US Market Open: RTY outperforms, USD attempting to rebound with focus on the House and tier-1 data

02 Jul 2025, 11:40 by Newsquawk Desk

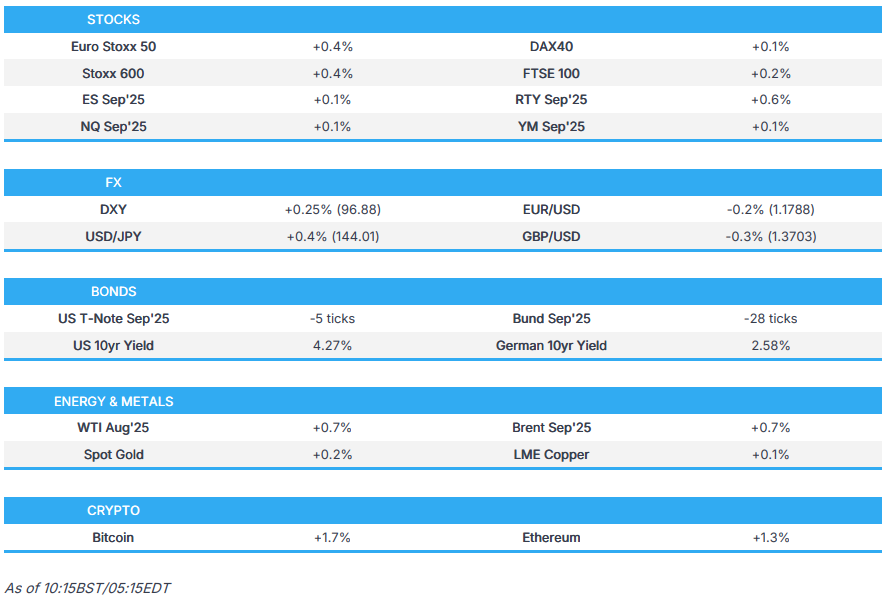

- European bourses in the green, shrugging off a mixed APAC lead. US futures post modest gains, RTY outperforms

- USD attempts to atone for recent pressure. DXY eyes 97.00 to the upside, JPY lags, EUR and GBP both hit

- Fixed in the red, Gilts lag after the UK Welfare Reform u-turn. USTs await data and fiscal updates

- US House set to convene at 09:00ET, Punchbowl reports several sources expressing alarm at the number of no's from lawmakers

- Crude in the green and despite light newsflow continue to climb, metals mixed

- Looking ahead, highlights include US Challenger Layoffs, ADP National Employment, Canadian Manufacturing PMI, NBP Policy Announcement, ECBʼs Lane & Lagarde.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- Japan's tariff negotiator Akazawa is arranging a US visit as early as this weekend for trade talks, according to TV Asahi; Japan and the US are continuing vigorous trade talks. Notes that staff level talks were held on June 30th, reiterates that an agreement that would hurt Japan's national interests for the sake of timing should not be made, will not deny possibilities of travelling to the US, but has no specific schedule to do so

- Canada's Ambassador to Washington said Canada still aims to lift all Trump tariffs as part of a deal with the US, according to the Globe and Mail.

- South American bloc Mercosur concluded talks for a free-trade agreement with European bloc EFTA, while the blocs are set to announce finalisation of a free trade agreement on Wednesday, according to Brazilian sources cited by Reuters.

- EU Trade Commissioner Sefcovic is to visit China in August, via SCMP citing sources; his team is reportedly compiling a list of specific "asks" that would seek from China; in turn, Sefcovic has been asked to be more specific with his requests. Chinese investment within Europe is seen as a potential area for discussion. On this, the SCMP piece references EVs and battery plants.

- Maersk (MAERSKB DC) says many customers are reassessing shipment timings in light of potential reintroduction of US-China tariffs in August, making Q3 planning more complex.

EUROPEAN TRADE

EQUITIES

- European indices opened in the green, shrugging off a mixed APAC lead. Euro Stoxx 50 +0.5%; newsflow has been a little light, primarily focussed on trade.

- European sectors were entirely in the green, Banks outperforming initially, bolstered by numerous equity specifics; however, strength has faded with sectors now mixed, Real Estate lags given the elevated yield environment.

- US futures posting modest gains, ES +0.1%; RTY +0.5% is the clear outperformer as it catches up to the gains made elsewhere on Tuesday. Handful of equity specifics in focus around Apple, Netflix, Spotify and others; day ahead looks to the Reconciliation Bill entering the House, data and any further trade commentary.

- Barclays increases its Stoxx 600 year-end target to 570 from 540 (implies circa 5.2% upside from current levels).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is attempting to atone for recent pressure with the DXY firmer and eyeing 97.00 to the upside, having breached Tuesday's 96.94 peak. Today's data slate sees Challenger layoffs and ADP employment, ahead of tomorrow's NFP print with markets likely to be particularly sensitive to any downside surprise.

- G10 peers are all lower vs the USD. The CAD fares best and is essentially flat on return from holiday and benefitting from crude strength.

- JPY lags, USD/JPY above 144.00 in a 143.33 to 144.24 band. Hit by the increasingly sour tone from the US administration regarding US-Japan trade talks. To recap, US President Trump said he doubts they'll have a deal with Japan; suggested Japan could pay 30% or 35% tariffs.

- Sterling under pressure against the USD, Cable below 1.37 to a 1.3689 trough, and also the EUR. Macro focus on the Welfare Reform vote which required another u-turn to ensure its passage, highlighting concern around the fiscal backdrop for the UK.

- While the EUR outpaces GBP, it is softer against the USD with EUR/USD below 1.18 and taking a breather from the 1.1830 multi-year peak that printed on Tuesday. Ongoing remarks from the Sintra conference, but nothing that has moved the dial thus far.

- PBoC set USD/CNY mid-point at 7.1546 vs exp. 7.1623 (Prev. 7.1534).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- In the red, Gilts lag after further concessions on the Welfare Reform Bill. Concessions that increase the odds of tax increases and calls into question the government's fiscal credibility, writes IFS. Lower by over 50 ticks on the session, but above support at 92.85 and 92.83 from last Friday and this Monday, respectively.

- A softer session for EGBs as well. Specifics light with nothing groundbreaking from Sintra just yet. Bunds at the low-end of a 130.08 to 130.50 band. One that is 10 ticks below Tuesday’s base but a similar amount clear of the WTD 130.00 base. If breached, we look to 129.92 and then 129.30 from the last two weeks of May.

- USTs also lower, though to a slightly lesser degree than the above peers. Holding at the low-end of a 111-20+ to 111-30+ band. A tick below Tuesday’s base and notching a fresh WTD low by half a tick. If the move continues, there is a bit of a gap until 110-25 from the week before.

- UK sells GBP 5bln 4.375% 2028 Gilt: b/c 3.46x (prev. 3.08x), average yield 3.847% (prev. 4.062%) & tail 0.1bps (prev. 0.3bps)

- Germany sells EUR 4.557bln vs exp. EUR 6bln 2.60% 2035 Bund: b/c 1.6x, average yield 2.63%, retention 24.05%

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are in the green and continuing to climb as the session progresses. Magnitude of strength initially in-line with that seen in European equity benchmarks but has since extended. Newsflow this morning light, handful of updates on the geopolitical front and no sustained follow through to the surprise private inventory build last night.

- WTI resides in a USD 65.23-65.93/bbl range while its Brent counterpart trades in a USD 66.94-67.75/bbl range.

- Precious metals somewhat mixed, XAU and XAG wane from peaks set in APAC trade, hit this morning as the USD gains ground. Though, for XAU, parameters are not too pronounced as participants await the next macro inflection point and look to Challenger Layoffs before ADP.

- Base metals mostly but modestly firmer, upside capped by discussed USD strength. For copper, attention on reports of mining disruptions in Peru while LME on-warrant aluminium stockpiles have hit a 2025 peak.

- US Private inventory data (bbls): Crude +0.7mln (exp.-1.8mln), Distillate -3.5mln (exp. -1.0mln), Gasoline +1.9mln (exp. -0.2mln), Cushing -1.4mln.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Unemployment Rate (May) 6.3% vs. Exp. 6.2% (Prev. 6.2%)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer won the vote in parliament on welfare reform; was forced to back down on certain aspects of his proposal. Savings under the plan are now expected to be closer to GBP 2bln vs. initially planned GBP 5bln.

- EU reportedly blocks Britain's attempts to join the pan-European trading bloc, according to the FT.

- ECB's Centeno says the ECB remains cautious on the rate path.

- ECB's Rehn says the ECB should be mindful of the risk that inflation stays persistently below 2% target; says joint EU borrowing to finance defence could also boost EUR's role by creating new safe asset.

- ECB's Wunsch says there is an argument for providing a mildly supportive policy stance; not uncomfortable with market rate expectations.

- BoE's Taylor says a soft landing on interest rates is at risk, don't think bigger cuts are needed or desirable. UK neutral real rate to be around 0.75-1.0%, putting the nominal rate around 2.75-3.0%. In Q1, reading of the deteriorating outlook suggested that the BoE needed to be on a lower rate path, needing five cuts in 2025 rather than the market-implied quarterly pace of four. QT is not on a pre-set path, like rates.

NOTABLE US HEADLINES

- US Senate passed President Trump's tax bill after VP Vance broke the tie to pass the Trump tax bill.

- US House Speaker Johnson said the Senate went a “little further than many of us would have preferred” in amending the bill, according to Punchbowl. It was later reported that US House Speaker Johnson said voting on the bill will be on Thursday at the latest, according to a Fox News interview.

- Punchbowl says the Reconciliation Bill schedule is to bring the US House back at 09:00ET/14:00BST today and vote as soon as possible. Punchbowl spoke to several people on the House GOP whip team Tuesday night, they expressed alarm about what they’re seeing on their whip cards. Sources said that they were racking up no’s from lawmakers who they didn’t expect would be opposed to the bill. Reports that a "bunch" of House Freedom Caucus members are saying they’ll vote no. Elsewhere, on the Democratic leader Jeffries' Magic Minute, sources suggest it will be around one hour long.

- CBO reports the new price tag for the Senate-passed US Reconciliation Bill is a USD 3.4tln deficit increase, via Bloomberg's Wasson.

- Netflix (NFLX) is reportedly discussing music-related events with Spotify (SPOT), via WSJ citing sources.

- Apple (AAPL) is facing a "hurdle" after supplier Foxconn (2317 TW) has pulled Chinese staff from India, according to Bloomberg.

GEOPOLITICS

MIDDLE EAST

- US President posted that his representatives had a long and productive meeting with the Israelis on Gaza and Israel agreed to the necessary conditions to finalise a 60-day ceasefire during which they will work with all parties to end the war. Furthermore, the Qataris and Egyptians will deliver this final proposal and he hopes, for the good of the Middle East, that Hamas takes this deal, because it will not get better and will only get worse.

- US officials said Iran made preparations to mine the Strait of Hormuz last month although mines were not deployed in the strait, according to Reuters.

- "Iranian Minister of Communications: Internet outages in the country caused by external attacks", according to Al Jazeera.

- "Advisor to the Commander-in-Chief of the IRGC: The war has stopped, but the United States and Israel have not achieved their goals", according to Iran International.

RUSSIA-UKRAINE

- US Pentagon has halted shipments of some air defence missiles and other precision munitions to Ukraine due to worries that US weapons stockpiles have fallen too low, according to Politico.

OTHER

- Quad joint statement expresses serious concern over the situation in the East China Sea and South China Sea, while they called for the perpetrators, organisers and financiers of the April 22nd attack in Indian Kashmir to be brought to justice.

CRYPTO

- Bitcoin in the green, to a USD 107.8k peak but yet to move towards the in-focus USD 100k mark.

APAC TRADE

- APAC stocks were mixed following a similar handover from the US where participants digested data, trade commentary and a slew of central bank rhetoric.

- ASX 200 gained as strength in the mining, materials and real estate sectors offset the losses in tech and financials, but with further upside contained by disappointing Australian Retail Sales and Building Approvals data.

- Nikkei 225 declined amid trade uncertainty after President Trump noted doubts about a deal with Japan and suggested Japan could pay 30% or 35% tariffs.

- Hang Seng and Shanghai Comp traded mixed with the Hong Kong benchmark underpinned on return from the holiday closure as gambling stocks surged owing to the jump in Macau gaming revenue for June, while the mainland was contained after the PBoC's open market operations resulted in a net CNY 266.8bln drain.

NOTABLE ASIA-PAC HEADLINES

- Japanese government issues emergency earthquake warning, near Tokara; with a 5.1 magnitude earthquake reported off the coast of Japan's Kagoshima prefecture, via NHK; Earthquake hit around 15:26 JST (07:26BST). No tsunami warning.

DATA RECAP

- Australian Retail Sales MM Final (May) 0.2% vs. Exp. 0.4% (Prev. -0.1%)

- Australian Building Approvals (May) 3.2% vs. Exp. 4.8% (Prev. -5.7%, Rev. -4.1%)

- South Korean CPI MM (Jun) 0.0% vs. Exp. 0.0% (Prev. -0.1%)

- South Korean CPI Growth YY (Jun) 2.2% vs. Exp. 2.1% (Prev. 1.9%)