Europe Market Open: Mixed, but relatively contained trade into numerous earnings

22 Jul 2025, 06:45 by Newsquawk Desk

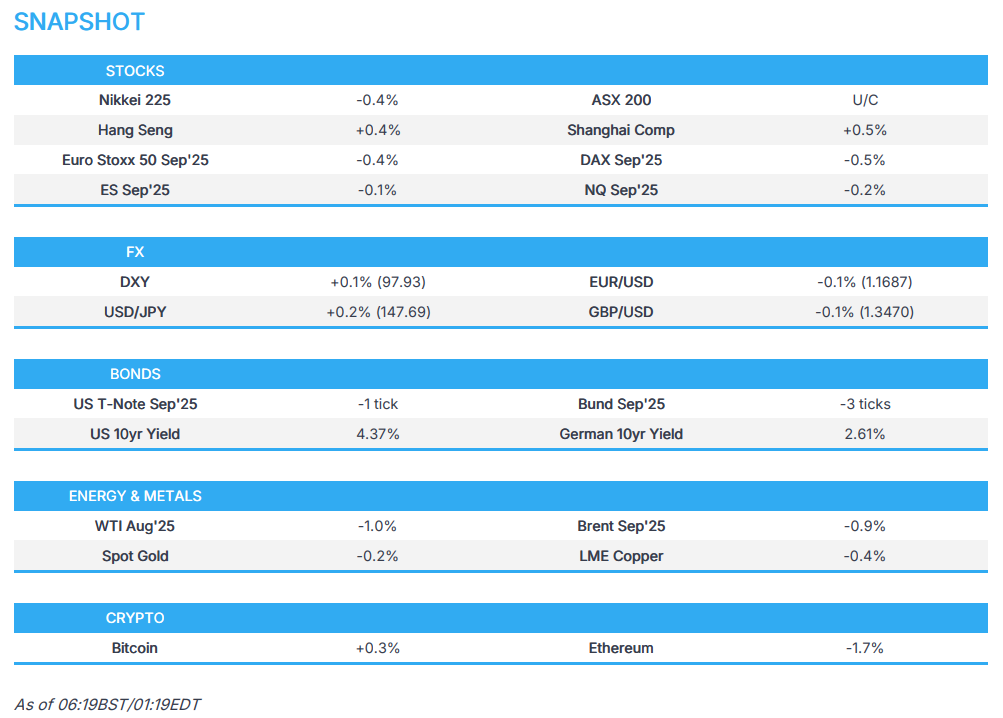

- APAC stocks traded mixed after failing to sustain the early upward momentum seen at the open following the fresh record intraday highs on Wall St.

- White House Press Secretary Leavitt said they could see more tariff letters for August 1st.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 future down 0.4% after the cash market finished with losses of 0.3% on Monday.

- DXY is steady, JPY is the marginal laggard as Japan returns from holiday, EUR/USD failed to hold onto the 1.17 handle.

- Looking ahead, highlights include US Richmond Fed Index, NBH Policy Announcement, Fed Chair Powell & Bowman, ECB’s Lagarde, BoE's Bailey, Supply from UK & Germany.

- Earnings from Akzo Nobel, ASM International, Dassault Aviation, Julius Baer, Lindt, SAP, Intuitive, Capital One, Baker Hughes, Coca Cola, Lockheed Martin, Philip Morris, RTX, DR Horton, Northrop Gruman, Danaher, MSCI & Pulte.

SNAPSHOT

US TRADE

EQUITIES

- US stocks saw two-way price action and ultimately finished mixed amid light pertinent catalysts and a quiet calendar to start the week. Nonetheless, there was mild outperformance in the Nasdaq owing to the gains in the heavyweight tech stocks, while the equal-weighted S&P (RSP) and the small-cap Russell 2000 were the laggards. Sectors were also mixed with notable strength seen in the communication sector and with health and energy at the other end of the spectrum.

- SPX +0.14% at 6,306, NDX +0.50% at 23,180, DJI -0.04% at 44,323, RUT -0.40% at 2,231.

- Click here for a detailed summary.

TARIFFS/TRADE

- White House Press Secretary Leavitt said they could see more tariff letters for August 1st.

- Canadian PM Carney issued a statement following a meeting with US Senators and stated they discussed work to strengthen continental defence and security, as well as Canada’s successes in dismantling illegal drug smuggling and securing the border.

- Canada's Minister of Intergovernmental Affairs Leblanc will be in Washington this week for trade discussions.

- Japan's tariff negotiator Akazawa and US Commerce Secretary Lutnick met for over two hours in Washington on Monday and held frank talks to seek agreement benefiting both Japan and the US, while Japan will continue to seek common ground on tariff issues with the US, according to the Japanese government.

- South Korean Finance Minister Koo said he will hold trade talks with his US counterpart on July 25th, while Koo added the Foreign Minister and Industry Minister will conduct meetings with US counterparts as soon as possible.

- India and US mini trade deal is ruled out before August 1st, according to CNBC TV18 citing sources.

- Malaysia has been asked by the US to extend tax exemptions for US EVs, while Malaysia is seeking a 20% US levy, but is said to be resisting EV and ownership demands, according to Bloomberg.

NOTABLE HEADLINES

- US Treasury Secretary Bessent said the Fed should conduct an exhaustive internal review of non-monetary policy operations and its decision to undertake massive building renovation at a time of operating losses should be reviewed.

- US CBO said the One Big Beautiful Bill will add USD 3.4tln to the deficit over a decade.

- SoftBank (9984 JT) and OpenAI's USD 500bln AI project struggles to get off the ground with the Stargate venture, introduced at a White House event earlier this year, now setting a more modest goal of building a small data centre by year-end, according to WSJ.

APAC TRADE

EQUITIES

- APAC stocks traded mixed after failing to sustain the early upward momentum seen at the open following the fresh record intraday highs on Wall St and with two-way price action seen in Japan following the ruling coalition's upper house election loss.

- ASX 200 was rangebound as strength in the mining, materials, resources and healthcare sectors offset the losses in financials, energy and industrials, while the RBA Minutes from the July meeting provided very little to shift the dial but continued to signal future cuts ahead.

- Nikkei 225 initially surged to above the 40,000 level as participants returned from the long weekend, but then wiped out its gains and then some, as participants second-guessed the ramifications of the ruling coalition's upper house election setback.

- Hang Seng and Shanghai Comp kept afloat in rangebound trade amid a lack of major fresh catalysts and after the Hong Kong benchmark breached the 25,000 level.

- US equity futures (ES -0.1%, NQ -0.2%) were little changed after the recent price swings amid a lack of drivers and as participants await upcoming key earnings releases.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 future down 0.4% after the cash market finished with losses of 0.3% on Monday.

FX

- DXY traded little changed overnight and got some respite from the prior day's selling pressure which dragged the DXY beneath the 98.00 level amid the softer yield environment in a session devoid of any major news catalysts or notable data releases and with the Fed in a blackout period. Note, the data calendar for the US remains light for the week, leaving the focus on the weekly jobless claims report and trade-related developments.

- EUR/USD proceeded sideways and held on to most of its recent spoils after having benefitted from the dollar's demise, although is off yesterday's best levels after failing to sustain the 1.1700 status. On the trade front, EU diplomats said the bloc is exploring a wider set of possible counter-measures against US tariffs and there were also comments by US Treasury Secretary Bessent that the EU have become more engaged and thinks they would want to negotiate faster.

- GBP/USD trickled lower from the 1.3500 mark but with the pullback limited amid quiet catalysts and ahead of comments from BoE Governor Bailey.

- USD/JPY rebounded off its lows but remained firmly beneath the 148.00 level after retreating yesterday alongside a weaker buck and with some solace in Japan provided by hopes of government stability following Japanese PM Ishiba's vow to remain in his post.

- Antipodeans were rangebound amid the lack of conviction in risk sentiment and after the RBA minutes provided very little incrementally and noted the majority agreed it was prudent to await confirmation on inflation slowdown before easing, although the Board agreed further rate cuts are warranted over time with focus on the timing and extent of easing.

- PBoC set USD/CNY mid-point at 7.1460 vs exp. 7.1635 (Prev. 7.1522).

FIXED INCOME

- 10yr UST futures took a breather after bull flattening in US trade despite light catalysts and with the Fed in a blackout period which likely puts the attention stateside on trade updates this week amid a relatively quiet data calendar, while on the fiscal situation, CBO estimated that Trump's Big Beautiful Bill will add USD 3.4tln to the deficit over a decade.

- Bund futures lingered around the prior day's highs after rallying north of the 130.00 level and with participants now looking ahead to today's Bund supply.

- 10yr JGB futures climbed higher and the curve marginally steepened as Japanese participants took their first opportunity to react to the ruling coalition losing its majority in the upper house, with the minority government facing pressure from opposition parties to cut taxes.

COMMODITIES

- Crude futures remained subdued after the prior day's lacklustre performance amid quiet newsflow and with a Ukraine-Russia meeting planned for Wednesday in Turkey.

- Iraq said Turkey seeks a broader energy agreement and has submitted a new draft deal, while Iraq will review and negotiate the new Turkish proposal to renew the energy pact and expand it into oil, gas, and electricity.

- Spot gold mildly pulled back after rallying yesterday to briefly above the USD 3,400/oz level alongside a softer dollar and lower yield environment.

- Copper futures lacked demand after the prior day's choppy mood and amid the overall mixed risk appetite in Asia-Pac trade.

CRYPTO

- Bitcoin was choppy overnight and tested the USD 117k level to the downside.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Kato said it was a tough upper house election result for the LDP and the government will take the outcome of the upper house elections seriously, while he added the government has repeated that sales tax cuts are not appropriate.

- RBA Minutes from the July meeting stated the Board agreed further rate cuts are warranted over time, while the focus was on the timing and extent of easing. The Minutes stated that the Board considered whether to leave rates at 3.85% or to cut by 25bps and a majority agreed it was prudent to await confirmation on inflation slowdown before easing, while the majority felt cutting rates three times in four meetings would not be cautious and gradual. The case for no change cited some data as inflation had been slightly firmer than expected, the job market had also not loosened as expected and there was less risk of a severe global downturn. Furthermore, members agreed monetary policy was modestly restrictive, though financial conditions had eased and it was difficult to know how far rates can fall before policy is no longer restrictive, so prudence is needed.

GEOPOLITICS

MIDDLE EAST

- Iran's Foreign Minister said Iran is open to talks with the US but not directly for now, while it was separately reported that Iran's Foreign Minister told Fox News they cannot give up Iranian enrichment.

- World Health Organisation's Tedros said WHO staff residence in Deir al Balah, Gaza, was attacked three times on Monday as well as its main warehouse, while he demanded the immediate release of the detained staff and protection of all its staff. Tedros said two WHO staff and two family members were detained although three were later released and one staff member remained in detention.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said the next Ukraine-Russia meeting is planned for Wednesday in Turkey.

- Netherlands will make a "substantial contribution" regarding the delivery of patriots to Ukraine, according to Dutch press.

OTHER

- US House lawmakers asked Microsoft (MSFT), Alphabet (GOOGL), Meta (META) and Amazon (AMZN) CEOs to answer if they have adequate safeguards to address concerns about China and Russia targeting submarine cables, according to a letter seen by Reuters.

EU/UK

NOTABLE HEADLINES

- UK Deputy PM Rayner is pushing for councils to be given new powers to tax tourists, despite opposition from Chancellor Reeves, according to The Telegraph.