US Market Open: US futures bolstered as Reconciliation Bill progresses, however July tariff deadline looms

30 Jun 2025, 11:55 by Newsquawk Desk

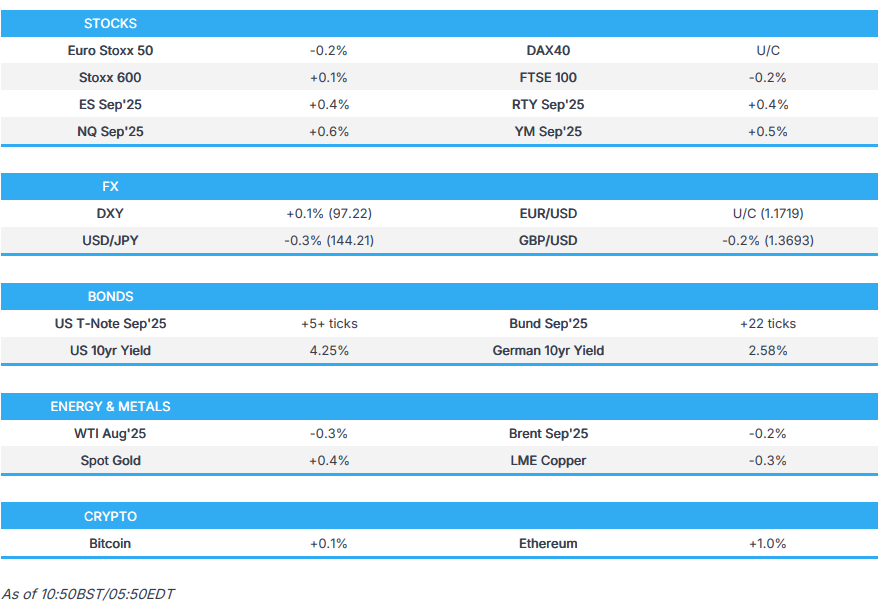

- A firmer start to the week Stateside, ES +0.4%, as markets focus on the progress of Trump's Bill; however, Europe is more contained, Stoxx 600 +0.1%, as the reciprocal deadline nears.

- US Senate voted to begin debating the Reconciliation Bill; vote-a-rama not expected to start until 09:00ET today, as such the House will not vote until Wednesday at the earliest, via Fox's Pergram.

- DXY has kicked off week-, month-, quarter- & H1-end on a mildly negative footing, though the magnitude of this has dissipated across the morning. EUR contained, JPY outperforms, GBP softer.

- Fixed benchmarks were contained overnight before EGBs picked up on numerous German data points.

- Crude benchmarks are in the red but only modestly so, updates continue on the geopolitical front, with Trump saying he is not offering Iran anything.

- Looking ahead, highlights include US Chicago PMI, Speakers including ECB’s de Guindos & Lagarde, Fed’s Bostic & Goolsbee.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- US President Trump announced on Friday that the US is stopping trade talks with Canada due to the latter putting a digital services tax on US tech companies. However, it was reported a few days later that Canada rescinded the Digital Services Tax to advance broader trade negotiations with the US, while PM Carney and US President Trump agreed that parties will resume negotiations with a view towards agreeing on a deal by July 21st.

- US President Trump said in an interview with Fox Business News, which aired on Sunday, that Japan takes in no American cars and its vehicles should be subject to a 25% auto tariff in the US.

- UK government said the UK-US trade deal has today come into force, slashing US export tariffs for the UK's automotive and aerospace sectors, while it added that UK car manufacturers can now export to the US under a reduced 10% tariff quota and that 10% tariffs on goods like aircraft engines and aircraft parts are removed with a commitment to maintain them at 0%.

- Canada acted to support its steel producers and workers in which it set new tariff rate quotas for steel mill product imports from non-FTA partners.

- China Customs said it resumed imports of qualified aquatic products from some Japanese regions.

- Indonesia is to ease import restrictions on some goods including forestry products, plastic materials and some fertilisers, while it offered the US to jointly invest in the Brownfield Project of critical minerals in Indonesia as part of tariff talks.

- Bank for International Settlements said the global economy and financial system have entered a new era of heightened uncertainty, while it added that rising protectionism and trade fragmentation are particularly concerning.

- EU Competition Commissioner Ribera say, on a EU-US deal, “We will not compromise … around sovereignty and around regulation on how to work in our own market,”, via Politico citing excerpts from The Capitol Forum.

- Japan's Tariff negotiator says they will continue working with the US to reach a tariff agreement, while defending national interests. Continuation of 25% auto tariffs would cause significant damage.

EUROPEAN TRADE

EQUITIES

- European bourses kicked off the first trading session of the week with modest gains following the upside on Wall Street, in which the sentiment reverberated into APAC markets before reaching Europe; Stoxx 600 +0.1%. However, gains are modest and benchmarks are gradually dipping into the red with traders cognisant of the looming July 9th reciprocal deadline.

- Sectors opened firmer with just Energy in the red, though the picture since has become more mixed but with the breadth of price action narrow. Focus on reports that US tariff policies coupled with low river levels are causing the worst supply chain congestion since COVID, according to FT. Issues at the ports of Rotterdam, Antwerp, and Hamburg are expected to last for several months.

- Stateside, futures in the green, ES +0.4%, NQ +0.5%; supported by compromises on the trade and fiscal fronts. Banks are firmer in the pre-market after they cleared Fed stress tests late-Friday. Docket ahead dominated by speakers, Treasury Secretary Bessent, Fed's Bostic & Goolsbee all before POTUS' latest executive order signing.

- UK CMA says Boeing (BA)/Spirit AeroSystems (SPR) merger deadline is August 28th for phase 1 decision.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has commenced the week, month-end, quarter-end and half-year-end off on a mildly negative footing after a run of five consecutive losses last week. Down to a 96.97 low at worst, while the benchmark remains in the red it has managed to reclaim the figure, but remains shy of the earlier 97.299 peak. For reference, the mentioned session low is another multi-year trough.

- EUR contained. EUR/USD faded out initial gains, peaked at 1.1750, just before Friday's 1.1753 multi-year peak. Focus on the inflation front, though no significant move to German State or Italian prelim CPI thus far, with near term focus firmly on the trade agenda.

- JPY tops the G10 leaderboard. USD/JPY as low as 143.79, is now back to the 144.00 mark but someway shy of the 144.76 peak.

- Sterling marginally softer vs both the EUR and USD. Incremental drivers for the UK light, though today sees the UK-US deal come into force. Cable currently contained within Friday's 1.3683-1.3752 range.

- Antipodeans benefitting from the constructive risk tone and after the PBoC set a firmer Yuan reference rate overnight.

- PBoC set USD/CNY mid-point at 7.1586 vs exp. 7.1681 (Prev. 7.1627).

- South Africa’s DA Party leader said the Democratic Alliance will withdraw from national dialogue with immediate effect and is in the process of losing confidence in the President’s ability to lead the government.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Contained overnight ahead of a busy and front-loaded week. Focus remains firmly on the trade and fiscal fronts; awaiting the reciprocal deadline and monitoring the Reconciliation Bills Senate passage respectively.

- While pertinent, the above developments have not changed the macro picture just yet with USTs in the green by just a handful of ticks within a narrow 111-22 to 112-00+ band, a range that is almost a repeat of Friday’s 111-22+ to 112-02 parameter.

- Bunds are firmer on the session, began in the green and lifted on the morning's German data points of Import Prices and Retail Sales. Thereafter, State CPIs printed and while the metrics were mixed the overall skew was cooler-than-previous, defying consensus for a mainland uptick, lifting Bunds to a 130.52 peak.

- Gilts in the green as well, largely following suit to the above price action in Bunds and USTs. Newsflow lighter domestically as the scale of Labour rebellion to PM Starmer’s Welfare Bill appears to have moderated significantly after the u-turn on Friday. While firmer, Gilts remain shy of the 93.36 peak on Friday and by extension last week’s 93.57 high.

- Spanish Economy Minister says we should work to increase the supply of EUR-denominated assets such as joint EU debt issued to finance defence spending.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks in the red but only modestly so with losses of c. USD 0.20/bbl, after a slightly choppy morning. Began the APAC session subdued given an absence of significant weekend newsflow. This morning, prices found a floor shortly after US President Trump posted that he is not offering Iran anything, and is not talking to Iran since destroying their nuclear sites.

- WTI resides in a USD 64.50-65.45/bbl range while its Brent counterpart trades in a USD 65.92-66.87/bbl range.

- Spot gold is firmer amid the Dollar softness and ahead of upcoming risk events. XAU stopped just shy of USD 3,300/oz this morning after rising from a USD 3,244/oz base.

- Copper futures are subdued with a similar performance to APAC seen in Europe amid the mixed risk appetite; overnight, the latest Chinese PMI data showed Manufacturing PMI remained in contraction territory despite the US-China trade truce, possibly also weighing on sentiment for the red metal.

- Israel’s Oil Refineries said it resumed partial operation of refining activity in Haifa after damage caused by an Iranian missile during the Israel-Iran war, with full operation expected by October.

- Smoke arose from Iran’s Tabriz refinery, which was caused by a nitrogen tank explosion, although there were no casualties from the incident.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Lloyds Business Barometer (Jun) 51 (Prev. 50); highest since 2015.

- UK GDP QQ (Q1) 0.7% vs. Exp. 0.7% (Prev. 0.7%); YY 1.3% vs. Exp. 1.3% (Prev. 1.3%)

- German Import Prices YY (May) -1.1% vs. Exp. -0.8% (Prev. -0.4%); MM (May) -0.7% vs. Exp. -0.4% (Prev. -1.7%)

- German Retail Sales MM Real (May) -1.6% vs. Exp. 0.5% (Prev. -1.1%); YY 1.6% vs. Exp. 3.3% (Prev. 2.3%)

- Swiss KOF Indicator (Jun) 96.1 vs. Exp. 99.3 (Prev. 98.5, Rev. 98.6)

- German State CPIs: Overall, the metrics were somewhat mixed with Baden Wurttemberg coming in above the prior as did the lower-Saxony M/M, prints that are in-fitting with the forecast for an uptick in the mainland figures. However, the other metrics came in cooler than the prior with the M/M for Bavaria and North Rhine-Westphalia both negative prints (-0.1%).

- UK Mortgage Approvals (May) 63.032k vs. Exp. 59.75k (Prev. 60.463k, Rev. 60.656k); Lending 2.054B GB vs. Exp. 2.5B GB (Prev. -0.759B GB, Rev. -0.776B GB)

- UK M4 Money Supply (May) 0.2% (Rev. -0.1%)

NOTABLE EUROPEAN HEADLINES

- UK launches the biggest financial advice shakeup in more than a decade with the regulator unveiling plans for targeted support to help individuals get better returns, according to FT.

- ECB's de Guindos says they are confronting "brutal uncertainty"; Q2, Q3 growth will be almost flat; Consumption as a driver has not happened; must keep all rate options open because of uncertainty.

- ECB updates its monetary policy strategy: Governing Council confirms symmetric 2% inflation target over the medium term; Symmetry requires appropriately forceful or persistent policy response to large, sustained deviations of inflation from target in either direction; all tools remain in toolkit and their choice, design and implementation will enable an agile response to new shocks; structural shifts such as geopolitical and economic fragmentation and increasing use of artificial intelligence make the inflation environment more uncertain.

NOTABLE US HEADLINES

- US President Trump’s sweeping tax cut and spending bill cleared the first US Senate hurdle on Saturday with a 51-49 vote to open the debate on the bill, which raises the odds of passage in the coming days, while US President Trump commented that there was a great victory in the Senate with the “great big, beautiful bill”.

- Non-partisan US Congressional Budget Office said the Senate version of the Trump tax bill will add USD 3.3tln to US debt over the next decade.

- Elon Musk posted on X that the latest Senate draft bill will destroy millions of jobs in America and cause immediate strategic harm to the country, while he added it is utterly insane and destructive, as well as gives out handouts to industries of the past while severely damaging industries of the future.

- Fox's Pergram says "Senate not expected to begin vote-a-rama until 9 am et on Big, Beautiful Bill. Most vote-a-ramas run 9 to 15 hours. House not expected to vote until Wednesday at the earliest"

- Fed Stress Test results on Friday showed large banks are well-positioned to weather a severe recession in 2025, and that all 22 banks passed.

- US President Trump posts "ONE GREAT BIG BEAUTIFUL BILL, is moving along nicely!".

- US President Trump posts "The Trump Administration has gotten costs down, very substantially, for the American Consumer. There has never been anything like this!"

- Fed's Bostic (2027 voter, Hawk) says this could be a more extended [pause] period than people think, via CNBC. Businesses tell the Fed they don't have plans to lay people off. There is some optimism amongst business leaders

GEOPOLITICS

MIDDLE EAST

- Israel’s army said it identified the launch of a missile from Yemen on Saturday.

- Egyptian Foreign Minister said work is underway on an upcoming agreement in Gaza that includes a 60-day truce, according to Alhadath via X.

- US President Trump said Israeli PM Netanyahu is in the process of negotiating a deal with Hamas to get hostages back.

- US President Trump said he knew exactly where Iran’s Supreme Leader Khamenei was sheltered and would not let Israel or US armed forces terminate his life, while Trump said he demanded that Israel bring back a very large group of planes that were headed directly to Tehran in the final act of the war. Furthermore, Trump said he was working on the possible removal of sanctions in the last few days and other things which would have given Iran a much better chance at a recovery but warned that Iran has to get back into the world order flow or things will only get worse for them.

- US justified its strikes on Iran as collective self-defence under the UN Charter in a letter to the UN Security Council and said the objective was to destroy Iran’s nuclear enrichment capacity and stop the threat that Tehran obtains and uses a nuclear weapon, while it added that the US remains committed to pursuing a deal with the Iranian government.

- IAEA chief Grossi said Iran has the capacity to start enriching uranium again for a possible bomb in a matter of months, according to BBC.

- Iran’s Foreign Minister said if US President Trump is genuine about wanting a deal, he should put aside the disrespectful and unacceptable tone towards Iran’s Supreme Leader.

- Iran’s Armed Forces Chief of Staff Mousavi told Saudi Arabia’s Defence Minister that they highly doubt Israel’s commitment to the ceasefire, according to Tasnim.

- Iran permitted the transiting of international flights over the centre and west of the country. In relevant news, Emirates cancelled all flights to and from Tehran until July 5th due to the regional situation, while it is to recommence operations to Baghdad on July 1st and Basra on July 2nd.

- US President Trump says he is not offering Iran anything, and is not talking to Iran since destroying their nuclear sites.

- "A source involved in the negotiations for a ceasefire in Gaza told the pro-Qatari news website Arabi 21 this morning that it is believed that an Israeli delegation will arrive in Cairo in the next two days", according to Israeli Radio's Kai.

- Iran's MFA spokesperson Baghaei says Iran and the EU have not agreed on a date for the next round of discussions. Talks are ongoing with the E3.

RUSSIA-UKRAINE

- Russia said its troops captured Novoukrainka in eastern Ukraine, according to RIA.

- US President Trump said on Friday that he may send patriot missiles to Ukraine and commented that he will get the conflict solved with North Korea’s leader Kim.

OTHER

- India’s Ministry of External Affairs said they have seen and rejected the official statement by the Pakistan Army seeking to blame India for the attack in Waziristan on June 28th.

CRYPTO

- A firmer start for Bitcoin, continuing the bullish trend that has been in play over the last eight sessions. However, BTC is yet to reapproach the USD 11k mark from early-June.

APAC TRADE

- APAC stocks began the week mostly in the green following last Friday's record highs on Wall St but with some of the gains capped heading into month-end and as participants digested a slew of data including somewhat mixed Chinese PMIs.

- ASX 200 edged higher with strength in the defensive sectors but with upside limited by data including softer-than-expected private sector credit.

- Nikkei 225 outperformed despite disappointing Industrial Production data which showed a surprise Y/Y contraction and with the index also unfazed by recent comments from US President Trump who noted that Japanese vehicles should be subject to a 25% auto tariff in the US.

- Hang Seng and Shanghai Comp were mixed following the latest PMI data which showed headline Manufacturing PMI remained in contraction territory, as expected, although Non-Manufacturing PMI accelerated at a faster pace than forecast.

NOTABLE ASIA-PAC HEADLINES

- US officials are drawing up plans for US President Trump’s state visit to China later this year with a delegation of dozens of CEOs, according to Nikkei.

- US President Trump said they have a buyer for TikTok and that it is a group of very wealthy people.

- Canada’s Industry Minister ordered Hikvision (002415 CH) to cease all operations and close its business in the country after a national security review.

- Japanese government official said regarding factory output that sentiment among manufacturers is worsening over uncertainties in the production environment and the number of firms concerned about the impact of US tariffs on production and shipments slightly increased in May from April.

DATA RECAP

- Chinese NBS Manufacturing PMI (Jun) 49.7 vs. Exp. 49.7 (Prev. 49.5); Non-Mfg PMI (Jun) 50.5 vs. Exp. 50.3 (Prev. 50.3)

- Chinese Composite PMI (Jun) 50.7 (Prev. 50.4)

- Japanese Industrial Production MM SA (May P) 0.5% vs. Exp. 3.5% (Prev. -1.1%); YY SA (May P) -1.8% vs. Exp. 1.6% (Prev. 0.5%)

- Australian Private Sector Credit (May) 0.5% vs Exp. 0.7% (Prev. 0.7%)

- New Zealand ANZ Business Outlook (Jun) 46.3% (Prev. 36.6%); Own Activity (Jun) 40.9% (Prev. 34.8%)