Europe Market Open: Europe primed for a marginally firmer open ahead of NFP, reconciliation & trade updates

03 Jul 2025, 06:50 by Newsquawk Desk

- APAC stocks failed to sustain the mostly constructive handover from Wall St counterparts with sentiment in the region cautious as participants braced for the key US jobs data and digested Chinese Caixin Services and Composite PMIs.

- Siemens confirmed it has been notified by the US Commerce Department that export control restrictions on EDA software and technology to customers in China are no longer in place.

- US House Republicans were reportedly stuck and didn't have the votes for the rule, while Republicans had told members to go back into their offices and a vote on the rule didn’t look imminent, according to Punchbowl.

- UK PM Starmer said Rachel Reeves will be the Chancellor for years to come and will be the Chancellor at the next election.

- European equity futures indicate a marginally positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with gains of 0.7% on Wednesday.

- Looking ahead, highlights include EZ, UK, US PMIs (Final), Swiss CPI, US NFP, International Trade, Jobless Claims, ISM Services, Canadian Trade, ECB Minutes & BoE DMP, Speakers including BoJ’s Takata & Fed’s Bostic, Supply from Spain & US Refunding Announcement.

- Desk Schedule: On Thursday 3rd July, the desk will shut at 18:15BST/13:15EDT due to the US Independence Day. The service will resume on Thursday 3rd July for the beginning of Asia-Pac coverage at 22:00BST/17:00EDT.

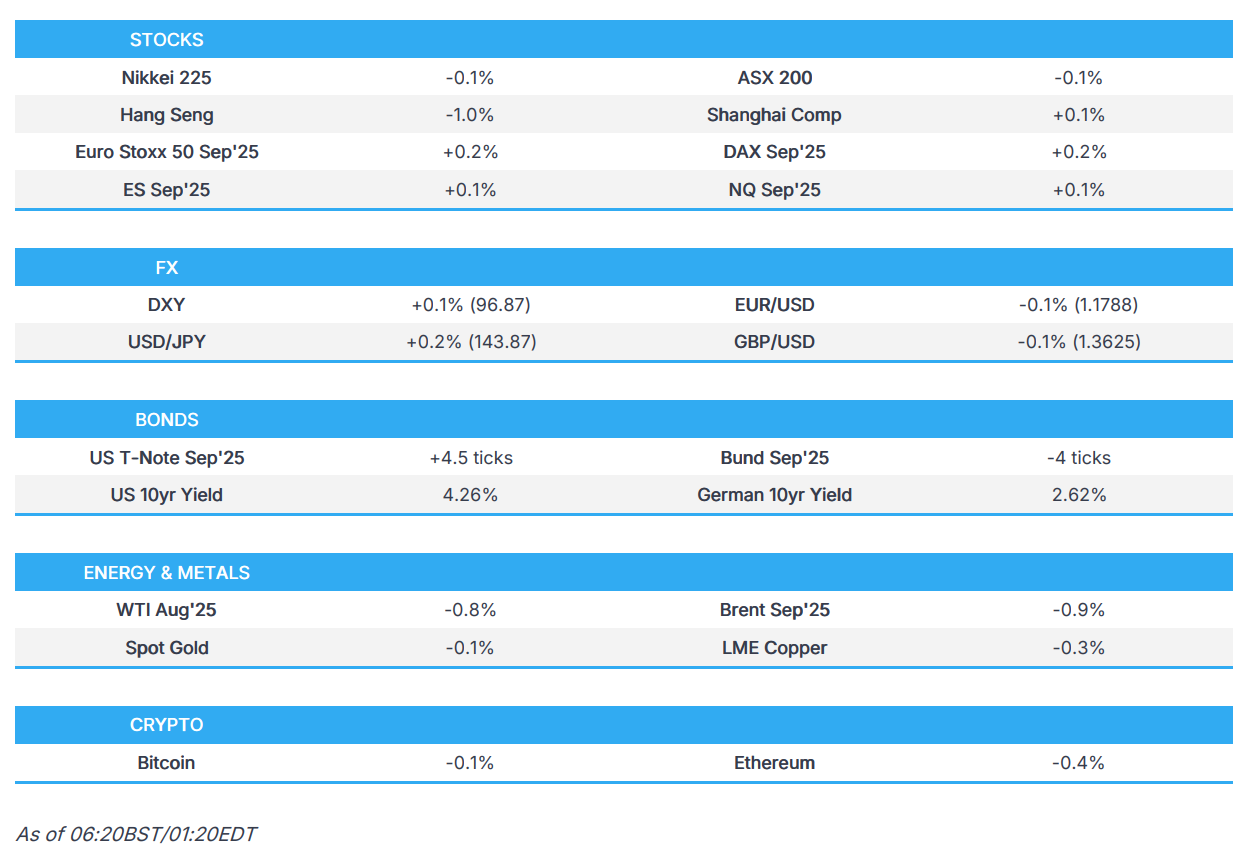

SNAPSHOT

US TRADE

EQUITIES

- US stocks mostly closed in the green but with pressure seen in the European morning after a woeful ADP report, which heavily missed expectations. Nonetheless, risk appetite started to stage a comeback around the opening bell with upside in Apple (AAPL) following an upgrade and with Tesla (TSLA) delivery numbers not as bad as feared, while a deal between the US and Vietnam on trade also lifted sentiment.

- SPX +0.47% at 6,227, NDX +0.73% at 22,642, DJI -0.02% at 44,484, RUT +1.31% at 2,226.

- Click here for a detailed summary.

TARIFFS/TRADE

- US-Vietnam final deal is still being worked on and is to be sealed "within coming weeks" with no numbers included on final tariff rates, while Vietnam will spend USD 8bln to purchase 50 Boeing (BA) aircraft and will buy USD 2.9bln in agriculture goods, according to Politico.

- FBN's Lawrence said multiple trade sources are telling him that they could get an announcement of a tariff deal with India as early as Thursday and he was told the language on an India deal was being finalised, although he caveated that it is still fluid until President Trump actually signs off on it.

- Siemens (SIE GY) said the US rescinded curbs for the Co. related to chip design software sales to China, according to Bloomberg. Siemens later confirmed it has resumed sales and support to Chinese customers after it was recently notified by the US Commerce Department that export control restrictions on EDA software and technology to customers in China are no longer in place.

- South Korea's President Lee said he cannot say if they can conclude US tariff talks by July 8th and the two sides are not really clear on what they want concerning tariff talks, while he added that US tariff negotiations are looking very difficult.

- Mexico's Foreign Minister said a delegation is set to visit Washington D.C. for talks on security, migration, and trade.

NOTABLE HEADLINES

- US President Trump posted on Truth Social calling for Fed Chair Powell to "resign immediately" and linked an article regarding calls by the FHFA head for the Fed chair to be investigated by Congress.

- US FHFA, Fannie Mac and Freddie Mac Chairman, Bill Pulte, called on Congress to investigate Fed Chair Powell due to his political bias and deceptive Senate testimony, which is enough to be removed "for cause".

- Fed's Barkin (2027 voter) said probably in assessing the jobs report is impact of slowing immigration and will be looking at the change in the unemployment rate, while he added they have a lot to learn before the next meeting, including jobs, inflation and on trade policy but noted the US economy remains solid.

- US House Republicans were reportedly stuck and didn't have the votes for the rule, while Republicans had told members to go back into their offices and a vote on the rule didn’t look imminent, according to Punchbowl. However, US President Trump later posted that it looked like the House was ready to vote and that they had great conversations all day, while House Speaker Johnson also commented that they are in a good place now referring to the House vote on the One Big Beautiful Bill.

- Many conservative House Republicans were reportedly worried about the Senate’s added Medicaid cuts in the megabill including for provider tax and state-directed payments, according to Politico.

APAC TRADE

EQUITIES

- APAC stocks failed to sustain the mostly constructive handover from Wall St counterparts with sentiment in the region cautious as participants braced for the key US jobs data and digested Chinese Caixin Services and Composite PMIs.

- ASX 200 marginally declined amid weakness in telecoms, financials and the consumer sectors, while trade data showed a monthly contraction in Australian exports.

- Nikkei 225 lacked conviction in the absence of tier-1 data from Japan and following mixed rhetoric from BoJ's Takata, while US-Japan trade uncertainty lingered and trade negotiator Akazawa recently reiterated that an agreement which would hurt Japan's national interests for the sake of timing should not be made.

- Hang Seng and Shanghai Comp were ultimately mixed following Chinese PMI data in which Caixin Services PMI missed expectations but Caixin Composite PMI accelerated and returned to expansionary territory.

- US equity futures were little changed with key US jobs data on the horizon and Trump's megabill stalling at the House.

- European equity futures indicate a marginally positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with gains of 0.7% on Wednesday.

FX

- DXY traded rangebound as participants braced for today's Non-Farm Payrolls release ahead of the US Independence Day holiday and with Republicans attempting to break down the resistance to the Trump megabill which has somewhat stalled at the House although both US President Trump and House Speaker Johnson had suggested they are in a better place now regarding a vote.

- EUR/USD price action was little changed near the 1.1800 focal point following yesterday's fluctuations and after the latest ECB rhetoric had little impact, while it was also reported that ECB officials question whether euro has strengthened too much as policymakers at the central bank fret that a surging currency increases the risk of inflation undershooting.

- GBP/USD rebounded off the prior day's trough after underperforming on political uncertainty related to UK Chancellor Reeves but with some relief seen after PM Starmer voiced support for Reeves and stated she will be the Chancellor for years to come and at the next election.

- USD/JPY lacked conviction amid the flimsy risk appetite in the region and in the absence of tier-1 data releases from Japan, while there was also a deluge of somewhat mixed comments from BoJ's Takata.

- Antipodeans marginally softened amid the cautious overnight sentiment and following mostly weaker Australian trade data.

- PBoC set USD/CNY mid-point at 7.1523 vs exp. 7.1618 (Prev. 7.1546).

FIXED INCOME

- 10yr UST futures mildly extended on the prior day's intraday rebound after initially tracking Gilts lower due to uncertainty regarding UK Chancellor Reeves although PM Starmer has since voiced support for Reeves, while the focus now turns to the looming NFP report and if Republicans can secure enough votes at the House to pass the Trump tax and spending bill ahead of the Independence Day holiday.

- Bund futures remained lacklustre after slipping beneath the 130.00 level and as the recent ECB rhetoric provided little incrementally.

- 10yr JGB futures continued the choppy performance so far this week and as participants digested a mixed 30yr JGB auction, while there was a slew of comments from BoJ's Takata who stated the price stability target is close to being achieved and the BoJ should continue to further adjust the degree of monetary accommodation if it can confirm the positive corporate behaviour is being maintained, but also noted the BoJ needs to maintain its current accommodative monetary policy stance to maintain momentum toward hitting its price target.

COMMODITIES

- Crude futures pared some of their gains after advancing yesterday on the positive risk tone and as Iran signed into law the suspension of work with the IAEA.

- UAE's ADNOC restores most Murban crude oil supply for equity holders in July after earlier cuts.

- Spot gold pulled back from a weekly peak with price action constrained amid a flat dollar and as participants await key data.

- Copper futures took a breather after recent advances and amid the cautious overnight sentiment.

CRYPTO

- Bitcoin was choppy and returned to flat territory after failing to sustain a brief incursion into USD 109k territory, while there was a recent bullish call from Standard Chartered which sees prices to climb as high as USD 200k by year-end.

NOTABLE ASIA-PAC HEADLINES

- BoJ's Takata said the price stability target is close to being achieved and careful monitoring continues to be warranted, while he added that the BoJ should continue to further adjust the degree of monetary accommodation if it can confirm the positive corporate behaviour is being maintained. Takata also commented that given uncertainties regarding various US policies remain high, the BoJ should conduct monetary policy in a more flexible manner without being too pessimistic and to maintain momentum toward hitting its price target, the BoJ also needs to maintain its current accommodative monetary policy stance. Furthermore, his view is that the BoJ needs to support economic activity for the time being by maintaining its current accommodative monetary policy stance but at the same time, he believes the BoJ should gradually and cautiously shift gears in its monetary policy.

- PBoC has asked European financial institutions for advice on dealing with the effects of low interest rates, according to the FT.

- European Commission VP Kallas and Chinese Foreign Minister Wang reaffirmed EU's commitment to engage constructively with China to address global challenges, while Kallas called on China to end distortive practices, including restrictions on rare earth exports, which pose significant risks to European companies and endanger the reliability of global supply chains. Kallas also highlighted the serious threat Chinese companies' support for Russia's war poses to European security.

DATA RECAP

- Chinese Caixin Services PMI (Jun) 50.6 vs. Exp. 51.0 (Prev. 51.1)

- Chinese Caixin Composite PMI (Jun) 51.3 (Prev. 49.6)

- Australian Balance on Goods (AUD)(May) 2,238M vs. Exp. 5,000M (Prev. 5,413M)

- Australian Goods/Services Exports (May) -2.70% (Prev. -2.40%)

- Australian Goods/Services Imports (May) 3.80% (Prev. 1.10%)

GEOPOLITICS

MIDDLE EAST

- US clarified to Israel and Hamas in recent days that if no agreement is reached on the terms for ending the war during the 60-day ceasefire, the Trump administration will support its extension as long as serious negotiations continue, according to Axios.

- US State Department said Iran must cooperate fully without further delay and it is unacceptable that Iran chose to suspend cooperation with the IAEA.

- Iran's Foreign Minister said it seems that their nuclear facilities were severely damaged by US strikes and it seems that it will be a long time before a return to work of their nuclear facilities if possible.

RUSSIA-UKRAINE

- Ukraine's Minister said Ukraine is ready to buy or rent air defence systems after US aid halt, according to AFP.

- Russia's Kremlin said Russia expects the 3rd round of talks with Ukraine soon.

- North Korea is sending an extra 30,000 soldiers to Russia, according to NHK.

EU/UK

NOTABLE HEADLINES

- UK PM Starmer said Rachel Reeves will be the Chancellor for years to come and will be the Chancellor at the next election.

- ECB officials question whether the euro has strengthened too much as policymakers at the central bank fret that a surging currency increases the risk of inflation undershooting, according to FT

- European Commission President von der Leyen is to face a European Parliament vote of no confidence on Thursday, although the vote is mainly symbolic as the majority of political groups have already signalled that they will vote against the motion of no confidence, according to officials cited by POLITICO.