US Market Open: NQ underperforms after ASML (-8%) earnings, PPI, earnings and Fed speak ahead

16 Jul 2025, 11:00 by Newsquawk Desk

- US President Trump says he is working on five to six trade deals and there will probably be two to three deals by August 1st. Also notes that pharma tariffs will probably begin at month-end and initial tariffs on pharmaceuticals will be low

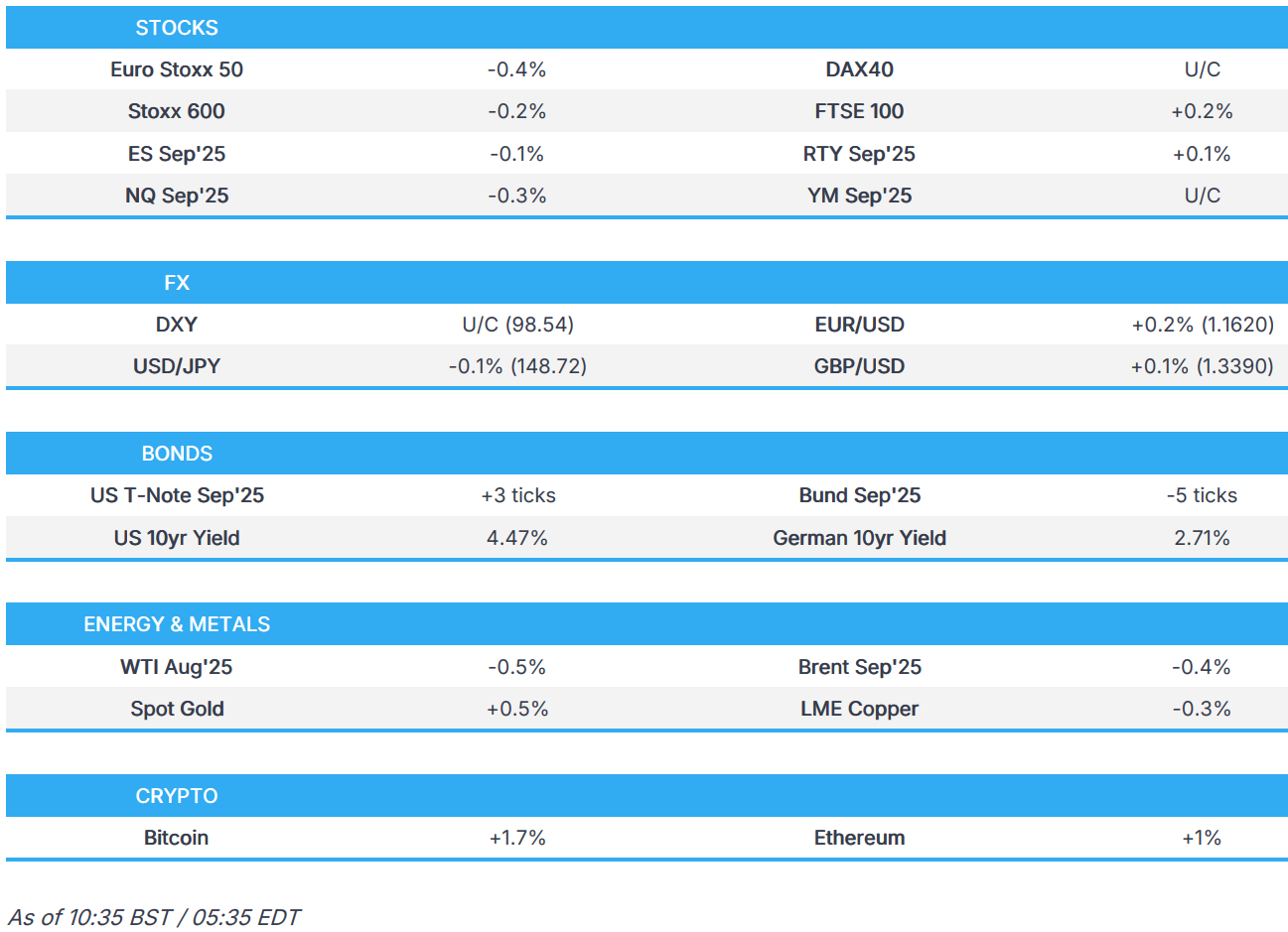

- European bourses are mixed having clambered off early morning lows, Autos/Tech lags following results from Renault and ASML.

- US equity futures trade on either side of the unchanged mark, NQ lags as it digests ASML’s results where it walked back on its 2026 growth outlook amid tariff uncertainty.

- DXY essentially flat awaiting US PPI, GBP digests hot inflation metrics.

- EGBs slightly heavy into the MMF, Gilts lag on CPI, USTs flat before PPI.

- Looking ahead, US PPI, Industrial Production & Capacity Utilisation, Speakers including Fed’s Barkin, Barr, Cook, Hammack, Logan, Kugler & Williams. Earnings from J&J, PNC, BAC, Goldman Sachs, Morgan Stanley.

TARIFFS/TRADE

- US President Trump they are working on five to six trade deals and there will probably be two to three deals by August 1st.

- US President Trump said pharma tariffs will probably begin at month-end and initial tariffs on pharmaceuticals will be low, while Trump also said they will release tariff letters for smaller countries soon and will probably set one tariff for all of them over 10%.

- US President Trump said a great deal for everybody was just made with Indonesia with Indonesia to pay 19%, while the US will pay nothing and similar deals are in the works. Trump later posted that "Indonesia has committed to purchasing $15 Billion Dollars in U.S. Energy, $4.5 Billion Dollars in American Agricultural Products, and 50 Boeing Jets, many of them 777’s."

- US Trade Representative announced the initiation of a Section 301 investigation of Brazil's unfair trading practices.

- China's Commerce Ministry said China and Australia signed a memorandum of understanding on the implementation and review of the China-Australia Free Trade Agreement.

EUROPEAN TRADE

EQUITIES

- European bourses opened mixed/mostly lower, but have traded with an upward bias throughout the European morning, to show a mixed picture.

- European sectors are mixed, with underperformance in Autos, dragged lower by post-earning losses in Renault (-16.4%) after it cut guidance; Stellantis (-4%) also moves lower after it halted its hydrogen fuel cell technology development programme. Tech has also been pressured by ASML (-8.7%) after its Q2 results; the Co. reported better-than-expected headline metrics, but guidance was light and the CEO said they cannot confirm growth in 2026.

- US equity futures (ES -0.1% NQ -0.3% RTY +0.1%) are modestly mixed and trade on either side of the unchanged mark, with underperformance in tech-heavy NQ as it wanes from Tuesday gains, along with underperformance in European tech names. Focus today on US PPI, Fed speak and a slew of earnings.

- NVIDIA (NVDA) CEO says Chinese supply chain is very advanced and sophisticated. Hopes to have a great future in China.

- Amazon (AMZN) has been removed from US 1 list at BofA

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

Earnings

- ASML -8.7%: Lowered Q3 rev., margin outlook, does not confirm 2026 growth target.

- Renault -16.2%: Provided dreary FY guidance, stressed poor retail market.

- Rio Tinto +1.2%: Pilbara iron ore output rise, copper production exp. at top of FY guidance.

- Richemont +0.5%: Q1 sales at constant FX rise.

- Sandvik -0.9%: mixed results, noted of strong momentum noted in mining, highest order intake ever in Q2

FX

- The dollar is giving back some of Tuesday's gains seen in the aftermath of US CPI data. Further inflation data is due today with Y/Y PPI expected to decline to 2.5% from 2.6%, M/M is expected to pick up to 0.2% from 0.1%. Once released, markets will be able to cement calls for the upcoming PCE report (the Fed's preferred inflation gauge). Today's Fed docket is a busy one with Barkin, Barr, Cook, Hammack, Logan, Kugler & Williams all due on deck. Note, the Fed Beige Book at 19:00BST will be parsed for the impact of Trump's tariff regime at a regional level. DXY sits towards the top end of Tuesday's 97.97-98.69 range.

- EUR is attempting to atone for Tuesdays’ losses, which saw EUR/USD slip onto a 1.15 handle for the first time since 25th June. French politics moved back into focus yesterday after PM Bayrou unveiled his plans to bolster France's finances. His outline was subsequently met with threats of no confidence from the hard left and far right. EUR/USD sits towards the bottom end of Tuesday's 1.1593-1.1692 range.

- JPY flat vs. the USD after a recent run of losses, which have lifted USD/JPY from the low seen on July 1st at 142.68 to a multi-month high today at 149.18. The main drivers for the move have been a broad pick-up in the USD and angst over the lack of trade progress between Japan and the US. The next upside level for USD/JPY comes via the 3rd April high at 149.33.

- GBP has seen some mild support in the wake of hotter-than-expected UK inflation metrics. Y/Y CPI unexpectedly advanced to 3.6% from 3.4% (exp. 3.4%) and the services metric held steady at 4.7% vs. expectations of a decline to 4.6%. Nonetheless, markets still expect the BoE to cut rates next month, but US Jobs data will be in focus on Thursday. Whilst Cable did briefly make its way back onto a 1.34 handle with a session high at 1.3416, the upside was limited by the aforementioned stagflationary outlook facing the UK.

- Antipodeans are slightly mixed vs. the USD with no obvious driver for the mild discrepancy. Newsflow surrounding both currencies remains light as markets await tomorrow's Australian jobs report.

- PBoC set USD/CNY mid-point at 7.1526 vs exp. 7.1914 (Prev. 7.1498)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are incrementally firmer/flat (whilst global peers are broadly lower). Currently in a in a very thin 110-08+ to 111-13+ band, awaiting PPI, Industrial Production and Fed speak. PPI will be scoured to see if the series’ internals are evident of tariff-driven price pressures emerging; a slew of Fed speakers are also due.

- Bunds are modestly lower today, but well off lows in a 129.19-56 band, matching Tuesday’s trough ahead of the 129.12 low from last Friday. The main event today for the bloc is the EU Multiannual Financial Framework (MFF) presentation, i.e. the bloc’s budget for the next seven years. As it stands, Commission President von der Leyen is scheduled to unveil it at 16:00BST.

- OATs are trading broadly in-line with peers, down by a handful of ticks. In French politics, PM Bayrou’s plan to save EUR 43.8bln from the budget in 2026 in order to get the debt-to-GDP ratio down, in-line with existing commitments/targets. The proposal has already drawn criticism from various political parties, unsurprisingly National Rally (RN) has said they will move to censure Bayrou if he does not change his plans.

- Gilts are underperforming, opened lower by 19 ticks and then slipped another 21 in short order to a 91.17 base. Notching a new WTD low and taking Gilts back to 91.16 from the first week of June. If breached, then we look to 90.11 from May as the next major point of support. Pressure emerged on the morning’s June inflation. A hotter-than-expected series, driven by motor fuel prices. While hotter, the series has only sparked a relatively modest move in BoE pricing with c. 1bps of implied easing removed from August and only around 3bps by end-2025.

- UK DMO sells GBP 1.5bln 4.5% 2034 Gilt: b/c 3.32x, average yield 4.553%, tail 0.4bps.

- Germany sells EUR 1.129bln vs exp. EUR 1.5bln 2.90% 2056 and EUR 0.8bln vs exp. EUR 1.0bln 1.25% 2048 Bunds

- Click for a detailed summary

COMMODITIES

- WTI and Brent are currently incrementally lower, and have held a negative bias throughout the European morning. Brent Sept’25 has traded in a very tight USD 68.46-69.09/bbl range, and ultimately awaiting US PPI.

- Precious metals are mixed with Palladium a little lower whilst spot Gold and Silver post modest gains. Newsflow has been relatively light today and Dollar price-action has been muted. The yellow-metal is seemingly attempting to pare back losses seen in the prior session. XAU/USD currently trades in a USD 3,325.21-3,342.49/oz range, with the low for today incrementally above its 50 DMA (3,323.42)

- Base metals are broadly lower continuing the downbeat mood seen overnight, in-fitting with the broader risk tone across the equities complex. 3M LME Copper currently trades towards the lower end of a USD 9,613.1-9,663/t range.

- US Private Sector Inventory data showed (bbls) crude +0.8mln (exp. -0.6mln), gasoline +1.9mln (-1.0mln), distillate +0.8mln (+0.2mln), according to Reuters citing sources.

- Gulf Keystone Petroleum has temporarily shut in production at the Shaikan field (capacity approx. 55k BPD) following reports over the past two days of explosions at several nearby oil fields.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK CPI YY (Jun) 3.6% vs. Exp. 3.4% (Prev. 3.4%); MM (Jun) 0.3% vs. Exp. 0.2% (Prev. 0.2%)

- UK Core CPI YY (Jun) 3.7% vs. Exp. 3.5% (Prev. 3.5%); MM (Jun) 0.4% vs. Exp. 0.2% (Prev. 0.2%)

- UK CPI Services YY (Jun) 4.7% vs. Exp. 4.60% (Prev. 4.70%); Services MM (Jun) 0.6% (Prev. -0.10%)

- UK ONS House Price Index (May): 3.9% Y/Y (prev. 3.5%)

NOTABLE EUROPEAN HEADLINES

- BoE Governor Bailey said multilateral institutions are essential for good policymaking and they are following financial stability risks closely, while he noted countries with big deficits typically come under most financial market pressure and he is yet to be convinced about the need for a retail CBDC.

NOTABLE US HEADLINES

- Fed's Logan (2026 voter) said the base case is that monetary policy needs to hold tight for a while longer to bring inflation down and she wants to see low inflation continue longer to be convinced, while she added that June CPI data suggests PCE inflation, which the Fed targets at 2%, will rise. Logan also commented that softer inflation and a weakening labour market could call for lower rates fairly soon and under the base case, the Fed can sustain maximum employment even with modestly restrictive policy. Furthermore, she said if the Fed misjudges and doesn’t cut soon enough, it could cut rates further to get employment back on track but also warned that cutting rates too soon risks deeper economic scars and a longer road to price stability.

- US President Trump is expected to sign an executive order in the coming days designed to help open up 401(k)s to private-market investments, according to WSJ.

- US Senator Cassidy said President Trump is to sign Fentanyl Act into law on Wednesday.

- US Defense Secretary Hegseth ordered the release of 2000 National Guard troops from the federal protection mission in LA.

GEOPOLITICS

MIDDLE EAST

- US President Trump's administration asked Israel to stop its strikes on Syrian military forces in the south of the country, while Israel promised that it would cease the attacks on Tuesday evening, according to a US official cited by Axios.

- US President Trump is to meet with the Qatari PM today to discuss negotiations over Gaza's ceasefire deal and are expected to discuss efforts to resume negotiations between the US and Iran to reach a new nuclear agreement, according to Axios.

- US, France and Germany agreed that Iran faces stiff sanctions if there is no deal by the end of August, according to Axios.

- Foreign tanker reportedly seized by Iran for 'smuggling' 2mln litres of fuel, according to SNN.

- Iranian Parliament issues statement saying negotiations with US cannot begin until preconditions are met, according to ISNA

RUSSIA-UKRAINE

- US President Trump said weapons are already being shipped to Ukraine and NATO will pay them back for everything and won't have boots on the ground, while he added that Iran wants to talk but he is in no rush to talk with Iran.

- Russia's Kremlin says subject of weapon supplies to Ukraine is high on agenda, via Ifax; phone call with US President Trump not planned but can be organised quickly, via Tass.

CRYPTO

- Bitcoin has found some footing after recent losses and sits just above the USD 119k mark.

- "House to try again today to clear procedural hurdle for defense bill and 3 crypto bills after conservatives blocked the rule yesterday", via Pergram on X

APAC TRADE

- APAC stocks were mostly subdued following the lacklustre handover from Wall St owing to an acceleration in US CPI data, while trade uncertainty lingered after President Trump suggested pharma tariffs could begin at month-end and tariff letters for smaller countries could be sent out soon.

- ASX 200 retreated with nearly all sectors in the red aside from tech and with miners not helped by the indecisive performance in Rio Tinto following its quarterly operations update in which it registered higher iron ore production but a decline in shipments Y/Y.

- Nikkei 225 traded indecisively in which the index swung between gains and losses amid the lack of pertinent drivers for Japan and some political concerns ahead of Sunday's upper house election as a recent poll showed the ruling bloc was at risk of losing its majority.

- Hang Seng and Shanghai Comp were mixed in the absence of any major fresh pertinent macro drivers and despite comments from China's Vice Premier He Lifeng who stated that China is accelerating the construction of a modern industrial system and is stepping up efforts to boost consumption.

NOTABLE ASIA-PAC HEADLINES

- China's Vice Premier He Lifeng said China is accelerating the construction of a modern industrial system and its industrial upgrading providing support to global industrial and supply chain operations, while He added China is stepping up efforts to boost consumption.

- Japan's ruling coalition risks losing a majority at the upper house election, according to Nikkei.