Europe Market Open: Europe primed for a firmer open on trade reports & earnings

17 Jul 2025, 06:40 by Newsquawk Desk

- US President Trump said they are very close to an India deal, could possibly make one with Europe & it is too soon to say re. Canada.

- US stocks finished higher but with volatile trade amid reports that Trump had drafted a letter to fire Powell; later, Trump denied this.

- DXY has regained some composure after getting hit on Fed independence concerns, G10s softer with AUD lagging after soft jobs data.

- USTs ease after Wednesday's upside, JGBs initially followed suit but picked up after the latest JGB liquidity auction.

- Crude remains afloat, XAU rangebound, base peers lack conviction in contained trade.

- Highlights include Australian Employment, UK Jobs, EZ HICP (Final), US Trade, Jobless Claims, Retail Sales & Atlanta Fed GDPNow, G20 Finance Ministers Meeting, Speakers including Fed's Kugler, Daly, Cook & Waller, Supply from Spain, France & UK, Earnings from Novartis, Publicis, Volvo, PepsiCo, GE, Abbott Laboratories, Netflix & TSMC.

- Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks ultimately finished in the green on what was a choppy session amid cooler-than-expected PPI data and mixed messages about Fed Chair Powell's future, with volatility triggered by several reports that US President Trump is looking to fire Fed Chair Powell and had drafted a letter, which Trump later refuted. Nonetheless, the major indices all closed higher and the Russell 2000 outperformed to atone for the prior day's weakness, while sectors mostly gained with outperformance in Health Care, Real Estate and Financials, while Energy, Communications and Consumer Discretionary lagged.

- SPX +0.32% at 6,264, NDX +0.10% at 22,908, DJI +0.53% at 44,255, RUT +0.99% at 2.227.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said they are very close to an India tariff deal and could possibly make a deal with Europe, while he stated regarding Canada tariffs that it is too soon to say, and he will probably put 10% or 15% tariffs on smaller countries.

- US President Trump said China has been helping with fentanyl. Trump commented that a deal with India may be coming up and they have some pretty good deals to announce, while they will probably live by the letter with Japan.

- Japanese trade negotiator Akazawa spoke with US Commerce Secretary Lutnick by phone, while Japan and the US reconfirmed each side's position on US tariff measures and engaged in deep interaction, according to Japan's government.

- EU reportedly stalls probe into Elon Musk's X amid US trade talks, according to FT.

- UK is said to be pushing the US to drop a key sticking point in the steel deal, according to FT.

- Canadian PM Carney said they continue to work for a US trade deal that works for Canadian workers, but noted that a deal is not yet on the table.

- Canada is to lower tariff-rate quota levels from 100% to 50% of 2024 volumes for steel products from non-free trade agreement countries.

NOTABLE HEADLINES

- Fed's Williams (Vice Chair) said current modestly restrictive monetary policy is appropriate and the current state of interest rate policy allows Fed time to analyse data, while he added that the tariff impact is modest so far but will increase over time and tariffs should boost inflation by one percentage point for the rest of 2025 into 2026. Furthermore, he said they will need to watch data to understand tariff impact he still needs to see more data before deciding what’s next for policy.

- Fed's Bostic (2027 voter) said he tries not to focus on news reports about the Fed, but on things that actually matter and stated that they may be at an inflexion point on inflation, and the most recent CPI suggests inflation pressures are building. Bostic commented he currently would wait on cutting rates, while he added that businesses said this is not a textbook tariff situation and are using different strategies for changing prices. Furthermore, he said it may be into 2026 before the full impact of tariffs on inflation is clear, as well as noted that inflation is not at the Fed's target and the Fed needs to preserve its credibility by meeting that goal.

- Fed Beige Book stated economic activity increased slightly from late May through early July and five Districts reported slight or modest gains, five had flat activity, and the remaining two Districts noted modest declines in activity (prev. half of Districts reported at least slight declines in activity). Furthermore, it stated that uncertainty remained elevated, contributing to ongoing caution by businesses.

- US President Trump reportedly drafted a letter to fire Fed Chair Powell and showed off a draft of the letter during a meeting with roughly a dozen House Republicans on Tuesday night, polling them as to whether he should do it and indicating that he likely would, according to sources. However, President Trump said shortly after that they are not planning on doing anything regarding Fed Chair Powell and get to make a change in 8 months, while Trump said he is not talking about firing Powell and it is highly unlikely that he will fire Powell unless there is fraud. Furthermore, he said the Fed board is not doing its job and noted that he has not drafted a letter.

- US President Trump said he would love if Fed Chair Powell resigned and noted it would disrupt markets if he removed Powell.

- US Senate GOP Banking committee member Tillis said firing a Fed chair over an economic decision would undermine US credibility and if the Fed Chair is fired, "you're going to see a pretty immediate response and we've got to avoid that".

- US President Trump's flip-flopping on firing Fed Chair Powell reflects divisions in the administration over his authority, according to FBN's Gasparino citing sources.

APAC TRADE

EQUITIES

- APAC stocks were somewhat mixed following the two-way price action stateside where the major indices ultimately gained, although price action was choppy amid Fed independence concerns due to reports regarding a potential firing of Fed Chair Powell, which President Trump refuted.

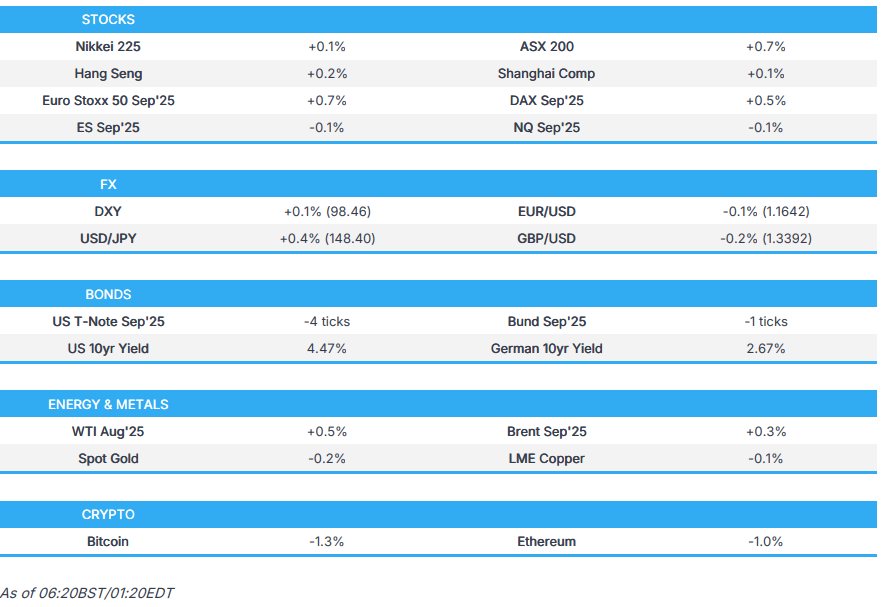

- ASX 200 advanced with gains seen in nearly all sectors while stocks were unfazed by disappointing Australian jobs data.

- Nikkei 225 declined at the open amid currency- and data-related headwinds but gradually clawed back its losses as the JPY resumed its weakening trend.

- Hang Seng and Shanghai Comp lacked conviction in the absence of any pertinent fresh macro catalysts.

- US equity futures were contained after recent mixed messages related to Fed Chair Powell's future, while participants await more Fed speakers, data releases and earnings.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.6% after the cash market closed with losses of 1.1% on Wednesday.

FX

- DXY regained some composure after weakening yesterday on Fed independence concerns, owing to reports that President Trump could fire Fed Chair Powell soon and had drafted a letter to fire Powell which he was said to have shown to House Republicans during a meeting on Tuesday. However, the dollar then rebounded off lows after Trump refuted the report and stated he is not talking about firing Powell and had not drafted a letter, while there were also several comments from Fed speakers but had little impact including from Williams who stated that current modestly restrictive monetary policy is appropriate and the current state of interest rate policy allows the Fed time to analyse data.

- EUR/USD was lacklustre after failing to sustain a brief surge to the 1.1700 territory with recent fluctuations at the whim of the Trump/Powell-related headlines.

- GBP/USD trickled lower to beneath the 1.3400 handle as participants awaited UK jobs and average earnings data.

- USD/JPY resumed its upward bias after rebounding from support near the 147.00 level amid a recovery in the dollar and mostly weaker-than-expected Japanese trade data.

- Antipodeans retreated with underperformance in AUD/USD following disappointing jobs data in which Employment Change missed forecasts owing to a contraction in Full-Time Employment and the Unemployment Rate unexpectedly climbed to its highest in three and a half years.

- PBoC set USD/CNY mid-point at 7.1461 vs exp. 7.1703 (Prev. 7.1526).

FIXED INCOME

- 10yr UST futures pulled back following yesterday's advances and curve steepening which were spurred by cooler-than-expected PPI data and Fed concerns.

- Bund futures took a breather after the mid-week resurgence and with a relatively light calendar in the EU aside from final HICP data and issuances from Spain and France.

- 10yr JGB futures were initially pressured despite the mostly weaker-than-expected trade data from Japan, but later rebounded following firmer demand at the enhanced-liquidity auction for long-to-super-long JGBs.

COMMODITIES

- Crude futures remained afloat following yesterday's intraday rebound which was facilitated by geopolitical tensions as Israel conducted strikes on southern Syria, while there were also reports of a drone attack on Iraq's Kurdistan oil field.

- Qatar set August-loading Al-Shaheen crude term premium at USD 2.48/bbl and raised September Al-Shaheen crude term price to USD 3.33/bbl above Dubai quotes, according to sources cited by Reuters.

- A drone attack reportedly targeted an oilfield in Iraqi Kurdistan, according to Reuters citing security sources.

- Spot gold traded rangebound after recently whipsawing on reports that President Trump is likely to fire Fed Chair Powell soon, which Trump refuted.

- Copper futures lacked conviction with price action rangebound amid the somewhat mixed overnight risk appetite.

CRYPTO

- Bitcoin mildly retreated overnight after failing to sustain a brief return to above the USD 119k level despite the House eventually advancing a trio of cryptocurrency bills following a recent standoff with GOP hardliners.

NOTABLE ASIA-PAC HEADLINES

- US is set to ban Chinese technology in submarine cables, while the measure aims to end key vulnerability in communications infrastructure after an attack on American telecoms, according to FT.

DATA RECAP

- Japanese Trade Balance (JPY)(Jun) 153.1B vs. Exp. 353.9B (Prev. -637.6B, Rev. -638.6B)

- Japanese Exports YY (Jun) -0.5% vs. Exp. 0.5% (Prev. -1.7%); Imports 0.2% vs. Exp. -1.6% (Prev. -7.7%)

- Australian Employment (Jun) 2.0k vs. Exp. 20.0k (Prev. -2.5k)

- Australian Full Time Employment (Jun) -38.2k (Prev. 38.7k); Unemployment Rate 4.3% vs. Exp. 4.1% (Prev. 4.1%)

GEOPOLITICS

MIDDLE EAST

- US Middle East Envoy Witkoff said Gaza negotiations are going well.

- Senior US official said they are very close to an agreement that will lead to halting the escalation between Israel and Syria, according to Axios' Ravid.

- New clashes broke out in Syria's Sweida city despite a ceasefire announcement, while it was also reported that a new Israeli airstrike hit a western suburb of Syria's Damascus, according to Reuters citing witnesses and local sources.

RUSSIA-UKRAINE

- Russian air defence units downed two Ukrainian drones headed for Moscow, according to the city's mayor. It was also reported that Russian air defence systems destroyed 122 Ukrainian drones overnight, according to RIA.

OTHER

- China-linked hackers are increasingly targeting Taiwan's chip industry, according to cybersecurity firm Proofpoint.

EU/UK

NOTABLE HEADLINES

- BoE's Mann said her view is that it will take some effort to get inflation down and without supply-side growth, demand is a sugar high, which does not end well. Mann also said that views differ on the MPC about where demand conditions really are and how they are playing out in the labour market, according to Business News Wales.