US Market Open: Stocks gain, USD softer & USTs firm ahead of Fed’s Waller and earnings

18 Jul 2025, 11:00 by Newsquawk Desk

- Fed's Waller says they should cut by 25bps at the July meeting and thereafter adjust meeting-by-meeting.

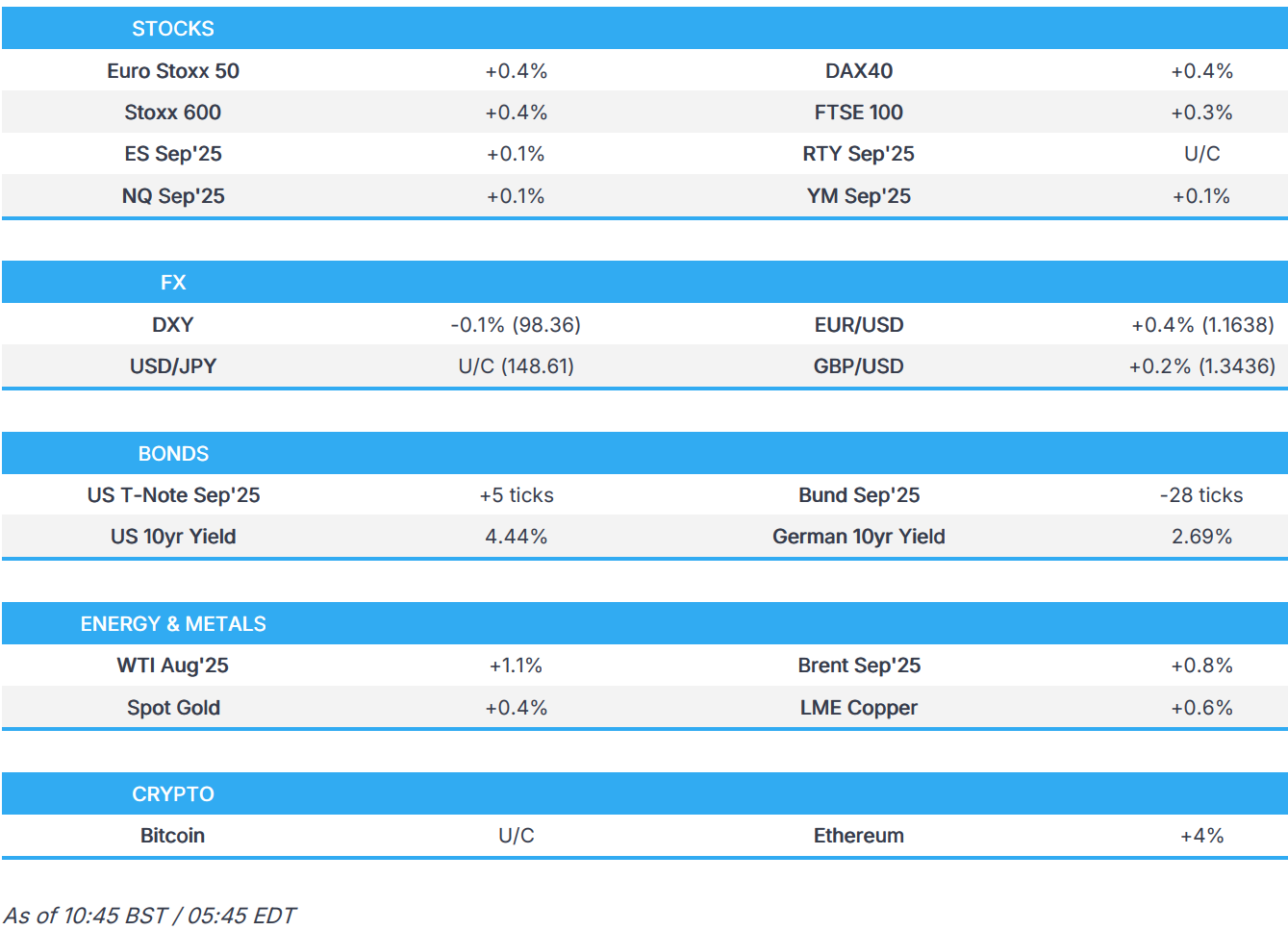

- European bourses are modestly higher whilst US futures take a breather following recent strength.

- USD a touch softer but still very much up on the week; Antipodeans benefit from the risk tone.

- USTs are firmer whilst Bunds underperform given the positive risk tone.

- Base metals bolstered by the risk tone, precious metals benefit despite this but remain in familiar territory.

- Looking ahead, US Building Permits/Housing Starts, UoM prelim, G20 Finance Ministers Meeting, Speakers include Fed's Waller. Earnings from 3M, American Express, Charles Schwab.

TARIFFS/TRADE

- China Commerce Minister Wang said China and US economic and trade relations have gone through storms and remain important to each other, while he added the US has adopted more unilateral, protectionist measures since 2018, provoking frictions and that decoupling is doomed to fail as it contradicts economic development. Wang stated that mutual benefit is the essence of US-China commercial ties, as well as noted that ups and downs have taught both sides that there are things they need from each other. Wang also commented that differences and frictions are inevitable but dialogue and consultation are the best way to fix problems, and the key is to respect each other’s core interests and major concerns. Furthermore, he said China still faces high US tariffs and that overall tariffs are in excess of 50%, while China wants to bring China-US commercial ties back to a state of healthy, sustainable development.

- Canada's International Trade Minister said they are getting officials to talk to Chinese counterparts as soon as possible to work through trade challenges, while the official also commented that there is appetite from both sides to have conversations with Mercosur and there seems to be energy to get things done quickly with ASEAN countries.

- Canada said it reached a mutually satisfactory solution with New Zealand to resolve the CPTPP dairy TRQs dispute, while a dairy agreement with New Zealand will result in minor policy changes to Canada's TRQ administration and does not amend Canada's market access commitments.

- Brazil's President Lula said regarding US tariffs that Brazil always has been open to dialogue, as well as stated that trying to interfere in the Brazilian justice is a serious attack on Brazilian sovereignty and that Trump’s letter about tariffs was unacceptable blackmail. Furthermore, he said the defence of Brazil’s sovereignty also applies to the operation of digital platforms in the country. In relevant news, US President Trump posted a letter to former Brazilian President Bolsonaro voicing sympathy and said he will be watching Brazil closely.

- Japanese Trade negotiator Akazawa says he discussed "various things" with US Treasury Secretary Bessent. Asked Bessent to vigorously continue discussions. Was friendly.

EUROPEAN TRADE

EQUITIES

- European bourses began the day with gains after constructive APAC and US sessions, and have since extended, helped by strong quarterly reports, mostly from Scandi-listed companies.

- European sectors opened almost entirely in the green, and retain this bias. The only sector in the red is Healthcare, which has been dragged lower by GSK (-6%) after Blenrep failed to win FDA panel support. Energy tops the pile, lifted by Vestas (broker upgrade) and BP (sold LS Power).

- US equity futures (ES +0.1% NQ +0.1% RTY U/C) are mixed/flat, paring from the upside seen in the prior session where the S&P 500 and Nasdaq 100 hit record highs.

- Netflix (NFLX) topped Q2 profit and sales expectations, and it raised its FY sales and margin view, citing strong performance despite broader media industry cutbacks. Shares, however, slipped in afterhours trading, as the company flagged content expense rises in Q3 and Q4. It reported Q2 EPS of 7.19 (exp. 7.05), Q2 revenue USD 11.08bln (exp. 11.04bln). Netflix said ad sales momentum is strong, and US upfront deals are nearly complete. Expects H2 2025 operating margin to be lower than H1.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is a touch softer but still up some 0.6% on the week and higher for a second week in a row. The drivers for the USD upside have been a combination of resilient US data, expectations that a tariff compromise will be reached between the US and global trading partners, inflation that will limit near-term Fed easing and the market pulling back from being overly short the dollar. DXY is back below its 50DMA and towards the bottom end of Thursday's 98.33-95 range.

- EUR/USD is attempting to recoup some lost ground vs. the USD after hitting a MTD low on Thursday at 1.1555. Price action for EUR/USD this week has largely been at the whim of the USD. EUR/USD has made its way back onto a 1.16 handle and is eyeing Thursday's best at 1.1642.

- JPY is flat vs. the USD as the ongoing rally in USD/JPY pauses for breath. Japanese inflation metrics overnight printed in-line and provided little traction for JPY with greater attention on this weekend's upper house elections. USD/JPY has moved back onto a 148 handle and trades in a 148.30-88 range vs. the multi-month high printed on Wednesday at 149.18.

- GBP is firmer vs. the broadly weaker USD with incremental drivers from the UK light today. Focus in the UK this week has been on the data slight with hot inflation data on Wednesday and soft labour market data on Thursday underscoring the market narrative that, whilst the BoE is expected to keep easing policy in the coming months, they are unlikely to accelerate their current quarterly pace of rate cuts.

- Antipodeans are outperforming alongside the mostly positive risk appetite and recent rebound in commodity prices.

- PBoC set USD/CNY mid-point at 7.1498 vs exp. 7.1736 (Prev. 7.1461).

- Citi upgrades USD to Neutral from Underweight.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are trading higher by a handful of ticks today and currently within a 110-19 to 110-24 range and trading towards the peak from Thursday at 110-25. Focus has been on commentary from the influential Fed Governor Waller; he continued to bolster his calls for a 25bps cut in July; he is set to talk later today also. Elsewhere, on trade updates, the White House said the EU continues to be very eager in trade negotiations. Elsewhere, on US/China relations, US is set to impose a 93.5% tariff on graphite used for battery material from China. Attention now turns to US Housing Starts/Building Permits and UoM Prelim data.

- Bunds have traded with a downward bias throughout the morning, and are the underperformer today. Nothing fundamentally driving the pressure today, but perhaps just a function of the relatively positive risk tone. Currently trading towards the bottom end of a 129.53 to 129.82 range. Further pressure may see a dip below 129.50 and then towards Thursday’s low at 129.38. Newsflow and data docket has been relatively light so far; some focus on German Producer Prices, whereby the Y/Y figure printed in-line with expectations whilst the M/M component ticked higher from the prior and came in a touch above expectations.

- Gilts are in the red, following EGBs, albeit to a lesser extent. Like above, downside today stems from the positive risk tone rather than any specific newsflow driven action. Trading in a tight 91.15 to 91.31 range, and currently just off the day’s trough. Today’s trough is a single tick above Thursday’s low, which also marks the WTD base.

- Click for a detailed summary

COMMODITIES

- Crude rallied from the early European morning, got as high as USD 68.53/bbl and USD 70.40/bbl for WTI and Brent. Newsflow at the time was fairly light, price action largely a continuation of Thursday’s upside (spurred by further drone attacks on refineries in the Middle East) and following the general risk tone, which remains underpinned after Thursday’s very strong US session. Newsflow this morning has been focussed on the latest EU sanctions package. A package which, as expected, includes a new lower Russian oil price cap. The cap will now by dynamic, set USD 15/bbl below market rates (prev. set at USD 60.0/bbl) and begin in the USD 45-50/bbl range as a starting point.

- Most recently, the complex has taken another leg higher and is approaching earlier peaks, no fresh fundamental driver behind the move.

- Gold is bid after climbing gradually through the latter-half of Thursday’s session despite the strong risk tone. Upside that was potentially driven by the softer yield environment, which in turn was possibly driven by Import Price data and remarks from former Fed official Warsh. The metal then picked up a little further overnight to a USD 3350.44/oz peak. Upside that comes in contrast to the mostly firmer APAC risk tone, with China largely shrugging off the latest unfavourable tariff updates.

- 3M LME Copper is following the risk tone, posting notable gains pretty much across the board thus far. This has taken it to a USD 9.75k peak and to a fresh high for the week.

- Asian refiners are reportedly increasing purchases of Kazakh CPC crude for August loadings amid lower European demand pressuring prices, according to Reuters citing traders.

- Click for a detailed summary

NOTABLE DATA RECAP

- German Producer Prices MM (Jun) 0.1% vs Exp. 0.0% (Prev. -0.2%); YY -1.3% vs. Exp. -1.3% (Prev. -1.2%)

NOTABLE EUROPEAN HEADLINES

- Dutch Finance Minister Heine says the EU's MFF proposal for just under EUR 2.0tln is "dead on arrival".

- Morgan Stanley expects BoE to hold rates steady in September, revising previous forecast for a cut.

- BofA expects the BoE to cut rates twice this year, in August and November, vs prev. exp. August, September and November Expects the bank to deliver cut in February 2026, taking terminal rate to 3.5%

- ECB's Nagel says financial markets speak their own language and are showing how Fed attacks affect them.

NOTABLE US HEADLINES

- Fed Chair Powell sent a response to questions from OMB Director Vought in which he stated the Fed Board believes transparency is of the utmost importance and cited ongoing reviews including by the Inspector General of the project since it began in 2017, while he added that collaboration with National Capital Planning Commission has been constructive and robust, but was voluntary on the part of the Fed. Powell said changes since the NCPC approval were to scale back and simplify construction and added no new elements, with no further review warranted.

- Fed's Waller (voter) said the Fed should cut interest rates by 25bps at the July meeting and rising risks to the economy favour easing the policy rate, while he added that if underlying inflation remains in check and growth tepid, more cuts are needed. Waller stated the Fed should not wait until the labour market hits trouble before cutting rates and delaying cuts runs the risk of needing more aggressive action later. Furthermore, he said a July rate cut could give the Fed space to hold rates for a few meetings and noted they should cut rates in July and then adjust policy meeting by meeting, as well as commented that data should determine the pace of rate cuts and there's nothing wrong with taking out an insurance rate cut, just in case.

- White House said President Trump signed an executive order creating a new classification of non-career federal workers and signed four proclamations, granting two years of regulatory relief from Biden-era regulations impacting sectors vital to security. Furthermore, the proclamations cover coal plants, taconite iron ore processing facilities, and certain chemical manufacturers that produce chemicals related to semiconductors, medical device sterilisation, and national defence systems.

- US President Trump is set to open the US retirement market to crypto investments with Trump preparing an executive order to allow 401k plans to tap a broad pool of alternative assets, according to FT.

GEOPOLITICS

- Qatar, Egypt, and the US presented Israel and Hamas with an updated Gaza ceasefire and hostage deal proposal on Wednesday, according to Axios.

- Iran is moving to rearm its militia allies and is sending missiles to Hezbollah, while it seeks to smuggle weapons from Iraq to Syria and is moving quickly to replenish Houthi weapons stockpiles after US-Israeli strikes, according to WSJ.

- French, German and UK Foreign Ministers and the EU high representative held a call with the Iranian Foreign Minister with an aim to relaunch talks on Iran's nuclear programme, while E3 ministers told Iran's Foreign Minister to return to the diplomatic pathway immediately to reach a verifiable and lasting nuclear accord, as well as stressed again their determination to reimpose UN sanctions on Iran if no concrete progress is made towards a nuclear accord by the end of summer.

- EU Foreign Representative Kallas says the EU has just approved one of its strongest sanction packages against Russia to date. Europe will continue to increase pressure on Russia until the war concludes. Includes a lower Russian oil price cap.

- Iranian Foreign Minister says any new round of negotiations will only be possible if the other side expresses its readiness for a fair and balanced nuclear agreement, according to Sky News Arabia.

- Ukrainian President Zelensky says the negotiation process with Russia requires "more momentum", assigned Umerov to the National Security Council.

CRYPTO

- Bitcoin is flat, whilst Ethereum outperforms and sits above the USD 3.6k mark; XRP has been soaring over the past couple of days, notching fresh ATHs overnight.

APAC TRADE

- APAC stocks were predominantly higher following the positive handover from Wall St where the S&P 500 and Nasdaq 100 rose to fresh record highs with sentiment underpinned by better-than-expected data.

- ASX 200 outperformed its regional peers and climbed to a fresh all-time high as advances were led by the Mining, Materials and Resources sectors with the former helped by gains in BHP following its Q4 production update and with Novonix shares up around 20% on plans to boost US graphite production as the US sets 93.5% anti-dumping duties on Chinese graphite.

- Nikkei 225 failed to sustain a brief return above the 40,000 level and pared its opening gains amid cautiousness heading into the upper house election on Sunday with Japan facing political uncertainty should the ruling coalition fail to retain its majority in the House of Councillors.

- Hang Seng and Shanghai Comp were underpinned in tandem with the gains across most of the Asia-Pac region and as participants shrugged off reports that the US is setting a 93.5% anti-dumping duty on graphite from China and that China threatened to block the Panama Ports deal unless its shipping giant COSCO is part of it.

NOTABLE ASIA-PAC HEADLINES

- China's Cyberspace Administration said China and the EU agreed to set up a working team to cooperate on bilateral cross-border flows of autodata.

- Japan's PM Ishiba to hold press conference at 06:00BST on Monday following upper house elections.

DATA RECAP

- Japanese National CPI YY (Jun) 3.3% vs Exp. 3.3% (Prev. 3.5%)

- Japanese National CPI YY Ex. Fresh Food (Jun) 3.3% vs Exp. 3.3% (Prev. 3.7%)

- Japanese National CPI YY Ex. Fresh Food & Energy (Jun) 3.4% vs Exp. 3.4% (Prev. 3.3%)