US Market Open: DXY hit on reports that Trump may name Powell successor early, US equity futures gain slightly into data

26 Jun 2025, 11:23 by Newsquawk Desk

- US President Trump may accelerate the announcement of a successor to Fed Chair Powell, according to WSJ sources.

- Chinese state planner official said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters.

- Micron (MU) said there may have been some tariff-related pull-ins by certain customers; customer inventory levels have been healthy overall across end markets.

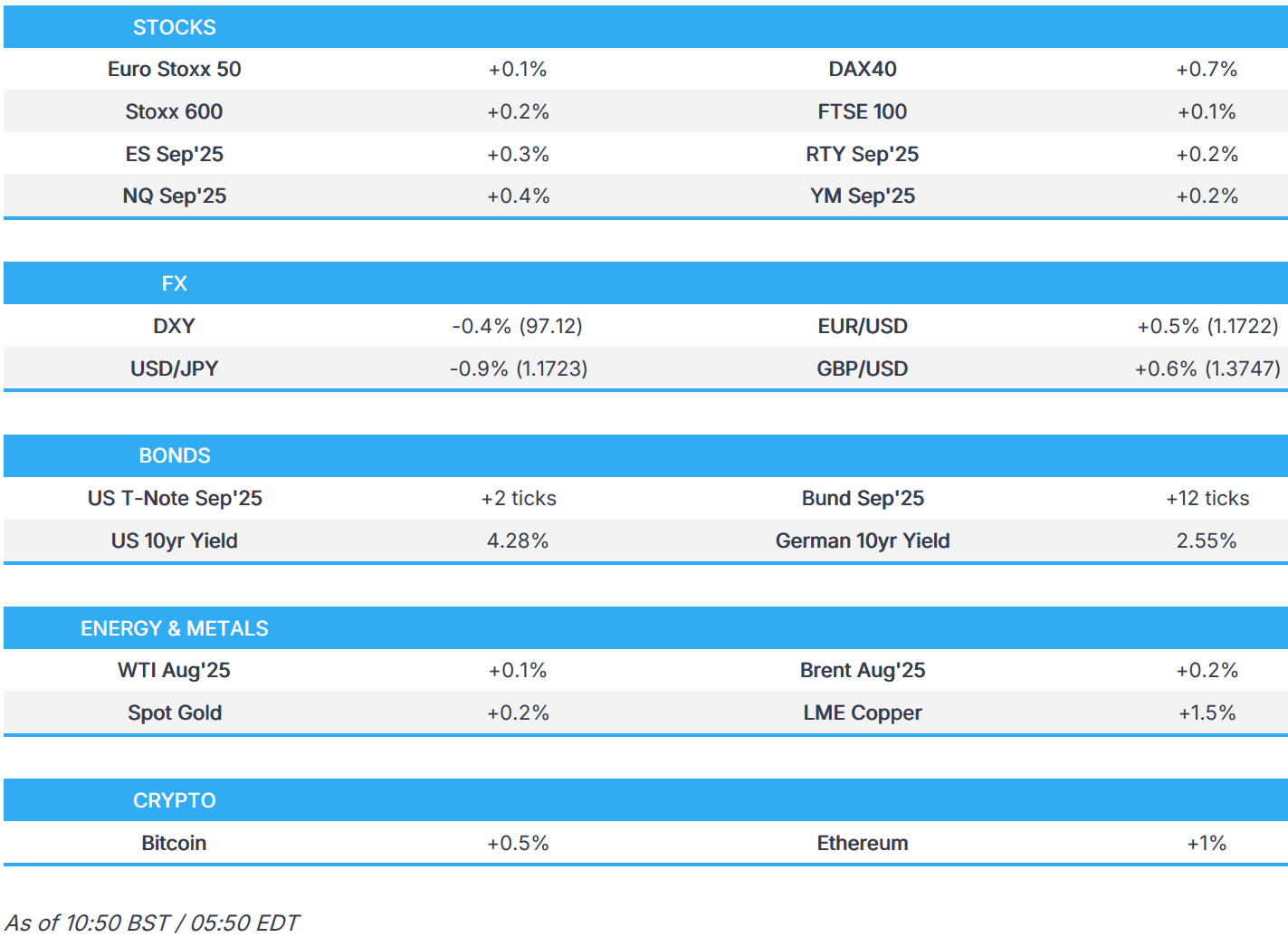

- European & US indices trade modestly higher, ES +0.3%; Shell has “no intention” of making an offer for BP.

- DXY hammered amid reports Trump is to name a Powell successor early; a report which has also weighed on US yields.

- Crude trims initial gains, metals glean strength from the dovish Fed source report, USD weakness and Chinese commentary.

- Looking ahead, US Durable Goods, GDP Final (Q1), PCE (Q1), Jobless Claims, National Activity Index, Advance Goods Trade Balance, Wholesale Inventories, Banxico Policy Announcement, ECB’s de Guindos, Schnabel, Lagarde; BoE’s Bailey; Fed’s Daly, Barkin, Hammack, Barr, Kashkari, Supply from the US, Earnings from Walgreens, Nike.

TRADE/TARIFFS

- Japanese Economy Minister Akazawa said Japan will continue tariff talks with the US ahead of reciprocal tariffs due on July 9th, but cannot accept the 25% auto tariff, according to Reuters.

- India and US trade talks face roadblocks ahead of the tariff deadline, according to Reuters citing sources; India is resisting tariff cuts without US commitments; delegation is exp. to travel to US before deadline.

- Chinese authorities are dragging out approval of Western companies’ requests for rare earths, two weeks after the nation said it would ease exports, according to WSJ.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) are generally modestly firmer across the board, following a mixed and choppy APAC session overnight. Though it is worth noting that price action (aside from the DAX 40) has been quite choppy and within a tight range so far.

- European sectors hold a positive bias, in-fitting with the broadly positive mood in European indices. Basic Resources takes the top spot, lifted by strength in metals prices following positive commentary from Chinese Premier Li and the State Planner; the latter said that with policy implementation and introduction, they are confident in minimising adverse effects from external shocks. Retail is found in the second spot, buoyed by post-earning strength in H&M (+5.2%).

- US equity futures (ES +0.3% NQ +0.4% RTY +0.2%) are modestly higher across the board, in-fitting with the cautiously optimistic risk tone seen in Europe; focus now turns to a slew of US data and Fed speak.

- Shell (SHEL LN) says it has no intention of making an offer for BP (BP/ LN).

- JPMorgan raises 2025 YE target for MSCI Emerging Markets index to 1,250 (prev. saw 1,150, currently ~1,225).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is on the back foot for the fourth consecutive day, and currently trades towards the lower end of a 96.93-60 range – the index now trades at levels not seen since March 2022. Overnight reporting suggested that US President Trump may accelerate the announcement of a successor to Fed Chair Powell, possibly as early as this summer, or in September or October, according to WSJ sources. A slew of US data later, including US PCE (Q1), GDP Final (Q1), Jobless Claims and Durable Goods. Fed speak today via Daly, Barkin, Hammack, Barr and Kashkari.

- EUR/USD continues to benefit from the broader Dollar weakness and currently trades above 1.17; session peak at 1.1744. EZ-specific docket has been exceptionally light today; German GfK Consumer Sentiment printed a touch below expectations, no reaction on this.

- JPY is the G10 outperformer today, largely thanks to the pullback in US yields overnight and broader Dollar weakness. USD/JPY has fallen below both its 21 DMA (144.50) and 50 DMA (144.27) to currently trade below the 144.00 mark at around 143.83. Overnight, upside in the JPY was briefly capped on reports that Japanese Economy Minister Akazawa said Japan will continue tariff talks with the US ahead of reciprocal tariffs due on July 9th, but cannot accept the 25% auto tariff.

- GBP also benefits from the Dollar weakness and trades at multi-year highs, and marginally topped its 2022 high at 1.3749. Beyond that, there is a little bit of clear air up until the 1.3800 mark, whereby the high from Oct 29 2021, at 1.3804 may be in focus. UK-specific newsflow has been very light so far, but docket ahead includes BoE's Bailey.

- Antipodeans are modestly benefitting from the Dollar weakness, but also amid some positive commentary out of China overnight – remarks which helped to boost base metals also. Firstly, the Chinese State Planner said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters. Secondly, Premier Li said authorities will take forceful steps to boost consumption. Lastly, Citi raised its China 2025 GDP growth outlook to 5.0% (prev. 4.7%).

- PBoC set USD/CNY mid-point at 7.1620 vs exp. 7.1561 (prev. 7.1668); strongest CNY fix since Nov 8 2024

- HKMA bought HKD 9.42bln as the Hong Kong dollar hit the weak end of its trading range, marking the first such intervention since 2023 to defend the currency peg.

- South African President Ramaphosa is reportedly considering a cabinet reshuffle, via News24 citing sources; this could involve Deputy Trade Minister Whitfield and Minister Nkabane. USD/ZAR lifted from 17.62 to 17.70 on speculation of, and since source reporting around, a potential cabinet reshuffle.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer, benefitting from the WSJ reports that President Trump could announce the next Fed Chair much earlier than is traditionally the case. Trump himself has intimated he has the list down to a handful of individuals; unsurprisingly, all those on the WSJ list are or are expected to err on the dovish side of things. USTs to a 111-28 peak thus far, notching another best for the month and now to within a point of the 112-23 peak from May, but of course still a significant distance from the mark. Ahead, 7yr supply rounds off the week’s taps, which have gone well thus far. US data and Fed speak is also due.

- Bunds are also bid, in-fitting with the above. A bout of upside was seen at 07:00BST, from 130.62 to 130.74 in the space of two-three minutes. Upside that occurred alongside a soft German GfK survey, a release that shows that while the government’s fiscal support is aiding business expectations this is yet to filter through to the individual consumer level. Since, Bunds have continued to climb and peaked at 130.80 before experiencing a modest pullback as the morning continued and the risk tone continues to improve. Action that has caused Bunds to pullback from the above high by around 15 ticks, but remain in the green by a similar magnitude. Ahead, the docket features ECB speak from heavyweights Lagarde, de Guindos and Schnabel.

- Gilts gapped higher by 14 ticks and then continued to climb, above Wednesday’s 93.38 open to a 93.45 high for today; just shy of Tuesday’s 93.51 peak and 92.57 from Wednesday thereafter. Ahead, the docket is sparse and as such Gilts will likely follow the narrative of US events, particularly anything further on the Fed Chair, and speeches from the ECB and Fed.

- UK sells GBP 1.0bln 4.25% 2046 Gilt, via tender: b/c 1.99x, average yield 5.162%.

- Click for a detailed summary

COMMODITIES

- WTI and Brent began the European morning on the front foot, taking impetus from the softer USD and improving risk tone. Drivers that were sufficient to lift WTI and Brent to peaks of USD 65.57/bbl and USD 67/08/bbl, respectively. However, as the morning progressed and despite or perhaps in-part because of the lack of newsflow the benchmarks have lost ground with WTI now below USD 65.00/bbl and threatening a move into the red.

- Spot gold is firmer given the softer USD and lower yield environment on the back of the WSJ-Fed report around an early Fed Chair nominee announcement. A move that has been interpreted as one to undermine the authority of Chair Powell, with a dovish move occurring on the back of it given the list of potential nominees all fall on that side of the hawk-dove discussion. XAU itself gleaning some further impetus on the narrative that the undermining of Chair Powell draws into question the Fed's credibility and/or independence. XAU up to a USD 3350/oz peak, firmer but yet to approach USD 3369/oz or USD 3398/oz from Tuesday and Monday.

- 3M LME copper is firmer, benefiting from the increasingly constructive risk tone and the discussed USD pressure. Sentiment boosted by China-related headlines overnight; Firstly, the Chinese State Planner said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters. Secondly, Premier Li said authorities will take forceful steps to boost consumption. Lastly, Citi raised its China 2025 GDP growth outlook to 5.0% (prev. 4.7%).

- Citi reaffirms its Brent forecast of USD 66/bbl and USD 63/bbl for Q3- and Q4-2025, respectively

- Goldman Sachs upgraded its H2 2025 LME copper price forecast to an average of USD 9,890/t (prev. USD 9,140/t), citing a tariff-driven reduction in ex-US stocks and resilient activity in China. The bank expects copper to peak at USD 10,050/t in 2025, before easing to USD 9,700/t by December. For 2026, it forecasts an average copper price of USD 10,000/t (prev. USD 10,170/t), reaching USD 10,350/t.

- Click for a detailed summary

NOTABLE DATA RECAP

- German GfK Consumer Sentiment (Jul) -20.3 vs. Exp. -19.3 (Prev. -19.9, Rev. -20.0)

- Swedish Total Industry Sentiment (Jun) 94.8 (Prev. 98.9); Sentiment (Jun) 92.8 (Prev. 94.6)Manufacturing Confidence (Jun) 99.3 (Prev. 100.1); Consumer Confidence SA (Jun) 84.6 (Prev. 83.1)

NOTABLE US HEADLINES

- US President Trump may accelerate the announcement of a successor to Fed Chair Powell, possibly as early as this summer, or in September or October, according to WSJ sources. The move could allow the nominee to shape investor expectations before Powell’s term ends. Potential candidates include: Former Fed Governor Kevin Warsh, National Economic Council Director Kevin Hassett, Treasury Secretary Scott Bessent, Former World Bank President David Malpass, and Fed Governor Christopher Waller.

- Micron (MU) Q3 2025 (USD): Adj. EPS 1.91 (exp. 1.60), Revenue 9.3bln (exp. 8.81bln), Adj. net income 2.2bln (exp. 1.8bln); strong Q4 guidance. Q4 adj. EPS view 2.35-2.65 (exp. 1.97). Q4 revenue view 10.4-11bln (exp. 9.89bln). Fiscal Q4 revenue is projected to grow another 15% sequentially. Co. said there may have been some tariff-related pull-ins by certain customers; customer inventory levels have been healthy overall across end markets. Shares +0.9% after hours.

- US Republican Representative Lalota said, in reference to SALT, "We are far from a deal still", according to Bloomberg.

- US President Trump is set to hold a “One, Big, Beautiful Event” at the White House on Thursday to urge the Senate to pass the reconciliation bill, according to a White House official cited by CBS News.

- Blue Origin and Jeff Bezos reportedly appealed to the White House for more government contracts following Elon Musk’s departure, according to WSJ.

- Meta (META) has reportedly poached three OpenAI researchers – Lucas Beyer, Alexander Kolesnikov, and Xiaohua Zhai, according to WSJ sources.

- BlackRock (BLK) is increasing its push into private investments, via WSJ; intends to offer a 401(k) target date fund with a 5-20% allocation to private investments, depending on investor age, in H1-2026.

- US Senate Republicans are reportedly considering delaying cuts to Medicaid in a bid to win over more moderate holdouts from the party, who threaten progress of the Reconciliation Bill, via Punchbowl.

GEOPOLITICS

- Al-Akhbar reports that another round of talks between Israel and Hamas is expected within the next few days, according to Egyptian sources cited; Hamas is reportedly ready to release all hostages in exchange for Israeli commitments

- Iranian defences shot down an unknown drone over the border strip with Iraq, according to Al Arabiya; the incident occurred over the border area of Siba in southern Iraq, according to Al Hadath.

- CIA Director said the CIA can confirm that credible intelligence indicated Iran’s nuclear programme had been severely damaged by recent strikes. Several key Iranian nuclear facilities had been destroyed and would have to be rebuilt over the course of years, according to Reuters.

- US President Trump called on Israeli Prime Minister Netanyahu’s domestic trial to be cancelled immediately and for him to be granted a pardon, via Truth Social.

- The Pentagon released a document outlining FY26 weapons requests, including funding for 24 F-35 warplanes and two submarines, according to Reuters.

CRYPTO

- Bitcoin is a little firmer and trades just above USD 107k whilst Ethereum also gains but still shy of USD 2.5k.

APAC TRADE

- APAC stocks traded mixed in choppy fashion following a similar session on Wall Street, with overnight newsflow relatively light as Israel and Iran seemingly continued to observe the ceasefire.

- ASX 200 was weighed on by the tech sector despite outperformance in the space stateside. ASX-listed software giant Xero fell over 7% after announcing its intention to purchase payments provider Melio for around USD 3bln.

- Nikkei 225 outperformed and topped the 39k mark for the first time in over a month, led by strong gains in the industrial sector. This came despite a firmer JPY, with market focus turning to the upcoming US-Japan trade talks after local media flagged Japanese Economy Minister Akazawa’s planned visit to Washington as early as June 26th.

- Hang Seng and Shanghai Comp were mixed, while Chinese Premier Li said authorities will take forceful steps to boost consumption. Thereafter, bourses drifter higher as a Chinese state planner official said that with policy implementation and introduction, "we are confident and capable of minimizing the adverse impacts from external shock."

NOTABLE ASIA-PAC HEADLINES

- Chinese state planner official said with policy implementation and introduction, "we are confident and capable of minimising the adverse impacts from external shock", according to Reuters.

- The PBoC injected CNY 509.3bln via 7-day reverse repos, maintaining the rate at 1.40%.

- Citi raised its China 2025 GDP growth outlook to 5.0% (prev. 4.7%).

- Chinese Commerce Ministry (on rare earth export licenses for EU firms) says it has been accelerating development of rare earth export licenses in accordance with the law

DATA RECAP

- South Korean Composite Business Sentiment Index (Jun) 90.2 (Prev. 90.7)