US Market Open: NVIDIA +5% pre-market as it resumes H20 shipments to China; US CPI and Fed speak ahead

15 Jul 2025, 11:20 by Newsquawk Desk

- EU draws up retaliatory tariffs for US goods in case a trade deal is not reached, including aircraft and booze, according to WSJ.

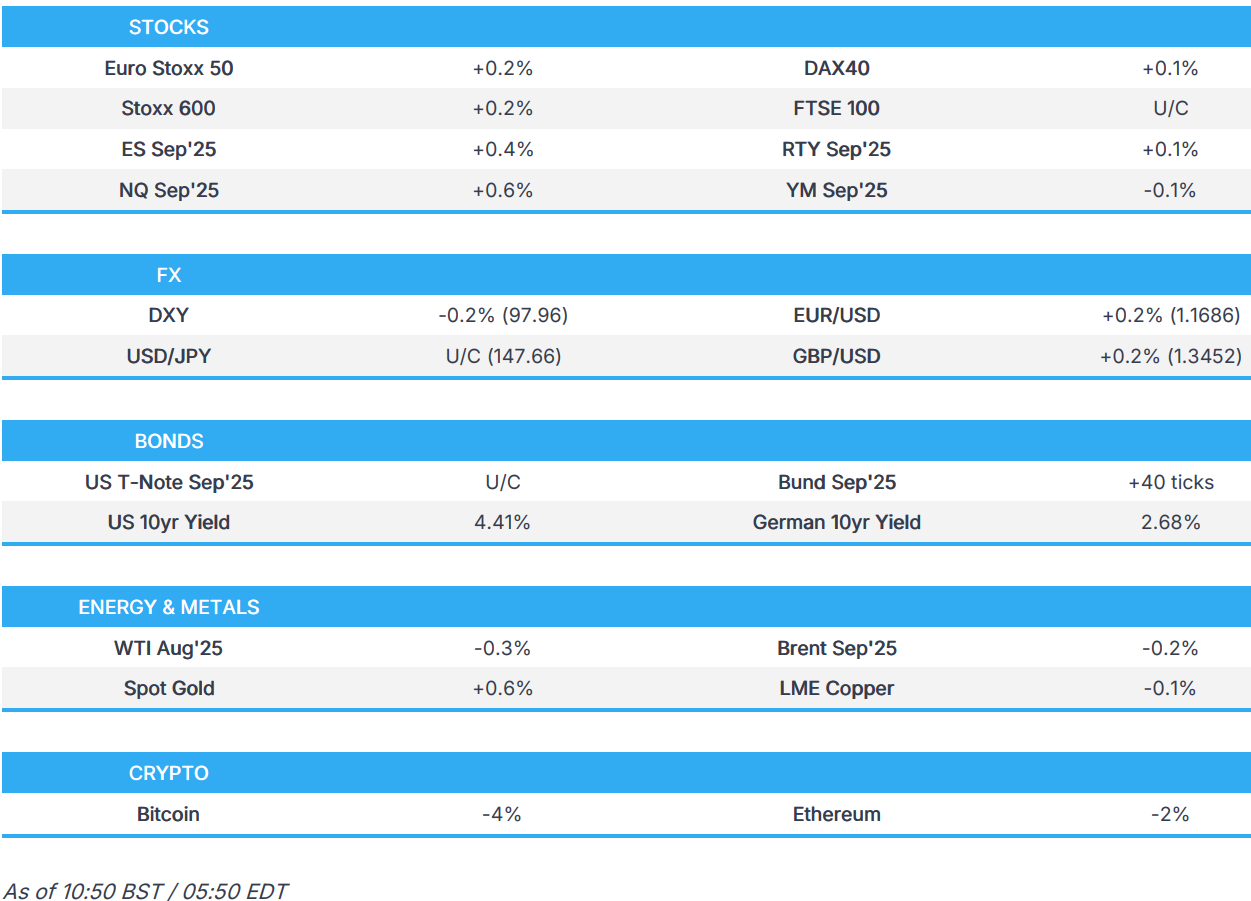

- European bourses are modestly firmer, US futures also gain with clear outperformance in the NQ boosted by NVIDIA.

- NVIDIA (+5% pre-market) to resume H20 sales to China and announces new, fully compliant GPU for China.

- USD a little lower into US CPI, Antipodeans top the G10 pile given the risk sentiment.

- USTs flat into CPI & Bowman, Bunds lead, OATs await Bayrou & Gilts await Bailey/Reeves.

- Crude lower but off worst levels on reports that Trump asked if Ukraine are able to hit Moscow with US weapons.

- Looking ahead, US & Canadian CPI, OPEC MOMR, Bundesbank Monthly Report, Speakers including Fed's Bowman, Barr, Barkin & Collins, BoE's Bailey & UK Chancellor Reeves. Earnings from JPMorgan, Blackrock, Wells Fargo, Citi.

TARIFFS/TRADE

- US Department of Commerce announced it is withdrawing from and terminating the 2019 agreement suspending anti-dumping duty investigation on fresh tomatoes from Mexico, while it is issuing an anti-dumping duty order, resulting in duties of 17.09% on most imports of tomatoes from Mexico.

- Mexico's Economy Ministry rejected the US decision on tomato duties which it considered unfair and against the interests of both Mexican producers and US industry, while it will support local tomato producers to seek a deal under which the duty is suspended.

- EU draws up retaliatory tariffs for US goods in case a trade deal is not reached with aircraft and booze among imports targeted as EU debates how to respond to Trump’s latest trade threats, according to WSJ.

- Japanese PM Ishiba and trade negotiator Akazawa are to meet with US Treasury Secretary Bessent during his trip to Japan, while the meeting is being considered for July 18th in Tokyo, according to Yomiuri.

- Japan's Economy Minister and trade negotiator Akazawa said Japan is still arranging the makeup of attendees for the US National Day at Osaka Expo, while he added they will continue dialogue through various channels to seek an agreement with the US on tariffs.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) are modestly firmer across the board, paring some of the pressure seen in the prior session but with gains capped ahead of today's key risk event, US CPI.

- European sectors hold a positive bias. Tech takes the top spot, with the chip sector boosted after NVIDIA (+5.0% pre-market) said it will resume H20 AI chip shipments to China. Telecoms is pressured by post-earning losses in Ericsson (-2.4%).

- US equity futures (ES +0.4%, NQ +0.6%, RTY +0.1%) are firmer today, with clear outperformance in the NQ, given the pre-market strength in NVIDIA shares (mentioned above). The RTY posts incremental upside into US CPI.

- Apple (AAPL) reportedly backs US President Trump's rare earth minerals push, according to Fox Business Apple and MP to build another factory in Fort Worth, Texas.

- NVIDIA (NVDA) CEO Jensen Huang met with President Trump and US policymakers this month, reaffirming Co.'s support for the administration effort to create jobs, while Co. expects licence to resume selling H20 GPU to China. To resume H20 sales to China, announces new, fully compliant GPU for China.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is giving back some of Monday's gains in quiet trade as markets await crucial CPI data for June. Core M/M CPI is expected to pick up to 0.3% from 0.1% with the Y/Y rate seen rising to 3.0% from 2.8%. The release will be parsed for any evidence that Trump's tariff policy is adding to price pressures in the US. DXY briefly made its way onto a 98 handle, matchings Monday's best at 98.12.

- EUR is firmer vs. the broadly weaker USD as markets await any material breakthrough in US-EU trade negotiations. On which, WSJ reports that the EU has drawn up retaliatory tariffs for US goods in the event a trade deal is not reached with aircraft and booze among the imports targeted. Elsewhere, it was reported that the ECB is to discuss a more negative scenario next week than previously envisaged in June after Trump's latest tariff threat, but is still seen as holding rates at the meeting. German ZEW data showed a better-than-expected improvement for the expectations and current conditions components but failed to have any sway on EUR. Elsewhere, French political risk could be a focus later today with French PM Bayrou to outline a plan to narrow France's deficit; will likely lead to calls for a vote of no confidence.

- JPY flat vs. the USD, halting a recent run of declines. Yen traders are still trying to assess the likelihood of an imminent US-Japan trade deal. Yen traders will also be mindful of the movements in the back-end of the Japanese curve, which, in part, has been supported by expectations of looser fiscal policy by Japan as a result of this weekend's election. USD/JPY ventured as high as 147.88 overnight before fading upside.

- GBP is a touch firmer vs. the USD and flat vs. the EUR. Newsflow surrounding the UK have been quiet at the start of the week given the UK has already secured a trade agreement with the US. However, newsflow is set to pick up with Mansion House text releases from BoE Governor Bailey and Chancellor Reeves due at 21:00BST today.

- Antipodeans are both towards the top of the G10 leaderboard on account of the bounce back in risk sentiment seen today. Both also digested mixed tier-1 data releases from China in which GDP figures for Q2 and Industrial Production in June topped forecasts, but Retail Sales and Fixed Assets Investments disappointed, while House Prices were varied and continued to contract.

- CAD is a touch softer vs. the USD in the run up to Canadian inflation metrics (coincides with the US release). As it stands, the BoC is currently on pause and avoiding forward guidance with the central bank taking a meeting-by-meeting due to economic uncertainty.

- PBoC set USD/CNY mid-point at 7.1498 vs exp. 7.1758 (Prev. 7.1491)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are flat and in narrow ranges ahead of US CPI. CPI is expected to pick up to 0.3% M/M in June (prev. 0.1%) for both the headline and core. While the Y/Y is seen at 2.7% (prev. 2.4%) and 3.0% (prev. 2.8%) for the headline and core respectively. A series that will be, primarily, scrutinised for any signs of tariff-induced price pressures.

- Bunds are leading peers, firmer by just under 50 ticks at best having peaked at 129.65 thus far. Upside that takes the benchmark to within reach of Friday’s 129.74 peak but leaves it shy of 130.00 and then multiple past peaks above, which continue all the way back to 131.95 from mid-June when the recent downward trend began. Outperformance potentially as the complex takes a breather from recent pressure and as traders digest reports the ECB will discuss a more negative tariff scenario at next week's meeting. No move in Bunds following the German ZEW figures, which were firmer-than-expected.

- OATs also firmer but to a lesser degree than Bunds. PM Bayrou from 15:00BST will begin presenting details of the 2026 budget. The goal will be cost savings of EUR 40bln by 2026, in order to bring the deficit-to-GDP ratio down to 4.6% vs the 5.4% projected for 2025, in-line with their fiscal commitments to the EU.

- Gilts are firmer, between USTs and Bunds in terms of magnitude. The immediate docket is light for the UK as we count down to the Mansion House speeches by BoE’s Bailey and Chancellor Reeves; the latter expected to announce a package amounting to the ‘biggest financial regulation reforms in a decade’. Into this, Gilts are at the upper-end of a 91.86 to 92.06 band. Notching a WTD peak and now eyeing 92.19 from last Thursday before that week’s 92.63 best.

- UK DMO sells GBP 1.0bln in 4.25% 2032 Gilts via tender: b/c 4.42x & avg. yield 4.161%.

- Germany sells EUR 3.899bln vs exp. EUR 5bln 1.90% 2027 Schatz: b/c 2.3x, average yield 1.87% and retention 22.02%.

- Click for a detailed summary

COMMODITIES

- WTI and Brent are currently lower in what has been a choppy session thus far; price action overnight was rangebound which continued into European hours where newsflow remained light up until a Trump-Russia related FT article. The report suggested that US President Trump asked Ukraine's Zelenskiy if Ukraine could hit Moscow if the US provided them with long-range weapons; the Ukrainian President replied with "absolutely...". This report sparked some modest upside, which then continued for around 30 minutes thereafter, taking Brent Sept'25 to a fresh session peak of USD 69.36/bbl.

- Precious metals are mixed, with slight gains seen in spot Silver/Gold whilst Palladium is a little lower. The yellow-metal currently trades towards the upper end of a USD 3,341.55-3,365.72/oz range, but with price action fairly muted ahead of US CPI. 3M LME Copper trades towards the mid-point of a narrow USD 9,602.33-9,656.5/t range.

- Base metals hold a negative bias, with incremental losses seen in 3M LME Copper prices as trades digest the latest Chinese GDP and activity metrics.

- Kazakhstan's PM Bektenov says they try to comply with OPEC+ commitments as much as possible. Not considering options to withdraw from the deal.

- China has lowered gasoline and diesel prices by CNY 130/ton and CNY 124/ton, respectively as of July 16th.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU ZEW Survey Expectations (Jul) 36.1 (Prev. 35.3)

- EU Industrial Production YY (May) 3.7% vs. Exp. 2.4% (Prev. 0.8%, Rev. 0.2%); Industrial Production MM (May) 1.7% vs. Exp. 0.9% (Prev. -2.4%, Rev. -2.2%)

- German ZEW Economic Sentiment (Jul) 52.7 vs. Exp. 50.3 (Prev. 47.5); ZEW Current Conditions (Jul) -59.5 vs. Exp. -66.0 (Prev. -72.0)

- UK BRC Retail Sales YY (Jun) 2.7% (Prev. 0.6%); Total Sales YY (Jun) 3.1% (Prev. 1.0%)

- Barclays UK June Consumer Spending -0.1% Y/Y (Prev. +1.0%)

- Spanish HICP Final YY (Jun) 2.3% vs. Exp. 2.2% (Prev. 2.2%); MM (Jun) 0.7% vs. Exp. 0.6% (Prev. 0.6%)

NOTABLE EUROPEAN HEADLINES

- BoE is announcing a "package of measures designed to maintain stability in the financial sector while offering new growth opportunities for mid-sized banks and building societies.".

- Incoming ECB member Radev says any further steps should remain firmly data dependent; I share the view that the threshold for additional rate cuts should remain high".

- UK Chancellor Reeves says under new reforms, banks will send investment opportunities to savers with cash sitting in low interest accounts for the first time. Govt will allow long term asst funds to be held in stocks and shares ISAs next year

NOTABLE US HEADLINES

- Fed Chair Powell responded to Senate Banking Chair Scott and Senator Warren regarding building renovations in which he stated the inspector general had full access to project information and receives monthly reports, while he has asked the board's inspector general to take a fresh look at the project, according to Politico and Reuters.

GEOPOLITICS

- US President Trump reportedly asked Ukrainian President Zelensky if Ukraine could hit Moscow in the scenario that the US provided long-ranged weapons, via FT citing sources; call that this conversation occurred within took place on July 4th. To the question from Trump, Zelensky reportedly replied, "Absolutely. We can if you give us the weapons." Trump reportedly signalled support for the idea, as a strategy to force Russia to the negotiating table. US president said to have encouraged Ukrainian leader to "step up deep strikes on Russia".

- Russian Kremlin says US President Trump's statement is serious and needs to be analysed Putin will comment on it if he deems it necessary. Decisions taken in Washington and Brussels are seen by Ukraine as a signal to continue the war. Russia is ready for a next round of talks with Ukraine. However, there have been no proposals for the Ukraine side so far.

- EU Foreign Representative Kallas says it is a good sign that the US appears to realise Russia does not want peace with Ukraine, hope the US will move forward with more sanctions against Russia.

- "Hamas member and leader Faraj al-Ghoul was killed in an Israeli raid", according to Al Arabiya.

CRYPTO

- Bitcoin is on the backfoot, giving back some of its recent advances; currently just above USD 117k.

APAC TRADE

- APAC stocks were ultimately mixed with the region indecisive in the aftermath of the latest Chinese GDP and activity data, while participants also awaited CPI data and the start of earnings season stateside.

- ASX 200 gained with strength in tech and some defensive sectors, while the positive sentiment was also facilitated by an increase in Consumer Confidence and as Australian PM Albanese met with Chinese President Xi.

- Nikkei 225 traded indecisively following recent currency weakness and rising JGB yields.

- Hang Seng and Shanghai Comp diverged following the somewhat mixed tier-1 data releases from China in which GDP figures for Q2 and Industrial Production in June topped forecasts but Retail Sales and Fixed Assets Investments disappointed, while House Prices were varied and continued to contract.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi met with Australian PM Albanese and said it is most important to seek common ground while sharing differences and that China is ready to work with the Australian side to push bilateral ties further and make great progress. Furthermore, Australian PM Albanese said in the meeting with Chinese President Xi that they welcome progress on cooperation on free trade and value their relationship with China, while he added they will continue to approach the relationship in a calm and consistent manner guided by their national interest.

- China's stats bureau spokesperson reiterated that the economic foundation needs to be consolidated and stated that overall economic performance in H1 was stable with steady progress, although structural contradictions within the economy have not been fundamentally alleviated. The stats bureau official stated that domestic demand as a contribution to economic growth has been a driving force for GDP but noted that they need to improve investment structure and environment, while the real estate market is heading towards stabilisation and policy support to boost consumption in H1 should sustain spending in H2. Furthermore, it was stated that China is at a critical moment in improving consumption structure and it will supplement policy support with measures to ensure a stable operation of the economy.

- China held its urban work conference and will vigorously promote the optimisation of urban structure, while it will pay more attention to overall urban planning and make efforts to build innovative cities with vitality, according to Xinhua.

- Japan and the EU will issue a joint statement to strengthen economic alliance with a focus on trade, tech and supply chain coordination, according to Yomiuri.

- China Commerce Ministry announces revisions to export control catalogue. Revises procedures for handling Gallium metal extraction tech. Adds battery cathode material prep tech to control list.

DATA RECAP

- Chinese GDP QQ SA (Q2) 1.1% vs. Exp. 0.9% (Prev. 1.2%); YY (Q2) 5.2% vs. Exp. 5.1% (Prev. 5.4%)

- Chinese Industrial Production YY (Jun) 6.8% vs. Exp. 5.7% (Prev. 5.8%)

- Chinese Retail Sales YY (Jun) 4.8% vs. Exp. 5.4% (Prev. 6.4%)

- Chinese Urban Investment (YTD)YY (Jun) 2.8% vs. Exp. 3.6% (Prev. 3.7%)

- Chinese House Prices MM (Jun) -0.3% (Prev. -0.2%); YY (Jun) -3.2% (Prev. -3.5%)