US Market Open: Tentative trade ahead of US Jobs and Bill updates

03 Jul 2025, 11:40 by Newsquawk Desk

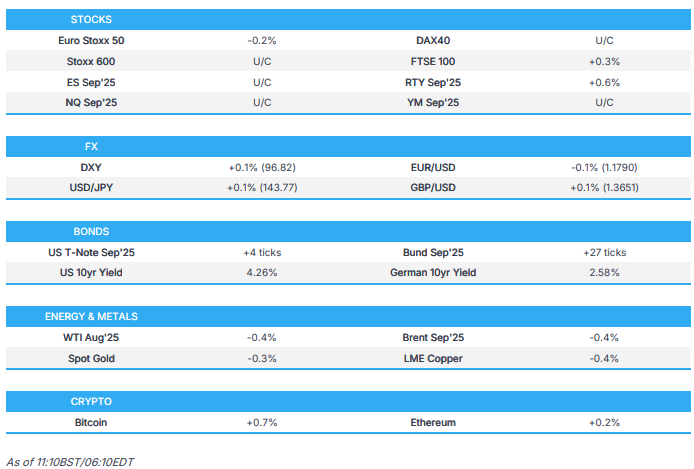

- European bourses began the session firmer, but that strength has waned to more mixed trade; US futures similar into a packed agenda

- DXY broadly flat intraday but with a marginal upward bias. G10s contained, but generally softer. GBP outperforms after Wednesday's post-PMQs pressure.

- Similarly, Gilts lead fixed income. USTs await data. Bunds unreactive to Final PMIs.

- Crude benchmarks softer, despite limited newsflow. Metals mixed, XAU off highs and fading as the USD picks up slightly.

- US Reconciliation Bill passed the Rules vote, awaiting full vote; timing unclear, dependent on the Minority Leader, but should be in the next hour(s).

- Looking ahead, highlights include US PMIs (Final), US NFP, International Trade, Jobless Claims, ISM Services, Canadian Trade, ECB Minutes. Speakers include Fedʼs Bostic

- Desk Schedule: On Thursday 3rd July, the desk will shut at 18:15BST/13:15EDT due to the US Independence Day. The service will resume on Thursday 3rd July for the beginning of Asia-Pac coverage at 22:00BST/17:00EDT.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- Siemens (SIE GY) said the US rescinded curbs for the Co. related to chip design software sales to China, according to Bloomberg. Siemens later confirmed it has resumed sales and support to Chinese customers after it was recently notified by the US Commerce Department that export control restrictions on EDA software and technology to customers in China are no longer in place.

- South Korea's President Lee said he cannot say if they can conclude US tariff talks by July 8th and the two sides are not really clear on what they want concerning tariff talks, while he added that US tariff negotiations are looking very difficult.

- Senior CCP official on US-China relations, says setting up barriers and thresholds will eventually harm both, says the US should recognise how much it has to gain from US-China cooperation.

- Vietnamese Foreign Minister says US and Vietnamese negotiating teams are coordinating to finalise the trade deal. Agreement creates expectation and hope for businesses. To continue boost exports and expand ties with other countries

EUROPEAN TRADE

EQUITIES

- European bourses began the session with gains into a packed afternoon agenda; however, as session has progressed this strength has waned a touch and the picture is now more mixed. Euro Stoxx 50 -0.2%; FTSE 100 +0.3% outperforms after the pressure seen on Wednesday.

- Sectors primarily in the green at first, though as above the picture has turned to more of a mixed one. Retail outperforms led by the initial readthrough of US-Vietnam updates, though the higher-than-expected tariff levy has caused this to fade. Real Estate also strong given UK yields.

- US futures are posting modest gains into the packed data docket, modest divergence between value and growth benchmarks this morning; ES +0.1%, RTY +0.5%.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is broadly flat intraday in typical pre-NFP trade. DXY just firmer in a 96.686 to 96.879 band, within yesterday's 96.62-97.16 parameter. ING does not believe that the FX market has reached "peak bearishness" on the USD, despite widespread negative sentiment and forecasts

- G10s are contained, but generally softer, vs the USD. Antipodeans have at points been at the bottom of the pile, with the AUD hit by primarily weaker Australian trade data overnight and potentially focus on the US-Vietnam deal.

- EUR contained on either side of 1.1800 throughout the morning. Since, has come under some modest pressure and slipping towards lows of 1.1787, clear of yesterday's 1.1746 base. Specifics light thus far, no move to Final PMIs. Awaiting US events.

- JPY and CHF mixed. USD/JPY lacked conviction overnight amid the flimsy risk appetite in the region, little move to a Rengo update for FY25; JPY under slight pressure but shy of 144.00. CHF a touch firmer after domestic inflation came in above market consensus, but roughly in-line with the SNB's quarterly view.

- Sterling outperforms, bouncing as markets in the UK welcome PM Starmer backing Chancellor Reeves after the sell off seen after PMQs. GBP/USD currently resides in a 1.3624-1.3675 range, well within yesterday's 1.3560-1.3752 parameter.

- PBoC set USD/CNY mid-point at 7.1523 vs exp. 7.1618 (Prev. 7.1546).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Gilts bounce as Starmer supports Reeves in extensive media rounds. Benchmark gapped higher by 23 ticks before extending further to a 92.74 peak. However, this still leaves it shy of Wednesday’s 93.41 peak and the WTD high above at 93.76. Amidst these moves, focus on yields as they recover from yesterday’s spike; 10yr down to 4.51% vs a 4.68% peak on Wednesday, 30yr to 5.30% vs 5.45%.

- USTs firmer, but only modestly so, into a frontloaded US agenda headlined by NFP (exp. 110k, prev. 139k). Thus far, the focus has been on the Reconciliation Bill; Rule vote passed, full vote expected in the next few hours, at this stage it should pass without too much issue. USTs in a slim sub-10 tick band, entirely within yesterday's slightly more expansive 111-16+ to 111-30+ parameter.

- Bunds bid and firmer by just over 30 ticks at best. Picked up gradually throughout the European morning with newsflow light aside from modest revisions to Final PMIs, no reaction to the prints. Supply well received, but again no reaction. Awaiting direction from the above US events.

- Spain sells EUR 6.049bln vs exp. EUR 5.0-6.0bln 2.40% 2028, 3.15% 2035, 3.50% 2041 Bono & EUR 0.735bln vs exp. EUR 0.25-0.75bln 1.15% 2036 I/L

- France sells EUR 11.95bln vs exp. EUR 10-12bln 3.20% 2035, 3.60% 2042 & 3.75% 2056 OAT

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are softer, despite limited newsflow. Bearishness potentially emanating from the lack of escalations regarding Iran, although a sixth round of US-Iranian negotiations is expected to be held in Oslo next week. More broadly, focus is beginning to turn to the weekend's OPEC+ meeting, where a production increase is expected.

- WTI resides in a USD 66.65-67.50/bbl range while its Brent counterpart trades in a USD 68.32-69.00/bbl range.

- Precious metals generally firmer into data. XAU has pulled back from WTD bests, but remains bid overall. As high as USD 3365/oz, vs USD 3329/oz from June 23rd.

- Base metals mixed, given the cautious typical pre-NFP tone. 3M LME Copper topped USD 10k/t and has been trading on either side of the level since.

- UAE's ADNOC restores most Murban crude oil supply for equity holders in July after earlier cuts.

- Click for a detailed summary

NOTABLE DATA RECAP

- Swiss CPI YY (Jun) 0.1% vs. Exp. -0.1% (Prev. -0.1%); MM 0.2% vs Exp. 0.0% (Prev. 0.1%)

- EU HCOB Composite PMI (Jun) 50.6 vs. Exp. 50.2 (Prev. 50.2); Services Final PMI (Jun) 50.5 vs. Exp. 50 (Prev. 50)

- German HCOB Composite Final PMI (Jun) 50.4 vs. Exp. 50.4 (Prev. 50.4); Services PMI (Jun) 49.7 vs. Exp. 49.4 (Prev. 49.4)

- UK S&P Global PMI: Composite Output (Jun) 52.0 vs. Exp. 50.7 (Prev. 50.7); Services PMI (Jun) 52.8 vs. Exp. 51.3 (Prev. 51.3)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer said Rachel Reeves will be the Chancellor for years to come and will be the Chancellor at the next election.

- ECB officials question whether the euro has strengthened too much as policymakers at the central bank fret that a surging currency increases the risk of inflation undershooting, according to FT

NOTABLE US HEADLINES

- US President Trump posted on Truth Social calling for Fed Chair Powell to "resign immediately" and linked an article regarding calls by the FHFA head for the Fed chair to be investigated by Congress.

- US FHFA, Fannie Mac and Freddie Mac Chairman, Bill Pulte, called on Congress to investigate Fed Chair Powell due to his political bias and deceptive Senate testimony, which is enough to be removed "for cause".

RECONCILLIATION BILL

- US House Republicans have now opened the way for final bill vote; rule vote passes with 219-213.

- The Democrat leader in the House began his Magic Minute at around 10:00BST/05:00ET; expected to last for one hour. After this, speaker Johnson will take the floor and then the final vote can begin.

GEOPOLITICS

- North Korea is sending an extra 30,000 soldiers to Russia, according to NHK.

- Deputy Commander of Russian Navy killed in Russia's Kursh, according to a Governor.

- "Israel's Channel 12: A sixth round of US-Iranian negotiations is expected to be held in Oslo next week", according to Sky News Arabia.

CRYPTO

- Bitcoin is firmer, breached the USD 110k mark and is currently holding essentially at the figure.

APAC TRADE

- APAC stocks failed to sustain the mostly constructive handover from Wall St counterparts with sentiment in the region cautious as participants braced for the key US jobs data and digested Chinese Caixin Services and Composite PMIs.

- ASX 200 marginally declined amid weakness in telecoms, financials and the consumer sectors, while trade data showed a monthly contraction in Australian exports.

- Nikkei 225 lacked conviction in the absence of tier-1 data from Japan and following mixed rhetoric from BoJ's Takata, while US-Japan trade uncertainty lingered and trade negotiator Akazawa recently reiterated that an agreement which would hurt Japan's national interests for the sake of timing should not be made.

- Hang Seng and Shanghai Comp were ultimately mixed following Chinese PMI data in which Caixin Services PMI missed expectations but Caixin Composite PMI accelerated and returned to expansionary territory.

NOTABLE ASIA-PAC HEADLINES

- BoJ's Takata said the price stability target is close to being achieved and careful monitoring continues to be warranted, while he added that the BoJ should continue to further adjust the degree of monetary accommodation if it can confirm the positive corporate behaviour is being maintained. Takata also commented that given uncertainties regarding various US policies remain high, the BoJ should conduct monetary policy in a more flexible manner without being too pessimistic and to maintain momentum toward hitting its price target, the BoJ also needs to maintain its current accommodative monetary policy stance. Furthermore, his view is that the BoJ needs to support economic activity for the time being by maintaining its current accommodative monetary policy stance but at the same time, he believes the BoJ should gradually and cautiously shift gears in its monetary policy.

- PBoC has asked European financial institutions for advice on dealing with the effects of low interest rates, according to the FT.

- European Commission VP Kallas and Chinese Foreign Minister Wang reaffirmed EU's commitment to engage constructively with China to address global challenges, while Kallas called on China to end distortive practices, including restrictions on rare earth exports, which pose significant risks to European companies and endanger the reliability of global supply chains. Kallas also highlighted the serious threat Chinese companies' support for Russia's war poses to European security.

- Japan Trade Union Rengo says final data shows avg. wage hike of 5.25% for fiscal 2025 (prev. 5.10% hike in 2024).

DATA RECAP

- Chinese Caixin Services PMI (Jun) 50.6 vs. Exp. 51.0 (Prev. 51.1); Composite PMI (Jun) 51.3 (Prev. 49.6)

- Australian Balance on Goods (AUD)(May) 2,238M vs. Exp. 5,000M (Prev. 5,413M)

- Australian Goods/Services Exports (May) -2.70% (Prev. -2.40%); Imports (May) 3.80% (Prev. 1.10%)