US Market Open: ES -0.3%, FX and Fixed markets contained after Trump announced 30% tariff on EU and Mexico

14 Jul 2025, 11:30 by Newsquawk Desk

- US President Trump sent trade letters to the EU and Mexico announcing 30% tariffs from August 1st (separate from sectoral tariffs).

- The EU is planning to "step up engagement" with other nations impacted by US President Trump's tariffs, according to Bloomberg sources.

- European bourses hampered by US-EU trade developments, US futures also in the red but off worst levels.

- FX & Fixed markets contained as traders continue to look through Trump tariff threats.

- Crude modestly boosted by Iran comments, XAU helped by tariff updates.

- Looking ahead, US President Trump's Comments on Russia, ECB’s Cipollone.

TARIFFS/TRADE

- US President Trump sent trade letters to the EU and Mexico announcing 30% tariffs from August 1st which would be separate from sectoral tariffs.

EU

- US President Trump sent a trade letter to the EU announcing 30% tariffs from August 1st which would be separate from sectoral tariffs.

- US President Trump commented that the EU is talking to the US and wants to open up their countries.

- White House Economic Adviser Hassett said President Trump has seen some outlines of proposed trade deals and thinks they need to do better, while he added that these tariffs are real if Trump gets proposals that he doesn’t think are good enough.

- European Commission President von der Leyen said imposing 30% tariffs on EU exports would disrupt the essential transatlantic supply chains, while they remain ready to continue working towards an agreement by August 1st and will take all necessary steps to safeguard EU interests including the adoption of proportionate countermeasures if required. Furthermore, she said they will extend the suspension of their countermeasures to US tariffs until early August and noted they have always been clear that they prefer a negotiated solution with the US which remains the case.

- The EU is planning to "step up engagement" with other nations impacted by US President Trump's tariffs, according to Bloomberg sources. Nations include Canada and Japan and could lead to potential coordination.

- French President Macron said France fully supports the European Commission in the negotiations and shares the same very strong disapproval of the announcement of horizontal tariffs of 30% on EU exports.

- German Chancellor Merz said US tariffs of 30% would hit the German export industry to the core and they want to use the time until August 1st, while he stated that tariff letters were also US negotiating positions.

- German Economy Minister Habeck said the EU must pragmatically negotiate a tariff solution with the US that focuses on the main points of conflict and stated that new US tariffs would hit European exporters hard. Habeck also commented that new US tariffs would have a strong impact on the economy and consumers in Europe and the US.

- German Finance Minister Klingbeil said Trump’s tariff policies threaten the US economy at least as much as European companies, as well as stated that the tariff conflict must end and nobody needs new threats or provocations. Furthermore, he said the EU needs to continue serious and targeted negotiations with the US but must take decisive countermeasures if a fair negotiated solution is not successful.

- German trade industry association said the newly announced tariffs are part of US President Trump’s negotiating strategy and Europe must not be impressed by Trump’s announcements but must seek a solution in talks on an equal footing.

- Italian Foreign Minister Tajani says if a deal is not attained with the US, then the EU has a list of tariffs prepared against US goods worth EUR 21bln. In the face of US tariffs, the ECB should consider a new QE programme and rate reductions.

- EU Trade commissioner Sefcovic says will speak with US counterparts later today; must prepare well-balanced countermeasures against the US. US tariff plan is prohibitive for mutual trade, approaching a good outcome for both sides.

MEXICO

- US President Trump sent a trade letter to Mexico announcing 30% tariffs from August 1st which would be separate from sectoral tariffs.

- Mexican President Sheinbaum believes they will reach an agreement with the US before tariffs go into effect on August 1st, while she stated that Mexico’s sovereignty is not negotiable It was also reported that Mexico’s Economy Ministry said Mexico is negotiating and the working group with the US will aim for an alternative before August 1st to protect companies and employees.

OTHER

- Chinese Foreign Minister Wang said China and ASEAN agreed to submit a free trade zone pact in October for approval and signing, while they agreed on a five-year action plan with all-round cooperation in over 40 fields and will complete a consultation on the ‘code of conduct in the South China Sea’ within 2026.

- US President Trump said South Korea is seeking a trade deal.

EUROPEAN TRADE

EQUITIES

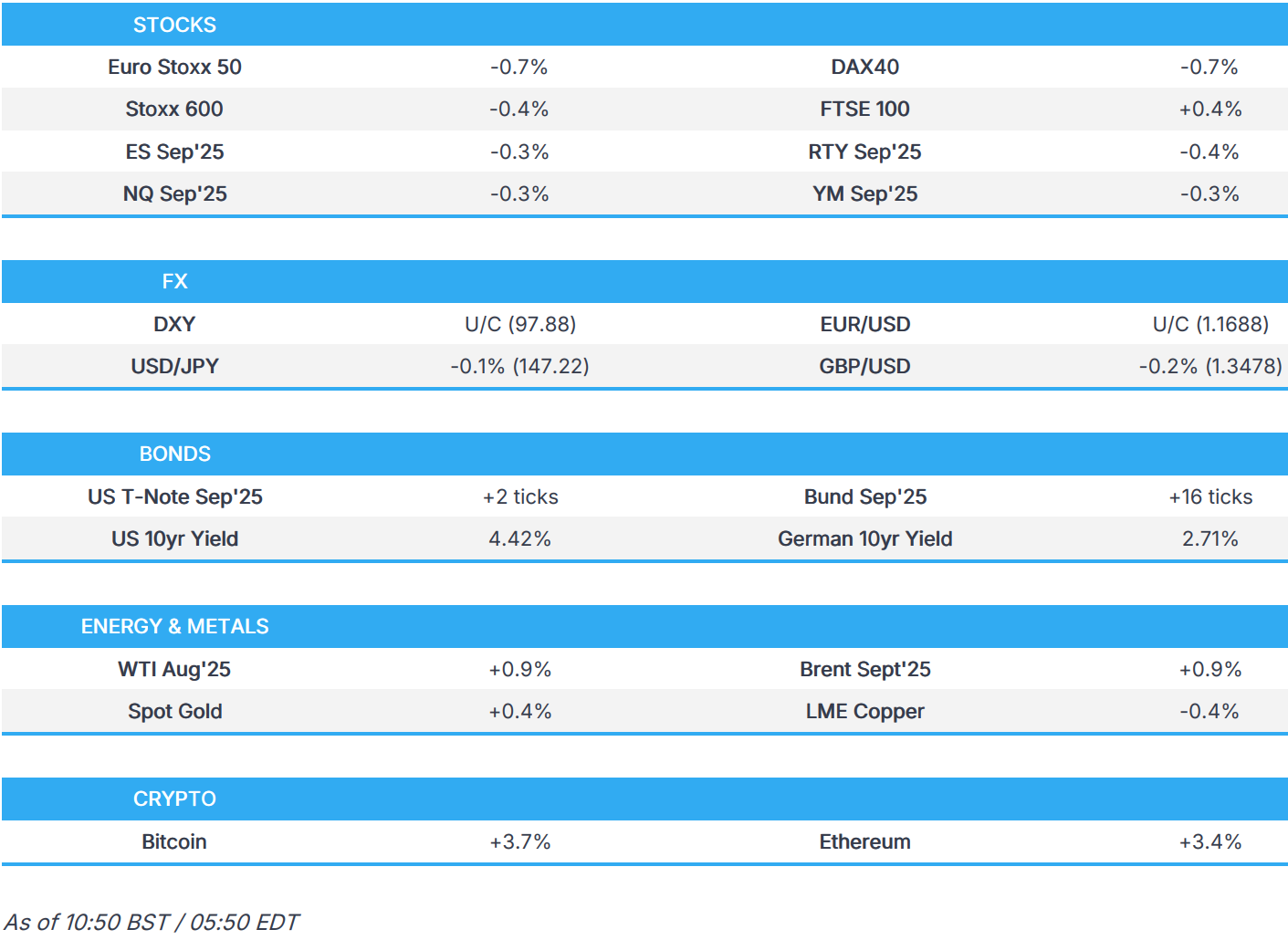

- European bourses (STOXX 600 -0.4%) have begun the week on the backfoot, after the US issued tariff letters to Mexico and the EU, threatening a 30% tariff rate, effective from August 1st.

- European sectors opened entirely in the red, though fare better now, with Healthcare and Basic Resources. The former boosted by upside in AstraZeneca (+1.4%) which benefits after its blood pressure related treatment met primary and secondary endpoints. Trade sensitive sectors such as Autos and Consumer Products sit at the foot of the pile.

- US equity futures (ES -0.3%, NQ -0.3%, RTY -0.4%) are moving in tandem with those in Europe. RTY is once again the underperformer, given the downbeat risk environment. We are off worst levels in the US, helped by earlier dollar strength which has since waned.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has kicked the week off on a steady footing following a solid showing last week. The macro narrative remains one dominated by the trade agenda after US President Trump sent trade letters to the EU and Mexico announcing 30% tariffs from August 1st. Despite some modest risk aversion this morning, the market remains of the view that eventual tariff rates will be notably below the currently proposed levels. DXY briefly made its way onto a 98 handle for the first time since 25th June with a current session high at 98.09.

- Despite a wobble in early European trade, the EUR has been resilient in the face of news that the US is to impose 30% tariffs on the EU from August 1st. Subsequently, EU Trade Commissioner Sefcovic says he will speak with US counterparts later today. However, he said the EU needs to prepare well-balanced countermeasures against the US.

- JPY is a touch firmer vs. the USD with the yen able to benefit from a very modest safe-haven bid and stronger-than-expected machinery order data. That being said, it is not lost on markets that a trade deal between the US and Japan does not appear to be close with Japanese negotiators looking to defend Japanese interests ahead of the Upper House elections due on July 20th. USD/JPY briefly made its way onto a 146 handle. However, the session low at 146.86 is some way off Friday's trough at 146.13.

- GBP is slightly softer vs. the USD and flat vs the EUR. Sentiment for the GBP remains negative with weekend commentary from BoE Governor Bailey adding to the bearishness after stating that the MPC is prepared to make larger rate reductions if the jobs market shows signs of a pronounced slowdown. Cable has slipped below the 1.35 mark (coincides with the 50DMA), delving as low as 1.3452; lowest since 23rd June.

- Antipodeans are both are softer alongside the soft risk appetite amid ongoing trade uncertainty and as participants digested Chinese trade data. After last week's RBA and RBNZ rate decisions, the sole scheduled highlight for the antipodes comes via Thursday's labour market metrics.

- PBoC set USD/CNY mid-point at 7.1491 vs exp. 7.1744 (Prev. 7.1475)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are contained. The bias from JGBs was a softer one after better-than-expected Machinery Orders data. USTs themselves in a thin 110-23+ to 110-28 band, entirely within but towards the trough of Friday's 110-22+ to 111-08 range. Newsflow has been focussed almost entirely on trade, after Trump delivered his EU letter, with European officials since indicating a desire to work towards a better outcome but outlining that countermeasures are being prepared. The relatively muted nature of moves thus far indicates that markets do not see the 30% tariff level as the likely end point and instead regard it as a negotiating tactic.

- Bunds opened higher by just under 10 ticks at 129.26 before meandering in a thin range and extending to a 129.41 peak at 07:00BST, no specific newsflow at the time and the move seemingly a function of the usual early-morning increase in activity. The jump of around 20 ticks over three minutes has since pared entirely with Bunds now back to Friday’s 129.17 close and essentially flat in a 129.11 to 129.41 band.

- Gilts opened a touch higher and then extended to a 91.85 peak, posting gains of around 15 ticks at best. Since, in-fitting with EGBs, the benchmark has pared from that high and is now essentially unchanged on the session in a 91.56-85 band. As has been the case recently, the UK is someone protected from direct trade updates owing to its deal with the US. However, newsflow is just as pronounced as the fiscal situation dominates domestically. Ahead, UK Chancellor Reeves is to speak.

- Click for a detailed summary

COMMODITIES

- WTI and Brent and currently trading higher by around USD 0.70/bbl and are just off session highs. Overnight, the complex traded with little direction given the lack of energy-specific newsflow and as geopolitical updates remained light. Brent Sept’25 currently trades towards the upper end of a USD 70.35-71.29/bbl range. The pick-up in the complex today stemmed from commentary via an Iranian Foreign Ministry spokesperson who highlighted that Tehran will respond to the return of UN sanctions after the snapback mechanism. Focus now turns to a “major statement” on Russia from US President Trump.

- Precious metals are firmer with some outperformance in spot silver, which continues to build on recent upside; XAG currently trading around USD 38.96/oz, briefly topping a 14-year high at USD 39/oz. Spot gold is a little firmer today, initially gapping higher at the open amid the risk deterioration sparked by the US letters to the EU. The yellow-metal currently trades in a USD 3,354.11-3,374.65/oz range.

- Base metals hold a negative bias, as traders digest the latest Chinese trade data which were mixed; exports beat expectations whilst imports continue to be dragged down by weaker commodities demand. 3M LME Copper is modestly lower and trades towards the lower end of a USD 9,623.8-9,703.6/t range.

- Iraq set August Basrah Medium Crude official selling price to Asia at plus USD 1.35/bbl vs Oman/Dubai, while it set OSP to Europe at minus USD 0.55 vs Dated Brent and set the OSP to North and South America at minus USD 1.15 vs ASCI.

- Australia's PM Albanese said they need to work together with China to address global excess steel capacity.

- Click for a detailed summary

NOTABLE DATA RECAP

- Swiss Producer/Import Price MM (Jun) -0.1% (Prev. -0.5%); Producer/Import Price YY (Jun) -0.7% (Prev. -0.7%)

NOTABLE EUROPEAN HEADLINES

- Japan and the EU are seeking to develop a joint satellite network, according to Nikkei.

- UK Chancellor Reeves is to hail fiscal ‘stability’ and City risk-taking in her Mansion House speech on Tuesday and will insist she has a grip on the UK economy and will not let borrowing run out of control, according to FT. CityAM also reports that she is to leave cash Isas untouched.

- BoE Governor Bailey says the MPC is prepared to make larger rate reductions if the jobs market shows signs of a pronounced slowdown, according to The Times.

- Netherlands rationed electricity to ease power grid stresses as thousands of businesses and households waited to connect to the Dutch grid, while officials and companies said lengthy waits for connections were holding up economic growth and could force businesses to rethink their investment plans, according to FT.

- Fitch affirmed Germany at AAA; Outlook Stable.

- UBS expects the ECB to cut rates by 25bps in September (prev. saw 25bps cut in July).

NOTABLE US HEADLINES

- US President Trump said to be directly involved in the USD 9.4bln rescissions measure, according to Semafor sources. "Senators are also bracing for him to erupt if the federal cuts fail, and the White House does not want the Senate to amend the package", a senior administration official told Semafor

- US President Trump said it would be a good thing if Fed Chair Powell quits and said that Powell should resign immediately, while he repeated criticism that Powell is too late.

- White House Economic Adviser Hassett said the Fed has a lot to answer for on renovation cost overruns and if there is cause to fire Fed Chair Powell, President Trump has the authority to do so.

- UK's King Charles will host US President Trump for a state visit from September 17th to 19th.

- NVIDIA (NVDA) CEO Jensen Huang is to hold a media briefing in Beijing on July 16th.

GEOPOLITICS

MIDDLE EAST

- Iran Foreign Ministry spokesperson says Tehran will respond to the return of UN sanctions after snapback mechanism. No date or location for US/Iran nuclear talks. Will not restart US talks unless we are certain they will work.

- Israeli official said talks in Doha are ongoing with Hamas for a ceasefire and hostage deal but noted Hamas is sticking to positions that do not allow mediators to advance an agreement.

- US envoy to the Middle East Witkoff said he is hopeful on Gaza ceasefire negotiations and was said to meet senior Qataris in New Jersey on Sunday.

- Iranian Foreign Minister Araghchi said they are carefully assessing options for talks with the US.

RUSSIA-UKRAINE

- US President Trump is considering greenlighting new funding for Ukraine to send a message to Russia, according to CBS. It was separately reported that President Trump is to announce an "aggressive" Ukraine weapons plan on Monday to arm Ukraine which is expected to include offensive weapons, according to Axios.

- EU envoys are nearing an agreement on lower Russian oil price cap, according to Reuters.

- Ukraine’s SBU intelligence agency accused Russia’s FSB of being behind the murder of an SBU Colonel in Kyiv last week and said agents responsible for the murder were killed during an operation to apprehend them.

- IAEA team at Ukraine’s Zaporizhzhia nuclear plant reported hearing hundreds of rounds of small arms fire on Saturday night.

- Russia’s Defence Ministry said Russian forces took control of Myrne and Mykolaivka in eastern Ukraine.

- North Korean leader Kim reaffirmed unconditional support for Moscow’s actions in the Ukraine war during a meeting with Russian Foreign Minister Lavrov, while North Korea and Russia pledged cooperation to safeguard each other’s territorial integrity. Furthermore, Russia expressed firm opposition to any attempt to undermine North Korea’s national security and sovereignty, while it was also stated that Moscow wants to further strengthen the strategic partnership.

- Ukrainian President Zelensky's Chief of staff says US Special Envoy Kellogg has arrived in Kyiv to discuss security and sanctions against Russia.

- Russian President Putin's envoy Dmitriyev says Russia-US dialogue will continue.

- Russia's Kremlin says it is obvious Ukraine is not in a hurry on peace negotiations, "we await timing of third round of talks".

OTHER

- North Korea warned it stands ready to take military action against threats from the US, Japan and South Korea following recent joint air drills involving a strategic US bomber, according to KCNA.

CRYPTO

- Bitcoin soars past USD 120k and sits a bit above USD 122k, as traders await "crypto week".

APAC TRADE

- APAC stocks were mostly positive but with some cautiousness seen following US President Trump's latest tariff letters in which he announced to impose 30% tariffs on the EU and Mexico from August 1st, while the region also reflected on somewhat mixed Chinese trade data.

- ASX 200 was rangebound as gains in mining, resources and materials offset the weakness in the consumer, industrial, financial and tech sectors, while data showed imports missed estimates for Australia's largest trading partner.

- Nikkei 225 initially retreated amid tariff uncertainty although the losses were gradually pared as sentiment overnight somewhat improved and Machinery Orders topped forecasts.

- Hang Seng and Shanghai Comp kept afloat amid the latest trade data in which exports topped forecasts and imports missed but returned to growth, while there were some encouraging comments from the meeting between US Secretary of State Rubio and Chinese Foreign Minister Wang last Friday which was described as constructive and with the odds said to be high for a future meeting between US President Trump and Chinese President Xi.

NOTABLE ASIA-PAC HEADLINES

- PBoC's Deputy Governor Zou Lan says they will continue to implement appropriately loose monetary policy Will support efforts taken to attain the FY growth target. To better use various structural tools to provide support to key sectors. To improve the market-based rate regime. Increased bond holdings by small banks within regulatory permits are permitted and reasonable. Such investment should be kept at a small level.

- BoJ is likely to increase its inflation forecast for fiscal 2025 but maintain consumer inflation forecasts for fiscal 2026 and 2027, according to sources cited by Reuters.

- Japan and the EU are seeking to develop a joint satellite network, according to Nikkei.

DATA RECAP

- Chinese Trade Balance (USD)(Jun) 114.8B vs. Exp. 109.0B (Prev. 103.2B)

- Chinese Exports YY (USD)(Jun) 5.8% vs. Exp. 5.0% (Prev. 4.8%); Imports YY (USD)(Jun) 1.1% vs. Exp. 1.3% (Prev. -3.4%)

- Chinese Trade Balance (CNY)(Jun) 826.0B (Prev. 743.6B)

- Chinese Exports YY (CNY)(Jun) 7.2% (Prev. 6.3%); Imports YY (CNY)(Jun) 2.3% (Prev. -2.1%)

- Japanese Machinery Orders MM (May) -0.6% vs. Exp. -1.5% (Prev. -9.1%); YY (May) 4.4% vs. Exp. 3.4% (Prev. 6.6%)

- Singapore GDP QQ (Q2 A) 1.4% vs Exp. 0.6% (Prev. -2.6%); YY (Q2 A) 4.3% vs Exp. 3.5% (Prev. 3.9%)