European Market Open: USD briefly dips on reports that Trump may name Powell successor early, APAC stocks traded mixed

26 Jun 2025, 06:50 by Newsquawk Desk

- APAC stocks traded mixed in choppy fashion following a similar session on Wall Street, with overnight newsflow relatively light as Israel and Iran seemingly continued to observe the ceasefire.

- US President Trump may accelerate the announcement of a successor to Fed Chair Powell, according to WSJ sources.

- Chinese state planner official said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters.

- HKMA bought HKD 9.42bln as the Hong Kong dollar hit the weak end of its trading range, marking the first such intervention since 2023 to defend the currency peg.

- Micron (MU) said there may have been some tariff-related pull-ins by certain customers; customer inventory levels have been healthy overall across end markets.

- Looking ahead, highlights include German GfK Consumer Sentiment, US Durable Goods, GDP Final (Q1), PCE (Q1), Jobless Claims, National Activity Index, Advance Goods Trade Balance, Wholesale Inventories, Banxico Policy Announcement, ECB’s de Guindos, Schnabel, Lagarde; BoE’s Bailey, Breeden; Fed’s Daly, Barkin, Hammack, Barr, Kashkari, supply from US, Earnings from Walgreens, Nike, H&M.

- Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks were ultimately mixed as the Nasdaq 100 was the one major index to close with gains and was largely buoyed by gains in the mega-cap names, highlighted by Tech and Communication, two of the only sectors, as well as Health, in the green. Real Estate, Consumer Utilities, and Consumer Staples lagged as the latter was weighed on by weak General Mills guidance.

- SPX +0.00% at 6,092, NDX +0.21% at 22,238, DJI -0.25% at 42,982, RUT -1.16% at 2,136

- Click here for a detailed summary.

NOTABLE HEADLINES

- US President Trump may accelerate the announcement of a successor to Fed Chair Powell, possibly as early as this summer, or in September or October, according to WSJ sources. The move could allow the nominee to shape investor expectations before Powell’s term ends. Potential candidates include: Former Fed Governor Kevin Warsh, National Economic Council Director Kevin Hassett, Treasury Secretary Scott Bessent, Former World Bank President David Malpass, and Fed Governor Christopher Waller.

- Micron (MU) Q3 2025 (USD): Adj. EPS 1.91 (exp. 1.60), Revenue 9.3bln (exp. 8.81bln), Adj. net income 2.2bln (exp. 1.8bln); strong Q4 guidance. Q4 adj. EPS view 2.35-2.65 (exp. 1.97). Q4 revenue view 10.4-11bln (exp. 9.89bln). Fiscal Q4 revenue is projected to grow another 15% sequentially. Co. said there may have been some tariff-related pull-ins by certain customers; customer inventory levels have been healthy overall across end markets. Shares +0.9% after hours.

- Fed proposes changes to ease ESLR for large banks. Proposal would reduce aggregate tier 1 capital requirements for global systemically important banks by 1.4% or USD 13bln. The proposal would reduce capital requirements for depository institution subsidiaries of global banks by 27% or USD 213bln. The proposal would replace a 2% ESLR buffer with a buffer equal to half of each bank's GSIB surcharge. The proposal would replace a 3% ESLR buffer for global bank subsidiaries with half of each bank's GSIB surcharge. Fed Vice Chair Bowman says changes would build resilience in US Treasury markets and reduce market dysfunction. Fed chair Powell says it is prudent for the Fed to reconsider the rule given the stark increase in the level of relatively safe assets on bank balance sheets. Fed governors Barr and Kugler oppose proposed changes, according to prepared statements.

- US NEC Director Hassett said plenty of room for the Fed to lower interest rates right now.

- US Republican Representative Lalota said, in reference to SALT, "We are far from a deal still", according to Bloomberg.

- US President Trump is set to hold a “One, Big, Beautiful Event” at the White House on Thursday to urge the Senate to pass the reconciliation bill, according to a White House official cited by CBS News.

- Blue Origin and Jeff Bezos reportedly appealed to the White House for more government contracts following Elon Musk’s departure, according to WSJ.

- Meta (META) has reportedly poached three OpenAI researchers – Lucas Beyer, Alexander Kolesnikov, and Xiaohua Zhai, according to WSJ sources.

TRADE/TARIFFS

- Japanese Economy Minister Akazawa said Japan will continue tariff talks with the US ahead of reciprocal tariffs due on July 9th, but cannot accept the 25% auto tariff, according to Reuters.

APAC TRADE

EQUITIES

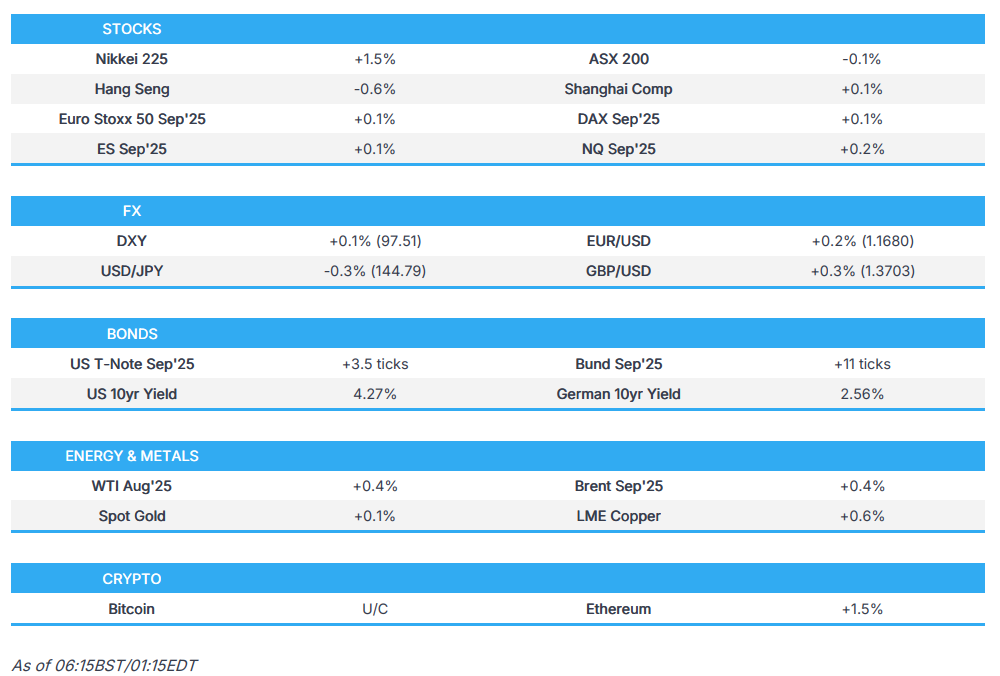

- APAC stocks traded mixed in choppy fashion following a similar session on Wall Street, with overnight newsflow relatively light as Israel and Iran seemingly continued to observe the ceasefire.

- ASX 200 was weighed on by the tech sector despite outperformance in the space stateside. ASX-listed software giant Xero fell over 7% after announcing its intention to purchase payments provider Melio for around USD 3bln.

- Nikkei 225 outperformed and topped the 39k mark for the first time in over a month, led by strong gains in the industrial sector. This came despite a firmer JPY, with market focus turning to the upcoming US-Japan trade talks after local media flagged Japanese Economy Minister Akazawa’s planned visit to Washington as early as June 26th.

- Hang Seng and Shanghai Comp were mixed, while Chinese Premier Li said authorities will take forceful steps to boost consumption. Thereafter, bourses drifter higher as a Chinese state planner official said that with policy implementation and introduction, "we are confident and capable of minimizing the adverse impacts from external shock."

- US equity futures were choppy in a tight range. Some downticks were observed after the WSJ reported that US President Trump may expedite naming a successor to Fed Chair Powell—potentially allowing the chair-in-waiting to influence investor expectations before Powell’s term ends. Thereafter, futures drifted higher after comments from China's state planner, potentially amid cushioning effects for global growth

- European equity futures are indicative of a flat open, with the Euro Stoxx 50 future U/C after the cash index closed 0.9% lower on Wednesday.

FX

- DXY traded choppy with a downward bias, pressured after reports suggested US President Trump may accelerate the process of naming a successor to Fed Chair Powell—potentially allowing the chair-in-waiting to shape investor expectations ahead of Powell’s term expiry. The move was broadly viewed as an attempt to undermine the current Fed Chair. DXY dipped below 97.50 to a multi-year low of 97.27.

- EUR/USD was kept afloat by Dollar softness, with little fresh newsflow for the Single Currency. The pair edged closer to the 1.1700 handle before eventually topping the level, potentially tripping stops along the way given the sudden rise to 1.1717, before stabilising around the round figure.

- GBP/USD was similarly underpinned by the weaker Dollar, with the pair eventually rising above 1.3700.

- USD/JPY was the marginal laggard overnight as US yields pulled back and focus turned to the upcoming US-Japan trade talks. Local media earlier in the week flagged Japanese Economy Minister Akazawa’s visit to Washington as early as June 26th. JPY's strength paused after Akazawa remarked that Japan cannot accept 25% auto tariffs. From a technical perspective, the pair found support near its 21DMA for the past two sessions and then overnight.

- Antipodeans were initially mixed before the aforementioned remarks from the Chinese state planner lifted sentiment in AUD and NZD.

- PBoC set USD/CNY mid-point at 7.1620 vs exp. 7.1561 (prev. 7.1668); strongest CNY fix since Nov 8 2024

- HKMA bought HKD 9.42bln as the Hong Kong dollar hit the weak end of its trading range, marking the first such intervention since 2023 to defend the currency peg.

FIXED INCOME

- 10yr UST futures continued grinding higher in a continuation of the prior day’s price action, with added support from reports that President Trump may accelerate naming a successor to Fed Chair Powell. Tuesday’s solid 5-year auction showed above-average non-dealer buying.

- Bund futures were firmer in tandem with US counterparts, with the German contract reclaiming the 130.50 level as focus turned to upcoming GfK Consumer Sentiment data and a slate of ECB speakers.

- 10yr JGB futures traded in lockstep with Western counterparts, as investors monitored any progress in US-Japan trade talks with Japan’s Finance Minister preparing for meetings in Washington. The 2-year JGB auction prompted some short-lived upticks in the future after drawing the strongest demand ratio since January.

- US sold USD 70bln of 5yr Notes; tails 0.5bps. High Yield: 3.879% (prev. 4.071%, six-auction average 4.183%). WI: 3.874%. Tail: 0.5bps (prev. -0.4bps, six-auction avg. -0.5bps). Bid-to-Cover: 2.36x (prev. 2.39x, six-auction avg. 2.39x). Dealers: 10.9% (prev. 9.2%, six-auction avg. 11.3%). Directs: 24.4% (prev. 12.4%, six-auction avg. 18.2%). Indirects: 65.7% (prev. 78.4%, six-auction avg. 70.5%).

- Japan sold JPY 2.6tln 2-year JGBs; b/c 3.90x (prev. 3.70x), and average yield 0.729% (prev. 0.752%) - draws strongest demand ratio since January.

COMMODITIES

- Crude futures tilted higher despite a lack of fresh headlines, with the Israel–Iran ceasefire seemingly holding as no new hostilities were reported from either side. During the futures close, Al Arabiya reported that “Iranian defences shot down an unknown drone over the border strip with Iraq,” though no further details were provided.

- Spot gold traded horizontally around the same levels seen during Wednesday’s APAC session, with newsflow on the quieter side. Traders looked ahead to the US Q1 GDP final reading, weekly Jobless Claims, and several scheduled Fed speakers.

- Copper futures eventually tilted higher after Chinese Premier Li said authorities would take forceful steps to boost consumption, and a Chinese state planner official said that with policy implementation and introduction, "we are confident and capable of minimizing the adverse impacts from external shock."

- Goldman Sachs upgraded its H2 2025 LME copper price forecast to an average of USD 9,890/t (prev. USD 9,140/t), citing a tariff-driven reduction in ex-US stocks and resilient activity in China. The bank expects copper to peak at USD 10,050/t in 2025, before easing to USD 9,700/t by December. For 2026, it forecasts an average copper price of USD 10,000/t (prev. USD 10,170/t), reaching USD 10,350/t.

- Russia is open to a new output hike if OPEC+ decides that it's needed, Bloomberg reports.

CRYPTO

- Bitcoin held an upward bias as it traded on either side of USD 108k.

NOTABLE ASIA-PAC HEADLINES

- Chinese state planner official said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters.

- The PBoC injected CNY 509.3bln via 7-day reverse repos, maintaining the rate at 1.40%.

- Citi raised its China 2025 GDP growth outlook to 5.0% (prev. 4.7%).

DATA RECAP

- South Korean Composite Business Sentiment Index (Jun) 90.2 (Prev. 90.7)

GEOPOLITICS

- Iranian defences shot down an unknown drone over the border strip with Iraq, according to Al Arabiya; the incident occurred over the border area of Siba in southern Iraq, according to Al Hadath.

- CIA Director said the CIA can confirm that credible intelligence indicated Iran’s nuclear programme had been severely damaged by recent strikes. Several key Iranian nuclear facilities had been destroyed and would have to be rebuilt over the course of years, according to Reuters.

- US President Trump called on Israeli Prime Minister Netanyahu’s domestic trial to be cancelled immediately and for him to be granted a pardon, via Truth Social.

- The Pentagon released a document outlining FY26 weapons requests, including funding for 24 F-35 warplanes and two submarines, according to Reuters.

EU/UK

NOTABLE HEADLINES

- Shell’s (SHEL LN) spokesperson said that no talks were taking place regarding market speculation that Shell was considering buying BP (BP/ LN). This followed reports by the WSJ that Shell had held early talks to acquire BP, and subsequent reporting by CNBC sources indicating that BP could be split in a sale and was unlikely to be bought outright.

DATA RECAP

- Citi/YouGov: UK public inflation expectations for 5-10 years ahead 4.3% in June (prev. 4.2% in May)

LATAM

- Brazil's lower house and Senate voted to overturn the presidential decree hiking the financial transactions tax, according to Reuters.

- Brazil’s lower house of Congress approved an extra pre-salt oil auction to boost revenue, according to Reuters.