US Market Open: RTY outperforms & bonds boosted after Japan’s LDP-led coalition loses its Upper House majority

21 Jul 2025, 10:50 by Newsquawk Desk

- Japanese PM Ishiba vowed to stay on despite exit polls from the election showing that the ruling coalition lost its majority.

- EU envoys are set to meet as early as this week to formalise a retaliation plan in the event of a possible no-deal scenario with the US, according to Bloomberg.

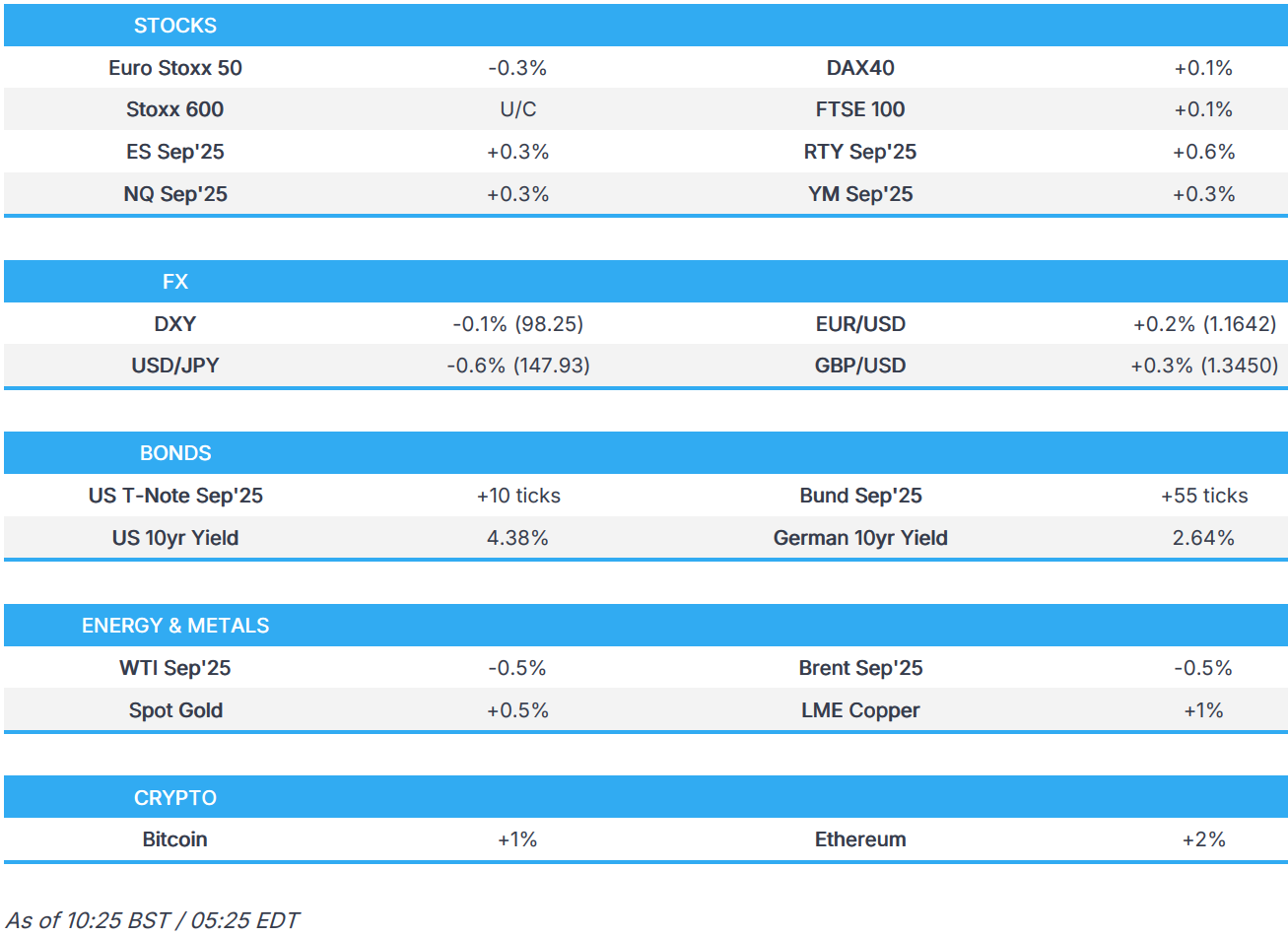

- European bourses are modestly lower, US equity futures are higher with outperformance in the RTY.

- JPY leads post-election, DXY trundles lower, EUR awaits trade updates.

- Bonds are boosted after PM Ishiba loses Upper House majority, but not as bad as feared.

- Choppy trade in crude while base metals are underpinned by China's dam construction

- Looking ahead, Canadian Producer Prices, US Leading Index Change, BoC SCE, NZ Trade Balance, Earnings from Verizon, Domino's Pizza & Cleveland Cliffs.

TARIFFS/TRADE

- US Commerce Secretary Lutnick said he is confident they will get a deal done with the EU, while Lutnick said that President Trump is ‘absolutely’ going to renegotiate the USMCA.

- EU envoys are set to meet as early as this week to formalise a retaliation plan in the event of a possible no-deal scenario with US President Trump, according to Bloomberg.

- US State Department announced visa restrictions on Brazilian judicial officials including Supreme Court Justice Moraes and his allies in court, as well as their immediate family members. It was later reported that Brazilian President Lula said US visa restrictions on Brazilian officials are another arbitrary and baseless move by the US government, while he added that interference by one country in another’s justice system is unacceptable. Furthermore, Lula said this violates the basic principles of respect and sovereignty between nations and no form of intimidation or threat from anyone will undermine Brazil’s powers and institutions' mission to preserve democracy.

- Japanese PM Ishiba said he will tackle US tariff issues before the August 1st deadline and they cannot give up the negotiation bases they’ve built through US tariff talks, while he added that tariff negotiator Akazawa is to visit the US on Monday.

- Japanese tariff negotiator Akazawa said he will visit the US this week and they are making arrangements for ministerial-level tariffs talks with the US to take place this week, while he also noted that he did not discuss tariffs with US Treasury Secretary Bessent on Saturday.

- South Korea's Industry Ministry said US tariff negotiations are in a serious situation and it pledged an all-out effort to smoothly wrap up US tariff talks.

- China's Commerce Ministry commented regarding Chinese firms being sanctioned, stating that the EU's actions have a serious negative impact on China-EU economic and trade relations and financial cooperation, while it will take necessary measures to resolutely safeguard the legitimate rights and interests of Chinese enterprises and financial institutions.

JAPANESE UPPER HOUSE ELECTION

- Results, according to NHK, have the LDP-Komeito coalition securing 47 seats and losing the Upper House majority (50 were required).

- Since, PM Ishiba has reiterated that he will remain as PM and the LDP will continue to govern with Komeito. Need to stay in office to deal with tariff talks, rising prices, and economic issues. Opposition proposals to cut taxes would take too long, need quicker action to help struggling households. Seeking the cooperation of other parties to deal with increasing prices. Will not expand the formal government coalition.

- Earlier, exit polls showed the ruling coalition is likely to lose its majority in the upper house with the LDP and coalition partner Komeito projected to win a combined 32 to 51 seats out of a total of 125 seats contested, according to NHK. Thereafter, Japanese PM Ishiba vowed to stay on despite the exit polls from the election and stated he "solemnly" accepts the "harsh result" but noted his focus was on trade negotiations, according to the BBC.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.1%) opened mixed and on either side of the unchanged mark. Though as the morning progressed, sentiment waned a touch to display a modestly negative picture in Europe.

- European sectors are mixed. Travel & Leisure was buoyed by post-earning upside in Ryanair (+5%); the Co. beat on its headline metrics and noted that Q2 demand is strong. Elsewhere, more bad news for Autos which is pressured by losses in Stellantis (-2.5%) after the Co. reported significant net losses.

- US equity futures (ES +0.3% NQ +0.3% RTY +0.7%) are modestly firmer across the board, ahead of a week which includes earnings from the likes of Alphabet and Tesla.

- Deutsche Bank turns Neutral from Overweight on European equities vs US equities.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD has kicked the week off on a slightly softer footing with DXY hampered by JPY strength (see JPY section for details). Macro drivers from the US have been quiet over the weekend and this could remain the case in the near-term with the Fed in its blackout period and this week's data slate a light one aside from housing metrics on Wednesday and Thursday and flash PMI data. There was a WSJ piece over the weekend suggesting that US Treasury Secretary Bessent reportedly advised US President Trump not to fire Fed Chair Powell. As it stands, the next Fed cut is not fully priced until October with a total of 47bps of loosening seen by year-end. DXY is contained within Friday's 98.09-57 range.

- EUR is firmer vs. the USD in what could be a busy week for the bloc. Focus remains on the trade front with Bloomberg reporting that EU envoys are set to meet as early as this week to formalise a retaliation plan in the event of a possible no-deal scenario with the US. Though, US Commerce Secretary Lutnick said he is confident they will get a deal done with the EU. Additionally, EU's von der Leyen and Costa are to visit China and meet with President Xi and co-chair the 25th China-EU summit.

- JPY is the best performing currency in the aftermath of the Japanese Upper House election. Exit polls showed that the LDP-Komeito coalition failed to secure the 50 seats required to retain a majority. A result that means PM Ishiba no longer controls a majority in the Upper or Lower Houses. Despite this, Ishiba has made clear he intends to remain PM - something which has been viewed as a positive by the market. Additionally, ING noted that opposition parties are very splintered and have little chance of coming together as a political force. As such, some of the worst fears of the outcome may have been avoided and therefore are driving the JPY strength. USD/JPY briefly made its way onto a 147 handle with a session low at 147.79.

- GBP is marginally firmer vs. the USD after an indecisive week last week which saw the UK leg of the pair focused on the data slate (CPI and Jobs metrics). Weekend reporting over the UK has been light with not much traction from the latest Rightmove house price data, which showed the largest M/M decline since records began in 2001. Cable remains on a 1.34 handle and around the mid-point of Friday's 1.3405-75 range.

- Antipodeans are lacklustre with mild headwinds seen in NZD following the softer-than-expected CPI data from New Zealand.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Bonds are in the green today and generally trading near session highs, with the complex seemingly boosted by 1) PM Ishiba losing Upper House majority, but better than feared, 2) EU-US trade fears (details below).

- PM Ishiba's LDP-Komeito lost their Upper House majority. Going into the election, Japanese bonds were heavily sold, given the fiscal implications of PM Ishiba losing Upper House majoirty. Overall, his coalition secured 47 seats, which was a better outcome than some polls had suggested, which would therefore would mean Ishiba only needs to secure a handful of additional votes and thus may be able to avoid making very significant concessions. With cash JGB trade shut for the day, the upside across global fixed income could be attributed to some short covering, with the result not quiet as bad as feared.

- USTs are higher by around 10 ticks today, and currently trades towards the upper end of a 110-24 to 111-04 range. Japan aside, nothing really US-specific driving the move, with the docket for the remainder of the day fairly light. On the ongoing Trump-Powell spat, US Treasury Secretary Bessent reportedly advised US President Trump not to fire Fed Chair Powell, may also explain some of the upside.

- Bunds are also stronger today and trades just off the day's high at 130.09, in a current 129.73-130.14 range. Ultimately following peers, but for the EU specifically, US Commerce Secretary Lutnick said he is confident they will get a deal done with the bloc; though Bloomberg reported that EU envoys are set to meet as early as this week to formalise a retaliation plan in the event of a possible no-deal scenario. Elsewhere, the ECB’s latest SAFE showed a drop in one year inflation expectations to 2.5% (prev. 2.9%), while the 3yr and 5yr views were maintained.

- Gilts also firmer today, but to a lesser degree than European peers. Currently trades in a 91.29-55 range, in what has (and will remain to be) a quiet day. Focus for the remainder of the week on PMIs (Thu) and Retail Sales (Fri). One piece of notable newsflow over the weekend came via The Telegraph, who report that the government is looking at the creation of a “crypto storage and realisation framework” to manage and potentially sell seized assets.

- Click for a detailed summary

COMMODITIES

- WTI and Brent are currently trading in negative territory, after trading rangebound overnight. Energy specific newsflow light over the weekend, with more focus on geopolitical updates. Iran confirmed that nuclear talks with France, Germany and the United Kingdom will be held in Istanbul on Friday; China and Russia will holds talks with Iran on Tuesday. Brent Sept'25 currently trading in a USD 69.08-63/bbl range.

- Spot gold is modestly firmer today and trades towards the upper end of a USD 3,338.03-3,370.87/oz range. Firmer alongside upside across global havens and also benefiting from the slightly softer Dollar.

- Base metals are broadly in the green today, with the complex boosted after China launched the construction of hydropower project in Tibet, which has significantly boosted iron ore and steel prices; the former rose to a multi-month high, with Dalion iron ore closing higher by 2.1%. Meanwhile, 3M LME copper trades +1% at the time of writing, in a USD 9,766.30-9,891.00/t range.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Rightmove House Prices MM (Jul) -1.2% (Prev. -0.3%); YY 0.1% (Prev. 0.8%)

NOTABLE EUROPEAN HEADLINES

- London Stock Exchange Group (LSEG LN) considers the launch of 24-hour trading, according to FT.

- UK pensions overhaul looms as pension minister Bell warns of a slump in retirement income, while he noted the government would revive the Pensions Commission that heralded sweeping changes under the Blair Labour government in the early 2000s and argued that reforms were only “a job half done”, according to FT.

- EU reportedly cracks down on state meddling in bank M&A as it recently issued warnings last week against meddling by the Italian and Spanish governments in banking tie-ups, according to the FT.

- EU is to force car rental companies to purchase EVs only from 2030, according to Bild.

- ECB Survey: Firms' 1-year ahead inflation expectation 2.5% (prev. 2.9%), 3-year and 5-year unchanged at 3.0% "Most firms affected by trade tensions," especially manufacturers and companies exporting to the US, are highly exposed to trade issues. A net 23% of firms are optimistic about developments in the next quarter but report a deterioration in their profits.

- Germany reportedly intends to reverse the increase in air traffic tax, according to Bild.

NOTABLE US HEADLINES

- China's Foreign Ministry says, on the Wells Fargo (WFC) bankers exit ban, that Ms Mao is involved in a criminal case and is temporarily unable to leave China.

GEOPOLITICS

MIDDLE EAST

- Iran and three European countries reached an agreement to resume nuclear talks, while an Iranian Foreign Ministry spokesperson said Iran and three European powers are to hold nuclear talks in Istanbul on Friday.

- Israel issued an evacuation order for Deir al-Balah in central Gaza as it prepared to extend a Gaza offensive to areas not yet reached by ground forces.

- Israel prepared a plan to control the Gaza Strip as an alternative to the idea of a humanitarian city, with the plan widely accepted among Israeli ministers and will be implemented if the Gaza negotiations fail, according to sources cited by Channel 12.

- Israel’s military said it operated to disperse a violent gathering involving Israeli citizens across the border with Syria.

- Syrian Presidency announced an immediate and comprehensive ceasefire, while it urged all parties to commit to a ceasefire and end all hostilities in all areas immediately. Furthermore, the Syrian Interior Ministry said the city of Sweida was cleared of Bedouin tribes fighters and clashes were halted after Syrian security forces were deployed to enforce a ceasefire.

- "A senior Iranian lawmaker warned on Monday that Tehran could halt its regional maritime security cooperation, including in the Strait of Hormuz, if European powers move to reimpose UN sanctions through the so-called snapback mechanism", via Iran Int.

- "Israeli Army Radio: Raids begin on Houthi positions in Hodeidah and the western coast", via Al Hadath.

- Iranian Foreign Ministry spokesperson says trilateral meeting with China and Russia to be held on Tuesday regarding nuclear file and UN snapback mechanism; no plans for talks with the US at the moment.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said a Russian attack damaged critical infrastructure in the Sumy region, while it was separately reported that Zelensky said Kyiv sent Moscow an offer to hold talks next week.

- Russian President Putin met with senior advisers to Iran’s Supreme Leader in the Kremlin, according to RIA.

- Kremlin spokesman said Russian President Putin repeated his desire to bring the Ukrainian settlement to a peaceful conclusion as soon as possible but it is a long and difficult process, while Russia is ready to move fast on Ukraine peace but the main thing is to achieve the goals which have not changed.

- Russian Defence Ministry said Russian forces took control of Bila Gora in eastern Ukraine, according to RIA.

OTHER

- South Korean Unification Ministry spokesperson commented that the government is looking into various plans to improve relations with North Korea, regarding a report of South Korea potentially allowing tourism to North Korea.

CRYPTO

- Bitcoin a little firmer today and trades around USD 118k.

APAC TRADE

- APAC stocks began the week mostly in the green but with gains capped following relatively light macro catalysts from over the weekend, aside from Japan's upper house election with the ruling coalition set to lose a majority, although markets in Japan were shut for a holiday.

- ASX 200 retreated with the index dragged lower by underperformance in its top-weighted financial sector, while miners were showing some resilience as South32 gained following its quarterly and full-year production update.

- Hang Seng and Shanghai Comp were kept afloat amid strength in tech and energy stocks, while China's LPRs were unsurprisingly maintained and there were also recent reports that US President Trump could meet with Chinese President Xi ahead of or during the October APEC meeting in South Korea.

NOTABLE ASIA-PAC HEADLINES

- Chinese Loan Prime Rate 1 Year (Jul) 3.00% vs. Exp. 3.00% (Prev. 3.00%); 5 Year 3.50% vs. Exp. 3.50% (Prev. 3.50%)

- US President Trump and Chinese President Xi could meet ahead of or during the APEC summit in South Korea.

- Chinese Foreign Ministry said European Commission President von der Leyen and European Council President Costa will visit China on July 24th and will meet with President Xi, while Chinese Premier Li will co-chair the 25th China-EU summit with the EU presidents.

DATA RECAP

- New Zealand CPI QQ (Q2) 0.5% vs. Exp. 0.6% (Prev. 0.9%); YY 2.7% vs. Exp. 2.8% (Prev. 2.5%)

- New Zealand RBNZ Sectoral Factor Model Inflation Index YY (Q2) 2.8% (Prev. 2.9%