US Market Open: European bourses gain on potential China stimulus, US stocks and USD lacklustre despite trade updates

10 Jul 2025, 11:40 by Newsquawk Desk

- European bourses began with modest gains and have gradually increased, largely led by reports of Chinese housing support.

- US futures are contained as newsflow has been limited, ex-China, since the overnight tariff developments.

- DXY is marginally firmer but well within Wednesday's band, G10s flat aside from Antipodeans benefiting from metals action and China support; BRL lags on 50% tariffs

- Fixed benchmarks have been gradually drifting from overnight highs, now essentially flat

- Base metals glean on reports of Chinese stimulus, precious peers also firmer though action has been more gradual

- Looking ahead, highlights include US Weekly Claims, Chinese M2/New Yuan Loans, Speakers including Fed’s Musalem, Waller & Daly, BoE’s Breeden, Supply from the US. Earnings from Delta & Conagra Brands.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- US President Trump announced a 50% tariff for Brazil and to initiate a Section 301 investigation on Brazil due to its "continued attacks on the Digital Trade activities of American Companies".

- US President Trump announced to impose a 50% tariff on copper effective August 1st after receiving a robust national security assessment, while he noted that copper is necessary for semiconductors, aircraft, ships, ammunition, data centres, lithium-ion batteries, radar systems, missile defence systems, and hypersonic weapons, which the US is building many of.

- EU is discussing car import quotas and export credits with the US in trade talks, according to sources cited by Reuters.

- Indonesia's Economy Minister said tariff discussions with US Commerce Secretary Lutnick and US Trade Representative Greer went positively. It was later reported that Indonesia and the US agreed to intensify tariff negotiations within three weeks to achieve optimal outcomes for both parties, while negotiations cover tariffs, non-tariff barriers, digital economy and commercial partnerships, according to the Economy Ministry.

- Philippine Economic Affairs Minister said they are concerned the US decided to impose 20% tariffs on Philippine exports and officials are to fly next week for talks with US counterparts,

- Indian Trade Official says Indian trade delegation to visit US soon for further trade talks.

- Vietnam said to be preparing new rules and penalties to crack down on trade fraud and illegal transhipments; focused inspections on Chinese products which face high tariffs in the US.

- South Korea Trade Minister says more time is needed for US trade talks; US expresses interest around cooperation in chips and shipbuilding.

EUROPEAN TRADE

EQUITIES

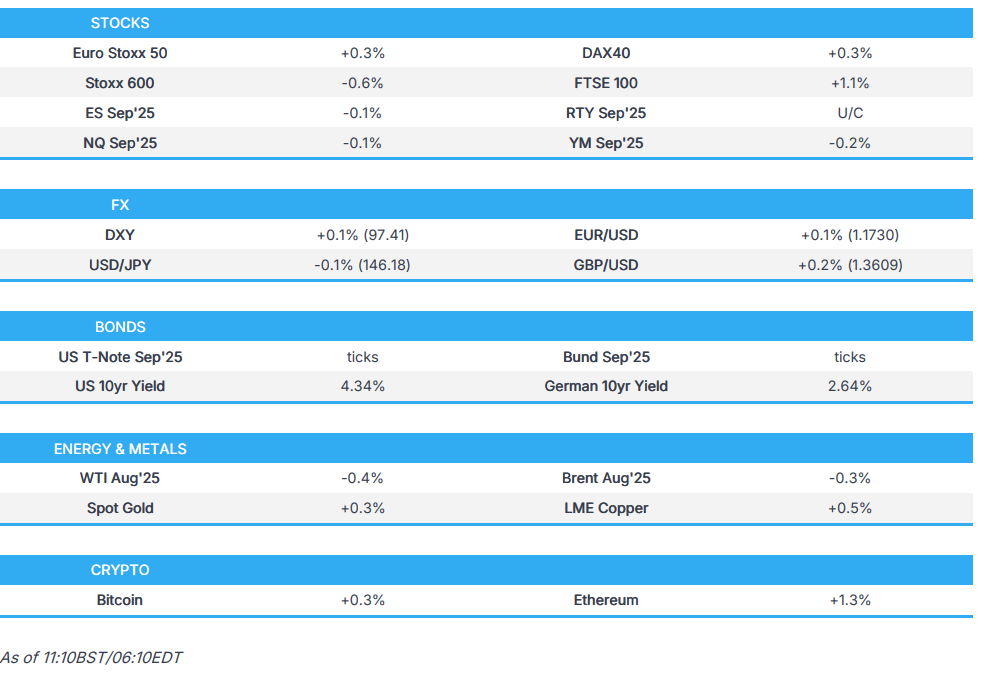

- European bourses began with modest gains, upside that has gradually and incrementally increased across the morning, Euro Stoxx 50 +0.3%. Region deriving strength from the boost seen in China-related stocks on recent reports around housing support.

- A narrative that has led to outperformance in the FTSE 100 +1.1%, given the large number of mining names in the region and associated benefit from touted China housing construction support.

- Sectors opened entirely firmer, though a few have drifted slightly into the red. Basic Resources lead, given the mentioned China stimulus. Tech benefits with ASML bolstered alongside gains in NVDIA on Wednesday and after TSMC revenue beat consensus. Those in the red are the more defensive ones, with Utilities currently lagging marginally.

- Stateside, futures are contained with newsflow after the early morning tariff updates limited, ES +0.1%; attention today on Fed speak, a few data points and a handful of earnings. Thus far, the numerous trade updates seem to have been overlooked by markets, with the TACO trade in play, as we await the all-important potential EU deal.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY contained but with a mild upward bias in a 97.271-97.469 range, vs Tuesday's 97.176-97.837 band. Specifics light thus far. On the Fed, ING wrote "Things can change a lot in the next three weeks, and our baseline call remains that the dollar will show significantly reduced interest in tariff noise. Data remains a bigger driver, and the potential FX impact of next week’s CPI figures still looks much bigger than trade news."

- EUR similarly uneventful in a thin 1.1715 to 1.1749 band, within Tuesday's 1.1682-1.1765. Commentary this morning includes European Commission President von der Leyen saying they are working non-stop to find a US agreement, to keep tariffs as low as possible.

- Havens flat. JPY and CHF contained in thin ranges. USD/JPY holding just above 146.00 but has been on either side of the figure at points. No move to Japanese PPI or remarks from various BoJ branch managers.

- Sterling a touch firmer despite a lack of newsflow, Cable in a 1.3587-1.3619 range at the time of writing, matching Wednesday's high before pulling back a touch. Ahead, BoE's Breeden scheduled on financial stability.

- Antipodeans firmer, AUD bolstered by ongoing gains in iron and copper prices with support emanating from speculation that a high-level meeting will be held next week to help revive the Chinese property sector, according to Bloomberg.

- Finally, the BRL lagged after Trump announced 50% tariffs and a Section 301 investigation.

- PBoC set USD/CNY mid-point at 7.1510 vs exp. 7.1757 (Prev. 7.1541)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained start to the day, awaiting fresh trade updates. USTs in a narrow 11-06+ to 111-13+ band, the upper point is a marginal WTD high. Resistance ahead at 111-28, 111-20+ and 112-12+ from last week.

- Ahead, aside from Fed speak and a few data points, 30yr supply rounds off the week’s outings. A tap that follows relatively average 3yr and 10yr issuance this week, with no sustained move spurred by US supply thus far.

- EGBs opened near-enough at highs and have been drifting since with specifics light aside from digestion of overnight trade updates. For Bunds, the peak is 130.08 and the benchmark is now down toward the 129.73 low, essentially flat on the day. No move to Final German CPI, unrevised.

- Gilts outperform, though are off best. Gapped higher and then lifted to a 92.19 peak early doors, seemingly a function of Gilts catching up to the strength seen in peers late-Wednesday. Since, with newsflow light from a few updates out of the ongoing US-France state visit (press conference expected later today), the benchmark has begun to conform to the gradual drift seen in above peers.

- Poland is considering JPY and CHF bonds, according to the Polish debt chief

- Click for a detailed summary

COMMODITIES

- Base metals firmer on Chinese stimulus hopes, amid speculation that a high-level Chinese meeting will be held next week to help revive the property sector.

- 3M LME Copper trades in a USD 9,635.20-9,711.15/t range at the time of writing., firmer but just off highs and back below the USD 9.7k mark.

- Precious metals also firmer, though gains are slightly more modest. XAU at a USD 3330/oz peak, seemingly deriving some further impetus above the USD 3.3k mark, benefitting from the contained USD with specifics otherwise very light thus far.

- WTI and Brent are in the red, came under a bout of pressure in the European morning though the magnitude of it keeps the benchmark within recent ranges. No move to remarks from the OPEC SecGen or the 2050 outlook from the organisation. Pressure this morning potentially a function of some constructive geopols, after President Trump said there is a chance this week or next of a Gaza ceasefire.

- WTI resides at the lower end of a USD 67.91-68.57/bbl range, similarly Brent in a USD 69.82-70.42/bbl.

- OPEC cuts world oil demand forecast for 2026-2029, peak demand not on the horizon.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK RICS Housing Survey (Jun) -7.0 vs. Exp. -8.0 (Prev. -8.0, Rev. -7)

- UK ONS, PPI Update: "We intend to reinstate full publication of our monthly PPI and quarterly SPPI bulletins in October 2025" and "So far, the development work is progressing well".

- UK ONS says in the week to 6 July 2025 compared with the previous week there were increases in: total Revolut debit card spending (+2% Y/Y), overall UK retail footfall (+1%). Decreases: ship visits to UK ports (-4%), flights (-3%).

- German HICP Final YY (Jun) 2.0% vs. Exp. 2.0% (Prev. 2.0%); MM (Jun) 0.1% vs. Exp. 0.1% (Prev. 0.1%)

NOTABLE EUROPEAN HEADLINES

- NBP's Wnorowski says another 25bps move is possible in September. Possible that there will only be one more rate adjustment in 2025.

- EU's von der Leyen survives no-confidence vote in EU parliament (as expected).

GEOPOLITICS

MIDDLE EAST

- Senior Israeli official said a Gaza ceasefire deal with Hamas may be possible within a week or two weeks but not in a day’s time, while Israel will offer a temporary ceasefire and if Hamas does not lay down its arms, Israel would proceed with military operations. Furthermore, the official said Israeli intelligence showed that before strikes on Iran, its enriched uranium was in Fordo, Natanz and Isfahan sites, while it has stayed there and has not been moved.

RUSSIA-UKRAINE

- US military is delivering artillery shells and mobile rocket artillery missiles to Ukraine, according to officials cited by Reuters.

- US State Department senior official confirmed that Secretary of State Rubio will meet with Russia's Foreign Minister Lavrov on Thursday on the sidelines of ASEAN.

- Drone said to have landed in the territory of Lithuania from Belarus. "Could be a jammed and diverted drone from this night's Russian assault against Ukraine, could also be a separate provocation, few details available", via a Lithuanian journalist on X.

CRYPTO

- Bitcoin is firmer, climbing above the USD 110k handle. Specifics light, as is the case elsewhere the complex awaits updates on the trade front.

APAC TRADE

- APAC stocks traded with a mostly positive bias following the gains on Wall St although some of the upside was limited as participants digested the latest batch of tariff letters and with underperformance in Japan due to recent currency strength.

- ASX 200 gained with the index led by strength in mining names due to recent upside in metal prices.

- Nikkei 225 bucked the trend amid headwinds from a firmer currency and following somewhat ambiguous Japanese PPI data.

- KOSPI outperformed despite the BoK's widely expected rate pause, while the central bank's language remained dovish as it maintained the rate cut stance and a majority of members were open to a cut in the three months ahead.

- Hang Seng and Shanghai Comp were marginally positive in quiet trade with little fresh macro drivers, although China's State Council recently issued a notice on stepping up support for employment and will support enterprises in stabilising jobs.

- TSMC (2330 TT) Q2 (TWD): Revenue 933.8bln (exp. 927.8bln), via a Reuters calculation; YTD sales +40% Y/Y, June sales +26.9% Y/Y.

NOTABLE ASIA-PAC HEADLINES

- BoK kept the base rate unchanged at 2.50%, as expected, with the rate decision unanimous, while it stated that it will maintain the rate cut stance to mitigate downside risks to economic growth and will adjust the timing and pace of any further base rate cuts. BoK said consumption is expected to gradually recover due to an improvement in economic sentiment and the supplementary budget but noted significant uncertainties concerning the pace of recovery in domestic demand and that future economic growth faces significant uncertainties concerning developments in trade negotiations with the US. BoK said it is to closely monitor changes in domestic and external policy environments and will examine the impact on inflation and financial stability. Furthermore, BoK Governor Rhee revealed that four board members were open to a rate cut in the next three months and two members saw the policy rate unchanged in the next 3 months, while he added that uncertainty is too high to say when to lower the interest rate and by how much.

- Gauge of Chinese property shares posting largest gain in nine months amid speculation a high-level meeting will be held next week to help revive the property sector, according to Bloomberg.

- BoJ Osaka Branch Manager says there is no big impact from US tariffs seen on Kansai Western Japan's economy for now; wage hike momentum likely to be sustained.

- BoJ's Nagoya Branch Manager says some firms are putting off capex plans. Auto exports to N. America are solid given robust demand, tariff impact is extremely high.

- Shanghai Securities Times, on Chinese CPI, reports "experts interviewed believe that CPI is expected to improve and show a trend of mild recovery from a low level".

DATA RECAP

- Japanese Corp Goods Price MM (Jun) -0.2% vs. Exp. -0.2% (Prev. -0.2%, Rev. -0.1%); YY (Jun) 2.9% vs. Exp. 2.9% (Prev. 3.2%, Rev. 3.3%)