US Market Open: TSMC +4% pre-market after Q2 results; Tier 1 data, Fed speak and earnings ahead

17 Jul 2025, 11:25 by Newsquawk Desk

- US President Trump said they are very close to an India deal, could possibly make one with Europe & it is too soon to say re. Canada.

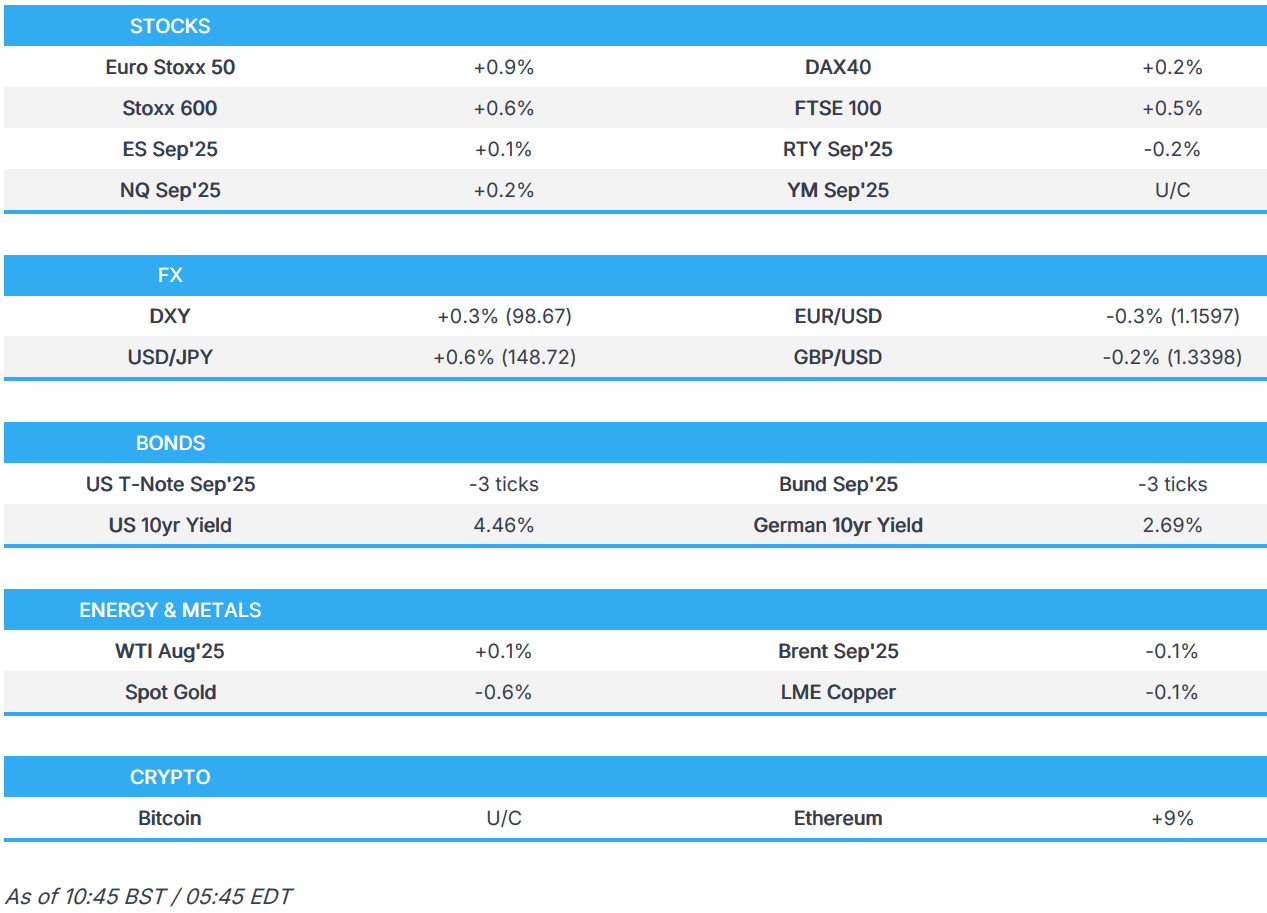

- European bourses broadly in the green, whilst US equity futures are mixed; TSMC +4% in pre-market trade after Q2 results.

- USD attempts to recover from Wednesday’s Powell/Trump drama; AUD underperforms post jobs data.

- Fixed benchmarks weighed on by the TSMC-driven risk tone, Gilts underperform after the UK’s job data which continued to show a weakening labour market but unlikely to change the BoE’s trajectory.

- Crude briefly boosted on reports of a drone attack on Iraq's Kurdistan oil fields; XAU modestly lower.

- Looking ahead, US Trade, Jobless Claims, Retail Sales & Atlanta Fed GDPNow, G20 Finance Ministers Meeting, Speakers including Fed's Kugler, Daly, Cook & Waller. Earnings from PepsiCo, GE, Abbott Laboratories, Netflix.

TARIFFS/TRADE

- US President Trump said they are very close to an India tariff deal and could possibly make a deal with Europe, while he stated regarding Canada tariffs that it is too soon to say, and he will probably put 10% or 15% tariffs on smaller countries.

- US Treasury Secretary Bessent to pay visit to Japanese PM Ishiba on Friday, according to Japanese government.

- EU is reportedly preparing a list of potential tariffs on US services alongside export controls, via FT citing sources; in the scenario that trade talks with the US fail. Brussels is also considering export controls if trade talks with Washington fail. One official made clear that the list would not only focus on US tech firms.

- Japanese trade negotiator Akazawa spoke with US Commerce Secretary Lutnick by phone, while Japan and the US reconfirmed each side's position on US tariff measures and engaged in deep interaction, according to Japan's government.

- Japanese Government says Top Tariff Negotiator Nakazawa is to travel to Osaka to host US delegation at expo on Saturday.

- EU reportedly stalls probe into Elon Musk's X amid US trade talks, according to FT.

- UK is said to be pushing the US to drop a key sticking point in the steel deal, according to FT.

- Canada is to lower tariff-rate quota levels from 100% to 50% of 2024 volumes for steel products from non-free trade agreement countries.

- Chinese Foreign Ministry says the responsibility with Fentanyl lies with the US itself, tariffs seriously impacted China's dialogue with the US on drug control.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.6%) opened firmer across the board and have traded sideways at elevated levels throughout the morning.

- European sectors hold a strong positive bias, with only a couple of industries holding marginally in negative territory. Industrials take the top spot, lifted by post-earning strength in ABB. Followed closely by Autos (post-earning strength in Volvo Car) and then Tech (TSMC results).

- US equity futures (ES +0.1% NQ +0.2% RTY -0.2%) are modestly mixed and trade on either side of the unchanged mark; the NQ is the incremental outperformer, with sentiment in the Tech sector boosted post-TSMC results. Docket ahead is headlined by US Retail Sales, Jobless Claims, Trade and Fed speak.

- Mastercard (MA) and Visa (V) are reportedly facing a class action claim in the UK over allegedly unlawful interchange fees paid by British businesses, via Sky News; case could be worth GBP 3bln. To be filed at the Competition Appeal Tribunal today.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

EARNINGS

- TSMC +4% pre-market: Q2 beat/above prior. Q3 Guide: Revenue 31.8-33.0bln (exp. 30.7bln), Operating Margin 45.5-47.5% (Q2 49.6%), Gross Margin 55.55-57.5% (Q2 58.6%). FY25 Guide: Revenue increase of +30% (prev. exp. mid 20s%). Commentary: more conservative about Q4 due to tariffs and other uncertainties; no change in customer behaviour so far, there is risk and uncertainty from tariffs, demand for chips will continue to be robust.

- ABB +6.4%: Rev. beat, guides strong growth.

- Volvo Car +5.5%: Rev beat, new EVs expected to have better margins, turnaround plan on track.

- Novartis -1.6%: Strong results, CFO to retire & Cosentyx misses sales exp.

FX

- After a volatile session on Wednesday, USD is attempting to recoup lost ground and resume its broader recovery seen since early July. A soft PPI report and sources that President Trump is set to fire Fed Chair Powell sent the Dollar lower; investors feared 1) the perceived likelihood of a lower FFR going forward and 2) the subsequent credibility loss in the US. Attention today will turn back to the data slate with retail sales and weekly claims both on deck. Elsewhere, TIC data due at 21:00BST will be eyed for any signs of foreign investors shunning US assets. Fed speak also on the agenda.

- It remains the case that the USD leg of the pair is providing the bulk of direction for EUR/USD with incremental drivers from the Eurozone on the light side. Traders await any breakthroughs in EU-US trade talks after US President Trump threatened a 30% tariff on the EU over the weekend. On the fiscal front, Germany has rejected the EU's proposed EUR 2tln budget, setting up a negotiation phase with the European Parliament and European Council. EUR/USD has slipped onto a 1.15 handle but remains within Wednesday's 1.1562-1.1772 range.

- After some fleeting upside vs. the USD on account of the Trump-Powell drama seen yesterday, USD/JPY has resumed its recent uptrend. The latest reporting noted that Japanese trade negotiator Akazawa spoke with US Commerce Secretary Lutnick by phone, while Japan and the US reconfirmed each side's position on US tariff measures and engaged in deep interaction. USD/JPY is currently tucked within Wednesday's wide 146.91-149.18 range.

- GBP softer vs. the USD but to a lesser extent than most peers. Macro focus for the UK has been on the labour market with the latest jobs data showing an unexpected uptick in the unemployment rate to 4.7% from 4.6%, another contraction in the HMRC payrolls change and stubborn wage growth. Cable has slipped back onto a 1.34 handle but is holding above Wednesday's low at 1.3365.

- Antipodeans have both have fallen victim to the USD with greater losses seen in AUD following the latest Australian jobs data. The release showed an unexpected jump in the unemployment rate to 4.3% from 4.1%; highest rate in 3.5 years. Accordingly, AUD/USD has slipped back onto a 0.64 handle and moved back below its 50DMA at 0.6491 with a session low at 0.6462.

- PBoC set USD/CNY mid-point at 7.1461 vs exp. 7.1703 (Prev. 7.1526).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are lower by a handful of ticks. Gradually drifting overnight after being driven to a 110-21+ peak in the US afternoon, a high that occurred in a continuation of the post-PPI move and as USTs picked up after the Powell reporting and subsequent pushback by Trump. Thus far, down to a 110-13 base which takes them back to roughly where they were before the first Powell reports hit. Today's focus will be on US data (Retail Sales, Jobless Claims, Atlanta Fed will update its GDPNow tracker), and a number of Fed speakers.

- Bunds are modestly lower. Slipped earlier doors, hit marginally by TSMC’s Q2 report and then more significantly when the name provided strong guidance for Q3 (see Equities) as the broad risk tone picked up. Over the early European morning, Bunds fell from the c. 129.60 level that they had been meandering around overnight to a 129.47 low before the European cash equity open and since to a 129.38 base. Supply from Spain passed without reaction as is usually the case, though the b/c for the 2048 line was weaker than normal. France, was strong overall though some modest pressure was seen in OATs on the results, potentially driven by the sub-3x b/c for the 2031 line.

- Gilts are underperforming. Hit at the open given the bearish bias from peers (see above), and also the morning’s jobs data. In brief, the series showed that the labour market is continuing to weaken with the Unemployment Rate unexpectedly ticking higher and another negative print for the HMRC Payrolls Change. However, this is caveated by a significant revision to the prior HMRC figure. Opened at 91.33, 20 ticks below yesterday’s close, and then slipped further to a 91.14 trough. No move seen on the DMO’s 2030 sale, results broadly in-line with the last outing.

- Spain sells EUR 5.7bln vs exp. EUR 5.0-6.0bln 2.70% 2030, 3.20% 2035 & 2.70% 2048 Bono.

- France sells EUR 12bln vs exp. EUR 10-12bln 2.40% 2028, 2.50% 2030 and 2.70% 2031 OAT.

- UK sells GBP 4.75bln 4.375% 2030 Gilt: b/c 3.12x (prev. 3.26x), average yield 4.078% (prev. 4.06%) & tail 0.2bps (prev. 0.2bps)

- Click for a detailed summary

COMMODITIES

- WTI and Brent are trading on either side of the unchanged mark, but have held a negative bias throughout the European morning, up until a geopolitical update. Al Arabiya reported of a drone attack on the Taouki oil field (80k bpd) in Iraq’s Kurdistan region. An update which has lifted the crude benchmarks more concertedly into the green, albeit did respect earlier highs. Brent Sept’25 currently trades around USD 68.50/bbl in a USD 68.34-69.01/bbl range, which is well within the prior day’s confines.

- Precious metals are broadly in the red, with losses all generally to a similar extent as each other. Spot gold traded rangebound overnight, finding some footing after extending higher on Wednesday amid reports that US President Trump would fire Chair Powell. This morning, the yellow-metal has traded with a downward bias thanks to the firmer Dollar and positive risk-tone across European equities. Currently in a in a USD 3,325.10-3,351.11 range.

- Base metals hold a negative bias, in part due to the firmer Dollar. 3M LME Copper posts very mild losses, in continuation of the rangebound trade seen overnight amid the somewhat mixed risk appetite in APAC trade. 3M LME Copper is incrementally in the red and trades in a USD 9,593.05-9,643.9/t range.

- Qatar set August-loading Al-Shaheen crude term premium at USD 2.48/bbl and raised September Al-Shaheen crude term price to USD 3.33/bbl above Dubai quotes, according to sources cited by Reuters.

- "March attack targeting the Taouki oil field in the Kurdistan Region of Iraq", via Al Arabiya.

- Indian oil minister sees potential for fuel price cuts if crude remains at current levels for next 2-3 months.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK ILO Unemployment Rate (May) 4.7% vs. Exp. 4.6% (Prev. 4.6%); Employment Change (May) 134k vs. Exp. 46k (Prev. 89k)

- UK Avg Wk Earnings 3M YY (May) 5.0% vs. Exp. 5.0% (Prev. 5.3%, Rev. 5.4%); Ex-Bonus (May) 5.0% vs. Exp. 4.9% (Prev. 5.2%, Rev. 5.3%)

- UK HMRC Payrolls Change (Jun) -41k (Prev. -109k, Rev. -25k); Claimant Count Unem Chng (Jun) 25.9k (Prev. 33.1k, Rev. 15.3k)

- EU HICP Final YY (Jun) 2.0% vs. Exp. 2.0% (Prev. 2.0%); HICP-X F&E MM (Jun) 0.3% (Prev. 0.1%).

NOTABLE EUROPEAN HEADLINES

- Pantheon Macro, on the UK labour market data, "So we shift our call. We now look for a one-and-done cut in August. We are still torn.".

- Germany's VCI reports H1 production down 1% Y/Y. Sales decline 0.5% to EUR 107 bln. Producer prices remain flat Y/Y. VCI maintains 2025 outlook. Lack of orders continues to pose a significant challenge for the chemical industry amid ongoing market tension, with no signs of recovery emerging this year.

- Citi now expects the ECB to lower rates in September and December (vs. previous view of July and September).

NOTABLE US HEADLINES

- Fed's Williams (Voter) said current modestly restrictive monetary policy is appropriate and the current state of interest rate policy allows Fed time to analyse data, while he added that the tariff impact is modest so far but will increase over time and tariffs should boost inflation by one percentage point for the rest of 2025 into 2026. Furthermore, he said they will need to watch data to understand tariff impact he still needs to see more data before deciding what’s next for policy.

- US President Trump says would love if Fed Chair Powell resigns and noted it would disrupt markets if he removed Powell.

- US senate passes bill codifying some DOGE cuts, sending it to the house, according to Bloomberg.

- BofA Institute total card spending (w/e July 12th): +4.5% Y/Y (vs +0.2% June avg.); notes online retail saw largest Y/Y spending growth due to Prime Day timing shift.

- US lawmakers are introducing a bill to nearly double the number of export control officers stationed around the world, according to Punchbowl. Punchbowl notes: "The bill comes during a heightened focus on export controls of American-made AI chips. While the Trump administration is relaxing some of those restrictions, many on Capitol Hill want to see a tougher approach regarding U.S. technology going to geopolitical rivals." The bill would mandate that there be at least 20 export control officers globally. There are currently 11 stationed in consulates across Asia, Europe and the Middle East.

- The Chinese government is reportedly threatening to block the sale of over 40 ports to BlackRock (BLK) and Mediterranean Shipping Co by CK Hutchinson (0001 HK), unless Cosco is an equal partner and shareholder, via WSJ citing sources.

GEOPOLITICS

MIDDLE EAST

- Senior US official said they are very close to an agreement that will lead to halting the escalation between Israel and Syria, according to Axios' Ravid.

- New US assessment finds US strikes destroyed just one Iranian nuclear site, according to NBC; strikes degraded two other sites. One of the three sites was mostly destroyed, setting work there back significantly. The two others were not as badly damaged and may have been degraded only to a point where nuclear enrichment could resume in the next several months if Iran wants it to. Officials believe the attack on Fordo, which has long been viewed as a critical component of Iran’s nuclear ambitions, was successful in setting back Iranian enrichment capabilities at that site by as much as two years, according to two of the current officials. Trump rejected a military plan for more comprehensive strikes that would have lasted for weeks.

RUSSIA-UKRAINE

- Russia's Deputy Chairman of the Security Council Medvedev says Russia should respond to West to full extent, with preventative strikes in needed, via Tass

- Russian air defence units downed two Ukrainian drones headed for Moscow, according to the city's mayor. It was also reported that Russian air defence systems destroyed 122 Ukrainian drones overnight, according to RIA.

- NATO's Top Military Commander Grynkewich says even if there is a peaceful solution in Ukraine, Russia will remain a threat.

OTHER

- China-linked hackers are increasingly targeting Taiwan's chip industry, according to cybersecurity firm Proofpoint.

CRYPTO

- Bitcoin is flat and trades just shy of the USD 119k mark whilst Ethereum outperforms following the US House advances crypto bills.

APAC TRADE

- APAC stocks were somewhat mixed following the two-way price action stateside where the major indices ultimately gained, although price action was choppy amid Fed independence concerns due to reports regarding a potential firing of Fed Chair Powell, which President Trump refuted.

- ASX 200 advanced with gains seen in nearly all sectors while stocks were unfazed by disappointing Australian jobs data.

- Nikkei 225 declined at the open amid currency- and data-related headwinds but gradually clawed back its losses as the JPY resumed its weakening trend.

- Hang Seng and Shanghai Comp lacked conviction in the absence of any pertinent fresh macro catalysts.

DATA RECAP

- Japanese Trade Balance (JPY)(Jun) 153.1B vs. Exp. 353.9B (Prev. -637.6B, Rev. -638.6B)

- Japanese Exports YY (Jun) -0.5% vs. Exp. 0.5% (Prev. -1.7%); Imports 0.2% vs. Exp. -1.6% (Prev. -7.7%)

- Australian Employment (Jun) 2.0k vs. Exp. 20.0k (Prev. -2.5k)

- Australian Full Time Employment (Jun) -38.2k (Prev. 38.7k); Unemployment Rate 4.3% vs. Exp. 4.1% (Prev. 4.1%)