US Market Open: European bourses benefit on US-EU trade optimism, DXY lower & US equity futures gain into PCE

27 Jun 2025, 11:00 by Newsquawk Desk

- US Commerce Secretary Lutnick stated that several deals will be announced in the coming week, with the Europe deal expected at the end.

- Punchbowl reports that Republican Senators say voting on the Reconciliation Bill will not begin until Saturday at the absolute earliest.

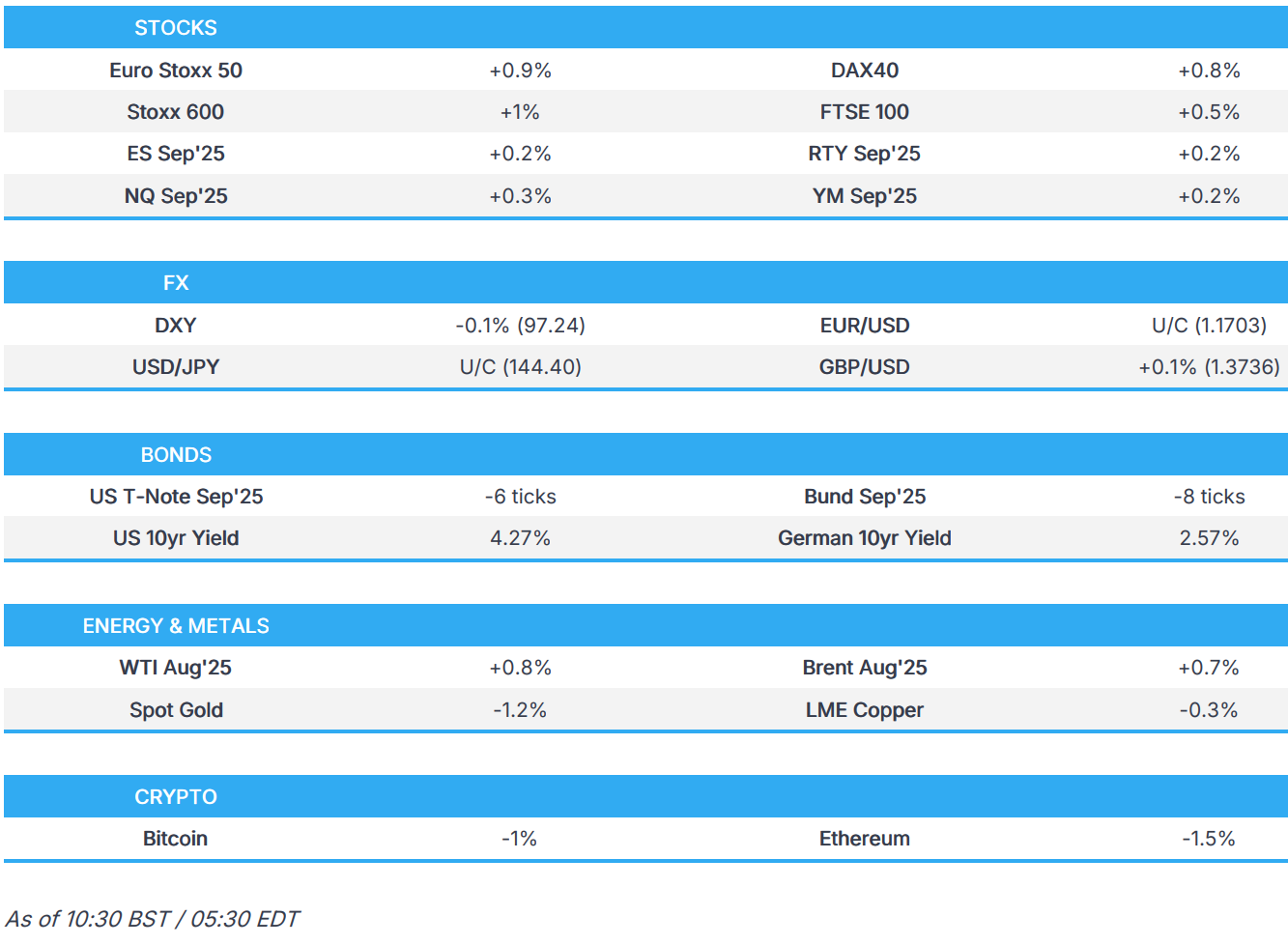

- European bourses benefit from a flurry of US-EU trade updates, US futures gain modestly into PCE.

- DXY extends its losing streak for a fifth session as PCE looms.

- USTs are under modest pressure with Bunds also hampered following French/Spanish inflation figures.

- Crude is firmer & XAU slips given the risk tone but base metals fail to benefit.

- Looking ahead, US PCE, UoM Survey Final, Fed’s Williams, Hammack; ECB's Cipollone.

TRADE/TARIFFS

- US President Trump said he just signed a deal with China on Wednesday, according to Reuters, and says he has one maybe coming up with India. Trump added that China is starting to open up. It was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement, according to a White House official cited by Fox’s Lawrence. A second Administration official confirmed that the framework finalises what was agreed in London and also addresses Chinese export controls, according to a source familiar with the agreement.

- China issues a statement on trade framework with US; two sides confirmed details on framework China will approve export applications for controlled items in accordance with the law. Both sides maintained close communications after meetings in London. The US side will accordingly lift a series of restrictive measures taken against China.

- European Commission President von der Leyen said the EU received the latest US proposal today and is prepared for both a deal and a no-deal outcome, stating all options remain on the table.

- French President Macron said he favours a speedy and fair EU–US trade deal, but warned that if the US maintains a 10% tariff, Europe would have to apply equivalent compensatory measures.

- US chip export curbs may slow China's adoption of DeepSeek’s next model, R2, via The Information.

- US Commerce Secretary Lutnick said tax bill passage is expected within the next week or two, adding that the China deal was "signed and sealed" two days ago. Lutnick stated that several deals will be announced in the coming week, with the Europe deal expected at the end. He noted that although Europe had a sluggish start, it is now performing excellently and there is optimism about a deal with the EU. Countries seeking further negotiations are welcome, and all nations will be categorised into appropriate tariff groups by the 9 July deadline for reciprocal tariff agreements. He added that the US is close to finalising a deal with India and that the tariff programme will not need to change if the bill is adjusted.

- German Chancellor Merz said von der Leyen proposed the creation of a new European trade organisation, and added that EU leaders are largely united on finalising the Mercosur trade deal.

- Chinese Foreign Ministry says Yi will travel to EU headquarters June 30th for China-EU high-level strategic dialogue; will also visit Germany and France.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +1%) opened with a strong positive bias and continued to trudge higher as the morning progressed – currently trading at session highs.

- Sentiment over the past couple of days has been boosted by; 1) Thursday’s report that Trump is looking to announce Powell’s replacement early, 2) WSJ reports that the EU is considering lowering tariffs on US imports in a bid to woo US President Trump, 3) von der Leyen suggesting the EU had received the latest US trade proposal – stressing that whilst they are ready for a deal, they have made preparations for no deal.

- European sectors are entirely in the green. Autos leads, followed by Consumer Products as the likes of Adidas (+4%) and Puma (+5%) benefit from Nike's post-earning strength.

- US equity futures (ES +0.2%, NQ +0.3%, RTY +0.2%) are modestly firmer across the board, taking impetus from a strong European morning but with gains capped ahead of the US PCE later today.

- Nike (+9.5% pre-market) signalled that the sales slump is bottoming out, and CEO's turnaround strategy gained investor support following an upbeat earnings call, reversing some of the stock’s recent declines.

- EU antitrust regulators says Meta (META) will only make limited changes to pay-or-consent mode; cannot say whether changes are sufficient to comply with EU rules; EU to consider next steps, including daily fines for non-compliance starting June 27th

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has extended its losing streak to a fifth session as a combination of geopolitical tensions easing, declining yields, concerns over Fed independence and ongoing fiscal concerns act as a drag on the greenback. Over the past 24 hours, the trade agenda has reasserted itself on the market narrative after US President Trump said he signed a deal with China on Wednesday; it was later clarified that the US and China have agreed to an additional understanding to implement the Geneva agreement. DXY is currently contained within Thursday's 96.99-97.60 range, into US PCE and a couple of Fed speakers.

- EUR is firmer vs. the USD amid some encouragement on the trade front for the EU. This comes after the WSJ reported that the EU is reportedly considering lowering tariffs on US imports in a bid to woo US President Trump. Furthermore, US Commerce Secretary Lutnick said that although Europe had a sluggish start, it is now performing excellently and there is optimism about a deal with the EU. That being said, European Commission President von der Leyen said the EU is prepared for both a deal and a no-deal outcome, stating all options remain on the table. EUR/USD currently trading around 1.1715.

- JPY is still struggling to make much headway vs. the USD relative to other peers with Japanese data overnight acting as a headwind for the Yen. National inflation data for June came in soft on a headline and core basis (retail sales were also weak). USD/JPY is currently tucked within Thursday's 143.75-145.26 range and sat just above its 50DMA at 144.32.

- GBP is a touch firmer vs. the USD and steady on a 1.37 handle. It has been a week lacking in fresh macro drivers for the UK and that remains the case. There has been some attention on the political scene with UK PM Starmer facing a possible rebellion from his own MPs over proposed welfare cuts. Cable is currently tucked below Thursday's multi-year high at 1.3770.

- Antipodeans are both marginally stronger vs. the USD alongside the positive risk tone and subsequently shrugging off a contraction in Chinese Industrial Profits. Both currencies are also likely being underpinned by the aforementioned developments between the US and China on the trade front. Albeit, details remain light at this stage.

- PBoC set USD/CNY mid-point at 7.1627 vs exp. 7.1771 (prev. 7.1620)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained/slightly softer start to the day for USTs. Benchmark pulling back from Thursday’s 112-03 MTD high, but only marginally with the current trough at 111-26+, comfortably clear of Thursday’s 111-21 base. Focus overnight has been on the latest US-China framework agreement, but essentially just firming the prior Geneva/London talks. Focus today now turns to US PCE and a couple of Fed speakers.

- Bunds are in-fitting with the above. Under modest pressure in the European morning into the region's first inflation figures for June. Before those, no reaction to ECB’s Knot who said to the FT that the possibility of a 25bps cut by end-2025 was "difficult for me to exclude”. To recap those HICP metrics, French figures were hotter-than-expected across the board sparking a modest hawkish reaction. Specifically, this sent Bunds down from near the 130.66 high to around 130.44. Spanish figures were a little more mixed, but also held a hawkish skew, taking Bunds to a fresh low of 130.20.

- Gilts opened higher by a few ticks and then extended a handful more to 93.36, catching up to the late-Thursday performance for USTs/Bunds, before conforming to the broader bias and slipping slightly. However, action has been minimal with Gilts comfortably above the 93.00 mark and shy of today and Thursday’s open at 93.32.

- Italy sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 2.70% 2030, 2.95% 2030 & 3.60% 2035 BTP and EUR vs exp. EUR 1.5-2.0bln 2034 CCTeu.

- Click for a detailed summary

COMMODITIES

- Crude is on a firmer footing today, in what has been a session lacking of pertinent geopolitical updates; more focus on US-China / US-EU trade updates, but details are light at the moment. Price action has been relatively steady throughout the morning, awaiting US PCE later. Brent Aug'25 currently trading around USD 67.20/bbl.

- Spot gold trades with a downward bias, and fails to benefit from the slightly softer Dollar and seemingly continuing to be weighed upon by the relatively calm in the Middle East; currently sits below USD 3.3k/oz.

- 3M LME Copper is unable to benefit from the risk tone. However, while softer, 3M LME Copper is holding onto essentially all of the upside it derived on Monday when it rose by near USD 200 to a USD 9.91k peak. As it stands, the base metal has slipped just below the USD 9.9k mark, but remains on track to close out the week with strong gains after opening it at USD 9.65k.

- The US Energy Department announced that scheduled oil deliveries into the Strategic Petroleum Reserve will be delayed until December, due to maintenance at SPR sites. Of the 15.8mln barrels originally planned through May, only 8.8mln have been delivered so far.

- Goldman Sachs said Brent crude could reach USD 90/bbl by year-end in a Strait of Hormuz disruption scenario, while options markets see a 60% chance Brent stays in the USD 60s in 3 months and a 28% chance it exceeds USD 70.

- Shanghai Warehouse Stocks: Copper -19.26k/T (prev. -1.1k).

- Click for a detailed summary

NOTABLE DATA RECAP

- French CPI (EU Norm) Prelim MM (Jun) 0.4% vs. Exp. 0.2% (Prev. -0.2%); Prelim YY (Jun) 0.8% vs. Exp. 0.7% (Prev. 0.6%)

- French CPI Prelim YY NSA (Jun) 0.9% vs. Exp. 0.7% (Prev. 0.7%); French CPI Prelim MM NSA (Jun) 0.3% vs. Exp. 0.1% (Prev. -0.1%)

- French Producer Prices YY (May) 0.2% (Prev. -0.8%); MM (May) -0.8% (Prev. -4.3%, Rev. -4.2%)

- French Consumer Spending MM (May) 0.2% vs. Exp. 0.1% (Prev. 0.3%, Rev. 0.5%)

- Spanish HICP Flash YY (Jun) 2.2% vs. Exp. 2.0% (Prev. 2.0%); Flash MM (Jun) 0.6% vs. Exp. 0.6% (Prev. 0.0%)

- Spanish CPI MM Flash NSA (Jun) 0.6% vs. Exp. 0.40% (Prev. 0.10%); YY Flash NSA (Jun) 2.2% vs. Exp. 2.0% (Prev. 2.0%); Core 2.2% (prev. 2.2%)

- Spanish Retail Sales YY (May) 4.8% (Prev. 4.0%)

- Italian Manufacturing Business Confidence (Jun) 87.3 vs. Exp. 87.0 (Prev. 86.5, Rev. 86.6); Confidence (Jun) 96.1 vs. Exp. 97.0 (Prev. 96.5)

- EU Selling Price Expec (Jun) 5.6 (Prev. 7.9, Rev. 7.7); Cons Infl Expec (Jun) 21.2 (Prev. 23.6); Consumer Confid. Final (Jun) -15.3 vs. Exp. -15.3 (Prev. -15.3); Services Sentiment (Jun); 2.9 vs. Exp. 1.6 (Prev. 1.5, Rev. 1.8); Economic Sentiment (Jun) 94.0 vs. Exp. 95.1 (Prev. 94.8); Industrial Sentiment (Jun) -12.0 vs. Exp. -9.9 (Prev. -10.3, Rev. -10.4).

NOTABLE EUROPEAN HEADLINES

- ECB's Knot, when asked about market expectations of one more 25bps cut by the end of the year, Knot said that possibility was “difficult for me to exclude”, via FT.

- German minimum wage to increase to EUR 14.60/hr by 2027; will take place via two steps from current level of EUR 12.82.

- ECB's de Guindos says the ECB is on track to meet its 2% inflation target

NOTABLE US HEADLINES

- On whether the US Reconcilliation Bill can be sent to President Trump by the July 4th deadline, Punchbowl surmises that it is possible, but is becoming increasingly difficult; Senators say voting will not being until Saturday at the absolute earliest. "...one key holdout said they’re far from the point when Trump will be needed to help close a deal." Senators say voting will not being until Saturday at the absolute earliest, with that viewed as optimistic. Senate parliamentarian ruling focused on "the provider tax freeze in the bill rather than the Senate’s more drastic constraints for Medicaid expansion states, according to two sources with knowledge of the decision". Republicans believe they can come up with a fix. President Trump has reportedly told multiple GOP senators privately that he prefers the House’s provider tax framework, which is much less drastic than the Senate’s version.

- US lawmakers said they would remove Section 899 from the tax bill, according to Reuters.

- US DOGE Service has sent staff to the Bureau of Alcohol, Tobacco, Firearms and Explosives with the goal of revising or eliminating dozens of rules and gun restrictions by July 4th, via WaPo citing sources.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Minister Araqchi said Tehran is assessing whether diplomacy with the US is in its interest, adding that there is currently no understanding for renewed talks with the US. Araqchi dismissed speculation about the resumption of negotiations with the US, saying it should not be taken seriously. There are no plans to receive IAEA Chief Grossi in Tehran, according to Reuters.

- Iran’s representative to the UN said Tehran is open to forming a regional nuclear consortium and exchanging uranium in the event of an agreement with Washington, via Sky News Arabia.

- An explosion occurred at the “Aluf” plant within a complex belonging to the Iranian defence industries in the Republic of Azerbaijan, according to Al Hadath.

- Israeli Prime Minister Netanyahu agreed with US President Trump to end the Gaza war within two weeks, according to Al Arabiya citing Israeli press.

- Israeli Defence Minister warned of further strikes on Iran if it resumes nuclear development, according to Al Arabiya.

RUSSIA-UKRAINE

- EU leaders agreed to renew existing Russia sanctions for another six months, according to Reuters.

CRYPTO

- Bitcoin is slightly lower and trades around USD 106.5k; Ethereum posts slightly deeper losses.

CENTRAL BANKS

- Fed’s Kashkari (2026 voter) said independent monetary policy generally leads to lower inflation and a better labour market, noting the Fed strives to base decisions on data and analysis rather than politics. He stated inflation remains above the 2% target and must be brought back down, while the labour market is still strong and not "falling off a cliff."

- US President Trump said it would be helpful if the Fed lowered rates; on Fed Chair Powell, Trump said "We have to fight this guy"

- Banxico cut rates by 50bps to 8.00% as expected, and stated that looking ahead, the board will assess further adjustments to the reference rate — a shift from its previous guidance that it could continue the calibrating policy and consider adjustments in similar magnitudes.

APAC TRADE

- APAC stocks traded mostly firmer for a bulk of the session following gains on Wall Street amid expectations of a future Fed Chair more aligned with the President. Sentiment was further supported after US President Trump announced he had signed a deal with China on Wednesday. Although initial reports were unclear and caused some confusion, White House officials later clarified that the signing finalised what had previously been agreed upon in Geneva and London. China has not yet confirmed the signing of the deal. APAC stocks later waned off best levels to trade mixed.

- ASX 200 was supported by the broader mood, with the rise in copper keeping miners propped up before paring back.

- Nikkei 225 outperformed across the region, buoyed by recent JPY weakness and a softer-than-expected Tokyo Core CPI reading, which could temper some of the recent hawkish rhetoric from BoJ’s Tamura.

- Hang Seng and Shanghai Comp opened with modest gains, drawing some support from US President Trump’s announcement of a signed deal with China. It was later clarified the deal finalised prior agreements made in Geneva and London, though China has yet to confirm the signing. Chinese bourses later turned flat.

NOTABLE ASIA-PAC HEADLINES

- The PBoC injected CNY 525.9bln via 7-day reverse repos, maintaining the rate at 1.40%.

- Japanese Finance Minister Kato said they will continue cautious consideration of potential buybacks of previously issued bonds, according to local Reuters.

- The South Korean government held an emergency meeting on household debt, and plans to strengthen measures to control it, according to the financial regulator.

- Li Auto (2015 HK) expects to deliver circa 108k vehicles in Q2 (vs. May 29th guidance of 123-128k).

DATA RECAP

- Chinese Industrial Profit YTD (May) -1.1% (Prev. 1.4%).

- Japanese CPI Tokyo Ex fresh food YY (Jun) 3.1% vs. Exp. 3.3% (Prev. 3.6%)

- Japanese CPI, Overall Tokyo (Jun) 3.1% (Prev. 3.4%)

- Japanese Retail Sales YY (May) 2.2% vs. Exp. 2.7% (Prev. 3.3%, Rev. 3.5%)

- Japanese Jobs/Applicants Ratio (May) 1.24 vs. Exp. 1.26 (Prev. 1.26)