Europe Market Open: Europe primed for a firmer open ahead of Fed speak, US CPI and bank earnings

15 Jul 2025, 06:40 by Newsquawk Desk

- APAC stocks were ultimately mixed with the region indecisive in the aftermath of the latest Chinese GDP and activity data.

- European equity futures indicate a marginally higher cash market open with Euro Stoxx 50 future up 0.3% after the cash market closed with losses of 0.2% on Monday.

- DXY has given back some of yesterday's gains, EUR/USD remains on a 1.16 handle, other majors are contained.

- EU draws up retaliatory tariffs for US goods in case a trade deal is not reached, including aircraft and booze, according to WSJ.

- Crude futures remained subdued after US President Trump announced 100% tariffs on Russia and secondary sanctions on other countries that buy oil from Russia if a Ukraine deal is not struck within 50 days.

- The ECB is to discuss a more negative scenario next week than previously envisaged in June after Trump's latest tariff threat, according to Reuters.

- Looking ahead, highlights include EZ Industrial Production, German ZEW, US & Canadian CPI, OPEC MOMR, Bundesbank Monthly Report, Fed's Bowman, Barr, Barkin & Collins, BoE's Bailey & UK Chancellor Reeves, Supply from Germany, Earnings from JPMorgan, Blackrock, Wells Fargo, Citi and Ericsson.

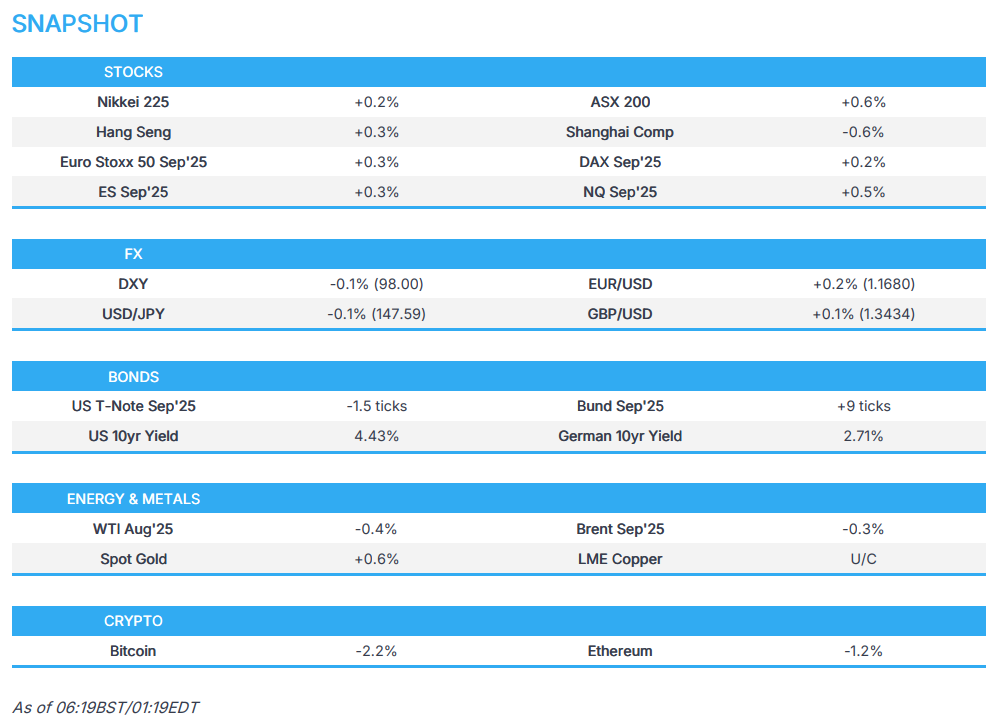

SNAPSHOT

US TRADE

EQUITIES

- US stocks closed with slight gains on Monday after gradually paring the weakness overnight in response to Trump's 30% tariff letters to the EU and Mexico. Sectors were mixed as communications and financial stocks outperformed but Energy and Materials lagged, while the underperformance in Energy tracked the move lower in crude prices after US President Trump announced a 100% tariff on Russia, and secondary sanctions on nations that buy Russian oil if a peace deal is not agreed to within 50 days. This allows time for negotiations and averts any imminent action from the US against Russia, which in turn, weighed heavily on the energy complex.

- SPX +0.14% at 6,269, NDX +0.33% at 22,856, DJI +0.20% at 44,460, RUT +0.67% at 2,250.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said he will talk to countries on tariffs and is open to trade talks including with Europe, while he added the EU is coming over to discuss trade.

- US Commerce Secretary Lutnick and USTR Greer are set to meet with GOP members of Ways & Means this week to talk about the latest trade negotiations, according to Punchbowl and Politico.

- US Department of Commerce announced it is withdrawing from and terminating the 2019 agreement suspending anti-dumping duty investigation on fresh tomatoes from Mexico, while it is issuing an anti-dumping duty order, resulting in duties of 17.09% on most imports of tomatoes from Mexico.

- Mexico's Economy Ministry rejected the US decision on tomato duties which it considered unfair and against the interests of both Mexican producers and US industry, while it will support local tomato producers to seek a deal under which the duty is suspended.

- EU draws up retaliatory tariffs for US goods in case a trade deal is not reached with aircraft and booze among imports targeted as EU debates how to respond to Trump’s latest trade threats, according to WSJ.

- Japanese PM Ishiba and trade negotiator Akazawa are to meet with US Treasury Secretary Bessent during his trip to Japan, while the meeting is being considered for July 18 in Tokyo, according to Yomiuri.

- Japan's Economy Minister and trade negotiator Akazawa said Japan is still arranging the makeup of attendees for the US National Day at Osaka Expo, while he added they will continue dialogue through various channels to seek an agreement with the US on tariffs.

- India and the US were reported to finalise an interim trade pact with GM crops rejected and tariffs rationalised, according to Times Now.

NOTABLE HEADLINES

- Fed Chair Powell responded to Senate Banking Chair Scott and Senator Warren regarding building renovations in which he stated the inspector general had full access to project information and receives monthly reports, while he has asked the board's inspector general to take a fresh look at the project, according to Politico and Reuters.

- US President Trump reiterated criticisms of high interest rates in the US and said the Fed should lower rates to less than 1%.

- White House economic adviser Hassett is rising in the race for next Fed chair, according to the Washington Post.

APAC TRADE

EQUITIES

- APAC stocks were ultimately mixed with the region indecisive in the aftermath of the latest Chinese GDP and activity data, while participants also awaited CPI data and the start of earnings season stateside.

- ASX 200 gained with strength in tech and some defensive sectors, while the positive sentiment was also facilitated by an increase in Consumer Confidence and as Australian PM Albanese met with Chinese President Xi.

- Nikkei 225 traded indecisively following recent currency weakness and rising JGB yields.

- Hang Seng and Shanghai Comp diverged following the somewhat mixed tier-1 data releases from China in which GDP figures for Q2 and Industrial Production in June topped forecasts but Retail Sales and Fixed Assets Investments disappointed, while House Prices were varied and continued to contract.

- US equity futures (ES +0.2%, NQ +0.4%) were briefly boosted overnight on reports that NVIDIA expects to resume H20 GPU sales to China after receiving assurances from the US government that licences will be granted, although some of the advances were pared with participants now awaiting US CPI data and the large banks to kick-start earnings season.

- European equity futures indicate a marginally higher cash market open with Euro Stoxx 50 future up 0.3% after the cash market closed with losses of 0.2% on Monday.

FX

- DXY marginally softened in rangebound trade and gave back some of the prior day's mild gains which were facilitated by the recent Trump tariff threats although he has since commented that he is open to trade talks including with Europe and that the EU is coming over to discuss trade. Furthermore, Trump reiterated his criticisms of high interest rates in the US and said the Fed should lower rates to less than 1%, while the attention now turns to incoming US CPI data and with several Fed speakers also scheduled later today.

- EUR/USD eked slight gains but with price action contained following yesterday's choppy performance and with sources noting that the ECB is to discuss a more negative scenario next week than previously envisaged in June after Trump's latest tariff threat, but is still seen as holding rates at the meeting with policymakers reluctant to act on a threat alone and any ECB rate cut discussion remains pushed back to September.

- GBP/USD languished near the prior day's lows following the recent underperformance in cyclical currencies and with participants looking ahead to Chancellor Reeves's Mansion House speech today where she is set to 'rip up' red tape in financial services and announce a pensions savings review.

- USD/JPY took a breather from recent advances amid the indecisive sentiment seen in Tokyo trade and in the absence of any Japanese data releases.

- Antipodeans attempted to nurse some losses but were thwarted by the mixed risk appetite and a weaker yuan.

- PBoC set USD/CNY mid-point at 7.1498 vs exp. 7.1758 (Prev. 7.1491)

FIXED INCOME

- 10yr UST futures lacked demand following the recent choppy performance ahead of US CPI data.

- Bund futures were rangebound amid incoming supply including a EUR 5bln Schatz issuance later today followed by EUR 2.5bln of Bund issuances on Wednesday.

- 10yr JGB futures extended on their recent declines as Japanese yields edged higher amid increasing fiscal concerns and heading into the Upper House elections at the end of the week with the ruling LDP party's approval rating at its lowest since 2012.

COMMODITIES

- Crude futures remained subdued and extended beneath the prior day's lows with pressure seen in the aftermath of US President Trump's announcement to impose 100% tariffs on Russia and secondary sanctions on other countries that buy oil from Russia if a Ukraine deal is not struck within 50 days.

- Spot gold attempted to regain composure after recent declines albeit with the upside gradual amid an uneventful dollar heading into the latest CPI data stateside.

- Copper futures saw two-way trade as participants digested the latest tier-1 economic releases from China including GDP and activity data, as well as reports that NVIDIA expects to resume H20 GPU sales to China.

CRYPTO

- Bitcoin retreated beneath the USD 117k level in a continuation of the pullback from yesterday's record high north of the USD 122k level.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi met with Australian PM Albanese and said it is most important to seek common ground while sharing differences and that China is ready to work with the Australian side to push bilateral ties further and make great progress. Furthermore, Australian PM Albanese said in the meeting with Chinese President Xi that they welcome progress on cooperation on free trade and value their relationship with China, while he added they will continue to approach the relationship in a calm and consistent manner guided by their national interest.

- China's stats bureau spokesperson reiterated that the economic foundation needs to be consolidated and stated that overall economic performance in H1 was stable with steady progress, although structural contradictions within the economy have not been fundamentally alleviated. The stats bureau official stated that domestic demand as a contribution to economic growth has been a driving force for GDP but noted that they need to improve investment structure and environment, while the real estate market is heading towards stabilisation and policy support to boost consumption in H1 should sustain spending in H2. Furthermore, it was stated that China is at a critical moment in improving consumption structure and it will supplement policy support with measures to ensure a stable operation of the economy.

- China held its urban work conference and will vigorously promote the optimisation of urban structure, while it will pay more attention to overall urban planning and make efforts to build innovative cities with vitality, according to Xinhua.

- Japan and the EU will issue a joint statement to strengthen economic alliance with a focus on trade, tech and supply chain coordination, according to Yomiuri.

DATA RECAP

- Chinese GDP QQ SA (Q2) 1.1% vs. Exp. 0.9% (Prev. 1.2%)

- Chinese GDP YY (Q2) 5.2% vs. Exp. 5.1% (Prev. 5.4%)

- Chinese Industrial Production YY (Jun) 6.8% vs. Exp. 5.7% (Prev. 5.8%)

- Chinese Retail Sales YY (Jun) 4.8% vs. Exp. 5.4% (Prev. 6.4%)

- Chinese Urban Investment (YTD)YY (Jun) 2.8% vs. Exp. 3.6% (Prev. 3.7%)

- Chinese House Prices MM (Jun) -0.3% (Prev. -0.2%)

- Chinese House Prices YY (Jun) -3.2% (Prev. -3.5%)

GEOPOLITICS

RUSSIA-UKRAINE

- US President Trump said he felt they had a deal on Ukraine about four times, while he added that Patriot batteries will be sent within days and will start arriving soon.

- White House official clarified that President Trump means he will impose 100% tariffs on Russia and secondary sanctions on other countries that buy oil from Russia if a deal is not struck within 50 days.

- US Senate Majority Leader Thune signalled the push for an imminent Russia sanctions vote will wait until President Trump gives the go-ahead and said the bill will be ready “at a minute’s notice", according to CNN's Raju.

EU/UK

NOTABLE HEADLINES

- BoE Governor Bailey stated in a letter to G20 finance ministers and central bank governors that they have seen further economic and geopolitical risks crystallise and global debt vulnerabilities remain high. Bailey added that uncertainty continues to weigh on growth expectations and they need to remain vigilant to the risk of disruptive market moves.

- ECB is to discuss a more negative scenario next week than previously envisaged in June after Trump's latest tariff threat, according to Reuters citing sources. However, the ECB is still seen as holding rates at the July 24th meeting as policymakers are reluctant to act on a threat alone and any ECB rate cut discussion remains pushed back to September.

- EU proposes a budget shake-up to shift billions of farm and development funds to eastern states, with Brussels to unveil a new way to allocate over EUR 750bln of EU farming and development funds, shifting the common budget to favour newer member states and those bordering Russia, according to FT citing a leaked proposal.

- French PM Bayrou is to outline a plan today to narrow France's deficit, which could risk triggering another government collapse, according to Bloomberg.

DATA RECAP

- UK BRC Retail Sales YY (Jun) 2.7% (Prev. 0.6%)

- UK BRC Total Sales YY (Jun) 3.1% (Prev. 1.0%)

- Barclays UK June Consumer Spending -0.1% Y/Y (Prev. +1.0%)