial assessment—based on battle damage evaluations from US Central Command—contradicted President Trump’s public statements that the sites were “completely and totally obliterated.” Two sources confirmed Iran’s enriched uranium stockpile remained intact, and one said the centrifuges were largely unaffected. The White House acknowledged the report but said it disagreed with the conclusions.

- Israeli security source, cited by Al Hadath, said they knew exactly where Iran transported its enriched uranium. However, they would not target the enriched uranium sites to avoid causing a nuclear disaster.

- Israel’s representative to the UN Security Council stated that Iran had been involved in producing a nuclear bomb, according to Sky News Arabia.

- Israel's representative to the United Nations said that diplomatic talks with Iran will take place soon, according to Al Arabiya.

- US is set to open its embassy in Jerusalem on June 25th, following the ceasefire between Israel and Iran and the lifting of all restrictions by Israel’s Home Front Command, according to a statement.

- Iran executed three men for allegedly working for Israel’s spy agency Mossad, according to the Mizan News Agency.

TRADE/TARIFFS

- Fox's Gasparino posted that Team Trump said it was close to announcing a handful of trade deals. The major ones the White House claimed progress on involved Japan, South Korea, and Vietnam. India was not on the list of pending agreements amid the recent spat with Pakistan.

- EU warned that a baseline Trump tariff would still spur retaliation, and noted that retaliatory tariffs on US imports could include Boeing (BA) aircraft, according to Bloomberg.

CENTRAL BANKS

- Fed Chair Powell said they would expect to see meaningful inflation effects from tariffs in June, July, and August. He added that if those effects failed to materialise, it could lead to an earlier rate cut. Powell said that US Treasuries remain a safe haven, adding that Treasury markets are functioning well and normally. He noted the Fed is getting closer to price stability, though not quite there yet. Once price stability is achieved, the Fed will be able to respond more forcefully to any economic downturns. Powell clarified that interest rates are modestly, not moderately, restrictive.

- Fed’s Barr (voter) said monetary policy is well positioned for the Fed to wait and observe how economic conditions unfold. He noted the US economy remained on solid footing, with low and steady unemployment and ongoing disinflation. However, he warned inflation was set to rise due to tariffs and flagged potential persistence from higher short-term expectations, supply chain adjustments, and second-round effects. Tariffs could also slow the economy and push unemployment higher. While real-world rates were shaped by various forces, Barr acknowledged Fed policy still played a role.

- Fed’s Collins (2025 voter) said the current state of monetary policy is necessary, according to Reuters.

- Fed’s Kashkari (2026 voter) said the Fed is in wait-and-see mode to gain more clarity on how tariffs would affect inflation, emphasising the need to better understand what’s really happening before making any policy changes. He acknowledged that tariffs had introduced complexity, noting that inflation remained above the 2% target, though substantial progress had been made. He said businesses are reporting strong fundamentals but also nervousness around tariffs. Kashkari added that while it was possible the Fed could cut rates even with elevated inflation if the labour market deteriorated sharply, that is not the current forecast.

- Fed's Schmid (2025 voter) said the central bank has time to study the effects of tariffs on inflation before making any rate decisions. He noted that both employment and inflation are near the Fed's goals. Contacts indicated that tariffs would raise prices and weigh on economic activity. He added that the economy’s resilience meant the Fed could afford to wait and observe developments before proceeding with rate cuts.

- Fed's Williams (voter) said the impact of tariffs is likely to grow stronger in the coming months, noting it would take time for the effects to fully play out in inflation data. He stressed that the Fed’s ability to pay interest on reserves remained critical to the execution of monetary policy, and added that policy is well-positioned at present. Fed’s Williams added the economy is expected to grow at a slower pace this year, though the job market would remain solid. He noted that uncertainty is just as significant as the direct impact of tariffs on economic performance, adding that resolving uncertainty could provide a boost to the economy. He said the tariff impact was already evident, possibly contributing around a quarter of a percentage point to current inflation. Outside of tariffs, inflation remained broadly on track. Williams described monetary policy as very well-positioned and stated that interest rates would eventually need to move lower. He added the Fed will rely on incoming data over time to inform its next interest rate decision. He said modestly restrictive monetary policy gives the Fed space to examine new data, and that the US economy is in a good place with a solid job market. However, he noted that uncertainty, tariffs, and reduced immigration would slow the economy, projecting GDP growth of around 1% this year. He expects unemployment to climb to roughly 4.5% by year-end, in line with the Fed’s median 2025 forecast. He said tariffs would lift inflation to 3% this year but sees it gradually falling to 2% over the next two years. While overall inflation is near target, underlying inflation remains elevated, and he sees signs tariffs are impacting some sectors. He flagged weak soft data versus more resilient hard data and said the Fed’s balance sheet drawdown continues smoothly.

- BoJ June meeting Summary of Opinions stated that, while much of the hard data for April and May had been relatively solid, it was likely that the effects of tariff policies had yet to materialise. Although uncertainty regarding trade policies remained extremely high, on the domestic front, wage developments had been solid and the CPI had been slightly higher than expected. Japan’s economy was at a crossroads between making a transition to a “growth-oriented economy driven by wage increases and investment” and falling into stagflation. Although the direct impact of US tariff policy has not been observed so far, Japan’s economy has been somewhat stagnant. Despite the impact of US tariff policy, many firms would likely continue to raise wages to address labour shortages and make high levels of business fixed investment. While the impact of the US tariff policy would certainly exert downward pressure on firms’ sentiment, the Bank needed to take some time to examine the magnitude of the impact on the real economy. Given high uncertainty, the Bank should at this point maintain accommodative financial conditions with the current interest rate level and thereby firmly support the economy. Even though prices had been somewhat higher than expected, it was appropriate for the Bank to maintain current policy given downside risks stemming from US tariff policy and the situation in the Middle East. Although the CPI had been higher than expected, the pass-through of higher wages to services prices seemed to have plateaued. The situation of government bond markets around the world had been a major topic of discussion, such as at international meetings, and attention was warranted on the possibility that developments overseas would spread to Japan. Increased volatility in the super-long-term zone might spill over to the entire yield curve, thereby spreading unintended tightening effects to the market as a whole.

- BoJ board member Tamura said that if upward price risks heightened, the BoJ could face a situation where it would need to raise rates decisively, even if uncertainty remained high, adding that he does not see 0.5% as a barrier for BoJ rate hikes. He stressed the need to steadily normalise the balance sheet, even though it may take time, and noted he had voted against the June decision to slow the pace of bond-buying taper next year, arguing the BoJ should normalise bond holdings as soon as possible. Tamura stated that while the JGB market function had improved somewhat, it still remained low. He reiterated his stance that rate hikes must be timely and appropriate, neither too quick nor too late. On the economy, he assessed that inflation was on track or somewhat stronger than expected, with upward risks having been elevated until March. He flagged that market-based services inflation was exceeding 2%, and both rent and public service costs were rising gradually. He noted the rise in fresh food prices could no longer be described as temporary and must be monitored carefully. Medium- and long-term inflation expectations were gradually heightening, with household and corporate expectations already around 2%. He warned of the risk that Japan’s inflation expectations could overshoot further. Tamura also said US tariffs would likely weigh on Japan’s economy and prices, but projected inflation would remain near 2% until fiscal 2027. Despite some downside risks, he assessed that the probability of Japan reverting to a low wage/price growth environment was low. Consumer inflation data for April and May had overshot expectations, and wage momentum in Japan was sufficiently strengthening.

APAC TRADE

EQUITIES

- APAC stocks traded stronger following the firm lead from Wall Street, with gains capped as traders were cautious amid the fragility of the Israel-Iran ceasefire. From a central bank perspective, some attention in US hours was on Fed Chair Powell, who echoed his wait-and-see stance but left July options open during the Q&A. Thereafter, sentiment in APAC trade was somewhat capped after BoJ taper-dissenter Tamura struck a hawkish tone, suggesting the BoJ may need to raise rates decisively—even amid high uncertainty—if upward price risks heighten. He also noted that he does not see 0.5% as a barrier for BoJ rate hikes.

- ASX 200 fluctuated between modest gains and losses before a sub-forecast Aussie Monthly CPI print provided a mild boost. The monthly gauge came in at 2.1%, towards the bottom end of the RBA’s 2–3% target range, though market pricing barely shifted.

- Nikkei 225 saw choppy trade in limited ranges following commentary from BoJ’s Tamura, who said he does not see 0.5% as a ceiling for rate hikes. On the trade front, FBN's Gasparino suggested progress in US-Japan trade talks. The BoJ Summary of Opinions noted that the effects of tariff policies are likely yet to materialise.

- Hang Seng and Shanghai Comp conformed to the broader tone following a muted open as traders awaited the next catalyst. The indices saw upticks following remarks from China's Premier Li who said judging from key indicators, China's economy showed a steady improvement in Q2, and he is confident in China's ability to maintain a relatively rapid growth.

- US equity futures (ES U/C, NQ +0.1%) were flat with a mild downward bias following the prior day’s gains on the back of the fragile ceasefire between Iran and Israel. Fed Chair Powell, during his Q&A yesterday, left July options open. Macro newsflow was light during APAC trade, with participants looking ahead to a speech by US President Trump at the NATO summit (expected to focus on his Iran operation), alongside another round of Powell testimony—this time before the Senate Financial Services Committee.

- European equity futures are indicative of a slightly firmer cash open with the Euro Stoxx 50 future +0.2% after cash closed higher by 1.5% on Tuesday.

FX

- DXY saw choppy trade within a tight range amid a lack of newsflow during the APAC session, with the index holding a downward bias overnight as participants remained cautious and after Fed Chair Powell left all July options open. DXY traded in a 97.81–97.96 range vs the weekly high of 99.42 (Monday) and low of 97.70 (Tuesday).

- EUR/USD moved in tandem with the Dollar after the pair eked out a fresh multi-year peak at 1.1641 on Tuesday, with the APAC range currently between 1.1605 and 1.1631.

- GBP/USD was also dictated by Dollar action amid a lack of UK-specific newsflow overnight, as Sterling traders braced for another slew of BoE speakers on Wednesday. Cable traded in a 1.3612–1.3628 range after finding resistance at 1.3650 on Tuesday.

- USD/JPY was initially softer amid gains in the JPY following hawkish remarks from BoJ taper-dissenter Tamura, who reiterated that 0.5% is not a barrier for BoJ rate hikes and took USD/JPY to session lows. FBN’s Gasparino flagged progress between the US and Japan on trade talks. The BoJ Summary of Opinions resulted in some modest USD/JPY choppiness but nothing notable. The pair later trimmed losses back towards 145.00. USD/JPY traded in a 144.63–145.04 range, with Tuesday’s low at 144.49 and the 50DMA at 144.22.

- Antipodeans marginally outperformed amid the upside seen stateside and a broader rise in commodity prices. AUD/USD saw an immediate knee-jerk lower on the sub-forecast monthly CPI metric, which ultimately did little to change the current course of the RBA.

- PBoC sets USD/CNY mid-point at 7.1668 vs exp. 7.1709 (prev. 7.1656)

FIXED INCOME

- 10yr UST futures took a breather after Tuesday’s rise, which was in part facilitated by the drop in crude prices and further supported by Fed Chair Powell keeping July options open. As for Tuesday’s 2yr auction, overall demand was decent, with a strong through indicating positive uptake—albeit slightly eased from the prior auction.

- Bund futures were choppy in a narrow range but with a downward bias. The Eurozone calendar for Wednesday is rather light, with attention turning to the NATO summit and any defence funding commitments.

- 10yr JGB futures bucked the broader trend while catching up to some of the gains seen in Western counterparts. However, gains were capped following hawkish commentary from BoJ taper dissenter Tamura, who reiterated that 0.5% is not a barrier for rate hikes. Meanwhile, one notable line from the BoJ Summary of Opinions stated that “increased volatility in the super-long-term zone may spill over to the entire yield curve, thereby spreading unintended tightening effects to the market as a whole.”

- US sells USD 69bln of 2yr notes: 0.1bps stop-through, High Yield: 3.786% (prev. 3.955%, six-auction average 4.075%); WI: 3.787%. Tail: -0.1bps (prev. -1.0bps, six-auction avg. -0.3bps). Bid-to-Cover: 2.58x (prev. 2.57x, six-auction avg. 2.62x). Dealers: 13.2% (prev. 10.5%, six-auction avg. 11.1%). Directs: 26.3% (prev. 26.2%, six-auction avg. 17.6%). Indirects: 60.5% (prev. 63.3%, six-auction avg. 71.3%)

- Australia sells AUD 1bln 3.50% 2034 AGB: b/c 3.73x (prev. 3.17x), Average yield 4.0895% (prev. 4.4349%)

COMMODITIES

- Crude futures pared back some of the recent losses, with overnight newsflow relatively light, although private inventories printed a larger-than-expected draw. Regarding President Trump’s post that China can continue to buy oil from Iran, Fox’s Lawrence clarified that “there have been no [US] sanctions lifted on Iran... the President was simply calling attention to the fact that... the Strait of Hormuz will not be impacted, which would have been devastating for China.”

- Spot gold took a breather from recent losses which were sparked by the improved geopolitical backdrop, having briefly dipped below USD 3,300/oz on Tuesday before stabilising around USD 3,330/oz in APAC trade.

- Copper futures saw modest upside, with 3M LME contracts trading on either side of USD 9,700/t. However, further gains were capped by the cautious risk tone.

- Private Inventories: Crude -4.28mln (exp. -0.8mln), Distillate -1.03mln (exp. +0.4mln), Gasoline +0.75mln (exp. +0.4mln), Cushing -0.08mln.

CRYPTO

- Bitcoin traded with cautious gains overnight on either side of USD 106.5k.

NOTABLE ASIA-PAC HEADLINES

- China’s Premier Li said that key indicators pointed to steady improvement in Q2, and expressed confidence in maintaining a relatively rapid growth rate. He added that regardless of global developments, China’s economy had consistently shown strong growth momentum.

- Chinese Premier Li said the world economy and international economic and trade cooperation once again faces new difficulties and challenges, according to remarks at the World Economic Forum in Tianjin. He added that the risk of fragmentation in global industrial supply chains is on the rise.

- Chinese President Xi Jinping is reportedly not attending next week’s BRICS summit, marking his first-ever absence, due to a scheduling conflict, according to SCMP sources.

- PBoC injected 365.3bln via 7-day reverse repos with the rate maintained at 1.40%.

- CBA now anticipates RBA to cut rate in July (prev. August), following the softer-than-expected Australian CPI data.

DATA RECAP

- New Zealand Trade Balance (May) 1.235B (Prev. 1.426B, Rev. 1.285B)

- New Zealand Annual Trade Balance (May) -3.79B (Prev. -4.81B, Rev. -4.97B)

- New Zealand Imports (May) 6.44B (Prev. 6.42B, Rev. 6.41B)

- New Zealand Exports (May) 7.68B (Prev. 7.84B, Rev. 7.70B)

- Japanese Services PPI (May) 3.30% (Prev. 3.10%, Rev. 3.40%)

- Australian Weighted CPI YY (May) 2.1% vs. Exp. 2.3% (Prev. 2.4%)0

EU/UK

NOTABLE HEADLINES

- UK is to reportedly purchase twelve F-35A fighter jets, with an announcement from the UK PM potentially on Wednesday, according to The Telegraph. Unlike the F-35B jets the UK currently possesses, the F-35A variant can carry nuclear weapons.

DATA RECAP

LATAM

- Brazilian Finance Minister Haddad said the debate about increasing public spending was halted, according to an interview with Record, adding, "At this moment no spending increase is welcome." He expressed concern about interest rates, noting they were very restrictive.