Europe Market Open: EU receives latest US trade proposal, European indices set to open higher

27 Jun 2025, 06:43 by Newsquawk Desk

- US President Trump said he just signed a deal with China on Wednesday; it was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement.

- US Commerce Secretary Lutnick stated that several deals will be announced in the coming week, with the Europe deal expected at the end.

- Iranian Foreign Minister Araqchi said Tehran is assessing whether diplomacy with the US is in its interest, adding that there is currently no understanding for renewed talks with the US.

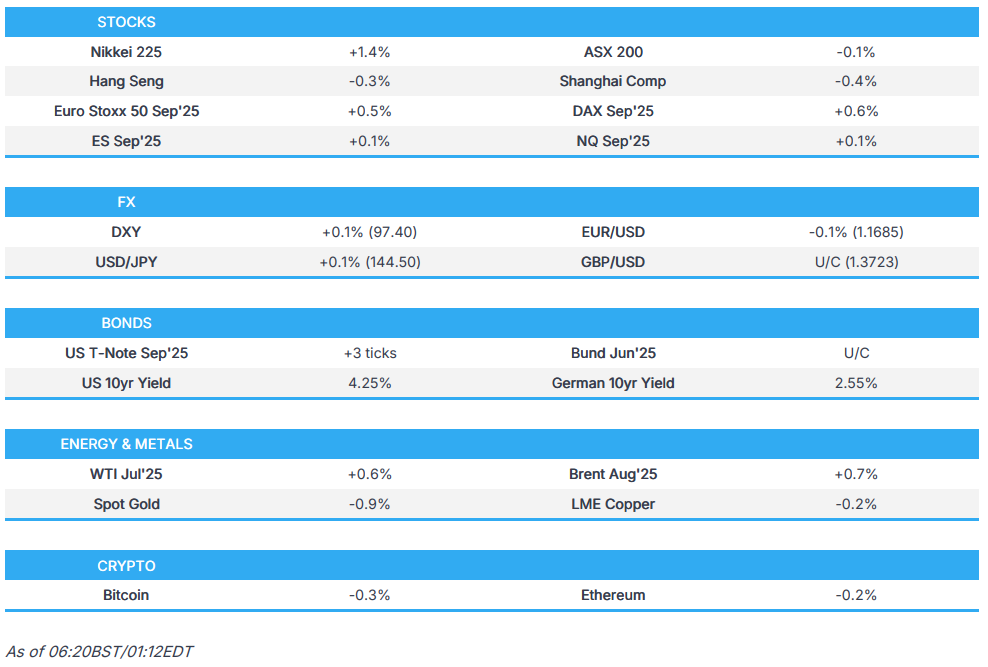

- APAC stocks traded mostly firmer for a bulk of the session following gains on Wall Street, before waning off best levels to trade mixed.

- European equity futures are indicative of a firmer open - catching up to some of the late Wall Street gains - with the Euro Stoxx 50 future +0.5% after cash closed -0.2% on Thursday.

- Looking ahead, highlights include French CPI, Spanish HICP, Retail Sales, EZ Business Climate, Italian Industrial Sales, US PCE, UoM Survey Final, Fed’s Williams, Hammack; ECB's Cipollone, and Supply from Italy.

- Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks were bid on Thursday to see SPX hover around record highs while NDX pushed above record highs.

- SPX +0.85% at 6,144, NDX +0.94% at 22,447, DJI +0.94% at 43,387, RUT +1.60% at 2,170

- Click here for a detailed summary.

NOTABLE HEADLINES

- US President Trump to appear on Fox News on Sunday morning.

- US Treasury Secretary Bessent said they have asked the Senate and House to remove the Section 899 protective measure from consideration in the "One, Big, Beautiful Bill". Bessent also said that following dialogue with other countries on the OECD global tax deal, the US will announce a joint understanding among G7 countries that defends American interests. He added that OECD Pillar 2 taxes will not apply to US companies, according to Reuters.

- US Senate Parliamentarians have struck a "massive blow" to Republican Medicaid cuts, via Punchbowl's Weiss citing Senate Budget Democrats; ruled that it is not compliant with the Byrd Rule.

- US Senate Republicans are reportedly going to attempt to rework the "provider" tax to retain it within the Reconciliation bill, via Politico's Carney citing sources; Republicans state that a vote on Friday remains a possibility.

- US lawmakers said they would remove Section 899 from the tax bill, according to Reuters.

- Nike Inc (NKE) Q4 2025 (USD): GAAP EPS 0.14 (exp. 0.12), Revenue 11.097bln (exp. 10.66bln), Net income 211mln (exp. 185.9mln), Pretax profit 318mln (exp. 233.5mln). Inventory 7.49bln (exp. 7.17bln). Q4 reflected the largest financial impact for its Win Now actions, and expect headwinds to moderate from here.Shares rose 10.7% after hours.

TRADE/TARIFFS

- US President Trump said he just signed a deal with China on Wednesday, according to Reuters, and says he has one maybe coming up with India. Trump added that China is starting to open up. It was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement, according to a White House official cited by Fox’s Lawrence. A second Administration official confirmed that the framework finalises what was agreed in London and also addresses Chinese export controls, according to a source familiar with the agreement.

- European Commission President von der Leyen told EU leaders that the EU executive received the latest counterproposal from the Trump administration today, according to two EU diplomats cited by POLITICO. This marks the latest engagement between Brussels and Washington, as the EU is coming to terms with potentially having to accept an agreement that still includes a “reciprocal”.

- European Commission President von der Leyen said the EU received the latest US proposal today and is prepared for both a deal and a no-deal outcome, stating all options remain on the table.

- EU reportedly considers lowering tariffs on US imports in a bid to woo US President Trump, via WSJ citing sources. "The European Union is considering lowering tariffs on a range of US imports in a bid to clinch a speedy trade deal with President Trump, according to people familiar with the matter." "EU leaders are set to debate how much they are willing to sacrifice to win over Trump at a meeting in Brussels on Thursday evening. Other concessions under consideration include lowering nontariff barriers, buying more American products including liquefied natural gas, and offering to cooperate with the US to tackle its economic concerns about China."

- French President Macron said he favours a speedy and fair EU–US trade deal, but warned that if the US maintains a 10% tariff, Europe would have to apply equivalent compensatory measures.

- White House Press Secretary Leavitt said the 9th July deadline for trade deals is not critical; trade deadline change would be Trump's decision. Trump can pick a reciprocal tariff rate if deals fail, according to Reuters.

- US chip export curbs may slow China's adoption of Deepseek's next model, R2, via The Information.

- US Commerce Secretary Lutnick said tax bill passage is expected within the next week or two, adding that the China deal was "signed and sealed" two days ago. Lutnick stated that several deals will be announced in the coming week, with the Europe deal expected at the end. He noted that although Europe had a sluggish start, it is now performing excellently and there is optimism about a deal with the EU. Countries seeking further negotiations are welcome, and all nations will be categorised into appropriate tariff groups by the 9 July deadline for reciprocal tariff agreements. He added that the US is close to finalising a deal with India and that the tariff programme will not need to change if the bill is adjusted.

- German Chancellor Merz said von der Leyen proposed the creation of a new European trade organisation, and added that EU leaders are largely united on finalising the Mercosur trade deal.

APAC TRADE

EQUITIES

- APAC stocks traded mostly firmer for a bulk of the session following gains on Wall Street amid expectations of a future Fed Chair more aligned with the President. Sentiment was further supported after US President Trump announced he had signed a deal with China on Wednesday. Although initial reports were unclear and caused some confusion, White House officials later clarified that the signing finalised what had previously been agreed upon in Geneva and London. China has not yet confirmed the signing of the deal. APAC stocks later waned off best levels to trade mixed.

- ASX 200 was supported by the broader mood, with the rise in copper keeping miners propped up before paring back.

- Nikkei 225 outperformed across the region, buoyed by recent JPY weakness and a softer-than-expected Tokyo Core CPI reading, which could temper some of the recent hawkish rhetoric from BoJ’s Tamura.

- Hang Seng and Shanghai Comp opened with modest gains, drawing some support from US President Trump’s announcement of a signed deal with China. It was later clarified the deal finalised prior agreements made in Geneva and London, though China has yet to confirm the signing. Chinese bourses later turned flat.

- US equity futures gradually edged higher ahead of Friday’s PCE data. Meanwhile, Nike shares surged 10.7% post-earnings, with traders citing “turnaround hopes.”

- European equity futures are indicative of a firmer open - catching up to some of the late Wall Street gains - with the Euro Stoxx 50 future +0.5% after cash closed -0.2% on Thursday.

FX

- DXY was flat for the bulk of the session in quiet trade ahead of the upcoming PCE release — the Fed’s preferred inflation gauge. The index later dipped to session lows despite a lack of newsflow, but as EUR/USD mounted 1.1700. DXY traded within a 97.23–97.41 range after finding support at 97.00 on Thursday.

- EUR/USD was choppy around the 1.1700 handle amid a lack of fresh newsflow during APAC hours and ahead of preliminary CPI prints from France and Spain, which typically influence the EUR. On the trade front, European Commission President von der Leyen confirmed the EU received the latest US document for further negotiations, but warned that all options remain on the table, stating: “We are ready for a deal; at the same time, we are preparing for the possibility of no deal.”

- GBP/USD gradually edged up towards 1.3750 from a 1.3717 base, with UK-specific newsflow quiet overnight. Focus turns to UK Q1 GDP, though key April GDP Estimate metrics were already released on June 12th.

- USD/JPY initially outperformed a softer JPY, with the pair underpinned by weaker-than-expected Tokyo CPI and Japanese Retail Sales figures. USD/JPY reclaimed its 50DMA at 144.32 to hit a peak of 144.80 before retreating back towards session lows as the USD weakened.

- Antipodeans eventually tilted modestly higher as the USD weakened despite the indecisive risk tone and a lack of catalysts. A contraction in Chinese Industrial Profits did little to help sentiment for AUD or NZD at the time.

- PBoC set USD/CNY mid-point at 7.1627 vs exp. 7.1771 (prev. 7.1620)

FIXED INCOME

- 10yr UST futures took a breather after the prior day’s gains, where T-notes remained largely unfazed despite a relatively weak 7-year note auction ahead of Thursday settlement. Market focus now turns to the US Core PCE metrics.

- Bund futures were flat and uneventful, with newsflow light during APAC hours. Traders now eye preliminary CPI prints from France and Spain in early European trade, which could introduce some volatility.

- 10yr JGB futures saw choppy trade within tight ranges. Some initial upside followed the softer-than-expected Tokyo CPI metrics, but gains were later trimmed. Meanwhile, Japanese Finance Minister Kato said they will continue cautious consideration of potential buybacks of previously issued bonds.

- US sells USD 44bln of 7yr notes; Stop through 0.2bps. High Yield: 4.022% (prev. 4.194%, six-auction average 4.289%); WI 4.024%. Tail: -0.2bps (prev. -2.2bps, six-auction avg. -0.9bps). Bid-to-Cover: 2.53x (prev. 2.69x, six-auction avg. 2.64x). Dealers: 11.64% (prev. 4.8%, six-auction avg. 10.1%). Directs: 11.62% (prev. 23.6%, six-auction avg. 21.0%). Indirects: 76.74% (prev. 71.5%, six-auction avg. 68.8%).

COMMODITIES

- Crude futures continued the choppy trade seen on Thursday, with newsflow from Israel and Iran considerably quieter amid the ceasefire. Some optimism for crude may have stemmed from US President Trump’s announcement that the US signed a deal with China on Wednesday — though the agreement appeared to finalise what was previously settled in Geneva and London.

- Spot gold was subdued with newsflow quiet, and the yellow metal remained capped by the lack of fresh geopolitical updates following the flurry of headlines earlier in the month prior to the Israel–Iran ceasefire. Traders looked ahead to the upcoming US Core PCE data.

- Copper futures gave up some of the earlier optimism linked to US-China headlines, with the red metal later aligning with the broader indecisive and cautious market tone ahead of the July 9th US reciprocal tariff deadline.

- The US Energy Department announced that scheduled oil deliveries into the Strategic Petroleum Reserve will be delayed until December, due to maintenance at SPR sites. Of the 15.8mln barrels originally planned through May, only 8.8mln have been delivered so far.

- Goldman Sachs said Brent crude could reach USD 90/bbl by year-end in a Strait of Hormuz disruption scenario, while options markets see a 60% chance Brent stays in the USD 60s in 3 months and a 28% chance it exceeds USD 70.

CRYPTO

- Bitcoin tilted higher during APAC trade and eventually rose above USD 107.5k.

NOTABLE ASIA-PAC HEADLINES

- The PBoC injected CNY 525.9bln via 7-day reverse repos, maintaining the rate at 1.40%.

- Japanese Finance Minister Kato said they will continue cautious consideration of potential buybacks of previously issued bonds, according to local Reuters.

- The South Korean government held an emergency meeting on household debt, and plans to strengthen measures to control it, according to the financial regulator.

DATA RECAP

- Chinese Industrial Profit YTD (May) -1.1% (Prev. 1.4%).

- Japanese CPI Tokyo Ex fresh food YY (Jun) 3.1% vs. Exp. 3.3% (Prev. 3.6%)

- Japanese CPI, Overall Tokyo (Jun) 3.1% (Prev. 3.4%)

- Japanese Retail Sales YY (May) 2.2% vs. Exp. 2.7% (Prev. 3.3%, Rev. 3.5%)

- Japanese Jobs/Applicants Ratio (May) 1.24 vs. Exp. 1.26 (Prev. 1.26)

CENTRAL BANKS

- Fed's Collins (2025 voter) said July is probably too early for a rate cut; the baseline outlook is to resume cutting later this year. The Fed has time to carefully evaluate incoming information, according to Reuters.

- Fed Governor Barr (voter) said monetary policy is well positioned to wait and see how economic conditions unfold, stressing the importance of bringing inflation back to target as low-income households are most vulnerable to price increases. He warned that tariffs will exert upward pressure on inflation with some persistence, while potentially slowing the economy and increasing unemployment. Barr noted that low-income workers are often the hardest hit during job market downturns and that there remains considerable uncertainty regarding tariff policies and their effects.

- Fed’s Kashkari (2026 voter) said independent monetary policy generally leads to lower inflation and a better labour market, noting the Fed strives to base decisions on data and analysis rather than politics. He stated inflation remains above the 2% target and must be brought back down, while the labour market is still strong and not "falling off a cliff."

- Bloomberg article highlighted the majority of Fed officials are leaning against a July interest rate cut - citing recent commentary.

- US President Trump said it would be helpful if the Fed lowered rates; on Fed Chair Powell, Trump said "We have to fight this guy"

- Banxico cut rates by 50bps to 8.00% as expected, and stated that looking ahead, the board will assess further adjustments to the reference rate — a shift from its previous guidance that it could continue the calibrating policy and consider adjustments in similar magnitudes.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Minister Araqchi said Tehran is assessing whether diplomacy with the US is in its interest, adding that there is currently no understanding for renewed talks with the US. Araqchi dismissed speculation about the resumption of negotiations with the US, saying it should not be taken seriously. There are no plans to receive IAEA Chief Grossi in Tehran, according to Reuters.

- Iran’s representative to the UN said Tehran is open to forming a regional nuclear consortium and exchanging uranium in the event of an agreement with Washington, via Sky News Arabia.

- Trump admin has discussed possibly helping Iran access as much as USD 30bln to build a civilian-energy-producing nuclear programme, easing sanctions, and freeing up billions of dollars in restricted Iranian funds, according to CNN sources. All that is part of an intensifying attempt to bring Tehran back to the negotiating table.

- An explosion occurred at the “Aluf” plant within a complex belonging to the Iranian defence industries in the Republic of Azerbaijan, according to Al Hadath.

- Israeli Prime Minister Netanyahu agreed with US President Trump to end the Gaza war within two weeks, according to Al Arabiya citing Israeli press.

- Israeli Defence Minister warned of further strikes on Iran if it resumes nuclear development, according to Al Arabiya.

RUSSIA-UKRAINE

- EU leaders agreed to renew existing Russia sanctions for another six months, according to Reuters.

EU/UK

NOTABLE HEADLINES

- ECB's Knot, when asked about market expectations of one more 25bps cut by the end of the year, Knot said that possibility was “difficult for me to exclude”, via FT.

LATAM

- Brazil Treasury Secretary Ceron said Congress' reversal of the IOF tax increase will have a significant impact in 2025 and 2026, adding that the government has 2 to 3 weeks to define what the budget solution will be, according to Reuters.

- Moody's cuts Colombia's rating to Baa3 from Baa2; outlook stable.

- S&P downgraded Colombia’s sovereign credit rating to BB from BB+ with a negative outlook, citing weaker fiscal performance.