US Market Open: Stocks subdued and DXY firm ahead of potential US/EU trade letter

11 Jul 2025, 11:20 by Newsquawk Desk

- US President Trump announced a 35% tariff for Canada and flagged a potential 20% blanket tariff for other countries; US is set to keep the tariff exemption for USMCA goods, according to a US official.

- Trump also noted the EU will receive a letter by Friday. Ahead of this, European bourses are in the red with sectors (ex-energy, post-BP) following suit.

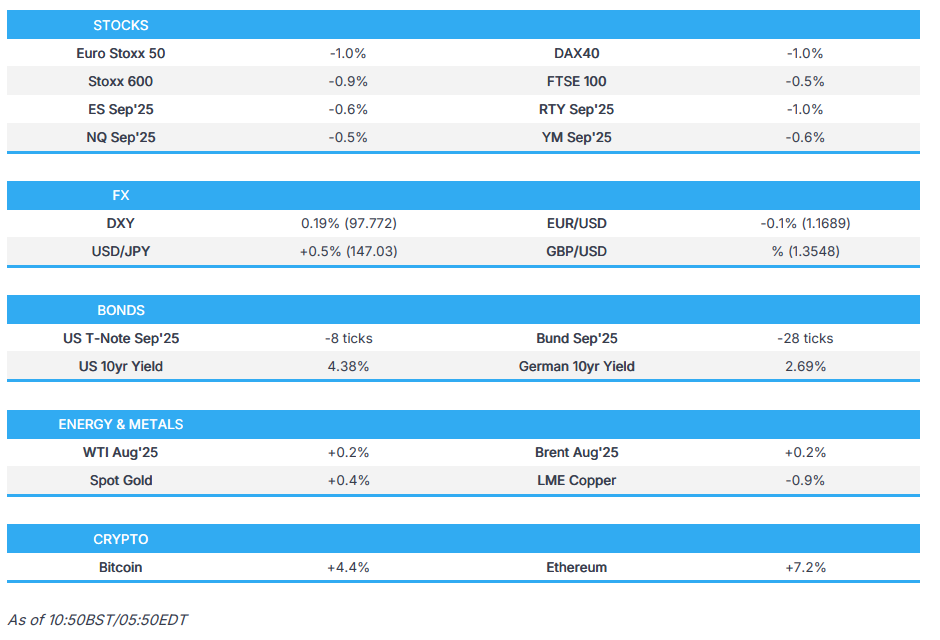

- Stateside, futures are lower into a docket headlined by potential trade developments, ES -0.6%.

- USD extends on its recent recovery, resilient to trade updates. DXY notched a 97.89 peak, G10s broadly under pressure with the JPY lagging.

- Fixed was lifted by the above updates, since pulled back and moved into the red, a pullback intensified by a hawkish interview with ECB's Schnabel.

- Choppy trade for crude awaiting developments on numerous in-play factors, precious metals glean from the risk tone while base peers are tarnished.

- Looking ahead, highlights include Canadian Jobs, Fitch on Germany, DBRS on Sweden, Speakers including ECB's Cipollone.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- US President Trump posted the tariff letter to Canada charging a 35% tariff on Canadian goods sent to the US starting August 1st separate from sectoral tariffs. US President Trump also said "we're just going to say all of the remaining countries are going to pay, whether it is 20% or 15%." He also noted the EU will receive a letter notifying them of new tariff rates by Friday.

- US President Trump is set to keep the tariff exemption for USMCA goods, according to a US official.

- White House Trade Advisor Navarro said the US will raise trillions from tariff revenue.

- Canadian PM Carney said throughout the current trade negotiations with the US, the Canadian government has steadfastly defended its workers and businesses, while it will continue to do so as it works towards the revised deadline of August 1st.

- Canadian tribunal finds steel dumping from China, South Korea, Turkey and Vietnam harming the domestic industry and finds reasonable indication that the subsidising of steel strapping from China is causing injury to the domestic industry.

- Proposed tariff of 50% on Brazil would halt the flow of Brazilian coffee to the US, according to Reuters citing trade sources.

- Chinese Foreign Minister Wang said China is ready to create new growth points with Thailand such as digital economy, artificial intelligence, cross-border e-commerce, and green development, while he noted regarding US tariffs, that he believes Thailand and ASEAN countries will safeguard their respective legitimate interests and resist unilateralism and bullying. Furthermore, he believes Southeast Asian countries have the ability to cope with a complex situation, stick to their principled positions, and safeguard their own interests and the common interests of all parties.

- US Secretary of State Rubio said had a "very constructive" meeting with China; odds are high for a meeting between US President Trump and Chinese President Xi. Does not have any date in mind for a Trump-Xi meeting. Obviously, there are some issues but going to have to work through them. US and China have to have relations and have to have communication.

- South Korea trade officials said the US is very reserved about including sectoral tariffs in a trade deal and has demanded that South Korea join efforts to curb China.

- Vietnam is said to be surprised by the 20% tariff and is seeking a lower rate, according to Bloomberg sources; Vietnam was surprised after pushing for tariffs in the 10-15% range.

- India said to be ready to offer concessions on non-ags products, according to Reuters sources; opposed to Australia's demand for more tariff cuts on dairy and wine for second phase of the trade pact

EUROPEAN TRADE

EQUITIES

- European bourses are in the red, Euro Stoxx 50 -1.0%; as traders de-risk and await trade updates after US President Trump suggested the EU would receive a letter sometime on Friday.

- Sentiment generally also dented by the higher-than-expected tariff on Canada and Trump stating nations that don't get a letter will be at 15% or 20%.

- Sectors follow suit with a negative bias. However, Energy bucks the trend bolstered by heavyweight BP after the Co. guided upstream production as likely being higher on the quarter. Laggards are primarily profit taking from the China-stimulus related gains seen on Thursdda, with Consumer Products & Services lagging.

- Stateside, futures are in the red, ES -0.5%. RTY -0.9% is faring the worst, pulling back after outperformance in small caps on Thursday.

- Specifics include: NVIDIA (-0.8%) CEO met Trump; Apple (-0.7%) plans new releases by early 2026; Cisco (-0.2%) takes CoreWeave (-2.6%) stake; Alphabet (-0.5%) to offer US govt discounts; DoJ clears USD 4.4bln T-Mobile (+0.7) deal with United States Cellular (+1.2); Levi Strauss (+7.2%) up after earnings, guidance.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD extends on its recent recovery, once again resilient to hostile trade updates relating to Canada and a possible blanket level as high as 20% for other nations. DXY is firmer, but contained towards the upper end of yesterday's 97.27-97.92 range.

- EUR continues to slip, EUR/USD back on a 1.16 handle but has found a bit of a floor ahead of 1.1650 with the current trough at 1.1666. Focus in the Eurozone is on an expected imminent announcement by the Trump administration after the President stated that the EU will receive a letter notifying them of new tariff rates by Friday.

- JPY under pressure once again, USD/JPY above 147.00. Pressure is primarily a by-product of the ongoing lack of progress for Japan in striking a trade deal with the US.

- Sterling in the red, hit by soft UK GDP which adds pressure on the Chancellor, who was already in a tricky fiscal position. GBP/USD as low as 1.3529, but held above the WTD trough from Tuesday at 1.3524.

- Antipodeans are softer. Given the USD strength and soft risk tone. Domestic drivers limited, as such the USD will likely continue to dictate. Softer auction occurs despite AUD/USD hitting a fresh YTD high at 0.6595 overnight before fading. Kiwi weaker, but holding just above 0.6000 vs the USD.

- PBoC set USD/CNY mid-point at 7.1475 vs exp. 7.1771 (Prev. 7.1510)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Benchmarks derived support from overnight Trump updates on Canada and a potential 20% tariff for those who do not have a deal. Thereafter, gradually faded from highs in the European morning awaiting a fresh catalyst before extending to lows in the period after a hawkish text from Schnabel.

- Specifically, USTs notched a 111-08 peak which was a few ticks shy of Monday’s 111-12+ best and the WTD high at 111-13+. While under pressure since and falling into the red the move remains relatively minimal in nature and comfortably in existing 110-21+ to 111-13+ WTD parameters.

- Bunds a repeat of the above, hit 129.74 early doors before gradually fading. An intensification of pressure occurred as ECB's Schnabel outlined that the bar to another cut is "very high", an view justified by the assessment that the ECB is already becoming more accommodative due to bank lending activity and a more resilient economy. Furthermore, noting that recent German fiscal measures may have also lifted the natural interest rate.

- Gilts followed suit, opened at 92.00 before lifting to a 92.08 peak. Seemingly acknowledging the overnight move in USTs and reacting to weaker-than-expected UK GDP. Since, this has faded with Gilts now well into the red, hit a 91.70 trough; pushed lower in tandem with Bunds but also potentially as participants digest the further pressure on Reeves' fiscal position from today's growth data.

- Italy sells EUR 8.75bln vs exp. EUR 7.50-8.75bln 2.35% 2029, 3.25% 2032, and 3.85% 2040 BTP.

- Click for a detailed summary

COMMODITIES

- Choppy trade for crude benchmarks, held an upward bias for much of the morning but are now near-enough flat in respective USD 66.64-67.20/bbl and USD 68.65-69.21/bbl ranges for WTI and Brent.

- Numerous factors in play, including: Trump guiding participants to a "major" Russia statement on Monday; European Commission reportedly to propose a floating Russian price cap, via Reuters; remarks from Israel's Netanyahu on Iran and other regional peers. Most recently, no move to reports that there have been no talks related to a possible OPEC+ pause of the increments, "all options are on the table for now," according to Kpler.

- Precious metals firmer, despite the strong USD. Havens propped up by the risk tone amid the latest bout of tariff uncertainty. XAU hit a USD 3343/oz peak after surpassing the 50-DMA at USD 3325/oz, now looks to USD 3345/oz from July 8th.

- Base metals are softer, reacting to the stronger USD, downbeat risk tone and ongoing renewed tariff uncertainty, 3M LME Copper -0.8%. In contrast, Dalian iron ore concluded the overnight session with gains in excess of 2%, seemingly amid speculation of a Chinese crackdown on steel overcapacity,

- Saudi crude oil supply to China is set to rise to about 51mln bbls in August which would be the highest since 2023, according to sources cited by Reuters.

- "According to 3 OPEC+ delegates there have been no talks related to a possible pause of the increments, all options are on the table for now.", via Kepler's Baker.

- IEA OMR: trims 2025 world demand growth forecast by 20k BPD to 700k BPD from 720k BPD; trims 2026 demand growth forecast by 20k BPD to 720k BPD from 740k BPD. World oil supply to rise by 2.1mln BPD in 2025 following latest OPEC+ hike (prev. forecast 1.8mln BPD rise).

- Shell (SHEL LN) has been granted environmental authorisation to drill up to five deep-water wells off South Africa's west coast, Reuters reports.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (May) -0.1% vs. Exp. 0.1% (Prev. -0.3%); YY 0.7% vs. Exp. 0.7% (Prev. 0.9%, Rev. 1.1%)

- UK GDP Est 3M/3M (May) 0.5% vs. Exp. 0.4% (Prev. 0.7%)

- French CPI (EU Norm) Final YY (Jun) 0.9% vs. Exp. 0.8% (Prev. 0.8%); MM (Jun) 0.4% vs. Exp. 0.4% (Prev. 0.4%)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer accepted the invitation to visit US President Trump during his trip to Scotland this month.

- UK Chancellor Reeves is considering recommendations by the IMF that are said to aim to reduce pressure for frequent fiscal policy changes, according to FT.

- ECB's Schnabel says there is no risk of a sustained undershooting of inflation over the mid term, the bar for another cut is very high, via Econostream. Would need material medium-term deviation from target to justify a cut, and a further rate cut is not appropriate. Fear of downward inflation pressure from euro ‘exaggerated’, pass-through to inflation from strong euro ‘limited’.

- ECB's Panetta says if downside growth risks reinforce the disinflationary process, ECB should continue easing policy.

- BP (BP/ LN) Trading Statement (USD): Q2 results expected to include post-tax impairment of USD 0.5-1.5bln, upstream production now expected to be higher in Q2 than Q1; Co. expects slightly lower net debt at the end of Q2 vs Q1. Sees stronger realised margins in the range of USD 0.3-0.5bln.

- Italy Economy Minister Giorgetti says it is following, with concern, signs of a credit contraction for companies; would not exclude that this is due to supply factors.

NOTABLE US HEADLINES

- Fed's Goolsbee (2025 voter) said the hard data on the economy was looking solid before April 2 Liberation Day tariffs but since then there has been potential disruption and ambiguity that the Fed needs to resolve, while he does not understand arguments the Fed should cut rates to make government debt cheaper and noted the mandate is on jobs and prices.

- Trump administration is reportedly backing away from abolishing FEMA, according to Washington Post.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said he hopes they can complete a deal within a few days, while he stated that Iran is now behind several years and they will get peace soon with Arab neighbours, according to an interview with Newsmax.

- Israeli army said a rocket was fired from southern Syria and landed near the Golan, according to Al Arabiya.

- Israel and Hamas reportedly inching closer to Gaza ceasefire deal, according to FT; yet to agree on the positioning of Israeli troops inside the shattered Palestinian enclave, according to sources.

RUSSIA-UKRAINE

- US President Trump said he is disappointed in Russia, but will see what happens over the next couple of weeks and thinks he’ll have a major statement to make on Russia on Monday. Trump said the US is sending weapons to NATO which it is going to give to Ukraine and NATO is paying 100%, while he expects the Senate to pass the sanctions measure and said they’re going to pass a very major and very biting sanctions bill, but it is up to the President whether or not to exercise it.

CRYPTO

- Bitcoin is bid and at highs this morning, with the crypto complex bolstered amid optimism around potential crypto-trading licences in China, and expectations that more firms will gain regulatory approval for crypto trading. Following a Shanghai regulator saying a meeting was held for local officials to consider strategic responses to stablecoins and digital currencies.

APAC TRADE

- APAC stocks were ultimately mixed as the initial impetus from the mostly positive lead from Wall St, where the S&P 500 notched a fresh record high, was dampened by the latest tariff updates after President Trump announced a 35% tariff for Canada and flagged a potential 20% blanket tariffs for other countries.

- ASX 200 failed to sustain its early momentum as gains in the mining, materials and resources sectors were offset by underperformance in real estate, consumer discretionary and tech, while there was a surge in Johns Lyng Group after it agreed to a takeover from a private equity group.

- Nikkei 225 was choppy as tailwinds from a weaker currency were counterbalanced by ongoing trade uncertainty.

- Hang Seng and Shanghai Comp were on the front foot despite the lack of obvious bullish catalysts although US Secretary of State Rubio and Chinese Foreign Minister Wang Yi are set to meet today in Malaysia at the sidelines of ASEAN.