US Market Open: Constructive risk environment focusing on tariff extension to August 1st; AUD outperforms on unexpected hold

08 Jul 2025, 11:40 by Newsquawk Desk

- US President Trump said the August 1st tariff deadline is firm, but he is open to other ideas.

- European bourses began on the front foot, digesting the deadline pushback and reports that the US offered the EU a 10% tariff deal, via Politico.

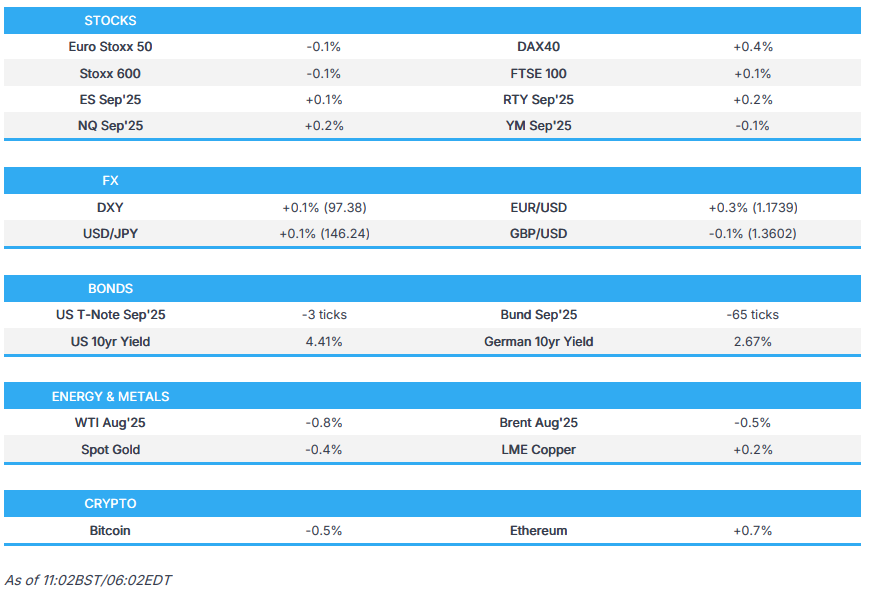

- Since, benchmarks have eased off best with the tone now mixed, Euro Stoxx 50 +0.1%. Stateside, non-tariff updates limited, ES +0.1%.

- DXY is giving back some of Monday's gains. AUD outperforms on a surprise RBA hold. EUR and GBP both firmer, but off best.

- Fixed benchmarks hit by the tariff deadline extension and a packed supply docket.

- Crude in the red but within familiar ranges, pressure intensified on reports that Doha talks recommenced. Metals follow the risk tone.

- Looking ahead, highlights include US NY Fed SCE, NFIB Business Optimism, EIA STEO, ECB's Nagel & de Guindos, Supply from the US

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

US

- US President Trump said regarding tariffs that the August 1st deadline is firm but he is open to other ideas, while Trump said he is close to making a trade deal with India and may adjust tariffs for some countries.

- White House announced that President Trump signed an executive order extending the tariff deadline to August 1st.

- US reportedly offered the EU a 10% tariff deal with caveats, although negotiations are still fluid, with any trade agreement subject to final approval by US President Trump, according to POLITICO.

OTHER NATIONS

- EU Commission President von der Leyen said Europe must show strength in trade negotiations with the US. Thereafter, German Finance Minister says if the EU does not reach a "fair" deal with he US, the bloc is ready to take counter-measures.

- Japanese PM Ishiba said haven't been able to reach an agreement because Japan kept defending what needs to be defended, and will continue dialogue with the US and seek a chance of agreeing on a deal that benefits both countries. Ishiba added they were able to avert a hike in tariffs to 30%-35%, as result of past negotiations, and the US has proposed to continue talks until the new August 1st deadline.

- Japanese Finance Minister Kato said they expect the US stance to change as they continue trade negotiations, while they will take necessary steps to help industries cope with US tariffs while communicating with other agencies.

- Japanese Tariff Negotiator Akazawa held a call with US Commerce Secretary Lutnick. Agreed to actively engage in trade negotiations. Auto sector is core to Japan's economy, can not tolerate the fact 25% tariffs on autos, and the auto parts tariff is inflicting huge losses on Japanese firms. No point in striking a US deal without an autos agreement.

- South Korea will step up trade negotiations with the US to win mutually beneficial results and clear up uncertainties caused by tariffs, while it added that trade talks with the US will be a chance to advance both countries' key industries through the 'Renaissance Partnership'.

- The UK is set to miss the original deadline to close its steel/aluminium trade deal with the US, according to Sky's Conway; Insiders say still some way from a breakthrough. However, "they are hopeful Donald Trump won't raise UK tariffs from 25% to 50% for the time being, despite having promised to on July 9th".

- Indian refiners reportedly plan to source around 10% of LPG imports from the US in 2026 in an attempt to reach a trade deal, according to Reuters sources.

EUROPEAN TRADE

EQUITIES

- European bourses opened higher, welcoming Trump's confirmation that the new tariff deadline is August 1st and as Monday's letters did not have any narrative-shifting surprises. Since, benchmarks have come off best and are either side of the unchanged mark, Euro Stoxx 50 U/C.

- Sectors in-fitting with the above and as such are now mixed. Basic Resources lead amid gains in Glencore (+2.5%) after an upgrade by and favourable commentary from JPMorgan. Retail at the other end, hit by the tariff letters on Asian manufacturing nations which are a key destination for European names such as Pandora (-1.1%).

- Stateside, futures are modestly firmer, ES +0.1%. Equity specifics a little light as we digest the tariff developments.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD has been giving back some of Monday's gains, upside that occurred alongside an increase in angst into the tariff letters. Ultimately, the main takeaway was Trump providing more time for negotiation and as such the TACO trade remains in play. DXY is currently tucked within yesterday's 96.89-97.66 range, currently just off highs of 97.43.

- AUD outperforms as the RBA surprisingly kept rates unchanged in a 6-3 vote, despite markets pricing in a 95% chance of a move pre-release. AUD/USD back above 0.65 but yet to breach Monday's 0.6564 peak.

- Upside that has pulled the Kwi along with it, NZD/USD has made its way back onto a 0.60 handle but is still some way off yesterday's 0.6063 high (current session peak @ 0.6034).

- EUR the next best, benefitting from reports which suggest 10% baseline tariffs remain an option for the EU. EUR/USD is currently firmer, just off a 1.1765 peak within Monday's 1.1686-1.1790 range.

- GBP just about in the green against the USD, but Cable is back to its earlier 1.36 base. A bout of further pressure emerged on an OBR risk report which laid out that "public finances in relatively vulnerable position and facing mounting risks", adds UK debt set to exceed 270% of GDP by early 2070s

- PBoC set USD/CNY mid-point at 7.1534 vs exp. 7.1772 (Prev. 7.1506)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Complex pushed lower by the tariff deadline extension and a packed supply docket.

- USTs saw a slightly softer start to the day, given the constructive risk tone. Similar story for EGBs and Gilts, though the magnitude of downside has increased throughout the morning, USTs to a 110-25+ trough, taking out Monday’s 110-29 base and now teetering just above 110-25, the WTD low from the last week of June.

- EGBs also dented, but with losses much more pronounced. Bunds lower by near 50 ticks. As referenced, pressure in EGBs has been increasing, an intensification that began alongside the constructive European cash equity open; furthermore, supply is weighing and the passing of some taps e.g. Germany failed to provide any relief (unsurprising, the German auction was somewhat soft and we await details on EU supply).

- For the most part, an absence of specifics for the UK. No follow through in Gilts from the OBR reporting that domestic finances are in a "relatively vulnerable position and face mounting risks". Nonetheless, Gilts lag with downside intensifying and the benchmark now looking to lows from mid-June, incl. 91.16.

- Germany sells EUR 3.754bln vs exp. EUR 5bln 2.20% 2030 Bobl: b/c 1.50x, average yield 2.26% & retention 24.92%.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are lacklustre, largely unaffected by trade updates with volumes light and awaiting further geopolitical updates from the Middle-East; Brent trades within a narrow USD 69.03 to 69.61/bbl range, re-approaching overnight lows following news regarding the resumption of Israel-Hamas Doha talks.

- Precious metals softer, dented by the broadly constructive risk tone in-fitting with pressure seen in other traditional havens (i.e. fixed and JPY). Though, downside is limited thus far with the softer USD and general tariff uncertainty, despite the welcome confirmation of an August 1st deadline, preventing a more concerted move lower. XAU down to a USD 3324/oz base and within Monday’s USD 3296-3343/oz band.

- Base metals, in contrast, welcome Trump signing an executive order pushing the tariff deadline to August 1st (prev. July 9th) and as the first batch of tariff letters didn’t contain anything particularly shocking. 3M LME Copper holds at the upper-end of a USD 9793-9889 band. However, it remains shy of Monday’s USD 9871 peak and last week’s USD 9889 best.

- US President Trump signed an Executive Order aiming to end subsidies for foreign-controlled energy sources.

- Click for a detailed summary

NOTABLE DATA RECAP

- French Trade Balance, EUR, SA (May) -7.8B vs. Exp. -8.25B (Prev. -7.968B, Rev. -7.6B)

- German Trade Balance, EUR, SA (May) 18.4B vs. Exp. 15.5B (Prev. 14.6B)

NOTABLE EUROPEAN HEADLINES

- German Finance Minister Klingbeil says they see that economic sentiment has improved.

- UK OBR says "public finances in relatively vulnerable position and facing mounting risks", adds UK debt set to exceed 270% of GDP by early 2070s.

NOTABLE US HEADLINES

- China's CPCA says Tesla (TSLA) exported 10,115 Chinese-made vehicles in June (May 23,074)

GEOPOLITICS

MIDDLE EAST

- US President Trump said he's got great cooperation from countries neighbouring Israel, when asked about Palestinian relocation plans. Trump noted Iran talks are scheduled and that Iran will not be a nuclear state, while he hopes they don't have to do another strike on Iran.

- White House said US Envoy Witkoff is to travel to Doha later this week for a Gaza ceasefire, while it was separately reported that Witkoff said they have an opportunity to get a peace deal in Gaza and that the Iran meeting will be in the next week or so.

- Subsequently, Iran's MFA Spokesman told state TV: "We have not handed in any requests to meet with the Americans", via France24.

- UKMTO says a vessel sustained significant damage and lost all propulsion after being attacked by 5 rocket grenades, 51NM West of Yemen's Hodeidah; vessel is under continuous attack and authorities are investigating.

- Ceasefire talks with Gaza have recommenced, in Doha, via journalist Elster (08:49BST/03:49ET).

RUSSIA-UKRAINE

- US President Trump said they have to send more weapons to Ukraine and that they have to defend themselves, while the Pentagon later announced the Department of Defense will send additional defensive weapons to Ukraine.

OTHER

- German Foreign Ministry says the Chinese Military has used a laser to target a German aircraft in EU operation aspides; Chinese ambassador summoned,

CRYPTO

- Bid, but in familiar ranges. For Bitcoin, holding at the upper-end of a USD 107.5k to 108.5k band.

APAC TRADE

- APAC stocks mostly traded with cautious gains as participants digested the latest trade-related developments including US President Trump's tariff letters to 14 countries so far including Japan, South Korea, South Africa, and Thailand with tariff rates ranging between 25%-40% and warnings against retaliation, although he also signed an Executive Order to delay the tariff deadline to August 1st.

- ASX 200 was indecisive as strength in tech and gold producers offset the losses in defensives, while an improvement in NAB Business Confidence was met with little fanfare as participants awaited the RBA rate decision which ultimately disappointed as the central bank defied the broad consensus for the first back-to-back cut since the pandemic, and instead decided to pause on rates through a 6-3 majority vote.

- Nikkei 225 recouped initial losses as recent currency weakness helped investors shrug off the tariff-related news with Japan facing a 25% tariff which is slightly higher than the 24% rate announced on Liberation Day.

- Hang Seng and Shanghai Comp were underpinned with the PBoC to support more onshore investors to invest in offshore bonds, while it will also expand the Bond Connect to include Chinese brokers, funds, wealth managers and insurers.

NOTABLE ASIA-PAC HEADLINES

- PBoC said it will support more onshore investors to invest in offshore bonds and will expand the bond connect to include Chinese brokers, funds, wealth managers and insurers, while it will also increase the quota under the swap connect.

- Chinese President Xi stressed developing the real economy to build up national strength and said the real economy should not be abandoned, nor should the traditional industries, according to Xinhua.

- Chinese Premier Li Qiang said China is confident in driving economic growth and has the resources to counter external headwinds.

- RBA unexpectedly kept the Cash Rate unchanged at 3.85% (exp. 25bps cut) with the decision made by a majority of 6-3 votes, while it stated that the Board will be attentive to the data and evolving assessment of risks to guide its decisions. RBA also noted that inflation has continued to moderate and the outlook remains uncertain although the Board continues to judge that the risks to inflation have become more balanced and the labour market remains strong. Furthermore, the Board remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply and it judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5% on a sustainable basis.

- RBA Governor Bullock says there will be more data and news by the next meeting. Made good progress on inflation, been within the target range for only one quarter thus far. Effect of 50bps of cuts is still to flow through. CPI interpretation was different to the markets, decision was about timing rather than direction; monthly CPI is too volatile, the quarterly figure could be higher. Confident they are on a path to ease further. On an easing path, timing is the question. Was an active debate within the RBA boardroom, the difference between the sides was not about direction. Bullock will not say how she voted.

DATA RECAP

- Australian NAB Business Confidence (Jun) 5.0 (Prev. 2.0); Conditions (Jun) 9.0 (Prev. 0.0)