US Market Open: Markets await Powell and US Senate vote-a-rama which Thune suggests is "getting to the end"

01 Jul 2025, 11:55 by Newsquawk Desk

- US Senate vote-a-rama is still ongoing, Thune suggests we are "getting to the end", unclear if he has enough votes

- EU reportedly wants immediate relief in any US deal, said to be accepting universal tariffs but is seeking key exemptions

- Risk tone began firmer after strong Chinese data; thereafter, deteriorated into and through the European morning

- US futures in the red, ES -0.2%, awaiting updates on the Reconciliation Bill, Chair Powell and a packed data docket

- USD continues to fall. JPY and CHF lead, fixed bid, XAU higher.

- EUR and EGBs unreactive to as-expected flash HICP and numerous ECB speakers who have focused on EUR strength

- Looking ahead, highlights include US Manufacturing PMIs, ISM Manufacturing, JOLTS Job Openings, ECB Central Banking Forum, Speakers including ECB’s Schnabel & Lagarde, Fed’s Powell, BoJ's Ueda, BoE’s Bailey & BoK's Rhee. Earnings from Constellation Brands. Holiday closures in Hong Kong & Canada.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- US narrows trade focus to secure deals, while officials were seeking phased deals with the most engaged countries as they race to find agreements by July 9th, according to FT.

- Japan's Chief Cabinet Secretary Hayashi said Japan won't do anything to sacrifice the agricultural sector in US trade talks, while Farm Minister Koizumi said he won't comment on US President Trump's posts regarding Japan's rice imports.

- EU is to accept Trump’s universal tariff but seeks key exemptions and it wants the US to commit to lower rates on key sectors such as pharmaceuticals, alcohol, semiconductors and commercial aircraft, while it is pushing for quotas and exemptions to effectively lower a 25% tariff on automobiles and car parts as well as a 50% tariff on steel and aluminium, according to Bloomberg.

- RTÉ News understands that EU ambassadors were informed that the ongoing Section 232 investigation into the pharmaceutical sector would continue and would lead to measures "one way or another". It is understood the EU's own drive for simplification of rules is being offered as a concession, as well as plans to increase purchases of LNG and AI technology.

- EU reportedly seeks immediate relief from tariffs in key sectors as part of any trade deal with the US; wants immediate relief as soon as an initial agreement is reached, rather than waiting weeks or month for a final accord, via Reuters sources. Many EU members said a deal without this is unacceptable.

EUROPEAN TRADE

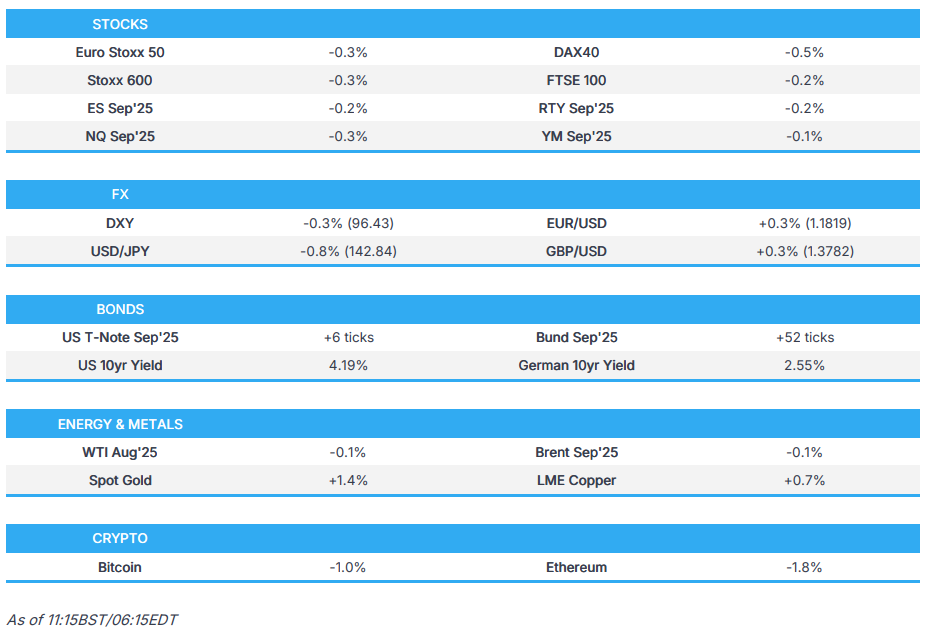

EQUITIES

- European benchmarks began the day in the green, though futures were drifting into the open and this trajectory has increased since, Euro Stoxx 50 -0.5%.

- Specifics behind the move somewhat light, potentially a function of a modest pullback from recent gains and as markets look to the first very busy day of a front-loaded week.

- Sectors mixed, at the top of the pile we have Utilities, potentially boosted by the European heatwave and soaring demand for A/C.

- Stateside, futures have also been drifting, ES -0.2%; focus on Capitol Hill as the Senate enters its 20th hour of vote-a-rama on the Reconciliation Bill. Updates fluid, no clear view on when the final vote will be as it stands. House expected to get it on Wednesday, remains to be seen how smooth the passage there will be and if Trump's 4th July deadline can hold.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY began the new month/quarter/HY relatively stable under 97.00 following recent selling pressure. However, as the morning progressed the pressure has ramped up with the index down to a 96.37 low. Focus firmly on the Reconciliation Bill (Senate debate ongoing, into its 20th hour).

- Havens outperform as the tone continues to deteriorate throughout the morning, USD/JPY as low as 142.83 vs a 144.06 high and USD/CHF below 0.79 to a 0.7875 base.

- EUR/USD above the 1.18 mark. Climbing gradually throughout the morning, a lot of ECB speak on the EUR. Further upside somewhat endorsed by de Guindos saying that EUR/USD at 1.17 is perfectly acceptable, even 1.20 could be overlooked, while any more would be "complicated".

- EUR unreactive to the morning's inflation data, which was as-expected across the board. No move in ECB pricing, still near-enough implies one more cut in 2025.

- Antipodeans have a slight upward bias, despite the risk tone, buoyed by the overnight release of the Chinese Caixin Manufacturing PMI, which topped forecasts with a surprise return to expansionary territory.

- PBoC set USD/CNY mid-point at 7.1534 vs exp. 7.1509 (Prev. 7.1586)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Complex is bid, continuing Monday's gains. Supported by the deteriorating risk tone and digesting/awaiting numerous central bank officials.

- USTs continue to bull-flatten this morning, extending the bias that was seen on Monday amid quarter-end, soft Chicago PMI data and Bessent dialling back expectations he will term out the debt.

- USTs are just off best in a 112-00 to 112-12 band, surpassing the 112-05 June high and now eyeing the 112-23 May peak.

- Bunds unreactive to Flash HICP for June, printed in-line with analyst forecasts for the three main figures and while the Services Y/Y ticked up to 2.3% (prev. 2.2%), it is worth reminding the print has trimmed significantly from the 4% level seen in April.

- Benchmark around 10 ticks off best in a 130.18 to 130.73 band. If the upside resumes, resistance eyed at 130.80 from last Thursday before a handful of levels earlier that week between 131.12 to 131.20.

- Gilts outperform, but only modestly so, no move to its own unrevised PMI or a strong Green auction (as is usually the case). Numerous remarks from Bailey, nothing that has moved the dial though yield commentary was interesting. Ahead, the government presents its Welfare Reform Bill to the Commons for a second read, should pass but not a guarantee given expected significant rebellion.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks in the red, but only modestly so, action this morning has been choppy with the space caught between the deteriorating risk tone and the softer USD. WTI resides in a USD 64.67-65.32/bbl range while Brent sits in a USD 66.31-66.97/bbl range.

- Specifics light, but we have seen a handful of geopolitical developments: 1) Iranian Government says there is no date or decision on negotiations with Washington, 2) "No breakthrough in Gaza negotiations and a large-scale campaign aimed at increasing pressure on Hamas remains an option", according to Sky News Arabia citing Israeli press.

- Precious metals firmer, bolstered by the discussed risk tone. XAU above the USD 3300/oz mark, surpassing its 50-DMA at USD 3320/oz but stalling before the 26th June peak at USD 3350/oz.

- Base metals firmer across the board, off best given the tone but proving much more resilient than other assets. Resilience that comes from the better-than-expected Chinese Caixin Manufacturing PMI data, a release which lifted 3M LME Copper to a three-month peak at USD 9.98k.

- HSBC increases avg. gold price at USD 3,175/oz by the end of this year; sees USD 3,125 in 2026 (prev. saw 2,915).

- Commerzbank sees year-end copper prices at USD 9,500/ton (prev. saw 9,400).

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HICP Flash YY (Jun) 2.0% vs. Exp. 2.0% (Prev. 1.9%); Services 3.3% (prev. 3.2%); X Food & Energy Flash YY (Jun) 2.4% vs. Exp. 2.4% (Prev. 2.4%); X Food, Energy, Alcohol & Tobacco Flash YY (Jun) 2.3% vs. Exp. 2.3% (Prev. 2.3%)

- ECB Consumer Expectation Survey: 1-year CPI 2.8% (prev. 3.1%), 3-year 2.8% (prev. 3.1%), 5-year 2.1% (prev. 2.1%).

- EU HCOB Manufacturing Final PMI (Jun) 49.5 vs. Exp. 49.4 (Prev. 49.4); German HCOB Manufacturing PMI (Jun) 49.0 vs. Exp. 49.0 (Prev. 49.0); French HCOB Manufacturing PMI (Jun) 48.1 vs. Exp. 47.8 (Prev. 47.8)

- German Unemployment Rate SA (Jun) 6.3% vs. Exp. 6.4% (Prev. 6.3%); Unemployment Chg SA (Jun) 11.0k vs. Exp. 15.0k (Prev. 34.0k)

- UK BRC Shop Price Index YY (Jun) 0.4% (Prev. -0.1%)

- UK S&P Global Manufacturing PMI (Jun) 47.7 vs. Exp. 47.7 (Prev. 47.7)

NOTABLE EUROPEAN HEADLINES

- Olaf Sleijpen takes over from Klaas Knot as head of Dutch central bank today, according to Bloomberg.

- ECB's Nagel says we are in "calm waters" on inflation, but cannot be complacent, via Bloomberg TV. Policy is in neutral territory. Uncertainty warrants a meeting-by-meeting approach.

- ECB's Wunsch says risks are more tilted to the downside, if a move on rates was needed it would be down, via CNBC; broad consensus is that the job is primarily done

- ECB's Lane says it is going to be a lively few years, via CNBC; not very helpful to provide too much forward guidance. 10% tariffs are part of the baseline. EUR appreciating has a tightening effect. Has been some rebalancing by global investors to the EUR.

- ECB's de Guindos says the level of uncertainty is huge, via Bloomberg TV; must keep all options open. EUR/USD at 1.17 is perfectly acceptable, even 1.20 could be overlooked, any more would be "complicated". The possibility of undershooting the 2% inflation target is quite limited. Risks tilted to the downside. An additional cut would not help the economy to improve, more certainty is what is required. Speed of the FX move is more concerning than the actual level.

- ECB's Escriva says the symmetric 2% inflation goal should continue to be the priority.

- ECB's Kazaks says any rate adjustments will be nothing big; further moves would be about signalling and fine-turning. Further EUR gains could increase the case for another cut. 10% US Tariff, plus EUR appreciation is large enough to hurt exports; any further rate cut would be small

- BoE Governor Bailey says need to watch carefully for the consequences of declining inflation; labour market is softening. Path of interest rates will continue to be gradually downwards. Not convinced cyclical productivity will come back. Have seen a steepening of the long-term bond yield curve. Does not think there is anything unusual about the UK when it comes to the yield curve. There will be no sustained growth without stable and low inflation.

- SNB's Zanetti says the central bank has the tools to deal with the current challenging situation; adds that negative rates are an option.

- Blonde Money reports there are 84 UK Labour MPs who are negative on the welfare reform, citing their latest analysis.

NOTABLE US HEADLINES

- US Senate parliamentarian has ruled that Sen. Murkowski’s Alaska carve-out for SNAP is compliant with the Byrd Rule, but the Medicaid one is not compliant, via Punchbowl's Desiderio.

- US Senate votes 99-1 to remove the AI state regulation moratorium from the Reconciliation Bill (i.e. Senate adopts Blackburn's amendment).

- Punchbowl reports US Senate Majority leader Thune said, “We’re getting to the end here.”, adds It’s unclear if Thune has the votes necessary for passage, or if he’s prepared to plow ahead with a final vote anyway.

- Punchbowl reports the House Rules Committee is "slated to come at noon to begin to prepare the bill for floor consideration. The full House is expected back Wednesday."

GEOPOLITICS

- US State Department approved the potential sale of munitions guidance kits and munitions support to Israel for an estimated USD 510mln, according to the Pentagon.

- G7 issued a joint statement on Iran and the Middle East reiterating support for a ceasefire between Israel and Iran.

- Iran's Foreign Minister told CBS that he doesn't think negotiations will resume so quickly, according to Al Jazeera.

- Large explosions were heard after the Israeli forces blew up residential buildings east of Gaza City, according to Al Jazeera.

- Visegrad 24 posted on social media platform X regarding a mass-casualty event in Tehran after a drone struck an IRGC meeting with several people killed and wounded.

- Rockets attack reportedly targeted an Iraqi military airbase in Kirkuk, according to security sources cited by Reuters.

- White House said President Trump will sign an EO to terminate Syria sanctions. It was separately reported that the US is reviewing Syria's state sponsor of terror designation, while the action will end Syria's isolation from the international financial system and set the stage for global commerce and investment from the region and the US, according to a senior Treasury official.#

- "No breakthrough in Gaza negotiations and a large-scale campaign aimed at increasing pressure on Hamas remains an option", according to Sky News Arabia citing Israeli press.

CRYPTO

- Bitcoin in the red, still comfortably above the USD 105k mark but drifting further away from the USD 110k level that was in some focus on Monday.

APAC TRADE

- APAC stocks began the new quarter mostly higher, albeit with gains capped amid this week's busy data calendar and with underperformance in Japan owing to recent currency strength.

- ASX 200 treaded water with the index just about kept afloat as strength in defensives offset the losses in the mining and materials sectors.

- Nikkei 225 underperformed as exporters suffered the ill effects of recent currency strength and with the predominantly better-than-expected BoJ Tankan survey increasing the scope for a more hawkish BoJ, while US President Trump also noted they will be sending Japan a letter regarding tariffs after not accepting US rice.

- Shanghai Comp edged mild gains after Chinese Caixin Manufacturing PMI topped forecasts with a surprise return to expansionary territory, although the upside was limited for Chinese markets amid the holiday closure in Hong Kong and the absence of Stock Connect flows.

NOTABLE ASIA-PAC HEADLINES

- BoJ official said some automakers mentioned the impact of US trade policy although others cited improvement in profits due to pass-through of costs, while the official added there were no clear voices from firms citing the impact of US trade policy on capex plans.

- BoJ's Masu says he does not have any strong disagreement to the view that underlying inflation is still short of 2%. Want to scrutinise how prices move after recent commodity spikes moderate (with specific reference to rice). At some point, the BoJ must "unload its huge ETF holdings". Must do so cautiously. When asked if he is a dove/hawk, responds "probably stand in the middle, have not strong view".

DATA RECAP

- Chinese Caixin Manufacturing PMI Final (Jun) 50.4 vs. Exp. 49.0 (Prev. 48.3)

- Japanese Tankan Large Manufacturing Index (Q2) 13.0 vs. Exp. 10.0 (Prev. 12.0)

- Japanese Tankan Large Manufacturing Outlook (Q2) 12.0 vs. Exp. 9.0 (Prev. 12.0)

- Japanese Tankan Large Non-Manufacturing Index (Q2) 34.0 vs. Exp. 34.0 (Prev. 35.0)

- Japanese Tankan Large Non-Manufacturing Outlook (Q2) 27.0 vs. Exp. 29.0 (Prev. 28.0)

- Japanese Tankan Large All Industry Capex Estimate (Q2) 11.5% vs. Exp. 10.0% (Prev. 3.1%)