Europe Market Open: Europe primed for a quiet open with the EU to accept Trump’s universal tariff while seeking sectoral exemptions

01 Jul 2025, 06:50 by Newsquawk Desk

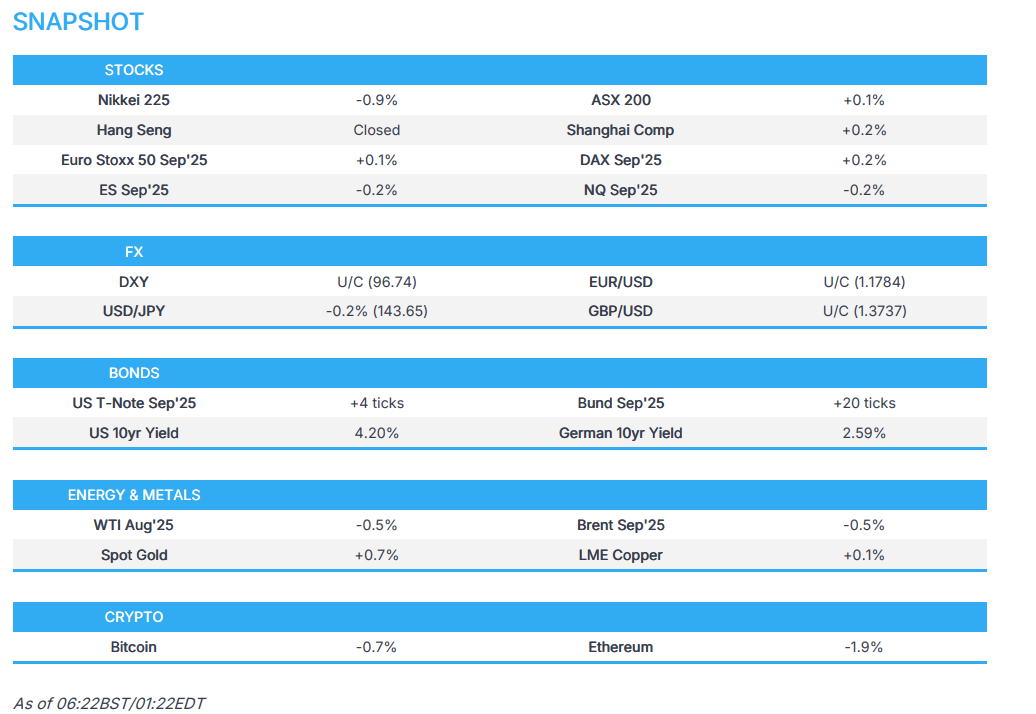

- APAC stocks began the new quarter mostly higher, albeit with gains tentative; Wall Street closed higher.

- The Senate vote-a-rama process is ongoing before a final version is sent back to the House to approve the bill, before then sending it to Trump's desk.

- EU is to accept Trump’s universal tariff but seeks key exemptions and wants the US to commit to lower rates on key sectors, according to Bloomberg.

- European equity futures indicate an uneventful cash market open with Euro Stoxx 50 future +0.1% after the cash market closed with losses of 0.4% on Monday.

- DXY is steady, EUR/USD briefly ventured onto a 1.18 handle, USD/JPY marginally extended on its downside.

- Looking ahead, highlights include EZ, UK & US Manufacturing PMIs, German Unemployment Rate, EZ HICP, US ISM Manufacturing, JOLTS Job Openings, ECB SCE & Central Banking Forum, Speakers include ECB’s de Guindos, Elderson, Schnabel & Lagarde, Fed’s Powell, BoJ's Ueda, BoE’s Bailey & BoK's Rhee.

SNAPSHOT

US TRADE

EQUITIES

- US stocks gained and the major US indices ended the month and quarter on the front foot as Apple (+2%) provided tailwinds amid reports that the tech behemoth reportedly weighs powering Siri with Anthropic or OpenAI tech. Nonetheless, the focus on Monday was on events at Capitol Hill with the Senate clearing a key hurdle in Trump's tax bill, with the vote-a-rama process now ongoing before a final version is sent back to the House to approve the bill before then sending it to Trump's desk. In addition, Trump continued to pile on the pressure on "Too Late" Powell, who participates in a conference with BoE's Bailey, ECB's Lagarde, and BoJ's Ueda on Tuesday. The Dollar was lower and sold off through the duration of the US session to the benefit of G10 peers (ex. GBP), while T-Notes bull flattened amid month/quarter-end, soft Chicago PMI and Bessent dialling back expectations he will term out the debt.

- SPX +0.52% at 6,205, NDX +0.64% at 22,679, DJI +0.63% at 44,095, RUT +0.12% at 2,175.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said they will be sending Japan a letter after not accepting US rice despite a rice shortage and commented that "we love having them as a Trading Partner for many years to come."

- White House Press Secretary said President Trump is meeting with the trade team this week to set country rates, while she said we will hear about a trade deal with India very soon.

- US narrows trade focus to secure deals, while officials were seeking phased deals with the most engaged countries as they race to find agreements by July 9th, according to FT.

- Japan's Chief Cabinet Secretary Hayashi said Japan won't do anything to sacrifice the agricultural sector in US trade talks, while Farm Minister Koizumi said he won't comment on US President Trump's posts regarding Japan's rice imports.

- EU is to accept Trump’s universal tariff but seeks key exemptions and it wants the US to commit to lower rates on key sectors such as pharmaceuticals, alcohol, semiconductors and commercial aircraft, while it is pushing for quotas and exemptions to effectively lower a 25% tariff on automobiles and car parts as well as a 50% tariff on steel and aluminium, according to Bloomberg.

- UK is currently planning to keep its digital services tax, according to Bloomberg sources.

NOTABLE HEADLINES

- US President Trump said "Jerome “Too Late” Powell, and his entire Board, should be ashamed of themselves for allowing this to happen to the US... We should be paying 1% Interest, or better!"

- White House Press Secretary Leavitt said high interest rates remain a problem and that President Trump sent a handwritten note to Fed Chair Powell asking Powell to lower rates, while Leavitt also commented she will not get ahead of President Trump about naming a potential Powell successor.

- Fed's Goolsbee (2025 voter) does not see any prospect of 1970s-style stagflation, while he said there is definitely the possibility of both inflation and employment getting worse at the same time.

- Goldman Sachs now expects the Federal Reserve to deliver three 25bp rate cuts in 2025, beginning in September, compared to its previous forecast of one cut in December.

- US House Rules Committee will meet on Tuesday at noon to consider the reconciliation package, according to Punchbowl.

APAC TRADE

EQUITIES

- APAC stocks began the new quarter mostly higher, albeit with gains capped amid this week's busy data calendar and with underperformance in Japan owing to recent currency strength.

- ASX 200 treaded water with the index just about kept afloat as strength in defensives offset the losses in the mining and materials sectors.

- Nikkei 225 underperformed as exporters suffered the ill effects of recent currency strength and with the predominantly better-than-expected BoJ Tankan survey increasing the scope for a more hawkish BoJ, while US President Trump also noted they will be sending Japan a letter regarding tariffs after not accepting US rice.

- Shanghai Comp edged mild gains after Chinese Caixin Manufacturing PMI topped forecasts with a surprise return to expansionary territory, although the upside was limited for Chinese markets amid the holiday closure in Hong Kong and the absence of Stock Connect flows.

- US equity futures (ES -0.1%, NQ -0.2%) were rangebound ahead of looming data releases and risk events, while participants awaited the developments on Capitol Hill where the Senate continued to debate amendments to Trump's megabill.

- European equity futures indicate an uneventful cash market open with Euro Stoxx 50 future +0.1% after the cash market closed with losses of 0.4% on Monday.

FX

- DXY traded rangebound beneath the 97.00 level which provides some much-needed respite from the recent selling pressure that contributed to the greenback's worst first-half performance in over 50 years. The attention stateside remained on the ongoing vote-a-rama related to Trump's "big, beautiful bill" at the Senate with final passage expected later today, while Trump reiterated criticism against Fed Chair Powell and renewed his call for the Fed to lower rates in which he suggested they should be paying 1% interest or lower.

- EUR/USD held on to the prior day's gains but is off intraday highs after failing to sustain a brief foray into 1.1800 territory and with little reaction seen to the latest ECB rhetoric as participants look ahead to the panel participation of top central bankers at the ECB's Sintra Forum later today.

- GBP/USD struggled for direction after yesterday's choppy performance and with a lack of surprises from the recent UK GDP numbers which matched their initial estimates.

- USD/JPY marginally extended on its declines following the dollar's recent demise and in the aftermath of the mostly stronger-than-expected BoJ Tankan survey.

- Antipodeans briefly pared some of Monday's advances albeit with the reversal limited after the PBoC set a firmer yuan reference rate and Chinese Caixin Manufacturing PMI topped estimates.

- PBoC set USD/CNY mid-point at 7.1534 vs exp. 7.1509 (Prev. 7.1586)

FIXED INCOME

- 10yr UST futures held on to its spoils after bull flattening yesterday amid quarter-end, soft Chicago PMI data and Bessent dialling back expectations he will term out the debt.

- Bund futures rebounded off the prior day's trough after support held at the 130.00 level with participants awaiting several ECB speakers later today.

- 10yr JGB futures were initially indecisive and traded on both sides of the 139.00 level after the mostly stronger-than-expected BoJ Tankan survey but were later boosted in the aftermath of the 10yr JGB auction which resulted in a slightly lower bid-to-cover but higher accepted prices.

COMMODITIES

- Crude futures were lacklustre amid the absence of oil-specific catalysts and as the Iran-Israel ceasefire remained intact.

- Spot gold gradually edged higher above the USD 3,300/oz level following recent dollar weakness and as participants brace for upcoming data releases.

- Copper futures lacked conviction but kept afloat after better-than-expected Chinese Caixin Manufacturing PMI data.

CRYPTO

- Bitcoin was ultimately little changed with price action choppy around the USD 107k territory.

NOTABLE ASIA-PAC HEADLINES

- BoJ official said some automakers mentioned the impact of US trade policy although others cited improvement in profits due to pass-through of costs, while the official added there were no clear voices from firms citing the impact of US trade policy on capex plans.

DATA RECAP

- Chinese Caixin Manufacturing PMI Final (Jun) 50.4 vs. Exp. 49.0 (Prev. 48.3)

- Japanese Tankan Large Manufacturing Index (Q2) 13.0 vs. Exp. 10.0 (Prev. 12.0)

- Japanese Tankan Large Manufacturing Outlook (Q2) 12.0 vs. Exp. 9.0 (Prev. 12.0)

- Japanese Tankan Large Non-Manufacturing Index (Q2) 34.0 vs. Exp. 34.0 (Prev. 35.0)

- Japanese Tankan Large Non-Manufacturing Outlook (Q2) 27.0 vs. Exp. 29.0 (Prev. 28.0)

- Japanese Tankan Large All Industry Capex Estimate (Q2) 11.5% vs. Exp. 10.0% (Prev. 3.1%)

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu is to meet with US President Trump on July 7th, according to Axios.

- Israel is willing to soften some of its positions in an attempt to reach a text agreement for the release of hostages and a ceasefire in the Gaza Strip that would also be acceptable to Hamas, but will not agree to a commitment in advance that the temporary ceasefire will bring an end to the war, according to Axios citing an Israeli senior official.

- US State Department approved the potential sale of munitions guidance kits and munitions support to Israel for an estimated USD 510mln, according to the Pentagon.

- G7 issued a joint statement on Iran and the Middle East reiterating support for a ceasefire between Israel and Iran.

- Iran's Foreign Minister told CBS that he doesn't think negotiations will resume so quickly, according to Al Jazeera.

- Member of Iran's National Security Committee said "The elimination of Revolutionary Guards commanders will lead to a decisive response; we too can threaten Netanyahu's life", according to Kann News.

- Large explosions were heard after the Israeli forces blew up residential buildings east of Gaza City, according to Al Jazeera.

- Visegrad 24 posted on social media platform X regarding a mass-casualty event in Tehran after a drone struck an IRGC meeting with several people killed and wounded.

- Rockets attack reportedly targeted an Iraqi military airbase in Kirkuk, according to security sources cited by Reuters.

- White House said President Trump will sign an EO to terminate Syria sanctions. It was separately reported that the US is reviewing Syria's state sponsor of terror designation, while the action will end Syria's isolation from the international financial system and set the stage for global commerce and investment from the region and the US, according to a senior Treasury official.

RUSSIA-UKRAINE

- US Envoy to Ukraine Kellogg said Russia cannot continue to stall for time while it bombs civilian targets in Ukraine.

EU/UK

NOTABLE HEADLINES

- ECB President Lagarde said the world ahead is more uncertain and that is likely to make inflation more volatile, while she added that regular supply disruptions are leading firms to adjust prices more frequently, contributing to greater inflation volatility. Furthermore, Lagarde said large shocks can trigger feedback loops and non-linear effects.

- ECB's Simkus does not know if they'll have all the information they need by September and any move on rates is more likely towards year-end, while he said the ECB would decide meeting by meeting and avoid pre-commitment due to an unpredictable environment.

- Olaf Sleijpen takes over from Klaas Knot as head of Dutch central bank today, according to Bloomberg.

DATA RECAP

- UK BRC Shop Price Index YY (Jun) 0.4% (Prev. -0.1%)